Intelligent Driving This Year: After Nine Bell Ringings on the Hong Kong Stock Exchange, Where to Next?

02/25 2026

02/25 2026

461

461

In late 2025, HiDi Intelligent Driving rang the bell at the Hong Kong Stock Exchange, marking a milestone for the autonomous driving industry. This was the ninth time that year the HKEX had rung the bell for a company in the autonomous driving supply chain. After a series of listings, investors in Hong Kong-listed stocks had already shifted from initial enthusiasm to fatigue.

Looking at global capital markets, investors may feel similarly. This year, four core autonomous driving (L4/Robotaxi) companies went public globally (including those that filed), along with six companies focused on assisted driving and intelligent driving solutions (solution providers/domain controllers). If we include companies in the autonomous driving-related supply chain (simulation, sensors), there are even more.

Amid the continuous ringing of bells, billions of dollars in capital have once again converged into an unstoppable wave, flowing from solution providers to the supply chain. However, unlike the funding boom in 2018, autonomous driving in 2025 has transformed from a "future commodity" seven years ago into a widely available product.

As the capital market's bell still echoes, has the era of autonomous driving truly arrived?

At the end of 2024, urban NOA (Navigate on Autopilot) began to be implemented in vehicles priced above 200,000 RMB. However, the driving experience was not yet smooth, with hesitant acceleration and deceleration, and the system often "gave up" when cut off by other vehicles. "Entrusting safety to machines is highly irresponsible," many experienced drivers told Guangzhui Intelligence about their views on autonomous driving.

But soon after, BYD led the charge in "intelligent driving democratization" after the Spring Festival. Two-thirds of new vehicles in China were equipped with L2 autonomous driving; the number of vehicles with urban NOA surged to 3.129 million in the first 11 months of 2025; by the end of 2025, the Ministry of Industry and Information Technology officially issued permits for L3 autonomous driving; Waymo, Pony.ai, WeRide, and Tesla's unmanned fleets expanded globally, with the trend of autonomous driving adoption turning into solid data, relentlessly overwhelming the "confidence" of every experienced driver.

Looking back, this outcome did not come easily.

Over the past year, the autonomous driving industry has experienced a complete "emotional cycle," shifting from eagerness at the beginning of the year to caution in the middle, and then to ambition by the end. By early 2026, the entire autonomous driving industry was filled with a sense of victory and urgency for expansion.

As autonomous driving technology began to mature, industry leaders started planning new goals. Horizon Robotics, Momenta, Huawei ADS, DeepRoute.ai, and QCraft—all of which have surpassed one million units in mass production—are now planning overseas expansion. Leading AI technology companies like Li Auto and XPeng are beginning to venture into "higher-level" embodied intelligence.

"By 2028 at the latest, L4 autonomous driving will achieve large-scale implementation,"

Perhaps the progress of the autonomous driving industry will unfold as Li Xiang, founder and CEO of Li Auto, envisioned at the company's all-hands meeting in January this year. Over the past decade, autonomous driving has evolved from nothing to something, and in the next decade, it will move faster and farther.

365 Days of Exuberance and Clarity in Autonomous Driving

In October 2024, Horizon Robotics, the intelligent driving supplier with the most mass production fixed point in China, rang the bell for its HKEX IPO. At that moment, the entire autonomous driving industry was filled with a sense of "ready for battle."

By early 2025, optimism permeated the industry.

In February, BYD announced that all its models would come standard with intelligent driving, bringing the price of L2+ intelligent driving-equipped vehicles below 100,000 RMB. Soon after, nearly all traditional automakers, including Chery and Geely, followed suit, kicking off the "intelligent driving democratization" movement in the automotive industry for the year.

"Following other vehicles is the most practical use of intelligent driving."

A salesperson at a 4S store recommended intelligent driving versions to Guangzhui Intelligence, saying, "Rush hour traffic is exhausting, but with intelligent driving, you can relax and even reply to messages." During that time, both consumers and industry professionals were confident in intelligent driving.

However, just a month later, an unexpected accident instantly cooled the industry.

Although the Xiaomi SU7 incident was officially attributed to "the driver's misuse of assisted driving functions in violation of regulations, posing significant safety risks," the view that "intelligent driving technology is immature" quickly spread. Under regulatory pressure, claims of "L2.9999" and various "door-to-door" intelligent driving features disappeared, with "assisted driving" becoming the industry's sole term. Chinese intelligent driving companies entered their "quietest" six months.

A turning point came in June. Tesla launched small-scale unmanned Robotaxi tests in Austin, prompting the entire smart car industry to flock to the U.S. for "inspection and experience." The excitement even surpassed that of Tesla's FSD v12, which introduced "end-to-end" technology.

One key reason for the attention surrounding Tesla's Robotaxi was that its autonomous driving solution was consistent with passenger vehicles, both relying on the FSD software stack and a pure vision approach. For the autonomous driving industry, if Tesla's Robotaxi operated smoothly, it would mean that high-level intelligent driving (hardware and software solutions) could directly reach the L4 Robotaxi endpoint. The industry seemed to glimpse a future where L4 autonomy could be achieved for just a few thousand dollars.

Although real-world tests revealed numerous comical mishaps with Tesla's Robotaxi, Tesla's entry undoubtedly disrupted the previous competitive landscape dominated by "traditional" L4 players like Waymo, Baidu Apollo, Pony.ai, and WeRide.

Stimulated by Tesla, the Robotaxi industry saw a series of successes. That year, Pony.ai and WeRide's Robotaxi fleets expanded to thousands of vehicles, with significant quarterly revenue growth. Baidu Apollo announced in November that it was handling over 250,000 weekly unmanned orders. Waymo reported up to 450,000 weekly paid rides, totaling around 15 million trips annually.

As L4 autonomous driving inched closer to commercial viability, capital began to refocus on the industry.

In November, Pony.ai and WeRide achieved dual listings on the U.S. and Hong Kong stock exchanges; Hesai Technology, a leading lidar company, completed the largest IPO in the global lidar industry. Suppliers like Innovusion (a lidar company primarily serving NIO), Botauto (cabin-driving integration), and Joyson Electronics (intelligent driving domain controllers) also went public. On December 19, HiDi Intelligent Driving, focused on unmanned mining trucks, officially listed, becoming the "world's first autonomous mining truck company." Currently, companies like Tiantong Vision (L2+ integrated parking), Freetech (automotive electronics Tier 1), UISEE, and Qianli Technology are awaiting their turn to go public.

Meanwhile, after six months of dormancy, intelligent driving suppliers began to reap the rewards.

By August 2025, Horizon Robotics announced that its Journey series chips had surpassed 10 million units in mass production. By the end of the year, QCraft had achieved mass production of one million units; Momenta's urban NOA function was deployed in over 410,000 vehicles; full-year sales of models equipped with Huawei ADS exceeded 900,000 units, a tenfold increase in two years.

"What level of intelligent driving does this car have?" became one of the most frequently asked questions by consumers at 4S stores. After the launch of intelligent driving models, Su Linke, general manager of software development at Seres, said, "I dare not ignore calls on weekends; salespeople keep asking how to explain the intelligent driving system to customers."

"I wouldn't use it for ride-hailing; I'm afraid passengers might misunderstand. But I'm used to it when driving myself, and it's common to see the little blue light (indicating intelligent driving is active) on expressways," a XPeng G6 ride-hailing driver told Guangzhui Intelligence.

Finally, in December 2025, L3 autonomous driving entered the implementation phase, marking the end of all controversies in the industry.

Thus, the autonomous driving industry completed a "spiral ascent." Over 365 days, it shifted from exuberance at the beginning of the year to caution in the middle, and then to clarity by the end. After "tempering," the industry became more solid.

Technology, Cost, and Software-Hardware Integration: The Golden Age of Autonomous Driving Begins

Why, in just one year, has autonomous driving regained consumer trust and moved from science fiction into everyday life?

The most intuitive (intuitive) answer lies in the democratization of intelligent driving at the start of 2025. Under sales pressure, automakers effectively "gave away" intelligent driving features to consumers, leading to a rapid increase in L2+ intelligent driving penetration.

Of course, this growth is also attributed to technological advancements.

From a software perspective, the biggest variable in the autonomous driving industry in 2025 was the maturation of world models and the VLA (Vision-Language-Action) technical route. These technologies can be seen as upgraded versions of the end-to-end imitation learning popular in 2024, further raising the ceiling for AI "thinking" and "capability training."

Simply put, VLA technology solved the problem of having to retrain autonomous driving systems for even minor issues.

It's worth noting that while VLA is a mainstream technical solution in the autonomous driving industry, not all companies use it. Currently, companies like Li Auto, XPeng, Horizon Robotics, and DeepRoute.ai have adopted or are considering VLA.

On the other hand, world model technology primarily addresses the issue of insufficient AI training data, solving the pain point of autonomous driving training being limited to "how many cars are on the road."

Traditional road testing methods for data collection are not only expensive and time-consuming but also rarely encounter truly extreme scenarios. With world model technology, autonomous driving systems can generate the exact data they need. For example, for scenarios that are nearly impossible in reality, world models enable targeted training. Regarding the value of world model technology for autonomous driving, Han Xu, founder and CEO of WeRide, summarized, "Using our internally developed AI testing platform (Genesis), we reduced data collection and training costs by 75%."

In addition to software advancements, the cost of intelligent driving solutions in 2025 has dropped to previously "unimaginable" levels.

According to a forecast by Rao Qing, chief solution architect at Momenta, "After 2026, the cost of a cost-effective urban NOA solution will further drop to 4,000-5,000 RMB, making intelligent assisted driving accessible to thousands of households." However, Guangzhui Intelligence has already seen urban NOA solutions priced at 3,000 RMB on the market. It is thanks to these ultra-low costs that high-level intelligent driving can now be implemented in vehicles priced below 100,000 RMB.

The price reductions in intelligent driving solutions are directly tied to cost reductions in chips and lidar. From a chip perspective, the computing power required for high-level intelligent driving has dropped from 508 TOPS (dual NVIDIA Orin X solution) in 2023 to 128 TOPS (QCraft's solution based on Horizon J6M). Lidar costs have declined even more significantly. Previously, high-level intelligent driving required four lidar sensors, but now one or even zero (as XPeng has shifted to pure vision) can suffice. According to a Goldman Sachs report, the prices of mainstream ADAS lidar sensors had generally fallen to the 1,000-1,500 RMB range by the end of last year, a decrease of over 60% from early 2024.

Perhaps all software and hardware advancements have been waiting for the moment of software-hardware integration.

After a year of evolution, more and more autonomous driving players have reached a consensus on developing their own chips.

"Only by doing it ourselves do we realize how much efficiency can be improved through chip-software integration," Li Xiang recently lamented to Guangzhui Intelligence.

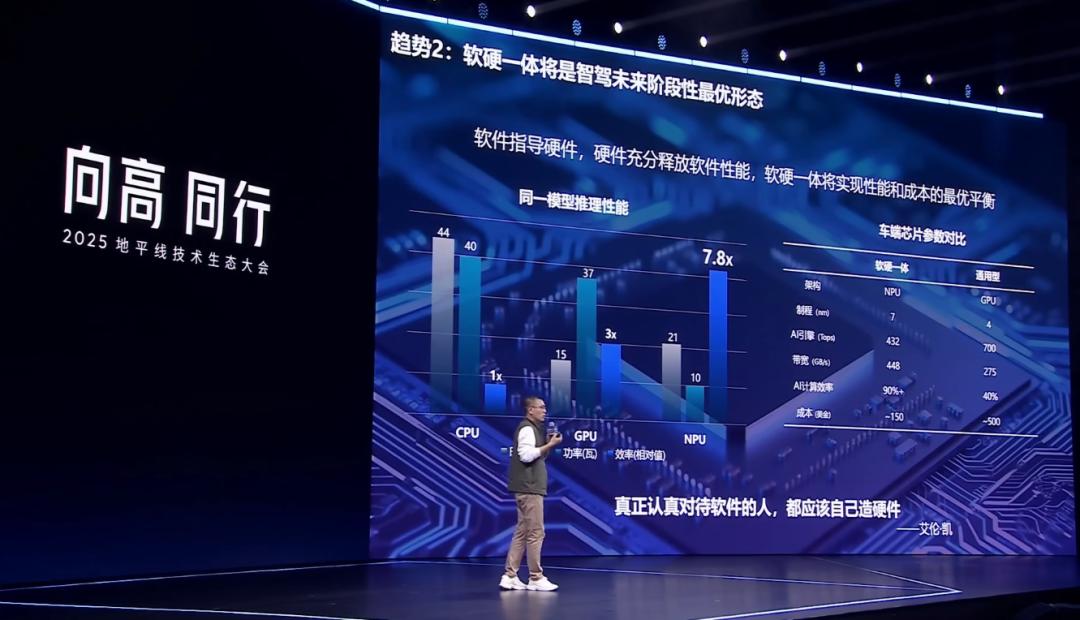

According to data provided by Jiang Haipeng, deputy general manager of Great Wall Motor's Technical Center, the computing efficiency of a custom chip architecture with software-hardware integration can exceed 90%, while a generic GPU architecture can only reach 40%.

Instead of "tweaking algorithms" on NVIDIA's computing platform and being constrained by the Orin X, which wasn't designed specifically for AI, XPeng, NIO, and Geely (Semiconductor) have now mass-produced their own chips and deployed corresponding algorithms. In 2026, we will also see Li Auto's new L9 equipped with the Mach 100 chip. Momenta's urban NOA chip, developed through its subsidiary Xinxin Hangtu, is progressing smoothly and has already secured fixed point from SAIC Volkswagen, SAIC IM, and Beijing Hyundai, with mass production expected in 2026.

At the same time, observing the iteration of chip designs, we can clearly see that autonomous driving companies are deepening their understanding of software-hardware integration.

For example, when Horizon Robotics developed its first-generation BPU architecture, the focus was on perceptual computing, enabling vehicles to "see" the world. On its latest "Riemann" architecture, Horizon emphasizes large language models and vector computing, representing a pursuit of "simplifying complexity" in computing while increasing demand for large models' thinking capabilities.

However, we must remain sober (sober) and acknowledge that autonomous driving technology in 2026 is still not perfect.

During the Spring Festival, Guangzhui Intelligence experienced an unexpected situation while riding in a leading automaker's vehicle updated to the latest intelligent driving version. The driving was smooth until the vehicle entered a left-turn lane at a red light. The navigation screen showed a straight route, and the car's system displayed normal navigation and lane information, but the VLA driver model decided to go straight. "If I hadn't taken over, would I have lost points?" the driver remarked with a hint of sarcasm after regaining control.

On the other hand, according to a recent report filed by Tesla, its Austin Robotaxi fleet experienced nine collisions over 500,000 miles driven between July and November 2025. This translates to an accident rate of one every 55,000 miles, which is 3-9 times higher than the U.S. human driving accident rate.

However, these minor setbacks will not hinder the widespread adoption of autonomous driving.

Currently, Tesla has begun mass production of the CyberCab, a Robotaxi without a steering wheel where passengers can only communicate with AI. Tesla has set a short-term goal of producing two million units annually. Meanwhile, Li Auto is preparing to challenge the limits of automotive intelligence with its new L9, equipped with an effective computing power of 2,560 TOPS.

"2026 marks the beginning of a golden decade for unmanned driving in the future,"

as Yu Qian, co-founder, chairman, and CEO of QCraft, eagerly anticipates. With 2026 as the starting point, the golden age of autonomous driving has arrived.

When Autonomous Driving Is No Longer Rare, What Lies Ahead?

Once hailed as the "pearl on the crown of artificial intelligence," autonomous driving is now transforming into a commonplace "sugar bean."

Perhaps there are no eternal truths. As autonomous driving technology grows, the century-old automotive industry is also undergoing transformation.

For example, in terms of driving safety and car maintenance costs, in January this year, Lemonade, a U.S. insurance company, announced the launch of autonomous vehicle insurance, which reduces the per-mile premium by about 50% when FSD (Tesla Autopilot) is enabled. This indicates that autonomous driving significantly enhances driving safety. Explaining the rationale behind this business adjustment, Shai Wininger, co-founder and president of Lemonade, said, 'A car that can observe 360 degrees, never gets drowsy, and reacts in milliseconds is simply incomparable to humans.'

On the other hand, some automakers have also discovered that autonomous driving is having an impact on the automotive industry itself.

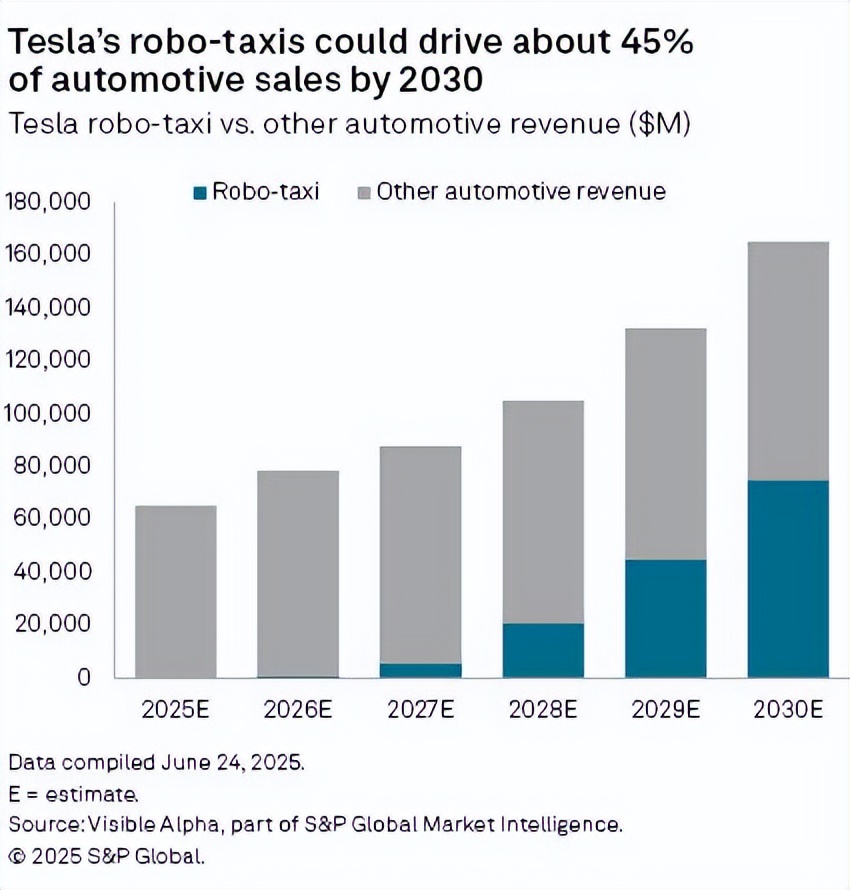

The source of anxiety stems from an analyst's point in July 2025 that Tesla's long-term ride-hailing revenue generated by Robotaxi could potentially surpass its revenue from car sales. For traditional automakers, this means that the conventional 'car-selling' business model is being 'overturned' by autonomous driving from two perspectives.

Firstly, the demand for traditional passenger vehicles is being replaced by Robotaxis. The sales logic for cars that meet daily commuting needs will no longer exist in the future. On the other hand, due to the differences in business attributes between Robotaxi and traditional car sales, the gross profit margin of revenue generated by autonomous driving (software + operations, which can reach 70%) is much higher than that of car sales (20% is considered a high level in the industry), thereby changing the valuation model for automakers. This means that automakers with a high level of autonomous driving technology will have better cash flow and can make more development plans.

'If we can't see it clearly now, we might not even have a chance to get in the game in the future,' Jiang Haipeng warned.

In the future, car sales may partially give way to 'mobility as a service,' with automakers shifting from selling cars to selling miles. Perhaps this transformation will not come as quickly, but considering a ten-year cycle, autonomous driving may change the automotive industry.

Focusing on the short-term future, suppliers of autonomous driving technology may also be feeling some anxiety.

Over the past year, we have witnessed the downfall of several former stars in the autonomous driving field. For example, Haomo.ai, backed by Great Wall Motors and once valued at nearly 10 billion yuan, was reported to have halted its operations; Zhongmu Technology, which once reached the threshold of an IPO, found itself in an operational crisis after a hasty transformation. According to incomplete statistics, nearly 10 companies that had achieved business implementation in autonomous driving faced significant difficulties in 2025.

'Now everyone's offerings (route solutions) are on the table, with the same goals. Everyone knows what their competitors are doing, and automakers are also aware of the capabilities of each supplier,'

as Shen Shaojie, CEO of ZhiYu, recently mentioned. When mass production in the millions has become the threshold for intelligent driving suppliers to 'survive,' all players in the industry must find more growth opportunities.

From the current perspective, 'intelligent driving democratization' will still apply in 2026.

This not only refers to the further reduction in prices of high-level intelligent driving models but also includes the intelligent driving transformation of fuel vehicles. Currently, Huawei ADS has implemented urban NOA in FAW-Audi vehicles. Yu Qian told Guangzhui Intelligence that QCraft is already prepared to adapt to fuel vehicles. Wu Yongqiao, President of Bosch Intelligent Driving Control China, stated, 'Bosch is confident in bringing the convenience of intelligent driving to more than 15 million fuel vehicle owners in China.'

However, this path is actually very challenging, requiring manufacturers to balance cost, algorithm development, and endless engineering adaptation capabilities. Su Qing, Vice President and Chief Architect of Horizon Robotics, described it as, 'After doing this for so many years, we know all too well that it's a double squeeze on intelligence and physical effort, and the process is extremely painful.'

Another route is to go global and pursue L4 autonomy, seeking a bigger piece of the pie.

On the global front, domestic autonomous driving companies are still primarily in the stage of competing for partnerships with overseas brands. Although Horizon Robotics has announced the establishment of its European headquarters, ZhiYu Technology (formerly DJI Automotive) has announced the establishment of a German subsidiary, and Momenta-powered IM Motors is already on sale in the UK, actual progress has not yet reached the point of widespread global implementation. In the domestic market, relatively stable (or upcoming) partnerships include XPENG + Volkswagen, Horizon Robotics + Volkswagen (CorePilot) + Japanese brands (Toyota, Suzuki), and Huawei ADS + Audi.

In the L4 sector, the market space becomes much larger. Over the past year, we have witnessed capital investments in the Robotaxi 'stories' of companies such as WeRide, Pony.ai, Qianli Technology, DiDi Autonomous Driving, and Ruqi Mobility. Meanwhile, mass production 'powerhouses' in intelligent driving, such as Horizon Robotics, Momenta, and QCraft, are also flocking to this space. This sufficiently hints at the potential contained within the L4 industry.

However, beyond these two routes, some autonomous driving players are shifting their focus away from 'vehicles' and preparing to climb the peak of physical AI.

In November 2025, XPENG proudly showcased its robot Iron and announced its entry into physical AI. In January 2026, Qualcomm announced the launch of a general-purpose computing platform for embodied intelligence based on its autonomous driving experience. In February, Li Xiang stated on Weibo that the ultimate answer for cars is robots.

For players with sufficiently advanced autonomous driving technology, the data, algorithms, and computing power accumulated in autonomous driving are becoming the cornerstone of embodied intelligence. Driving may be the 'first task to conquer' for AI in the physical world. Once driving is conquered, it means that embodied intelligence may next conquer new complex scenarios such as housework, factories, and healthcare.

Looking back, the development of the autonomous driving industry has always been about AI's penetration into the physical world. However, after the developments of 2025, autonomous driving has suddenly shown infinite possibilities.

Conclusion

The past decade marks the final cycle of the embryonic stage of autonomous driving technology. Over the past ten years, we have witnessed a range of emotions on the faces of industry practitioners—confidence, joy, frustration, anxiety, busyness, and, by early 2026, broad smiles.

Whenever I study a technology that has the potential to change the world, I often recall U.S. President Kennedy's moon landing speech in 1962. At that time, the United States was gripped by anxiety over its technological backwardness. Facing public skepticism and scientists' hesitation, Kennedy's almost 'unrealistic' rallying call imbued the pursuit of technology with a romantic hue.

'We choose to go to the moon... We choose to go to the moon in this decade and do the other things, not because they are easy, but because they are hard, because that goal will serve to organize and measure the best of our energies and skills, because that challenge is one that we are willing to accept, one we are unwilling to postpone, and one which we intend to win, and the others, too.'

From the perspective of industry cycles, autonomous driving may just be another iteration of the technology maturity curve. But for countless individuals working day and night to overcome challenges, every step is as difficult as a moon landing.

In 2025, we have scaled the 'Everest' of autonomous driving. Ahead lie the peaks of general-purpose embodied intelligence, physical AI, and even AGI. No one can guarantee that we will reach the summit, but we have already begun our journey.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once