Spring Festival AI Surge: AI Emerges from Its Infancy

02/25 2026

02/25 2026

514

514

Source | Bohu Finance (bohuFN)

Author | All too well

This February, while the Hang Seng Tech Index was still on a downward trend, two emerging AI stars stood out with their remarkable market performances. Zhipu, which had been listed for two months, saw its share price soar from HK$226.4 at the end of January to HK$628 before this report was published. MiniMax, listed for just one and a half months, rose from HK$473 per share at the end of January to HK$880 per share before the report was released.

The market capitalization of both companies once exceeded the HK$300 billion mark.

What does HK$300 billion signify? A straightforward comparison clarifies the picture: Bilibili's current total market value stands at HK$95.717 billion, while JD.com's is approximately HK$301.679 billion. In essence, these two AI companies, founded less than a decade ago, have quietly surpassed many internet giants in terms of market value.

Unlike these emerging stars thriving in the secondary market, major tech companies are focused on making AI accessible to a broader audience.

During this year's Spring Festival, ByteDance, Alibaba, and Tencent all canceled holidays for their teams, gearing up to meet the AI demand they had heavily invested in. According to their reports, on New Year's Eve alone, Doubao AI recorded 1.9 billion interactions. Alibaba spent RMB 3 billion to enable nearly 200 million users to make purchases through Qianwen. Tencent distributed RMB 1 billion in red envelopes, achieving a new monthly active user high of 114 million.

This marked the first significant clash among major companies in 2026. Key questions loom large: How can they unlock and discover more demand? How can they secure a foothold in the AI era ahead of competitors?

Whether it's major companies investing heavily to acquire users or AI startups dominating the secondary market, these are different facets of the AI era. Undoubtedly, AI applications have begun to deeply integrate into our lives, riding the wave of Hong Kong-listed AI startups and fueled by the FOMO (Fear of Missing Out) sentiment among major companies, urging them to push AI to the masses.

01 2026: The First Year of AI Commercialization?

The rapid ascent of MiniMax and Zhipu has raised eyebrows, largely because their market values defy traditional valuation models.

Even when compared to other AI companies, they appear severely overvalued. Anthropic, their U.S. counterpart, is valued at approximately $380 billion, with annualized revenue exceeding $2 billion and a price-to-sales ratio of around 190 times. In contrast, if MiniMax's revenue of $53.44 million in the first nine months is used to justify its HK$300 billion market value, its price-to-sales ratio exceeds 700 times.

However, a key driver behind the surge of MiniMax and Zhipu is that their new models demonstrate that Chinese AI teams can compensate for hardware shortcomings with algorithmic efficiency, creating models that professional users are willing to pay for and find useful.

Take Zhipu as an example.

Programmers have always been a significant paying group for AI, with the previously popular Vibe Coding using AI as a tool to write code. However, in global authoritative programming benchmark tests, closed-source models have consistently held a clear lead.

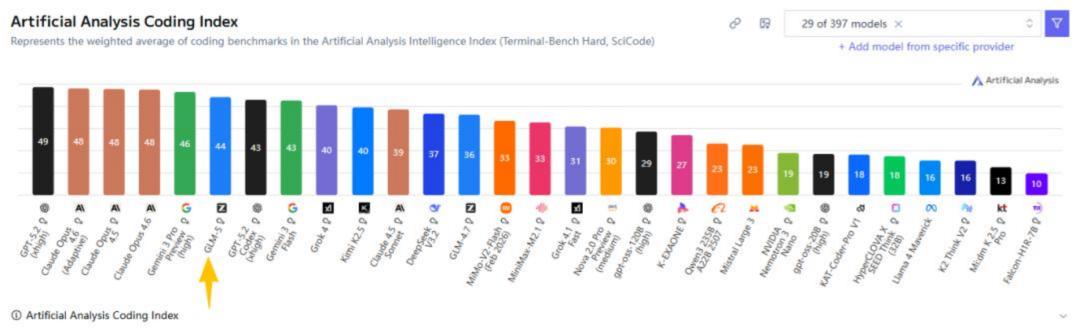

Zhipu's newly released GLM-5 breaks this tradition. According to Artificial Analysis test results, GLM-5 ranks 4th globally in intelligence, 6th in programming ability, and 3rd in agency capability, closely trailing top closed-source models. In the AA-Omniscience hallucination rate test, GLM-5 reduced the hallucination rate to 34%.

Beyond comprehensive upgrades in reasoning, coding, and autonomy, GLM-5 significantly reduces operational costs. Its deep sparse attention mechanism allows it to intelligently filter the most important words based on content. For example, when processing a long text of 128,000 words, GLM-5's computational load is cut by half to two-thirds. As a result, while GLM-5's total parameter count has expanded to 744 billion, only 40 billion parameters are actually activated in each operation.

After the new model's release, due to a rapid increase in user scale and API calls, Zhipu announced a price hike of over 30% for its GLM Coding Plan. MiniMax M2.5, focusing on lightweight efficiency and driven by Agent demand represented by OpenClaw, became the top-ranked model in terms of Tokens called on OpenRouter in just one week.

Instead of pursuing model parameters, the focus has shifted to actual user adoption, marking a stark contrast to the price war competition familiar in the past among AI vendors.

Even major companies, which still spend heavily to acquire users, are ultimately competing on usability.

LatePost reported that in early 2025, ByteDance CEO Liang Rubo stated at a company-wide meeting that Doubao did not exhibit the internet product characteristic of 'improving with more users.' He urged ByteDance to pursue higher intelligence limits. Before the Spring Festival, Doubao 2.0 was upgraded, and Qwen3.5 was launched. Both emphasized Agent execution capabilities, focusing on practicality and effectiveness. After the release of the video generation model Seedance 2.0, Feng Ji, CEO of Game Science and producer of Black Myth: Wukong, exclaimed, 'The childhood of AIGC is over.'

Unlike the emerging stars, these giants with vast ecosystems spanning e-commerce, lifestyle services, short videos, gaming, and even payments, need to leverage AI to further solidify their positions.

Thus, Qianwen was integrated into Alibaba apps like Taobao Flash Sales, Alipay, Taobao, Fliggy, and Amap. To enhance Qianwen's user experience, Alibaba invested heavily, updating it 2-3 times weekly, with some features going from design to launch in just 1-3 days.

Whether it's Zhipu and MiniMax taking an early lead or major companies engaging in red envelope wars, all are striving to make AI genuinely usable for different audiences.

02 Underlying Concerns Amid Prosperity

OpenRouter data shows that AI tokens processed in the first week of February this year reached 13 trillion, nearly doubling from the first week of January. This is closely tied to the explosive growth of Agents in the industry.

Overseas, OpenClaw, an open-source personal AI assistant, can run autonomously on local computers or servers, executing various tasks through natural language instructions. Its popularity skyrocketed, surpassing 100,000 stars on GitHub within a week of its release, becoming one of the fastest-growing and most attention-grabbing open-source projects in GitHub history.

While currently thriving both domestically and internationally, AI applications still face numerous concerns.

First, high investment and losses are the industry norm, as seen with Zhipu and MINIMAX.

From 2022 to 2024 and the first half of 2025, Zhipu's revenue was RMB 57 million, RMB 125 million, RMB 312 million, and RMB 191 million, respectively, with net losses of RMB 143 million, RMB 788 million, RMB 2.956 billion, and RMB 2.351 billion, totaling RMB 6.238 billion in losses over three and a half years.

From 2022 to 2024 and the first three quarters of 2025, MINIMAX's revenue was $0, $3 million, $31 million, and $53 million, respectively, with net losses of $74 million, $269 million, $465 million, and $512 million, totaling $1.32 billion in losses over three years and three quarters.

Losses primarily stem from labor and computing power costs. According to Dolphin Research, both companies have fewer than 1,000 employees, with Minimax having under 400. Research and development personnel account for nearly 75% of their workforce, with per-capita monthly costs ranging from RMB 65,000 to RMB 85,000 (excluding stock-based incentives). Notably, Minimax's per-capita monthly R&D cost reaches RMB 160,000.

While labor costs seem high, they pale in comparison to the fierce competition where companies spend hundreds of millions of dollars to poach talent. The real pressure comes from computing power.

Data from both companies reveals that computing power investments related solely to model training account for over 50% of total expenditures, making it the primary cost driver and core source of losses.

For example, in 2023, training a first-generation model cost approximately $40-50 million. As models evolve to the next generation, achieving intergenerational differences often requires exponential growth in data volume, parameter scale, and computing power demands. It is almost commonplace for training costs to increase by 3-5 times with each model upgrade.

In other words, while computing efficiency improves, total computing demand expands.

On one hand, model scales continue to grow, with multimodal capabilities stacking up. On the other hand, high-frequency scenarios like Agents and programming assistants begin to materialize, leading to a rapid rise in API calls. In this context, even if the cost per token declines sharply, the total computing bill for companies may continue to soar as total calls and model complexity surge simultaneously.

This explains why, despite declining inference costs, companies are burning money faster than ever.

According to CIC data, the industry's average inference cost dropped from about $20 per million tokens at the end of 2022 to less than $0.1 by the end of 2024, with further declines likely. Single calls have indeed become cheaper.

Meanwhile, in 2024, MiniMax's total cloud computing costs for inference and training reached approximately $167 million, accounting for 545% of its revenue. In other words, for every $1 earned, over $5 was spent on computing power. Zhipu's combined computing and cloud service fees that year totaled RMB 1.583 billion, accounting for 506% of its revenue. For every $1 earned, about $5 was consumed by computing power.

Moreover, this trend is intensifying. Zhipu's computing service fees as a proportion of R&D expenditures climbed from 17.3% in 2022 to 71.8% in the first half of 2025. MiniMax's cloud computing expenditures for training as a proportion of R&D rose from 39.4% to nearly 80%.

This means that, under current conditions, the more excellent the model, the higher the training cost, and revenue seems unable to keep pace with the speed of updates and iterations. When will there be a resolution?

Second are regulatory and infringement risks. For example, Seedance 2.0 not only received cease-and-desist letters from copyright holders but also disabled its highly controversial real-person reference capability.

Amid this wave, expecting an immediate, decisive victory is unrealistic. AI participants face a genuine commercial war, and the Spring Festival that just passed may have been merely an appetizer.

Reference Sources:

1. TopAI Lab: Zhipu GLM-5 Technology Revealed: Can Its Coding Ability Match Claude?

2. Silicon-Based Starlight: After Zhipu and Minimax Unleash Their 'Big Moves,' DeepSeek 'Attacks' with a 'Basic Move'

3. LateAI: Full Record of the Spring Festival AI Battle: Red Envelopes, Models, and Computing Power

4. LetterAI: Zhipu and MiniMax Launch Dual Models to Compete with Claude

5. Dolphin Research: A Deep Dive into Minimax and Zhipu: A Brutal Showdown of Computing Power Intensity and Financing Endurance?

6. GeekPark: Why Does Everyone Think MiniMax and Zhipu Are 'Too Expensive'?

7. Thick Snow Research: China's 'Two AI Giants' Go Public: 70-80% of R&D Spending Goes to Computing Power

The copyright of the article's cover image and illustrations belongs to their respective owners. If the copyright holders believe their works are unsuitable for public browsing or should not be used without compensation, please contact us promptly, and our platform will make immediate corrections.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once