Is Baidu Bidding Farewell to Search? Its Financial Report Undergoes a Major Shift: No More Mention of Ad Revenue, Fully Embracing AI’s New Era

03/06 2026

03/06 2026

463

463

Introduction: Smart Cloud Leads as Baidu’s AI Journey Enters a New Phase

Recently, Baidu released its financial report for the fourth quarter and full year of 2025, marking a pivotal moment in its strategic evolution.

In this latest report, Baidu redefines its core business as "Baidu General Business," encompassing its core AI innovations, traditional operations, and other ventures.

The traditional segment primarily involves advertising services across search, information feeds, and other product lines.

Notably, the financial report featured two significant milestones:

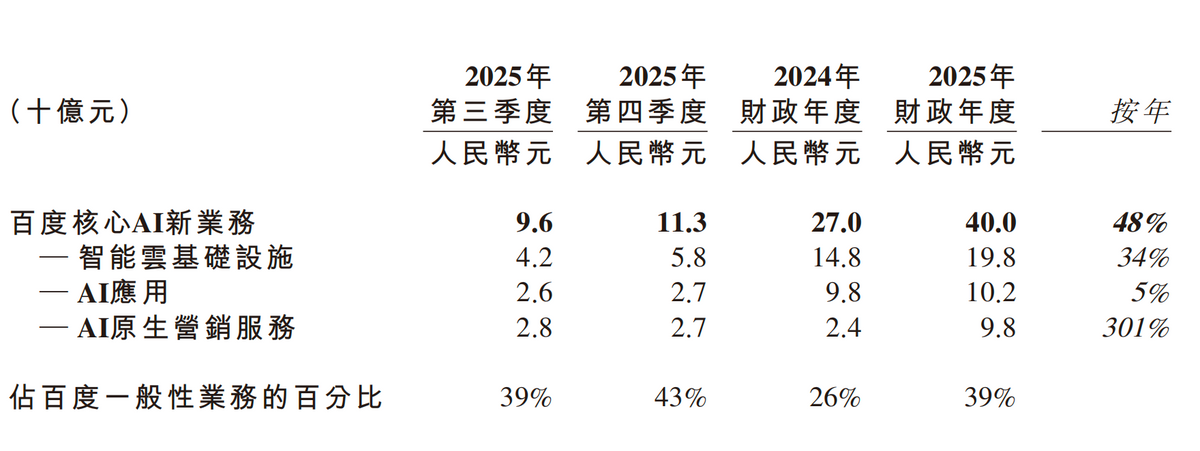

First-ever disclosure of AI revenue proportion: In 2025, Baidu’s AI business revenue soared to 40 billion yuan, marking a 48% year-on-year increase. In the fourth quarter alone, AI revenue accounted for 43% of Baidu General Business revenue, with total quarterly revenue reaching 32.7 billion yuan.

First time omitting online marketing revenue: Previously on a six-quarter decline, with the rate worsening from 2% to 18%, this revenue stream was notably absent from the report.

The contrast is stark: one segment surging, the other fading, with the latter still holding a slight edge in overall impact.

For the full year, Baidu’s total revenue stood at 129.1 billion yuan, down 3% year-on-year, primarily due to the contraction in traditional business, partly offset by growth in its core AI innovations. Net profit attributable to Baidu plummeted to 5.6 billion yuan, a 76% decline.

After a decade of ‘All in AI,’ Baidu’s transformation is far from over.

I. Smart Cloud Spearheads Baidu’s Accelerated Transformation

A closer look at the financial report reveals that Baidu’s performance challenges stem more from proactive adjustments than operational missteps.

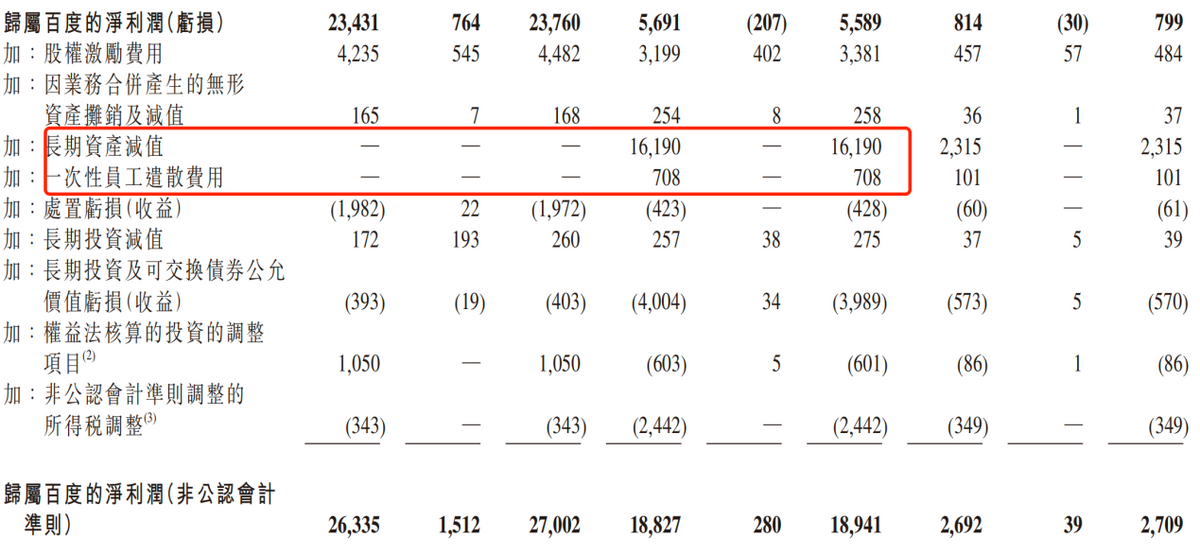

In Q3 2025, Baidu took a one-time impairment charge of 16.19 billion yuan on long-term assets. For the full year, it incurred 708 million yuan in one-time employee severance costs.

These moves directly impacted Baidu’s reported profits, with the asset impairment turning operating profit negative.

The impairment primarily targeted outdated traditional equipment. Baidu executives explained, “We’re accelerating investments in cutting-edge AI computing, necessitating a comprehensive review of our infrastructure. Some assets no longer meet today’s efficiency standards.”

Staff optimizations were also efficiency-driven.

According to China Entrepreneur, in late November 2025, Baidu undertook its largest staff reduction in years, offering affected employees a ‘N+3.5’ severance package.

The MEG division saw the most significant adjustments, affecting user growth and security platforms, while AI and cloud-related departments remained relatively unscathed.

These bold moves underscore Baidu’s commitment to slashing non-core operations and focusing on AI.

Combined with shifts in financial disclosures and recent publicity efforts, it’s clear Baidu is eager to shed its traditional image and fully embrace AI’s new narrative.

Public opinion generally views Baidu’s AI performance as exceeding market expectations.

Structurally, of the 40 billion yuan in revenue from Baidu’s core AI innovations in 2025, smart cloud infrastructure contributed nearly half, growing 34% year-on-year and 38% quarter-on-quarter in Q4.

AI-native marketing services saw explosive growth, up 301% year-on-year.

AI application revenue remained stable, with a 5% year-on-year increase.

Quarterly trends showed only smart cloud infrastructure maintaining rapid Q4 growth (38% QoQ). AI applications and AI-native marketing services were flat compared to Q3, with the latter even declining slightly.

The Robotaxi business remains a standout feature for Baidu. As of February 2026, Luobo Kuaipao operated in 26 cities globally, delivering over 20 million autonomous rides and accumulating over 30 million kilometers, including 19 million fully driverless kilometers.

According to National Business Daily, Baidu achieved per-vehicle break-even in Wuhan in Q2 2025.

However, from a revenue standpoint, with just over 20 million cumulative orders—even at 20 yuan per order—total revenue would barely exceed 400 million yuan, a negligible fraction of Baidu’s overall revenue.

In the short term, Luobo Kuaipao serves more as a brand showcase than a revenue pillar.

Thus, Baidu’s most promising AI segment remains smart cloud infrastructure.

Baidu Smart Cloud stands out as one of the few cloud providers globally with full-stack AI capabilities across four layers: chip, framework, model, and application. This positions it competitively in terms of adaptability and cost-effectiveness.

According to China Daily, Baidu Smart Cloud led in large model-related bid wins and total bid value in 2025, securing the top spot for two consecutive years.

In January 2026, Baidu announced plans to spin off Kunlunxin for listing, boosting market expectations.

Tianyancha APP data shows Baidu’s total market value at 322.595 billion Hong Kong dollars as of March 3, 2026.

Contrasting Fortunes: AI Soars, Advertising Declines

While Baidu’s AI business thrives, its advertising segment faces a downturn.

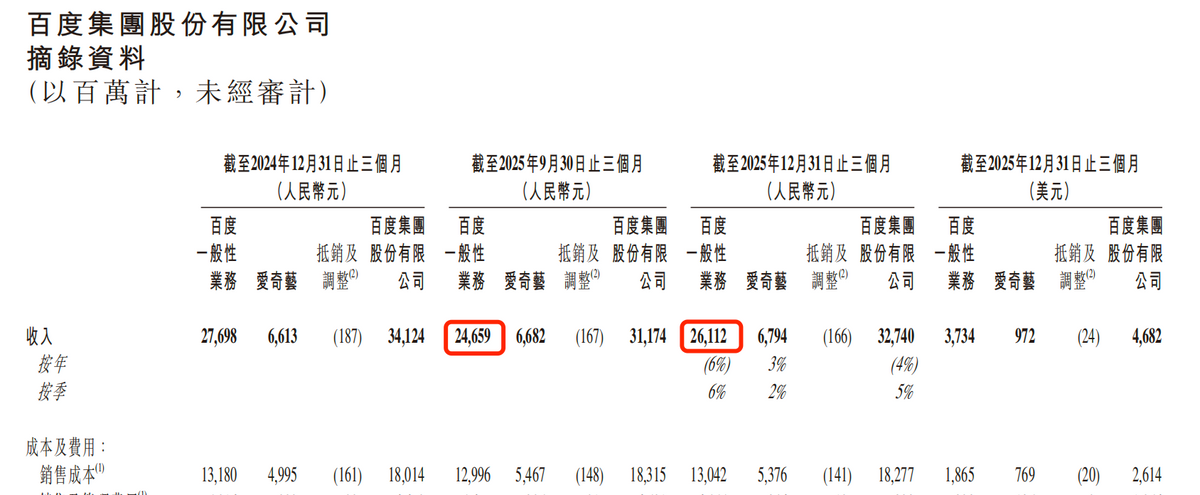

Though the financial report no longer breaks down online marketing revenue, reverse calculations show traditional business (led by advertising) declined from 15.1 billion yuan in Q3 2025 to 14.8 billion yuan in Q4.

With Baidu allocating more resources to AI, traditional business may face an even tougher road ahead.

Financial data reveals Baidu APP’s monthly active users dropped from 708 million in September 2025 to 679 million in December, suggesting a rebound may still be distant.

However, a silver lining emerges: Baidu General Business revenue rose from 24.659 billion yuan in Q3 2025 to 26.112 billion yuan in Q4.

This indicates that AI revenue growth in Q4 2025 more than offset the advertising decline, with room to spare.

Meanwhile, Baidu’s operating cash flow turned positive in H2 2025, totaling 3.9 billion yuan.

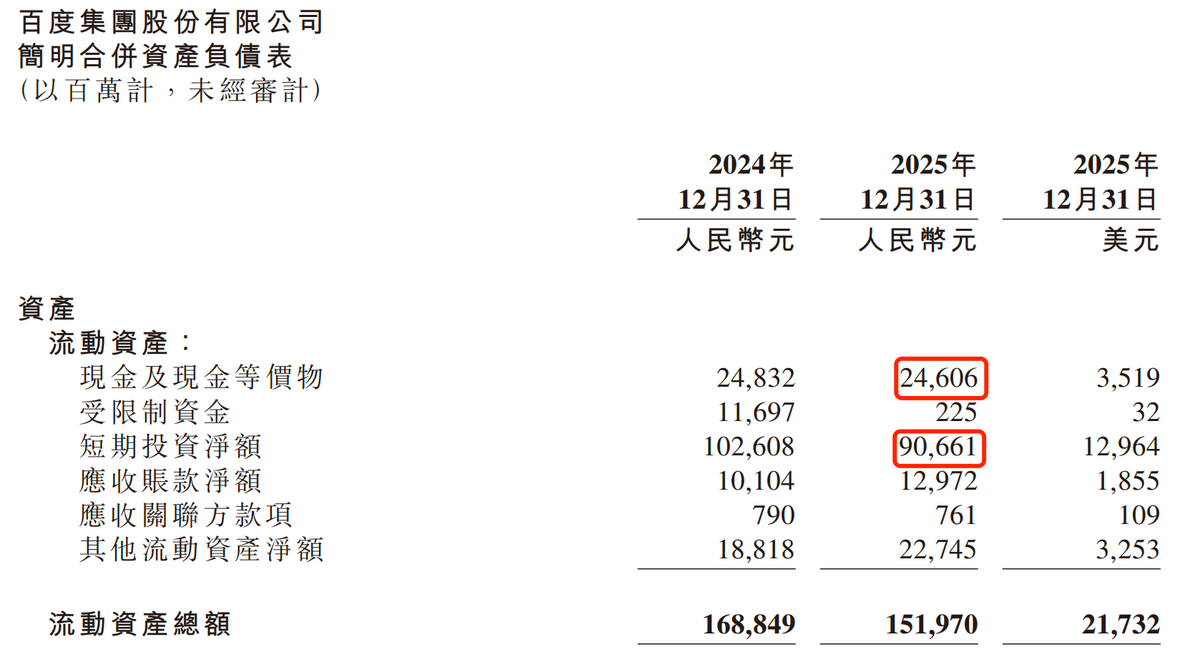

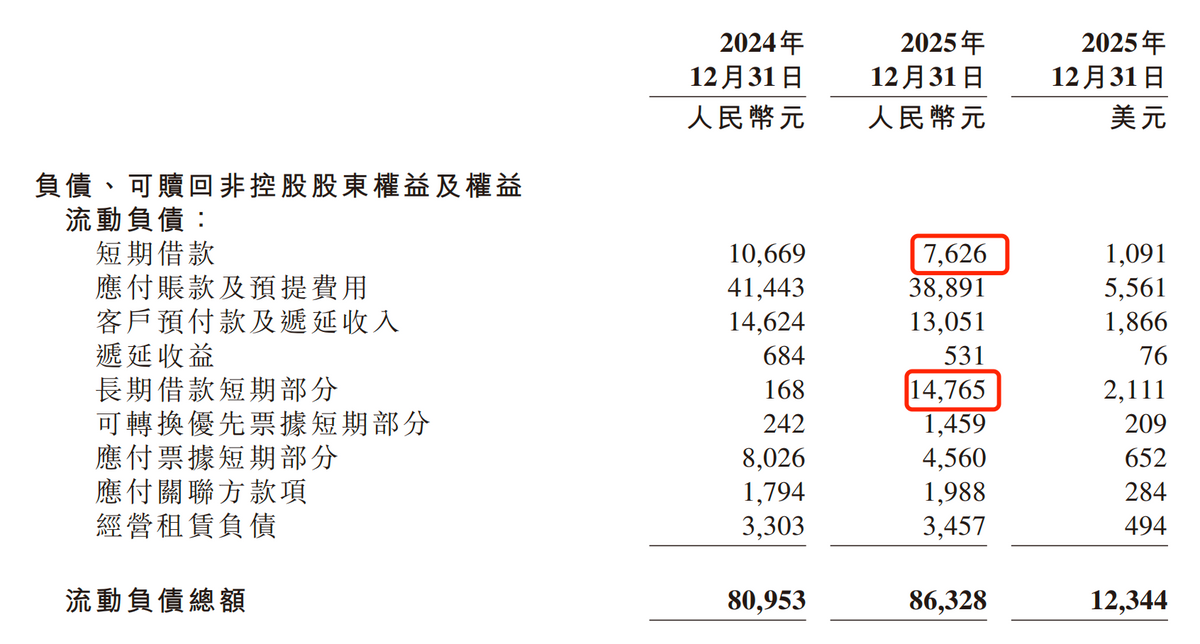

As of December 31, 2025, Baidu held 24.606 billion yuan in cash and equivalents and 90.661 billion yuan in net short-term investments.

Liabilities included 7.626 billion yuan in short-term borrowings and 14.765 billion yuan in short-term portions of long-term debt.

Subtracting these leaves 92.876 billion yuan, indicating Baidu’s financial health remains robust despite the advertising slump.

Ample funds provide strategic flexibility, giving Baidu confidence to double down on AI.

Yet, this doesn’t mean risks can be ignored.

II. A High-Stakes ‘All-or-Nothing’ Gamble

While many tech giants are investing in AI, few have gone all-in like Baidu.

Tencent leverages WeChat’s massive traffic, but Yuanbao leads its AI charge. Alibaba pours resources into AI, yet Taobao and Tmall remain its core.

Google, though a leader in AI with Google Cloud and Gemini, still relies on advertising for over 70% of its revenue.

Even Elon Musk, while championing Robotaxi and humanoid robots, bases his confidence on Tesla’s sales.

Baidu’s approach—upgrading equipment and conducting large-scale layoffs—reflects a ‘all-or-nothing’ mentality, as if sacrificing its core business is justified for AI’s success.

While courage is commendable, is it premature to go all-in?

Despite Baidu’s AI prowess, its brand identity remains tied to search, much like WeChat is to Tencent and Taobao to Alibaba.

User perception, though intangible, is invaluable. For instance, many still shop on Taobao out of habit, despite Pinduoduo’s lower prices.

In AI, no player dominates user perception yet, meaning the race is wide open.

Currently, the AI competition remains an uncertain gamble.

According to LatePost, during the 2026 Spring Festival ‘10 Billion AI Red Packet War,’ ByteDance’s Doubao leveraged CCTV Spring Festival Gala interactions to achieve over 1.9 billion engagements on New Year’s Eve. Its DAU surged to 200 million, stabilizing at 150 million post-festival.

Tencent’s Yuanbao, integrated into WeChat, saw red packet MAU exceed 110 million, with DAU topping 50 million.

Alibaba’s Qianwen acquired over 100 million new users via 3 billion red packets, peaking at 73 million DAU and embedding AI into e-commerce and local services through ‘free orders for referrals.’

In contrast, Baidu’s Wenxin Yiyan was barely noticeable in this consumer-facing battle. Official data showed Baidu Wenxin Assistant’s MAU quadrupled year-on-year post-campaign.

In B2B services, Baidu faces stiff competition from Alibaba Cloud and Huawei Ascend, with outcomes still unclear.

Moreover, the AI race is far from over, and ‘black swan’ events like DeepSeek’s rise could disrupt again. Victory isn’t guaranteed by investment alone.

Secondly, traditional search isn’t obsolete yet.

Before AI eliminates hallucination risks, traditional search engines’ traceability and transparency remain irreplaceable. For example, analyzing financial reports still requires raw data from official sources, not AI summaries.

Additionally, search’s value lies beyond efficiency—serendipitous discoveries during leisurely browsing are hard to replicate with AI.

As long as use value persists, commercial value won’t vanish.

Data shows Google’s search ad revenue hit $63.1 billion in Q4 2025, up 17% year-on-year, accelerating growth.

Industry insiders note, “AI hasn’t ‘killed search’; it’s expanded the traffic and ad ‘pie’ in real terms.”

Thus, while AI’s impact on search is debated, it’s unlikely to happen immediately.

If Baidu optimizes search and rebuilds trust, its advertising business could stabilize and rebound.

Unfortunately, with resources now focused on AI, this possibility dims.

Still, Baidu Search remains powerful, contributing over half of revenue.

Robin Li noted in an interview that he entered search before Google’s founders, and his patented hyperlink analysis—a cornerstone of modern search engines—predates Google’s.

Perhaps, like Google, Baidu’s search could be reborn with AI enhancements.

Disclaimer:

This analysis is based on publicly available information (financial reports, announcements, etc.). The author doesn’t guarantee the completeness or timeliness of sources. The stock market involves risks; principal may be lost. Investment decisions require extreme caution. All views here are the author’s opinions and not buy/sell recommendations. Investors must conduct independent research and exercise prudent judgment, bearing all risks themselves.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once