Short Drama Industry: 'Trapped' by Hongguo's Dominance

03/08 2026

03/08 2026

539

539

In March, the short drama industry was rocked by news: Several production companies, especially smaller ones, had their guarantee mechanisms revoked by Hongguo. The platform is now focusing on top-tier premium projects, while some mid-sized producers report that their teams were instructed to 'halt script selection' before the Spring Festival.

After just two to three years of rapid growth online, this development came as a complete shock.

Many industry insiders took to social media to vent their frustrations: 'Just started making money, and the rug got pulled out from under us.' 'Our company's projects have been slashed by at least half.' Some producers even lamented, 'Under current conditions, even if they resume operations, platforms will only provide scripts. Producers must self-finance and shoulder all risks.'

As of 2025, Hongguo has established partnerships with over 600 content institutions.

Why this sudden shift? The industry points to two primary factors: First, the past two years have witnessed reckless expansion in live-action short dramas, resulting in high output but a severe imbalance between quality and revenue. Second, the rise of comic dramas is directly impacting content costs, suggesting that Hongguo may be placing its bets on AI-driven short dramas.

Whatever the underlying motive, backed by ByteDance's ecosystem, Douyin's traffic, Tomato IP, and triple support from Doubao and Seedance AI, Hongguo already commands a dominant position in the short drama market. Its increasingly aggressive 'dominance' in the content sector demands attention not just within the industry but across the entire internet landscape:

Perhaps a traffic empire that firmly controls access to short dramas is emerging.

Production Companies on the Brink

'After two years in the short drama business, if we don't pivot now, it'll be too late,' said Zhang Miao (a pseudonym), a seasoned veteran in the field.

How many short drama companies are there? As of October 2025, over 350,000 short drama-related enterprises are operating nationwide, covering the entire industry chain—from upstream IP rights holders and midstream production companies to downstream distribution and playback platforms. Midstream firms dominate, accounting for over 70% of the chain.

The short drama boom over the past two years has led to a surge in production companies, primarily due to Hongguo's full-fledged support since 2023. Back then, Hongguo even provided upfront payments to guarantee returns. Blockbuster hits earned producers hefty profit shares, with top teams raking in tens of millions monthly in 2024.

In other words, during the industry's heyday, many producers secured a slice of the pie through guarantees alone.

Times have changed. Since November of the previous year, Hongguo has been gradually phasing out guarantees for producers. The cooling of the live-action short drama market—not just due to overcapacity and declining revenue—is closely tied to the rise of AI comic dramas. In February, the top 100 comic dramas saw a staggering 7.587 billion increase in playbacks, up over 20% month-on-month.

Currently, Hongguo releases around 2,000 new comic dramas daily—20 times the number of live-action dramas. It's also incubating a dedicated comic drama app. QuestMobile data reveals that just one month after launch, 'Hongguo Comic Drama' reached 8.54 million MAU, ranking among the top three short drama apps.

Incentives once reserved for live-action short dramas now favor comic dramas.

In January 2026, Douyin categorized AI live-action drama scripts into four tiers (S+, S, A+, A), offering up to 80,000 yuan in guarantees and a 20% permanent revenue share. Meanwhile, dynamic comic commentary coefficients dropped to 5x, and static ones to 1x. This marks a formal shift toward AI live-action dramas within the comic drama track, once dominated by silly/dynamic comics.

Market data confirms this trend. DataEye's February top 100 comic drama list shows that AI simulated human short dramas account for nearly 60%. While comic and live-action dramas once complemented each other, AI-driven comic dramas are now indirectly replacing traditional live-action ones.

Some players in the short drama industry chain are already feeling the chill.

Take actors, for example. Detawen Film & TV predicts that by 2026, over half of short drama actors will be phased out as ByteDance and Tencent develop exclusive virtual actors—zero salaries, zero scandals, and available 24/7. For producers, AI simulated human short dramas offer lower costs and higher output. If platforms shift resources to AI, mid-sized producers will be forced to pivot or exit the market.

Zhang's team halved its staff after the Spring Festival to transition into AI comic dramas.

But are cost-free comic dramas truly easy to produce?

AI comic dramas rely heavily on a 'gacha'-style generation model, where each output incurs real costs. For example, Google's Veo 3 charges $6 per 8-second, 720P clip; MiniMax's Conch AI sparked controversy with its 10,788 yuan/year 'Premium' membership. Model calls, rendering, subscriptions—rigid costs persist.

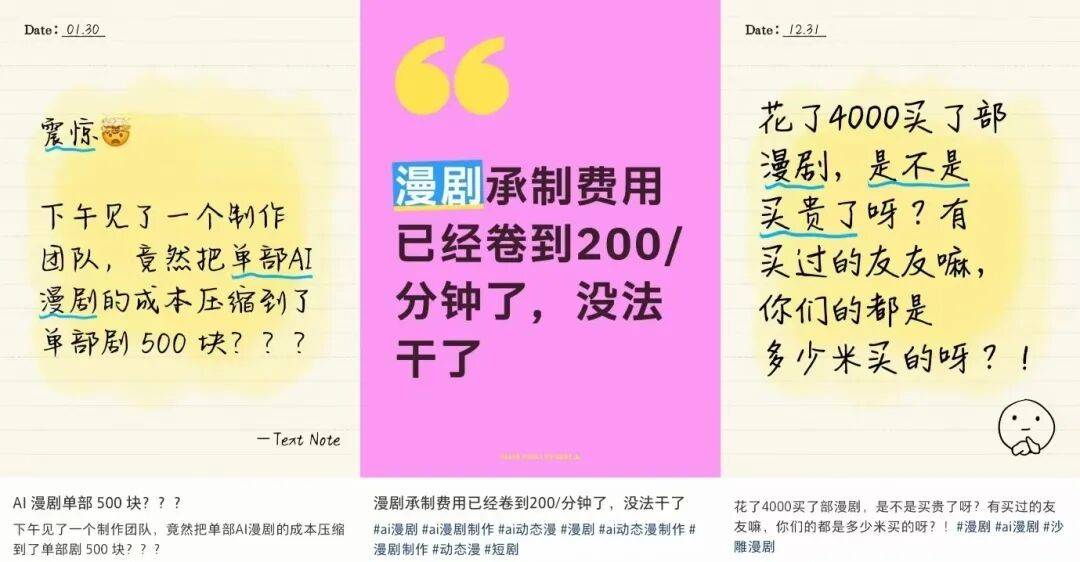

Second, AI enables lightweight operations, forcing gacha artists, animators, and small production teams into low-price competition. According to Time Weekly, AI comic drama production rates plummeted from 3,000-5,000 yuan/minute in 2024 to 500-1,000 yuan today, with some teams bidding as low as 200 yuan/minute.

Uneven platform traffic distribution further shatters producers' profit hopes.

From June to August 2025, the top 100 comic dramas dominated traffic. In August, they accounted for over 80% of total playback increases, with just 8 titles (0.4%) exceeding 100 million views. Meanwhile, 64% of comic dramas had under 1 million cumulative views.

Amid this content revolution, only platforms consistently profit.

Tech Planet reports that Hongguo's short drama revenue may surpass 15 billion yuan in 2025. With AI, capital reaps even greater rewards: Jimeng AI boasts over 20% user payment conversion and 20 million yuan in monthly GMV; Kuaishou's Kling AI has over 60 million global users, generating over 250 million yuan in Q2 2025.

Others—producers, creators, workers—will merely become collateral damage in the industry's transformation.

Killing the Competition with Traffic

Hongguo's DAU recently surpassed 100 million, becoming ByteDance's fifth '100-million-user' app.

Hongguo borrowed Tomato Novels' ad-for-content model, boosting users from 300,000 to 10 million. Its MAU now exceeds Bilibili, Youku, and even Xiaohongshu.

Beyond its model, Hongguo's 'killer move' is traffic. Leveraging Douyin and Tomato, supplemented by channels like Pangle Alliance, Xigua Video, and Toutiao, its multi-dimensional traffic matrix effectively reaches users—especially through Tomato and Douyin.

While Tomato supplies content to Hongguo, it also serves as a massive traffic pool, much like Douyin. In H1 2025, 12 Hongguo short dramas exceeded 1 billion views, with 10 adapted from Tomato Novels.

In the long-video era, IPs came with built-in fan bases—a principle that still applies to short dramas.

Douyin's role is even more critical. Sina Finance reports that over 60% of Hongguo's early users came from Douyin referrals, with this ratio remaining above 55% in early 2026. This ByteDance ecosystem synergy significantly reduces Hongguo's customer acquisition costs (CAC).

Tonews data reveals that Hongguo's CAC is just 1/5 of the industry average. A well-promoted new drama often hits 1 million views within 24 hours. Even during paid phases, Hongguo achieves a 13.2% payment rate—5x the industry average—with a lifetime user value of 80 yuan.

Douyin 'feeds' Hongguo with traffic, while Tomato provides content—a duo that dictates Hongguo's growth pace and long-term competitiveness. This forms a 'traffic-secure, content-abundant' advantage, further squeezing smaller platforms and producers.

However, this seemingly flawless business logic isn't foolproof. Hongguo's traffic abundance fosters content innovation laziness.

Protected by ByteDance's traffic, the platform neglects originality, favoring 'multiple adaptations' and 'homogeneous remakes.' *Excessive Wilderness* had 8 versions, *My Kept Man Is the Beijing Elite* had 12, and female-frequency hit *Peach Blossom Horse Seeks Long Spear* even spawned a gender-swapped edition. In 2026, *Sheep and Orchid*, with over 50 million in popularity, launched both live-action and AI comic drama versions.

Moreover, Hongguo's script approval rates have plummeted.

Media estimates suggest the industry's overall approval rate has dropped to ~20%, with adapted works faring much better than originals. Platforms prefer proven Tomato IPs with built-in fanbases and traffic, which align perfectly with Douyin's algorithm for initial exposure and conversions.

Simply put, Hongguo—now the sector's undisputed leader—prioritizes traffic in content selection. In the AI comic drama era, this logic may intensify. Among H1 2025's top comic dramas with over 10 million views, 70% were adapted from top IPs, with original fans contributing 60% of initial traffic.

This worries producers:

Will platforms build their own script libraries and distribute standardized scripts, reducing producers to mere contract manufacturers? With IP scarcity broken and values rapidly declining, platforms can bypass original screening and copyright negotiations, controlling everything from scripting to distribution.

Producers would then become pure content contractors, with platforms dominating entirely.

Is the Sector's Endgame 'Free'?

Despite efforts to catch up, rivals haven't surpassed Hongguo, largely due to its free model.

Today, paid models are fading in content, both among users and businesses.

On the user side, young audiences favoring free short dramas now snub paid long dramas and nested-membership long-video platforms. In 2025, the top 20 long dramas amassed 29.6 billion views—down 20% YoY.

Meanwhile, iQIYI, Youku, Tencent Video, and Mango TV have lost steam. QuestMobile shows that Hongguo users averaged 2.01 daily hours in October 2025—surpassing the 'Big Four' long-video platforms—directly hitting their profits.

Take iQIYI: In H1 2025, revenue fell 9% YoY to 20.5 billion yuan; Q3 revenue dropped 8% to 6.68 billion yuan, with a 250 million yuan loss. Its core membership business earned 4.21 billion yuan in Q3—down 4% YoY.

On the business side, brands have favored custom short dramas for years.

The *2025 Q3 Media Industry Report* shows that as of August 2024, 'free' short videos dominated ad spending (38.8%), while 'paid' online videos accounted for just 3.1%. By H1 2025, 149 brands ventured into micro-short drama marketing, with 52% (77 brands) being first-timers. If brands continue shifting budgets to free short dramas (comic dramas) in 2026, will the entire content sector embrace 'free'?

Some players are already acting accordingly.

Tencent launched 'Fire Dragon Comic Drama,' a 'free-to-watch' app, mirroring Hongguo's strategy. iQIYI and Youku added prominent comic drama sections, embracing the free trend. By late 2025, iQIYI had 20,000 short dramas, with free content exceeding 70%.

DataEye estimates that free short dramas will capture ~2/3 of the micro-short drama market.

Interestingly, user surveys show that ~20% of China's ~400 million micro-short drama DAUs watch pirated content via platforms, browsers, and cloud drives. Redirecting this traffic could yield over 20 billion yuan in incremental revenue—still through low-barrier free models.

Undeniably, user choice, monetization, and competition all point to 'free' as content's likely endpoint. Hongguo capitalized on this trend first. Can rivals like iQIYI, Youku, and Tencent catch up?

Despite Hongguo's growth, Tonews reveals that its user retention rate dropped from a peak of 58% to 42%, with single-episode completion rates down 17 percentage points YoY. Its recent reforms aim to address this.

However, as the sector shifts to free, competition will escalate from model battles to traffic, IP, AI output, and ecosystem clashes. Whether anyone can dethrone Hongguo remains uncertain. In this game, you either devour Hongguo or get pushed out.

There seems little room for a third option.

Dao Zong You Li (formerly Weidaodao), a new media outlet covering internet and tech. This is an original article. Any reproduction without retaining author information is prohibited.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once