One Year Since the Food Delivery War: No More Subsidies or Hype, Just Meituan Falling Short on AI

03/13 2026

03/13 2026

640

640

PART01

After the Subsidies Faded

Wanting to order bubble tea, you switch between several apps but balk at the high prices. This is a common feeling for many returning to work after the Spring Festival holiday.

It’s not just bubble tea. The ¥10 coffees and ¥15 lunch deals that were once common on food delivery platforms have quietly disappeared. In some regions, delivery fees remain stubbornly high, making you wonder if the Spring Festival holiday—with its tight delivery capacity—is still in effect. Someone calculated: A bowl of potato noodles costs ¥12–15 in-store but ¥24 on a delivery app. Add in the delivery fee, and the total nears ¥30—“enough for two people to dine in.”

A key reason behind this is the reduction in platform subsidies. “None of the three are fighting as hard anymore,” a restaurant owner in Changsha told me. Subsidies dropped noticeably after the holiday, with one platform ending them entirely much earlier.

It feels like a different era. A year ago, the food delivery war erupted. JD made a high-profile entry, Meituan defended its turf, and soon Alibaba struck with its Taobao Flash Sales. Alibaba’s determination during this period made you wonder if the company, which had just proclaimed itself AI-driven, was actually becoming delivery-driven.

A year later, both the hype and the subsidies are gone.

The food delivery war was once dubbed “the internet’s last hand-to-hand combat,” but in hindsight, the market landscape hasn’t substantially changed after ¥100 billion in subsidies were burned. Meituan remains first, Alibaba second, though the gap between them has narrowed.

It seems like a war without winners.

Meituan’s stock price and profits have taken a hit. Since March 2025, its market cap has shrunk by over HK$600 billion. Its food delivery business, once considered an impenetrable moat, now looks less secure under Alibaba’s fierce assault.

Profit-wise, Meituan enjoyed comfortable days with nearly ¥100 million in daily net profit in 2024. But by 2025, it fell from heaven to hell, reporting an annual loss of about HK$25.6–26.7 billion. Its core local commerce segment swung from a ¥57.7 billion profit to a ¥7.5–7.7 billion loss.

Meituan's Hong Kong stock price has continued to decline since the start of the year

Every discounted coffee we ordered from Meituan may have mixed a bit of Wang Xing’s bitterness.

Alibaba’s victory is also a bloody one. At its peak, Taobao Flash Sales lost ¥4–5 per order. While Alibaba is vast, its aggressive tactics led to soaring marketing costs and plunging operating profits. It remains to be seen how many users truly adopted Taobao for shopping by chasing delivery deals.

After all, expecting loyalty from food delivery consumers, streaming service members, or disloyal partners is like talking to a brick wall. Once subsidies faded, some users who had switched to Taobao Flash Sales during the war lamented: The habit of “opening Meituan whenever I crave delivery” is back.

No need to feel sorry for Jiang Fan.

With Alibaba clearly scaling back Flash Sales investments starting in Q1 2026, he likely saw this short-term outcome coming. For Alibaba, any sub-battlefield and individual ambitions must yield to corporate strategy. As Jiang Fang, Alibaba’s Chief People Officer, put it: “We don’t put anyone on a pedestal.”

PART02

Pivoting Rivals

Alibaba’s AI ambitions are so intense, you’d almost forget it’s an e-commerce company.

In the past six months, Alibaba’s AI ads are everywhere: Airport jet bridges proclaim “AI Starts with Alibaba Cloud,” bus stops and elevators loop ads for Alipay’s Afu and Jackson Yee promoting QianWen App, while stations and subways are plastered with promotions.

Ad fatigue is real, but compared to food delivery, Alibaba’s AI push feels like serious business.

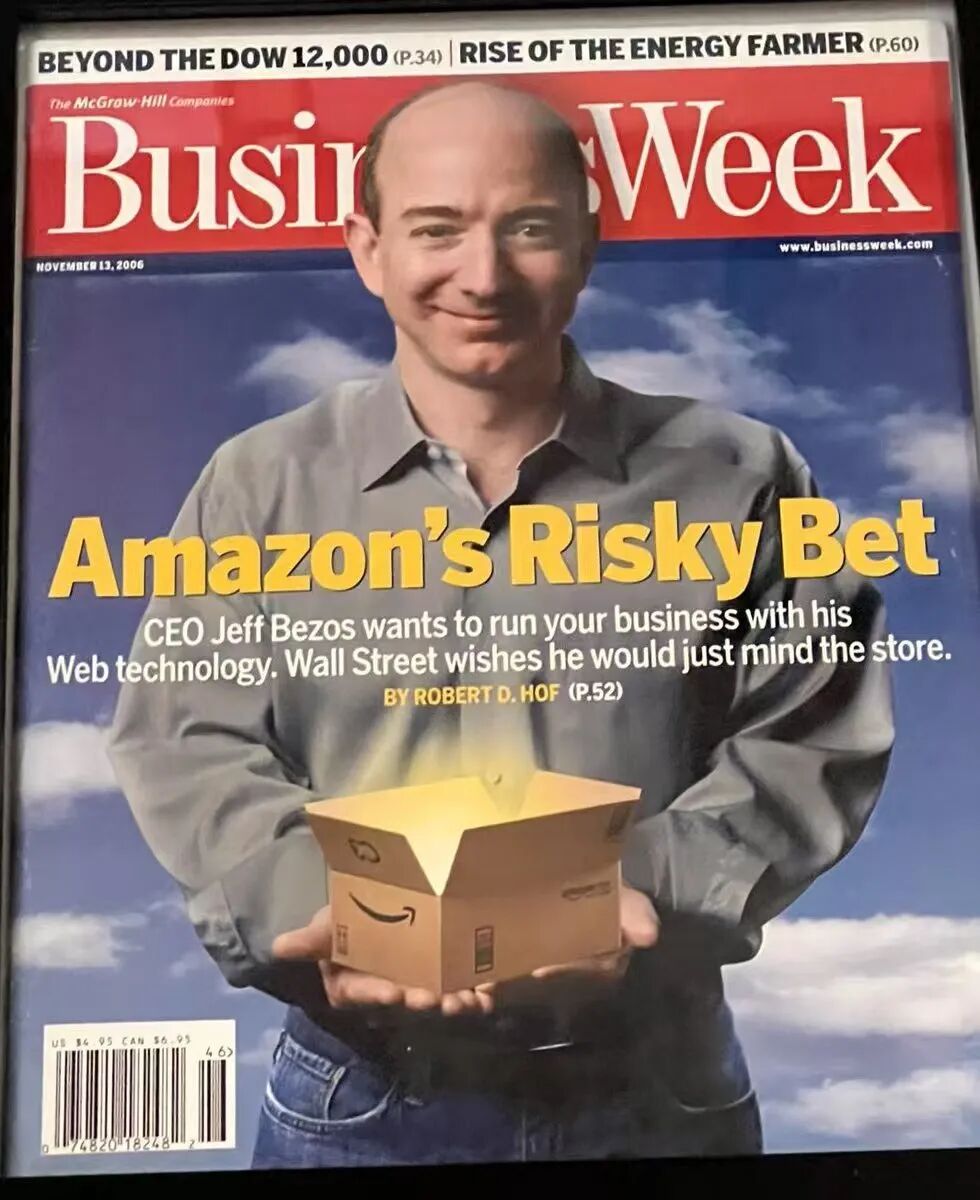

This follows Amazon’s path. AWS, launched in 2006, was mocked by Wall Street as “Bezos’s money-burning fantasy.” Today, as the global cloud leader and largest AI computing provider, AWS is Amazon’s cash cow: generating ~1/3 of revenue and over 70% of profits. It transformed Amazon from a boring e-commerce firm into a computing power seller—same sales, but vastly different margins and growth.

BusinessWeek’s iconic 2006 cover featured Jeff Bezos and AWS, labeling it a “risky gamble”

Alibaba “copied the homework” early. Alibaba Cloud launched in 2009 and lingered in obscurity until upgrading to Alibaba Cloud Intelligence in 2018. By 2024, it stood alongside e-commerce as one of Alibaba’s two core businesses. In FY2025, it contributed ¥118 billion in revenue (11.8% of group total), second only to China e-commerce. Profit contribution was lower, at ¥10.6 billion (6.8% of group).

In short, Alibaba’s AI + cloud revenue is high, but so are costs. To tell a “growth” story, Alibaba highlights another metric: As of Q3 2025, revenue from AI-related Alibaba Cloud products had grown triple-digits YoY for nine straight quarters.

Profit matters. Sustained, higher profits matter more. Alibaba’s AI business is now entering the “results” phase. The recent Lin Junyang resignation controversy essentially pitted individual open-source idealism against corporate commercial strategy.

Confront reality or chase ideals? Interpretations of Alibaba’s food delivery pivot vary.

From Meituan’s perspective, the AI and Agent craze, coupled with ByteDance’s knack for disruptive moves, forced Alibaba to exit food delivery and focus on AI. But Alibaba claims it never strayed from AI, using food delivery as a high-frequency scenario to accelerate AI adoption and data accumulation.

So, was the real target never food delivery? Was hurting Meituan just collateral damage?

That stings even more.

Of course, Meituan has bigger concerns. While the food delivery war quieted, it kept busy with preparations: Offensively expanding its fastest-growing instant retail business by acquiring Dingdong Maicai’s China operations for $717 million, boosting fresh produce hubs to ~2,000; accelerating offline store openings like discount chain Happy Monkey and larger-format Xiang Supermarket to enrich its supply chain.

Meituan's offline discount store Happy Monkey. Source: Social media

Looking back, Meituan’s instant retail ambitions may have sparked the 2025 food delivery war.

One theory: Meituan’s expansion into 3C, apparel, and daily essentials provoked JD and Alibaba to target its food delivery business. It sounds like schoolyard turf wars, but sometimes business battles are that straightforward. The grand narratives are just face-saving rationalizations.

Why did Meituan pursue instant retail? Simple: Retail can spawn trillion-dollar companies like Walmart, but food delivery likely cannot.

Gruubhub, the 2004 food delivery pioneer, was acquired by Europe’s Just Eat Takeaway (JET) for $7.3 billion in 2021, then dumped three years later for $650 million—a terrible asset. The most valuable global food delivery firm, DoorDash, is worth ~$73 billion, a fraction of Walmart’s market cap.

DoorDash’s U.S. food delivery business

Stuck with a 3% profit margin in food delivery, Meituan needed a new story. Domestic e-commerce growth had peaked, pressuring Alibaba to do the same. Alas, when these two companies with similar needs clashed in food delivery, they showed no mercy. Last summer, they pushed young workers at overloaded cold drink shops to their limits.

PART03

AI: The Unmissable Trend

Trends and bubbles often look alike.

OpenClaw’s recent “lobster craze” in China exemplifies this. Some see it as the future; others dismiss it as a modern-day “qigong fad.” When indistinguishable, anxiety sets in. Humans hate losses—psychologists Kahneman and Tversky argue that losses hurt 2–2.5x more than gains feel good. Thus, many prefer acting wrongly to risking missing out.

Meituan seems unbothered.

Though Wang Xing insists Meituan’s AI strategy is “offensive,” not “defensive,” its overall approach feels cautious.

Meituan began developing its Large Language Model, LongCat, in 2023—soon after ChatGPT’s debut—but Wang Xing only announced it in March 2025. Meituan’s AI investment remains in the tens of billions, dwarfed by Alibaba and ByteDance’s hundred-billion-dollar commitments.

In a era of trends and bubbles, caution is safe. Meituan isn’t Alibaba; it can’t afford to burn cash recklessly. Yet this leaves Meituan’s AI in an awkward spot:

Some success, but not much.

At least, consumers barely notice. From “Agent Xiao Mei” as a lifestyle assistant to built-in “Ask Xiaotuan” and the recently launched AI browser Tabbit, none have gained much traction. The only buzz came from Tabbit’s plagiarism allegations—a sign of human fascination with scandal, not importance.

Tabbit’s plagiarism controversy and official response after launch

Meituan has a ready defense. As Wang Puzhong, CEO of Meituan’s core local commerce, emphasized in October 2025, Meituan’s AI focuses on practical dining and local life operations—like using AI for merchant site selection, product choice, and pricing.

With LongCat-powered Kangaroo Advisor, merchants can boost site selection accuracy to 87%. Meituan likely has many such cases.

Improving operational efficiency via AI to better serve consumers is Meituan’s AI logic. Unlike Alibaba’s aggressiveness, Meituan prioritizes defending its turf. It’s not sexy, but for a business, that’s fine.

As Sam Walton noted: “Walmart’s success isn’t because I’m smart, but because we consistently do what’s right—save customers money.” Yet Walmart also evolved, embracing e-commerce. Its online revenue topped $150 billion in 2026, accounting for 23% of global sales. Thanks to Sam’s Club, China’s e-commerce share exceeded 50%.

Still think it’s a rigid old retailer?

Hold firm, embrace change—that’s how most companies survive cycles. But first, they must recognize the need to change.

For Meituan, Alibaba’s food delivery “pivot” is a signal.

AI, including Agents, may redefine many businesses. Jensen Huang recently predicted: Traditional software and apps could fade in coming years. AI Agents will likely dominate. Humans set goals; Agents break them into tasks, use tools, and execute.

This implies stronger disruption than the internet or mobile eras, which mostly migrated offline content/services online or from PCs to phones. AI Agents will reconstruct everything.

First to lose meaning: DAU. This makes the 2025 food delivery war seem pointless—its core was fighting for traffic to boost app DAU.

If the foundation crumbles, why keep the old house?

For Meituan, if AI dominates phone screens, its traffic acquisition and monetization models must evolve. Its moat needs rebuilding. If it stays comfortable in “dining AI” for merchants, it may soon face an even tougher rival: itself.

Historically, Meituan hasn’t been passive. It survived rounds of competition by calculating costs and launching rational offensives.

Thus, Meituan’s 2026 focus will likely remain instant retail and AI. The former will expand SKUs, prioritizing high-margin categories like baijiu, branded tea, and 3C for profitability—even if this sparks new wars.

For AI, Meituan will focus on scenarios and efficiency. It plans to invest ¥20 billion to upgrade AI dispatch and autonomous delivery systems, cutting average delivery time from 34 to under 28 minutes.

It may also develop more standalone Agents like “Xiao Mei” or optimize existing ones. But this feels defensive, since QianWen is already ordering takeout. Meituan has two choices: Build its own or partner with others like Doubao or Tencent’s new Agent product. Clearly, self-reliance is better.

Adapt while moving—a dilemma for many today.

What seemed unshakable a year ago may vanish the next. The world changes too fast; focus on what you can control.

When the takeout war cooled down in 2025, it was widely believed in the industry that this was only a temporary lull and that it would resurge in the following spring and summer. Now, that may not be the case.

Pragmatism has become a consensus. Even if Alibaba launches another offensive, it is most likely to revolve around new forms of AI. Qianwen App is the most likely candidate to be the main force, as it not only promotes AI products but also captures the takeout market, killing two birds with one stone. Although JD Takeout, currently holding the third-largest market share, has set a goal of "increasing its market share to 30%," it has also stated that its investment will be lower than in 2025, and losses will narrow quarter by quarter.

For Meituan, the year 2026 is likely to be even less comfortable than 2025. And this takeout war, which has changed dramatically in just a year, may also make more people realize: once many things are gone, they are truly lost. Cherishing the present is very important.

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?