From Building Cars to Building Robots: New Forces Embark on a Second Venture

03/13 2026

03/13 2026

583

583

Not the Most AI-Savvy Automaker, but the Most Product-Savvy AI Company.

Editor|Mao Shiyang

Original content from Autopix (ID: autopix)

01

The Most AI-Savvy Among Automakers

Early last year, He Xiaopeng stated in an exclusive interview that he aimed to be a CEO focused on large-scale manufacturing and technological innovation. The term “technological innovation,” once at the forefront of XPENG's DNA, was shifted to the end.

He intended to transform XPENG into a more substantial and grounded manufacturing automotive company.

However, by the end of last year's Tech Day, the tone had shifted again. He Xiaopeng's focus on stage was not on new cars but on AI large models, robots, and embodied AI.

More surprisingly, Li Auto, the top performer among the “Three Amigos” of new forces, began doing the same.

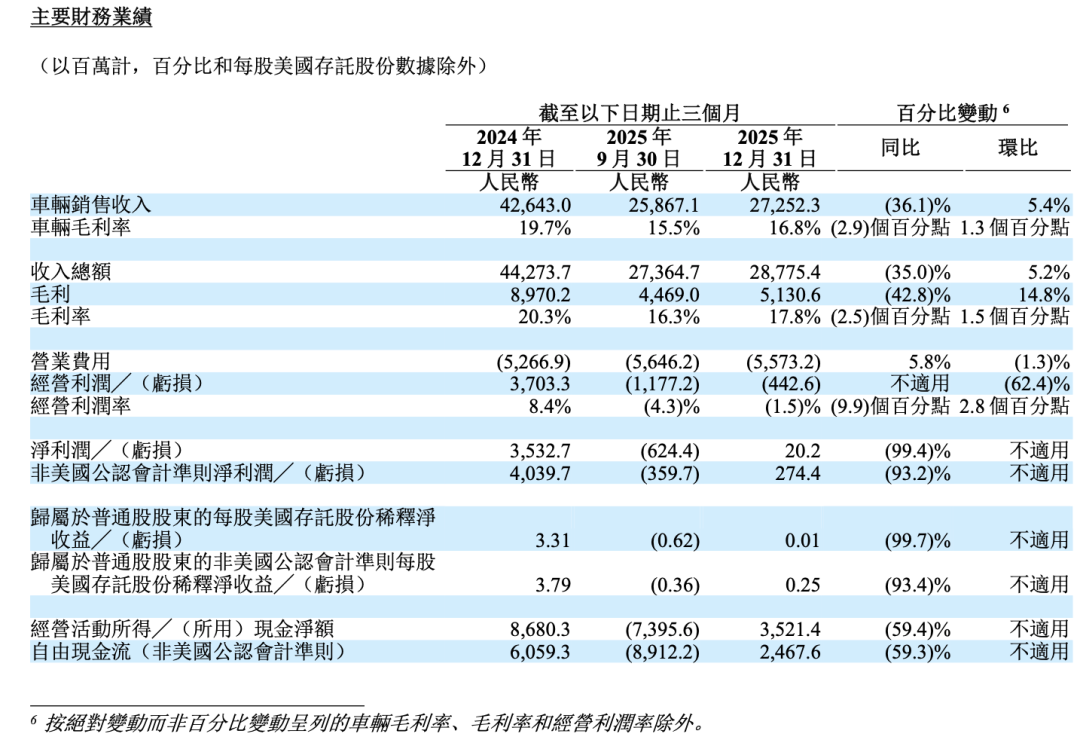

On March 12, Li Auto released its 2025 financial report. The company's total revenue was 112.3 billion yuan, a year-on-year decrease of 22.3%. Net profit attributable to ordinary shareholders was 1.139 billion yuan, an 85.8% decline. The company recorded an operating loss of 521 million yuan, compared to an operating profit of 7 billion yuan the previous year.

▍Excerpt from Li Auto's Hong Kong Stock Exchange Financial Report

The outside world expected to see how Li Auto would navigate its biggest sales challenge since inception. However, during the post-financial report conference call, Li Xiang and his executive team focused extensively on AI, stating that this year is crucial for Li Auto's evolution into an “embodied AI enterprise.” In 2025, Li Auto's R&D expenditure will be 11.3 billion yuan, with half allocated to AI-related projects.

He believes that for Li Auto, AI involves two levels: creating AI to imbue products with vitality and using AI to enhance organizational efficiency.

During an internal meeting in late January, Li Xiang spent most of his time discussing AI and robots, rarely mentioning cars. By early this year, Li Auto disbanded its autonomous driving team and reorganized its entire intelligent R&D system to focus on AI.

That year, XPENG's sales soared while Li Auto's declined—one riding the wave, the other facing headwinds.

Logically, both companies should capitalize on momentum or pressure to sell more cars. Like Leapmotor, which competes fiercely domestically and expands channels overseas, the core goal is to expand scale. However, according to Li Auto's recently announced plan, the 2026 sales target is 480,000 units, 20,000 fewer than the 500,000 units achieved in 2025.

Two veteran companies among the new automotive forces simultaneously made the same decision: de-emphasize cars and go all-in on AI.

Why is this happening?

If we only look at sales, XPENG saw a 126% year-on-year increase in 2025. Although Li Auto experienced negative growth, it still maintained its position among the top new forces, with XPENG selling 420,000 units and Li Auto 400,000 units. Looking downward, they are faring better than most new energy brands.

However, looking upward, they are not on par with truly manufacturing-oriented automakers like BYD and Geely, lagging by more than an order of magnitude.

Geely Auto sold 3.02 million vehicles last year, a 39% year-on-year increase, with a net increase of 860,000 units—more than the combined annual sales of Li Auto and XPENG. BYD sold 4.6 million vehicles in 2025, a 7.7% increase, translating to a net growth of 330,000 units.

The gap between new forces and traditional domestic brands is not narrowing but widening. This signals a dangerous trend: in the new energy vehicle sector, the competitive advantage from leading technological advancements is reaching its limits.

The priority is no longer to achieve further breakthroughs in intelligent technologies but to expand scale for cost advantages and to amortize intergenerational technology R&D.

With a base of millions of vehicles, Geely and BYD can strategically pivot with ease. For instance, BYD, after several years of slowing growth, completed a second innovation in pure electric technology last year, launched second-generation blade batteries and flash-charging technology earlier this month, and established a solid overseas presence. These achievements give them the confidence to aim for 6 million vehicle sales this year—a net increase of 1.4 million.

Internally, BYD conducted a strategic simulation, predicting that by 2027-2028, leading global automakers—Toyota with over 10 million units and Volkswagen with over 8 million units—will complete their transition to new energy.

Before these giants pivot, even a major player like BYD needs to seize the strategic window of opportunity. New forces, stuck at the 400,000-unit threshold, require time to accumulate, adjust, validate, and correct, refining technological details and product strategies.

Continuing to be the most AI-savvy among automakers is no longer a winning strategy. Decision-makers at new force automakers need new approaches.

02

The Most Manufacturing-Savvy in the Embodied AI Industry

In 2026, AI is a topic of discussion across industries. Nearly every month, new models push the boundaries, with surging reasoning capabilities and declining computational costs.

However, what truly shakes the industry—beyond surging capital, parameter scales, and computational power—is the generalization of AI large models' capabilities.

Intelligent driving models are no longer limited to recognizing traffic lights and lane markings. They now use VLA and rudimentary world models to understand the physical world, predicting object movements and human trajectories. They can even “pre-visualize” what will happen next.

This represents a potential paradigm shift. Traditional advanced driver-assistance systems (ADAS) relied on rules and perception. Now, large models focus on understanding and prediction—moving from mere answer machines to true AI.

At that moment, many realized that if AI can truly enhance its understanding of the physical world, driving is just one simple task requiring a more complex body—one capable of movement, grasping, and interacting with reality.

▍Li Auto's AI Glasses, Livis

▍Li Auto's AI Glasses, Livis

Although automakers' intelligent driving models are smaller and less sophisticated than those of many AI companies, they possess the necessary frameworks. Moreover, automakers are closest to commercialization and real-world usage scenarios, enabling them to achieve preliminary data closures—a core competitive moat for all AI companies.

Breaking down the robotics industry reveals an interesting dynamic. What does it need? A brain for perception, decision-making, and control; a body composed of motors, batteries, controllers, and structural components; ideally, scalable mass production capabilities to reduce costs; and real-world commercial applications.

These four links—algorithms, hardware, manufacturing, and commercialization—are areas where entrepreneurial embodied AI companies can manage at most half, while automakers control all four.

With improved generalization of autonomous driving models, they can serve as the brain for embodied AI. Automobile factories provide ready-made production lines, while dealerships and service networks offer natural sales channels. Automakers possess mature manufacturing processes, supply chain management, and scheduling capabilities—all challenging for embodied AI startups to replicate.

This is why He Xiaopeng stated on AI Day: “For intelligent automotive companies, building robots is not just about technological convergence but also an inevitable exploration of AI.”

03

Rebuilding Moats: Real-World Applications, Commercialization, and Data Closure

Beyond algorithms, hardware, and manufacturing, commercialization capabilities for embodied AI companies determine not just profitability but also the establishment of data closures—the most valuable competitive moat.

While simulation data is becoming increasingly powerful, and real-world videos from platforms like Douyin and YouTube can be used for training, data directly collected from real-world scenarios remains the most valuable for AI model training.

Embodied AI companies need to sell products and deploy them in real-world scenarios to gather authentic data for iterative algorithm improvements. This explains why embodied AI companies vied to appear on this year's Spring Festival Gala—not just to attract capital attention but to reach consumers directly.

Achieving significant product sales remains a distant goal for embodied AI companies. They may excel as engineering and technical experts but may struggle as product managers—a strength of Li Auto.

For automakers, these are non-issues. They already have a natural real-world application: millions of vehicles on the road, transmitting data.

While vehicle driving data is valuable for training AI to understand the physical world, it is relatively limited for training humanoid robots.

Fortunately, automakers have additional application scenarios—most directly, automotive production lines. Current humanoid robots are far from capable of intricate tasks like twisting bottle caps or making coffee.

▍XPENG's Robot, IRON

▍XPENG's Robot, IRON

However, on large-scale automotive production lines with repetitive, heavy, and enclosed tasks, humanoid robots are nearly capable—and even hold advantages, such as endurance.

Wang He, founder and CTO of Galaxy General Robotics, calculated that if an embodied AI company were to invest in deploying robots for data collection, each humanoid robot costs around 100,000 yuan. Deploying 10,000 units would require 1 billion yuan.

Factoring in labor costs for remote operation, annotation, and quality control—with two shifts per robot—the monthly employee costs for maintaining 10,000 robots would range from several hundred million to 1 billion yuan.

For embodied AI companies, this represents pure cost. However, for automakers, it involves both costs and cost substitution. The labor costs replaced by robots can partially offset robot maintenance expenses.

04

The Car Stops, but the Road Continues

Looking back at Li Auto and XPENG's early 2026 moves, it becomes clear why their first actions involved organizational restructuring rather than adjusting automotive products.

Li Xiang disbanded the once-core autonomous driving team, reorganizing it into three teams: foundational models, software ontology , and hardware ontology .

This is not an expansion of the automotive industry but a relaunch in the AI sector. At a January 26 all-hands meeting, Li Xiang declared: “2026 is the last window to become an AI leader. Without transformation, there will be no place left.”

Autonomous driving and intelligent cockpits were once XPENG's earliest and proudest strengths. Now, they are merged into a “General Intelligence Center,” directly overseen by He Xiaopeng.

The goal is to build a general AI brain, enhancing technological generalization for use in both vehicles and humanoid robots. He Xiaopeng even publicly stated: “In the next three to five years, all cars will become super intelligent agents.” In other words, cars are merely AI's first physical form.

Doubling down on AI represents Li Auto and XPENG's strategic move to transcend traditional automotive manufacturing and establish moats in the embodied AI sector.

Is this a gamble? Not necessarily, as Tesla has already demonstrated across the ocean.

From day one, Tesla never viewed itself as a traditional automaker, refusing to focus solely on large-scale manufacturing centered on volume and supply chain management.

This is why Elon Musk insisted against producing a cheaper “Model 2,” which could boost car sales but shift the company further toward manufacturing. A new model requires new molds, potentially new production lines, and increased part complexity.

Musk even discontinued the Model S and X, streamlining the product line to just the 3 and Y. He preferred cheaper “value editions” or pricier 7-seater variants—simple modifications within the existing manufacturing system.

The saved energy was redirected toward model training and humanoid robots. FSD serves as the brain, Cortex as the training model, and the humanoid robot Optimus directly reuses the entire visual and hardware system.

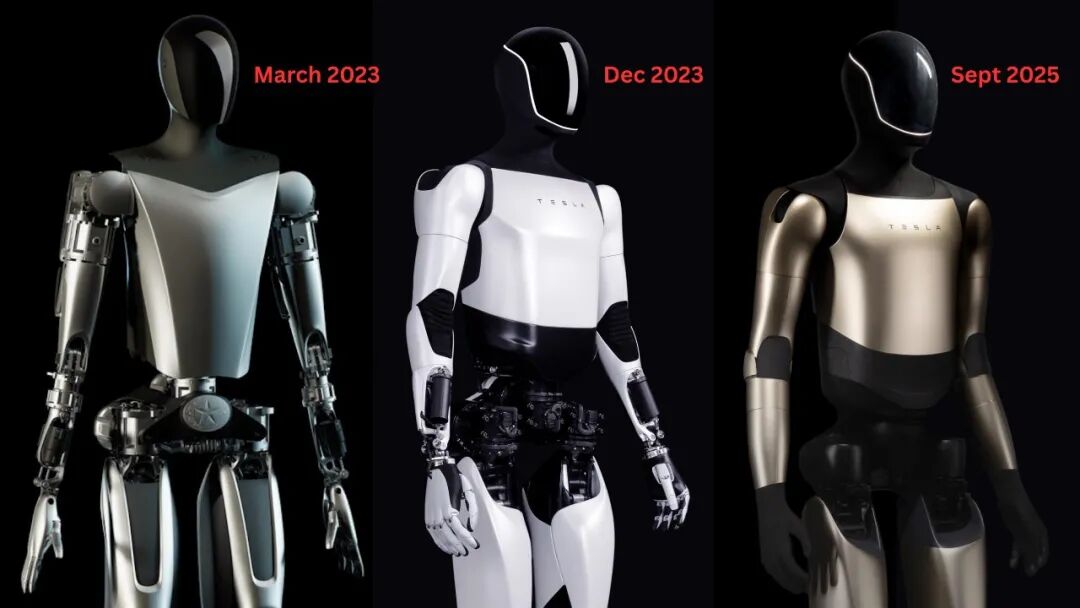

▍Tesla's Optimus

Robots, like “new models,” occupy the superfactory production lines once reserved for the Model S and X. Optimus's first customers are Musk's own factories.

This is why, in March, Musk confidently declared on social media that Tesla would become the first company to manufacture humanoid general intelligence.

Over the past few years, XPENG and Li Auto initially followed the “traditional automaking” logic, competing on products, technology, sales, and branding, only to realize how quickly the automotive ceiling approached.

Looking up, they suddenly recognized that their assets closely resembled Tesla's.

A decade ago, the energy transition propelled XPENG and Li Auto to prominence among new automotive forces. Now, the intelligent technology transition has made cars the gateway.

If cars are viewed as robots, the question shifts: Could automakers become the next generation of physical AI companies?

No one knows the answer yet. But at least, XPENG and Li Auto have begun rewriting their entrepreneurial stories in the embodied AI sector.

This article is original content from Autopix (autopix) and is not authorized for reproduction without permission.

-

![]()

"3D Vision Pioneer" Grapples with Internal Strife: $120 Million in Share Reductions Offset by $147 Million Private Placement

-

![]()

The domestic auto sales have declined so much that dealers who can't hold on have started closing stores en masse

-

![]()

Five Brands Team Up with Huawei: Will Dongfeng Still Pursue Independent R&D?

-

![]()

The Large Six-Seater SUV Market: Overhyped and Overrated

-

![]()

The Smart Driving Blue Light: Urgent Need for Rectification

-

![]()

Would OpenAI Be Fascinated by Anthropic’s Concepts?

-

![]()

Tencent: Few Great Queries, Yet Possessing the Ultimate One

-

Does DingTalk Need Revolutionaries or Reformers?