Trillion-Dollar Market Cap Evaporates: What's Wrong with Microsoft?

03/06 2026

03/06 2026

628

628

Introduction: Compared to the slowdown in revenue growth of the Azure cloud platform, the end of the 'honeymoon period' between Microsoft and OpenAI is a more fundamental reason for the weakness in Microsoft's stock price.

Li Ping/Author Lishang Business Review/Producer

1

Evaporation of Trillion-Dollar Market Cap

As the AI boom recedes, Microsoft has become the first 'domino' to fall.

On July 31, 2025, Microsoft's market capitalization touched the important threshold of $4 trillion for the first time during trading, becoming the second company globally after NVIDIA to surpass this milestone. On October 28, 2025, Microsoft's stock price surged by 2%, closing above the $4 trillion market cap mark.

However, since November 2025, Microsoft's stock price has continued to weaken, showing a 'four-month losing streak' in its monthly K-line. As of the most recent trading day's close, Microsoft's stock price closed at $410.68 per share, with a total market capitalization of $3.05 trillion. In just four months, Microsoft's total market cap has evaporated by nearly $1 trillion.

Dramatically, Microsoft's accelerating stock price decline stemmed from a financial report considered the 'best ever.'

On January 29 (local time), Microsoft released its Q2 FY2026 financial results (ending December 2025). Data showed that in Q2 FY2026, Microsoft achieved revenue of $81.27 billion, up 16.7% year-over-year, 1% higher than market expectations; operating profit reached $38.28 billion, up 21% year-over-year; GAAP net profit hit $38.5 billion, up 60% year-over-year, primarily due to fair value changes from OpenAI's capital restructuring.

From a revenue breakdown, Microsoft's main businesses are divided into three segments: Microsoft Productivity and Business Processes (PBP), Intelligent Cloud, and More Personal Computing (MPC). The Intelligent Cloud business consists of server products and cloud services, mainly offering IaaS and PaaS services; the Productivity and Business Processes segment primarily provides SaaS products, including Office 365, Dynamics, and LinkedIn; the Personal Computing business includes Windows OS, gaming, hardware, search engines, and advertising.

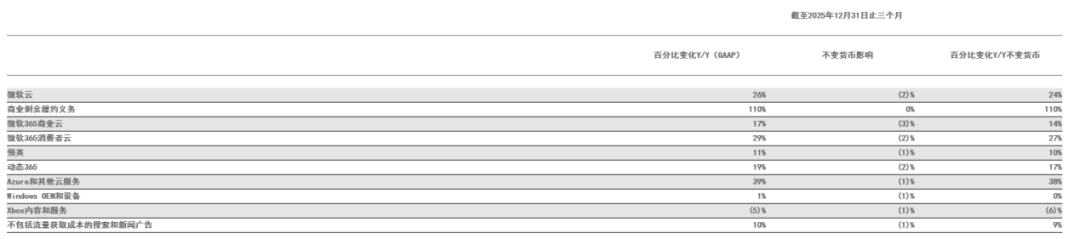

In Q2 FY2026, Microsoft's Intelligent Cloud business achieved revenue of $32.9 billion, up 29% year-over-year, slightly higher than analysts' expectations of $32.39 billion. Among this, Azure and other cloud services generated $25.6 billion in sales, up 39% year-over-year, with growth slowing by 1 percentage point from the previous quarter—the first decline in Azure cloud computing growth in nearly a year.

During the same period, Microsoft's Productivity and Business Processes segment achieved revenue of $34.12 billion, up 16% year-over-year; Microsoft 365 commercial cloud services revenue grew by 17%; Microsoft 365 consumer cloud services revenue grew by 29%; LinkedIn revenue grew by 11% year-over-year; Dynamics products and cloud services revenue grew by 19% year-over-year.

It is evident that both Microsoft's Productivity and Business Processes segment and Intelligent Cloud business maintained double-digit growth, with a very stable performance in their core businesses. However, due to poor sales of hardware products such as PC devices and Xbox consoles, Microsoft's Personal Computing and Devices business experienced negative growth this quarter. Financial results showed that this segment achieved revenue of $14.25 billion, up -3% year-over-year. From a revenue share perspective, Microsoft's personal business now accounts for less than 18% of the company's total revenue.

Despite multiple financial metrics exceeding market expectations, Microsoft's stock price experienced an 'epic plunge' after the earnings release. On January 29, Microsoft's stock price opened sharply lower, with intraday losses exceeding 12% at one point. By the close, Microsoft's stock price had plunged nearly 10%, marking its worst single-day decline since July 2013, with a single-day market cap evaporation exceeding $350 billion.

Some analysts believe that behind Microsoft's seemingly impressive revenue and profit figures lie many 'devilish details' often overlooked. First, Microsoft's highly watched Azure cloud services revenue growth slowed from 40% in Q1 to 39% in Q2, with growth excluding currency impacts at 38%—both declining by 1 percentage point from the previous quarter, raising concerns about slowing growth in its core business.

2

Microsoft Azure Falls Short of Expectations

Since Satya Nadella became CEO in 2014, Microsoft has established a 'mobile-first, cloud-first' strategy, fully committing to the cloud computing space. Since 2021, the cloud business has become Microsoft's largest revenue segment and the strongest driver of its performance growth.

In the past two years, strong AI demand has driven exceed expectations (unexpectedly strong) growth in Azure's business. In July 2025, Microsoft disclosed Azure's actual revenue for the first time. Data showed that for FY2025 (ending June 30, 2025), Azure revenue exceeded $75 billion, up 34% year-over-year. In Q1 FY2026, Azure cloud services revenue grew by 40% year-over-year, or 39% excluding currency impacts, holding steady from the previous quarter but slightly below some optimistic buyer expectations of 41%-42%.

Because Azure's growth did not outperform buyer expectations, Microsoft's stock price remained relatively stable after the Q1 FY2026 earnings release. However, the latest financial data showed that Azure's growth once again fell short of market expectations, with quarter-over-quarter growth slowing for the first time, triggering sell-offs by some investors.

More seriously, while Azure's revenue growth slowed, Microsoft's capital expenditure growth once again exceeded market expectations. Data showed that in Q2 FY2026, Microsoft's capital expenditures reached approximately $37.5 billion, up nearly $15 billion year-over-year and 9% higher than broadly market expectations. In the first half of FY2026, Microsoft's total capital expenditures reached $72.4 billion, primarily for purchasing short-life equipment such as AI data centers and servers.

With capital expenditures surging, signs of slowing revenue growth in the Azure cloud platform have raised concerns about Microsoft's ability to meet demand in the AI field. Over time, significant uncertainty remains about whether Microsoft's high capital expenditures will yield corresponding returns, becoming another key factor weighing on the company's stock price.

Fortunately, Microsoft's remaining performance obligations (RPO) continue to climb. Data showed that as of Q2 FY2026, Microsoft's RPO reached $625 billion, up about 110% year-over-year, with a weighted average term of approximately 2.5 years. About 25% will be recognized as revenue within the next 12 months, up 39% year-over-year. The remaining portion will be recognized as revenue after twelve months, up 15% year-over-year.

However, it should be noted that most of Microsoft's new orders this quarter came from OpenAI. Microsoft stated that about 45% of the contract value in its order backlog comes from OpenAI, with the remainder (including Anthropic's committed $30 billion) growing by 28% year-over-year.

However, since OpenAI is not yet profitable, whether these orders will materialize has raised doubts among some investors. Previously, Oracle was briefly hyped after receiving a massive $300 billion order from OpenAI, but its stock price ultimately only experienced a rollercoaster ride. Therefore, Microsoft's doubling of its order backlog has instead raised concerns among some investors about Microsoft's risk exposure.

3

End of the 'Honeymoon Period' with OpenAI

It should also be noted that after several years of a honeymoon period, the cooperative relationship between Microsoft and OpenAI appears to have undergone subtle changes. As early as early 2025, Microsoft announced that OpenAI would no longer rely solely on Microsoft's Azure cloud infrastructure and would be allowed to use computing resources from other competitors. Additionally, Microsoft approved OpenAI's plan to build additional computing capacity independently.

Public records show that OpenAI's AI training initially took place on Google Cloud. From 2019 to 2020, OpenAI paid Google $120 million in cloud computing fees, becoming one of Google Cloud's top five enterprise customers.

In March 2019, OpenAI established its for-profit subsidiary OpenAI LP and received a $1 billion investment from Microsoft. Afterward, OpenAI gradually migrated its cloud services from Google Cloud to Microsoft Azure.

In January 2023, Microsoft invested an additional $10 billion in OpenAI to further deepen technical cooperation. Under the agreement, Microsoft secured exclusive licensing rights to ChatGPT. Since then, all of OpenAI's computing needs have been supported by Microsoft's Azure cloud.

Benefiting from OpenAI's exclusive 'cloud authorization ,' Microsoft successfully integrated AI capabilities into Teams and the Office suite, marking a major breakthrough in the SaaS industry's business model. Meanwhile, Microsoft also integrated ChatGPT into its Azure cloud platform. Since then, Azure global enterprise customers could directly invoke OpenAI models on the cloud platform, enjoying Azure's trusted enterprise-grade services and AI-optimized infrastructure.

As global companies raced to train and deploy AI models, Azure became an indispensable computing infrastructure. Over the past two years, Microsoft has been virtually seen as the biggest winner in AI commercialization, a key factor behind its stock price surpassing $4 trillion.

However, as time passed, cracks gradually appeared in the close cooperative relationship between Microsoft and OpenAI. On one hand, OpenAI, which has been operating at a loss, urgently needed further financing, but Microsoft remained unmoved. Some analysts believe that as Microsoft executives grew increasingly concerned about whether their AI business relied too heavily on OpenAI, Microsoft began hedging its bets on OpenAI.

On the other hand, due to previous exclusivity agreements restricting OpenAI's ability to collaborate with other cloud providers and raise external funding, OpenAI continuously sought to modify its exclusivity agreement with Microsoft. Meanwhile, to reduce operational costs, OpenAI repeatedly attempted to negotiate with Microsoft to lower costs and allow it to purchase computing resources from other companies.

In response, even Microsoft CEO Nadella admitted in a rare interview in June 2025: 'Our cooperative relationship with OpenAI is changing.'

Ultimately, on October 28, 2025, Microsoft and OpenAI officially announced a major adjustment to their cooperation model. Under the new agreement, OpenAI is allowed to procure computing capacity from other cloud providers, and Microsoft no longer has the right of first supply. In return, OpenAI committed to purchasing $250 billion worth of Azure cloud services from Microsoft in the future, explaining the surge in Microsoft's remaining enterprise contract balance this quarter.

Additionally, the new agreement added clauses allowing OpenAI to co-develop products with third parties, but any API functionality developed by OpenAI would remain exclusively available on Azure, the only cloud service platform.

The latest news shows that on February 27, 2026, OpenAI announced the completion of $110 billion in financing, with a pre-money valuation of $730 billion. Among this, Amazon invested $50 billion, NVIDIA and SoftBank each invested $30 billion, while Microsoft did not participate in this funding round. From a equity structure (equity structure) perspective, Microsoft remains OpenAI's largest external shareholder, but its stake diluted from about 28% to 27%.

In return for Amazon's massive investment, OpenAI announced that it would grant AWS exclusive third-party distribution rights for its cutting-edge enterprise-grade Agent platform 'Frontier' and committed to consuming significant computing resources on AWS (including 2 gigawatts of Trainium chip computing capacity). Thus, OpenAI has shifted from relying solely on Azure to a 'multi-cloud' strategy, somewhat weakening Microsoft's core infrastructure position in OpenAI's ecosystem.

Overall, Microsoft Azure remains a key player in the cooperation between Microsoft and OpenAI and is still the exclusive cloud service provider for OpenAI's APIs. However, since Microsoft lost its right of first refusal as OpenAI's computing service provider, OpenAI will inevitably shift some of its cloud computing needs to other providers in the later stages. As a result, Amazon and Google have gained opportunities to catch up with Microsoft Azure in AI large models and related ecosystems. Clearly, this issue is far more serious than the slowdown in Azure's revenue growth and serves as a deeper reason for the sharp decline in Microsoft's stock price.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once