AI Showdown During the Spring Festival

02/25 2026

02/25 2026

455

455

The Spring Festival of 2026 is destined to be a watershed in the history of artificial intelligence development in China.

While the entire nation is immersed in the festive atmosphere of reunion, red envelopes, and the Spring Festival Gala, a silent war is quietly unfolding.

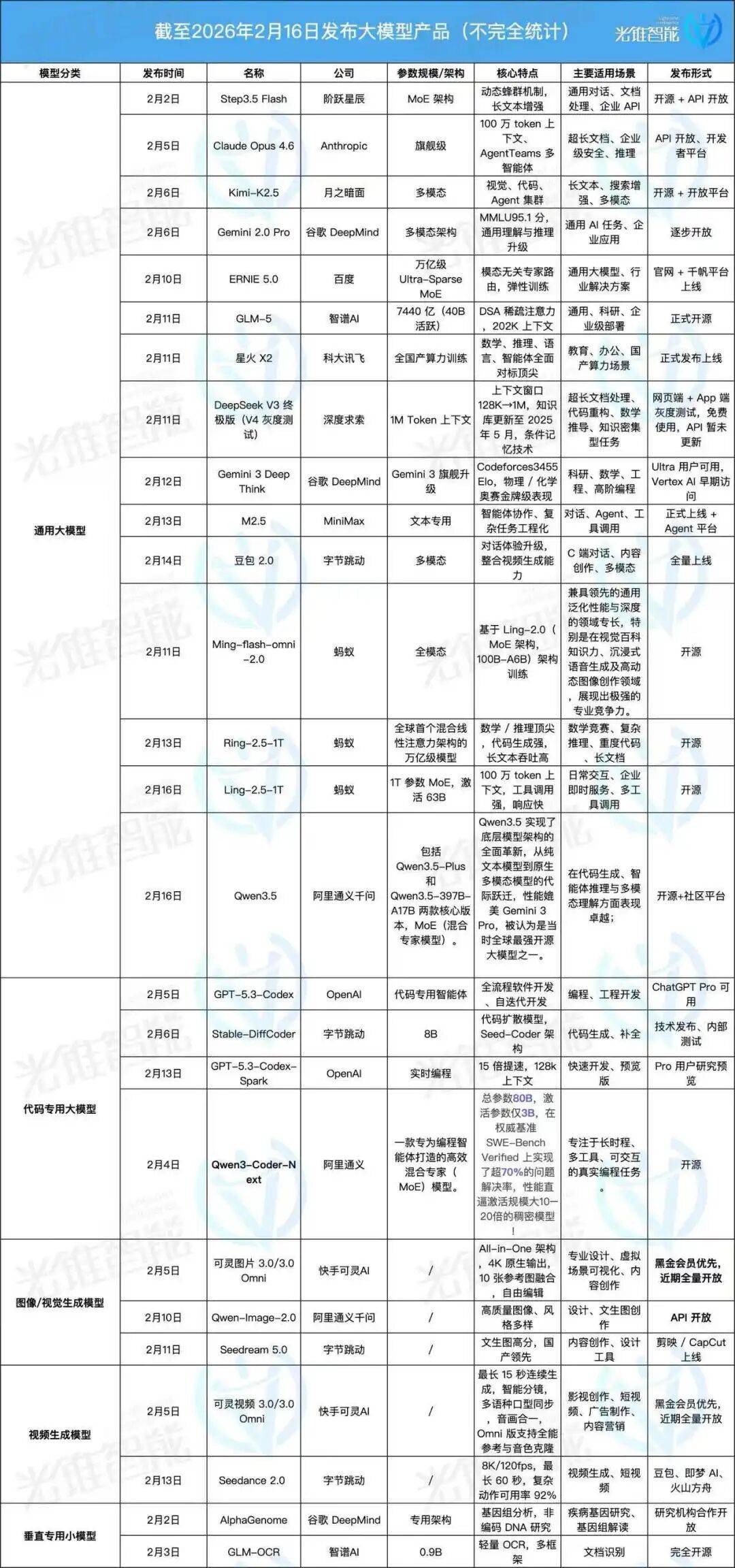

On one hand, from early February to New Year's Eve, the AI large model industry experiences an unprecedented wave of releases.

According to incomplete statistics, in just 15 days, more than 20 large model products have been launched across both domestic and overseas markets, covering five core sectors: general-purpose, code, image/visual generation, video generation, and vertical-specific applications.

On New Year's Eve itself, Alibaba quietly unveiled its latest large model, Qwen3.5, whose performance rivals top closed-source models like Gemini-3-pro and GPT-5.2.

Clearly, this unprecedented wave of releases has pushed the intensity of technological competition in AI large models to its peak. Beyond technology, a deep-seated competition for the "national-level AI gateway" is also fiercely underway.

Alibaba, Tencent, ByteDance, and Baidu have collectively invested nearly 5 billion yuan, deeply integrating AI with Spring Festival Gala interactions and red envelope features, truly staging a nationwide "AI popularization movement."

According to the diffusion of innovations theory, a new technology must cross the 14% penetration threshold to enter the mainstream.

By the end of 2025, mainstream AI products were nearing this critical point. The pulse-like traffic surge during the Spring Festival completed the final "national experiment": Doubao recorded a staggering 1.9 billion AI interactions on New Year's Eve, with 130 million people using Qianwen to say "help me" for the first time, and 5 billion commands input into the backend.

This Spring Festival AI application marketing battle has propelled general-purpose AI assistant products from occasional use to daily engagement.

The technological maturity of foundation models and the comprehensive boom in the application layer have ultimately reverberated through the capital market.

On the fifth day of the Lunar New Year (February 21), the first trading day of the Hong Kong stock market, Zhipu's stock surged by 42.72%, closing at HK$725 with a market capitalization exceeding HK$323.2 billion. MiniMax rose by 14.52%, closing at HK$970 with a market cap surpassing HK$304.2 billion.

In the primary market, reports suggest that the latest funding round for Yuezhiaimi values the company between $10 billion and $12 billion, meaning its market valuation has doubled in just over 40 days, soaring from $4.3 billion to the $10 billion club.

However, as publicly traded companies, Zhipu and MiniMax saw their market caps briefly surpass HK$300 billion before plummeting. By the close of trading on February 23, Zhipu fell by 22.76%, and MiniMax by 13.35%, with their combined market caps evaporating by nearly HK$100 billion.

Despite the volatility experienced by Zhipu and MiniMax, one thing is clear: around the 2026 Spring Festival, capital market valuations of Chinese AI enterprises began to align with those of overseas giants.

Behind this shift lies the validation of a new phase in the AI large model market during this year's Spring Festival: C-side popularization has opened up short-term growth space, while B-side penetration over the past year has laid the foundation for long-term value.

Undoubtedly, the 2026 Spring Festival marked a perfect logical closed loop of foundation model competition, application layer exuberance, and capital market fervor, propelling the Chinese AI market into a brand-new phase.

This year's "AI Spring Festival Battle" may appear lively on the surface, but underlying currents run strong. Ultimately, what remains will be a profound restructuring of the market landscape. Clearly, the leading players in China's AI large model sector have been established, both in terms of foundation models and the application layer.

AI Spring Festival Showdown: The Arms Race for Foundation Large Models

Technology continues to iterate rapidly, and the capabilities of AI large models have yet to reach their peak.

Since OpenAI released ChatGPT in early 2023, the Spring Festival period has become a coveted time window for AI companies.

Comparatively speaking, the density of this year's release wave has set a new record in the history of large model development. The speed, quantity, and breadth of these releases are unprecedented in global AI development.

On February 2, Jieyue Xingchen took the lead by launching the Step3.5 Flash model, designed specifically for intelligent agents, pushing reasoning speed to 350 TPS and supporting 256K ultra-long contexts.

Subsequently, various companies began releasing their foundation large models. According to incomplete statistics, in the week leading up to the Spring Festival alone (February 11-16), dozens of large model products were released, covering nearly all core directions of current AI technology.

From the statistics, it is evident that general-purpose large models remain the main battleground this Spring Festival, with 15 releases accounting for half of the total.

In overseas markets, the main players are OpenAI, Google DeepMind, and Anthropic, a rising star. The difference lies in OpenAI's focus on vertical sectors this round, releasing code-specific models like GPT-5.3-Codex and GPT-5.3-Codex-Spark, while Google DeepMind and Anthropic updated their general-purpose models, launching Gemini 2.0 Pro and Claude Opus 4.6, respectively.

In the domestic market, ByteDance updated Doubao 2.0, while Alibaba released Qwen3.5. Among startups, Zhipu, Jieyue, Yuezhiaimi, MiniMax, and DeepSeek became the main forces in this round of updates.

Notably, Ant Group, a newcomer in foundation large models, has been particularly active in this round, open-sourcing three foundation large models: Ming-flash-omni-2.0, Ring-2.5-1T, and Ling-2.5-1T.

Subsequent reports indicate that Ant Digital will soon launch the Bailing Large Model Enterprise Edition. To further promote the deployment of the Bailing Large Model in B2B scenarios, Ant Digital has also established a dedicated "Large Model Technology Innovation Department" this year.

From a technological perspective, Mixture of Experts (MoE) architecture, multimodal fusion, and ultra-long contexts have become the three core keywords of this round of updates.

Jieyue Xingchen's Step3.5 Flash adopts a sparse MoE architecture, while MiniMax M2.5 also centers its design around MoE... Clearly, MoE has become the mainstream architectural paradigm for current AI large models.

More importantly, this round of updates has shifted the competition beyond mere parameter scale to ultimate efficiency—achieving more with less.

Take Alibaba's Qwen3.5 as an example: through sparse computing and architectural optimization, it achieves trillion-parameter-level performance with just 17 billion active parameters, marking a transition from "bigger is better" to "more efficient is better."

"Million-token-level long contexts" have become the "entry ticket" for general-purpose large models.

Claude Opus 4.6's 1 million tokens, DeepSeek V3's 1M context, and Ring-2.5-1T's 1 million tokens directly address pain points in "ultra-long documents, code refactoring, and knowledge-intensive tasks."

Multimodality has become a "standard feature." Products like Doubao 2.0, M2.5, and Gemini 2.0 Pro during the Spring Festival have integrated full capabilities in "dialogue, content, multimodality, and agents." Future large models will no longer be "single-function" tools but "intelligent operating systems."

Moreover, many initiatives during the Spring Festival are driving the "democratization" of AI. DeepSeek V3's "free grayscale testing," Doubao 2.0's "full rollout," and Kling Images' "priority access for Black Gold members" are all lowering user barriers.

From a vertical sector perspective, code, biology, healthcare, and education will become the main battlegrounds in the next phase. Product layouts like GPT-5.3-Codex, Qwen3-Coder-N, and AlphaGenome demonstrate the giants' emphasis on "professional barriers."

In the image and video generation sectors, domestic AI large models have achieved a " Overtaking on a curved road " (overtaking on a curve). Key competitors here include Kuaishou and ByteDance, which released products like Kling Images 3.0/Omni, Kling Video 3.0/Omni, and Seedance 2.0.

Localization is another major trend. iFLYTEK's Spark X2 emphasizes "training with fully domestic computing power," while Ant Group's Ring-2.5-1T positions itself as the "world's first trillion-parameter model with hybrid linear attention," achieving "domestic substitution" from underlying computing power to upper-layer applications.

In just three years (2023-2026), the development of AI large models has undergone tremendous changes.

From the release of pure text models to the fusion of text + images, and now to multimodal capabilities in text, images, and videos; from 4K-8K context windows to 1M+ contexts, representing a 125-fold increase in context capacity; from parameter stacking to the rise of MoE architecture, and then to sparse activation + architectural optimization, the evaluation of AI large model performance has shifted from "bigger is better" to "more efficient is better."

In terms of core capabilities, the progression has been from initial dialogue generation to multimodal understanding + simple agents, and now to agent clusters + autonomous planning + tool invocation, marking a leap from "talkative" to "capable."

It is clear that the technological capabilities of AI large models continue to evolve. However, technology can only sustain development when it truly moves toward applications. This year's Spring Festival has also been a carnival for AI applications.

AI Application Layer Carnival: C-Side Mass Penetration, B-Side Undercurrents

If the release of foundation models represents "infrastructure construction," then the application layer battle during the Spring Festival is the "topping out ceremony."

Over the past year, ByteDance's Doubao has achieved relatively high penetration among ordinary users. In December last year, Doubao's daily active users surpassed 100 million, topping China's AI application charts.

For example, a friend of the author mentioned that her 60-something mother is a heavy user of Doubao.

One day, the mother suddenly suffered from benign paroxysmal positional vertigo (BPPV). While waiting at home after calling 120, she used Doubao to search for symptoms and determine the possible cause.

This is just one instance of Doubao's application. Among many middle-aged and elderly users, Doubao has become a key tool for querying various information.

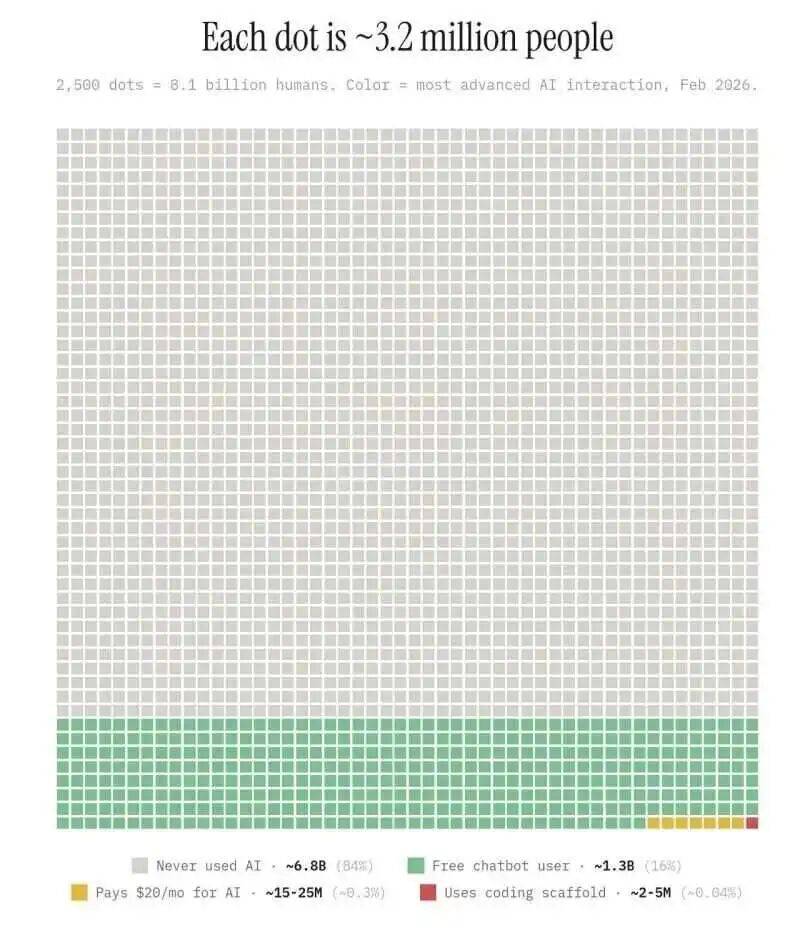

However, compared to traditional internet apps like WeChat, the overall penetration rate of AI tool assistants remains relatively low, even globally.

According to data from an X post, among the world's 8.1 billion people, 84% (6.8 billion) have never used AI, while only 0.3% (15-25 million) are willing to pay for AI services. Another 16% (1.3 billion) have used free chatbots.

In contrast, the Spring Festival AI marketing battle in China has brought AI assistants into millions of households, penetrating second- and third-tier cities.

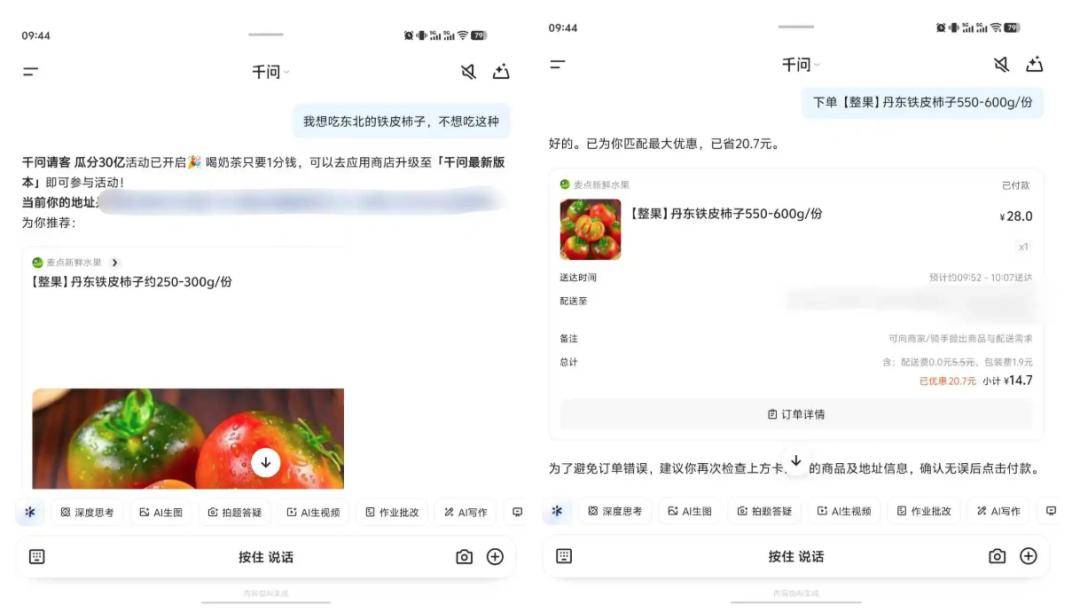

During the Spring Festival, social media feeds were filled with users sharing their experiences with AI assistants—whether snagging red envelopes or ordering milk tea for just 0.01 yuan using Qianwen.

After the Spring Festival, Doubao, Yuanbao, Qianwen, and Deepseek all joined the "100-million club." Doubao's monthly active users (MAUs) had already reached 200 million. Tencent recently announced that Yuanbao's daily active users (DAUs) exceeded 50 million, with MAUs reaching 114 million. Qianwen peaked at 140 million DAUs on its free order day. Ant Group's core AI businesses saw explosive growth, with over 100 million users of Alipay's "AI Pay" and Ant Afu APP also surpassing 100 million total users. The C-side market landscape for AI applications is rapidly consolidating.

More importantly, the core outcome of this marketing battle is not just a surge in traffic but the cultivation of user habits.

For example, Qianwen's battle report revealed that 130 million users tried AI for the first time during the Spring Festival, transitioning from "curiosity" to "dependency." The 5 billion command inputs enabled rapid iteration of AI models in real-world scenarios. The 73.52 million DAUs proved that "turning to AI for help" has gained a nationwide foundation.

(Ordering tomatoes using Qianwen)

(Ordering tomatoes using Qianwen)

Even in their hometowns, previously AI-illiterate relatives from the parental generation have started using these AI assistants. However, while the C-side impact is the broadest, it remains relatively shallow.

At this stage, user demand for AI is still concentrated in superficial scenarios like New Year greetings, recipe searches, and red envelope strategies. The core challenge for all players is retaining users through product strength after subsidies fade.

While the C-side opens up user traffic gateways, B-side penetration and growth are key to laying the foundation for AI companies' future development.

Currently, AI large model companies have two main B-side business segments:

One is API calls, which constitute the core revenue stream, especially for foundation model providers. API calls are currently the most stable source of income.

For example, in MiniMax's B-side business, API calls contribute significant revenue. For AI foundation large models, the logic behind API calls is simple: the better the foundation model, the more API call orders it can secure.

The other segment is B-side customized services, offering deep services from Model-as-a-Service (MaaS) to Platform-as-a-Service (PaaS).

For instance, Ant Digital has integrated all its AI-to-B businesses, leveraging its strengths in finance and healthcare to provide customized MaaS and PaaS solutions. Zhipu disclosed in its prospectus that it has secured numerous government and enterprise orders, achieving commercialization through private deployments and industry-specific customizations.

Additionally, nearly 70% of general-purpose models in this round of updates emphasize "enterprise-grade applications," offering "industry solutions, API integrations, and developer platforms."

This means these AI large model companies aim to build both developer ecosystems and generate revenue. As a result, the coexistence of open-source/open models and closed-source APIs has become mainstream.

Jieyue Xingchen, Ant Group, and Alibaba have chosen to open-source their core models to lower developer barriers and rapidly build ecosystems. Meanwhile, some industry giants and emerging startups insist on closed-source models, monetizing through API calls and forming a dual pattern (landscape) of "open-source for ecosystem building, closed-source for profit generation."

In fact, this round of foundation model releases has been accompanied by clear developer strategies, namely price reductions and open-sourcing.

For example, the API price of Alibaba's Qwen3.5 is as low as 0.8 yuan per million Tokens, which is only a fraction of that of mainstream international models. Companies such as Stepfun, Ant Group, and Moonshot AI have chosen to open-source their core models, allowing developers to use them for free and lowering technical barriers.

However, at this stage, the B-end market has not yet been finalized, and there is room for survival in each vertical category. A large number of intermediate service providers rely on foundational models from major companies or startups to provide customized solutions for vertical industries through 'contextual engineering.' For instance, they develop intelligent risk control models for financial institutions, clinical diagnosis assistants for medical companies, and intelligent production scheduling agents for the manufacturing sector.

Capital Reevaluates AI: The Logic and Skepticism Behind Sky-High Valuations

The dust from the Lunar New Year battle has settled, but its aftershocks continue to reverberate throughout the AI industry, particularly in the capital markets.

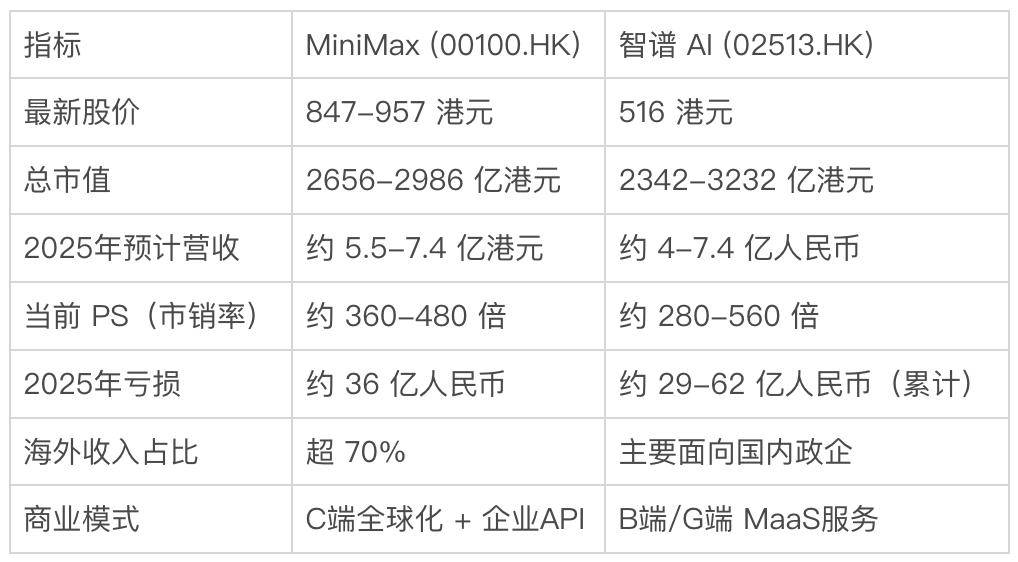

In just one week, the market capitalizations of Zhipu and MiniMax on the Hong Kong Stock Exchange experienced dramatic surges and subsequent crashes.

On the first trading day after the Lunar New Year, Zhipu's stock price soared by 42.72%, closing at HKD 725, with its total market value surging to HKD 323.2 billion. MiniMax also rose by over 14%, reaching HKD 970 per share. Together, the market values of the two companies broke through the HKD 300 billion threshold.

For comparison, JD.com's current market value is approximately HKD 294.584 billion. This means that two AI companies founded less than a decade ago have quietly surpassed the market value of a well-established internet giant with over two decades of operation.

However, after briefly breaking through the HKD 300 billion mark, the stock prices of Zhipu and MiniMax began to plummet. By the close of trading on February 23, Zhipu had fallen by 22.76%, and MiniMax by 13.35%, with their combined market value evaporating by nearly HKD 100 billion.

Why did the stock prices of these two companies experience such significant volatility in just one week?

From a news perspective, the capital market's focus on Zhipu and MiniMax stems from their proven commercialization capabilities.

Take Zhipu as an example. On the same day it announced the release of GLM-5, Zhipu also declared a price hike for its core product packages, with overall increases of at least 30%. The subscription price for the overseas version doubled, and even first-time user discounts were eliminated.

Despite the price increase, users continued to pay.

Relevant data shows that Zhipu has 2.7 million paying users. In January, due to a surge in user calls, the company had to reduce the daily sales volume of its packages to 20% of the original amount, initiating a sales restriction mode.

For MiniMax, the market generally believes that the official launch of its new-generation text model, MiniMax M2.5, was a significant catalyst for its sustained stock price growth.

The latest news reveals that MiniMax M2.5, released on February 13, quickly topped the OpenRouter Token usage rankings within a week of its launch. During the statistical period from February 9 to February 15, OpenRouter's weekly Token usage surged by 3.19T Tokens compared to the previous week, with MiniMax M2.5 alone contributing 1.44T Tokens. Its usage volume exceeded the combined total of Kimi K2.5, GLM-5, and DeepSeek V3.2.

Undoubtedly, the commercialization capabilities of AI large model companies, particularly their B-end revenue, are the fundamental drivers behind the capital market's revaluation of AI.

The rapid development of API calls and B-end customization has also shifted AI companies' revenue models from 'single subsidy' to 'diversified monetization.'

Ant Group's in-depth financial and medical services, Zhipu's government and enterprise orders, and MiniMax's API revenue all demonstrate the profitability of B-end business. The capital market generally believes that B-end business will become the core revenue source for AI companies in the future.

Additionally, the valuation of Chinese AI companies in the capital market has gradually aligned with overseas markets. Benchmarking against overseas companies' valuation logic has also driven up the valuations of domestic AI companies.

Take Anthropic as an example. Its ARR (Annual Recurring Revenue) surged from USD 100 million in 2023 to USD 14 billion in February 2026. In its recent funding round, the company's valuation soared to USD 380 billion. This translates to a PS (Price-to-Sales) ratio of 27 times, a very reasonable valuation range.

Domestic companies like Zhipu, MiniMax, and Stepfun have achieved technological parity with overseas startups, leading the capital market to assign them higher valuation levels. As of February 20, the PS ratios of Zhipu and MiniMax both reached several hundred times. To align with Anthropic's valuation level, this implies an expected tenfold revenue growth over the next three years.

This risk is not insignificant.

Note: Data as of February 20

Note: Data as of February 20

In summary, from the wave of foundational model releases to the penetration of AI applications in the C-end and B-end markets, and then to the capital market's revaluation, the 2026 Lunar New Year has become a watershed moment for China's AI market.

Just as WeChat Red Packets transformed payment methods in 2014, the 2026 Lunar New Year has changed how people interact with the digital world. AI is evolving from a 'tool' into an 'environment,' becoming an integral part of people's lives and work.

But this is just the beginning. When subsidies recede, when traffic returns to rationality, and when the capital market's fervor cools, the real AI war will begin. In the coming days, China's AI industry will enter a new phase of 'value realization.'

The melee among foundational models, applications, and capital will continue, but companies with genuine technological prowess, commercial capabilities, and ecological thinking will ultimately emerge, defining the next golden decade of China's AI industry.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once