Alibaba: E-commerce Slumps Again, AI Emerges as the Savior

03/20 2026

03/20 2026

696

696

Alibaba, striking on two fronts—food delivery and AI—released its Q3 FY26 results before the U.S. market open tonight (March 19). Overall, from an expectations gap perspective, performance largely aligned with recently lowered guidance, except for weaker international e-commerce growth and larger losses in other businesses. However, in absolute terms, performance was undoubtedly weak.

The primary issue is the significant slowdown in core e-commerce growth after the end of the cycle driven by government subsidies and rising monetization rates. The silver lining is Alibaba Cloud's continued strong growth, as detailed below:

Bloomberg's consensus expectations for this quarter were not updated in time and hold little reference value. Below, we analyze based on timely updated expectations from major banks:

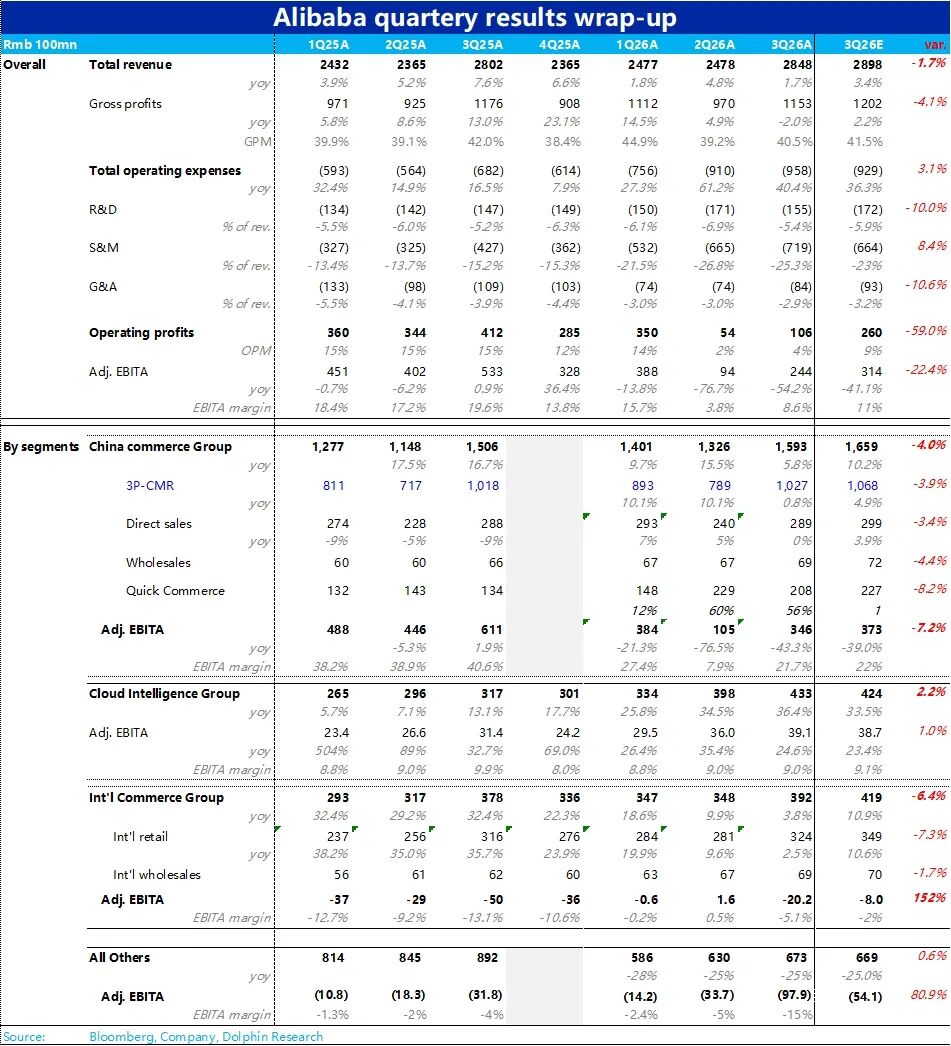

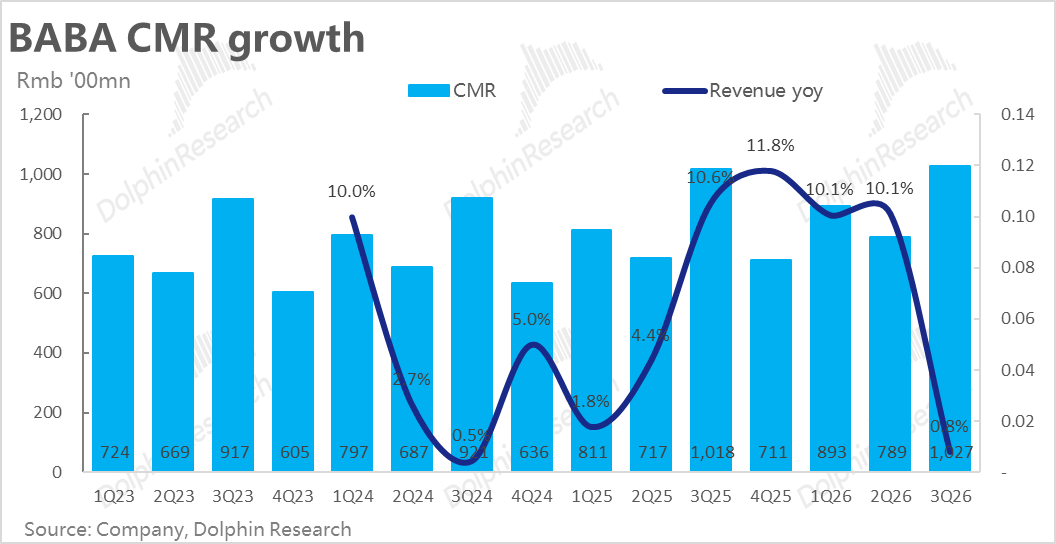

1. CMR Growth Below 1%: The core metric for traditional long-distance e-commerce, CMR, grew by just 0.8% YoY this quarter, a sharp deceleration from the previous quarter's 10%. Similar to JD.com, this reflects the waning impact of 2025 government subsidies, a high base in 2024, and a later Chinese New Year, delaying domestic shopping to Q1 2026.

Additionally, the 0.6% service fee introduced in September 2024 and the rollout of full-site advertising tools have exhausted their positive impact on monetization rates, leading to a rapid decline in CMR growth. Fortunately, the company had fully communicated this to the market, and actual performance met expectations.

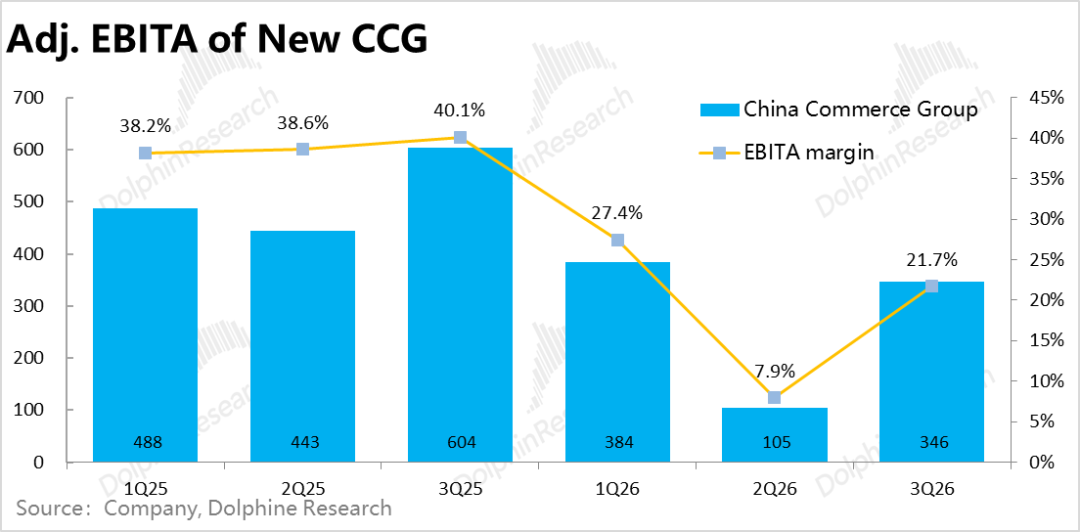

2. Food Delivery Losses Narrow but Progress Slow: China E-commerce Group's adjusted EBITA for the quarter was RMB 34.6 billion, down about RMB 26.5 billion YoY. Considering negligible CMR growth and assuming a slight YoY decline in profit from the original Taobao and Tmall Group, we estimate flash sales' net loss at around RMB 25 billion this quarter.

While losses narrowed significantly from last quarter (indicating improving UE for flash sales), they reached the upper end of market expectations (RMB 20-25 billion), suggesting slower-than-expected improvement. Based on Dolphin Research's estimates, Taobao Flash Sales' average loss per order narrowed from over RMB 5 last quarter to about RMB 3.5 this quarter (unofficial data; estimates only).

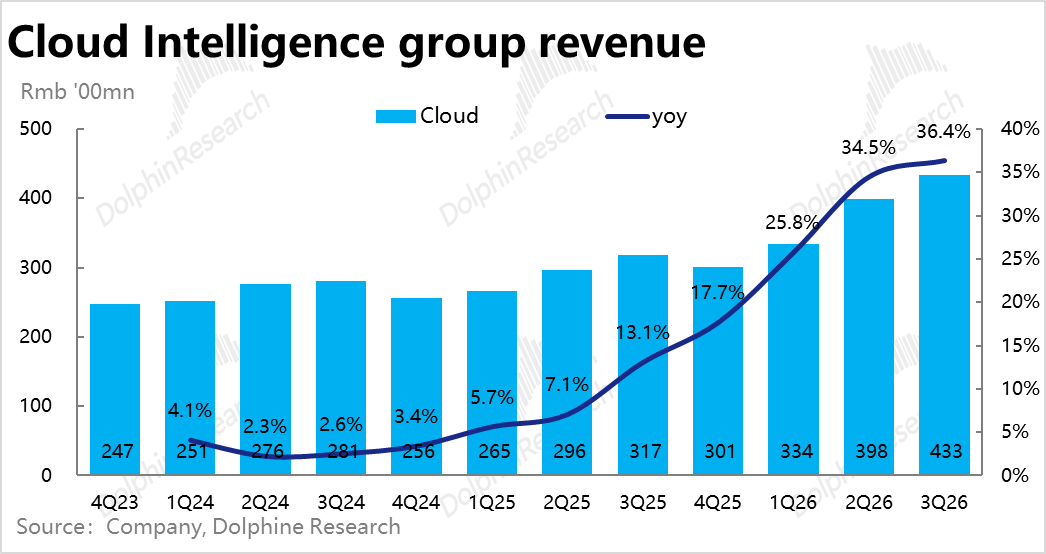

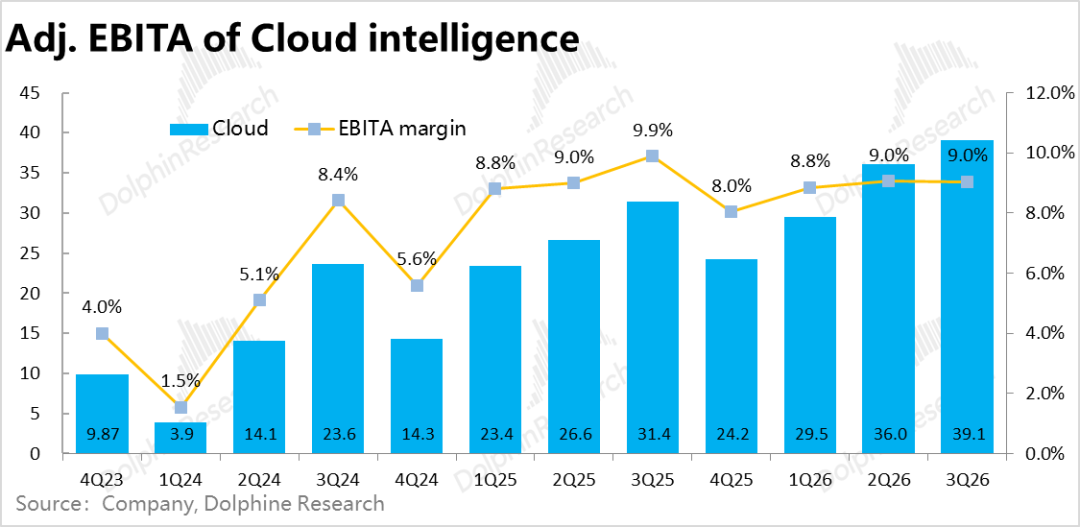

3. Alibaba Cloud Accelerates Again, Still Impressive: Fortunately, Alibaba performed well on the AI front. Alibaba Cloud's revenue grew by 36%, slightly accelerating as expected.

While not exceeding expectations and with a modest acceleration, Alibaba Cloud's external revenue grew by 35% this quarter versus 29% last quarter, a significant improvement. From a group-wide perspective, this substantial acceleration in external revenue holds higher value.

The company also stated that over the past three months, token consumption in the public model service market on the BaiLian MaaS platform has increased sixfold (as AI evolves from chatbots to agents, demand for tokens and computing power doubles), leading Dolphin Research to maintain a long-term positive outlook on cloud computing demand.

Meanwhile, Alibaba Cloud's profit margin remained at 9%, unchanged from last quarter, without any drag from the rising proportion of AI business—a decent outcome.

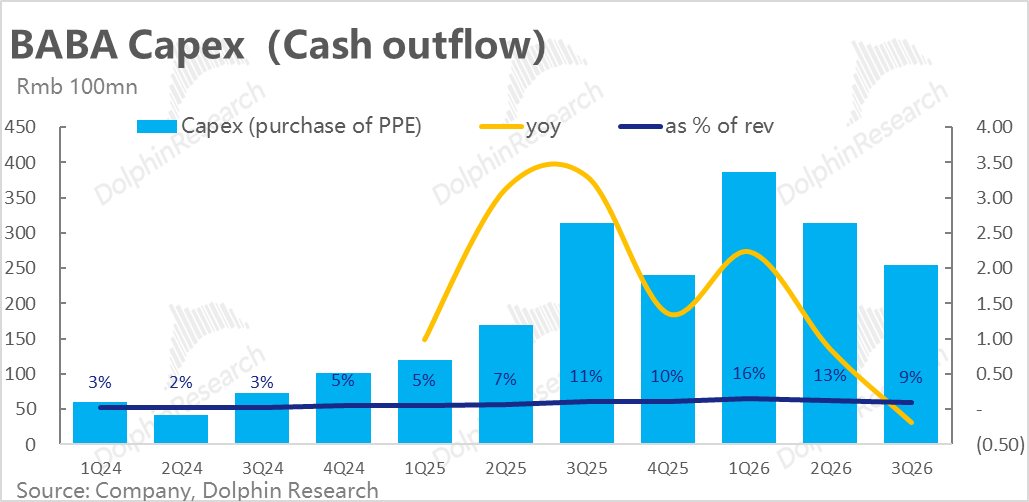

Capex spending for the quarter was RMB 29.9 billion, down from last quarter, possibly due to the ban on NVIDIA chips. Given Alibaba's previously aggressive investments and the market's stronger emphasis on ROI, reduced spending may not be a bad thing. Consequently, Alibaba's free cash flow turned positive again this quarter.

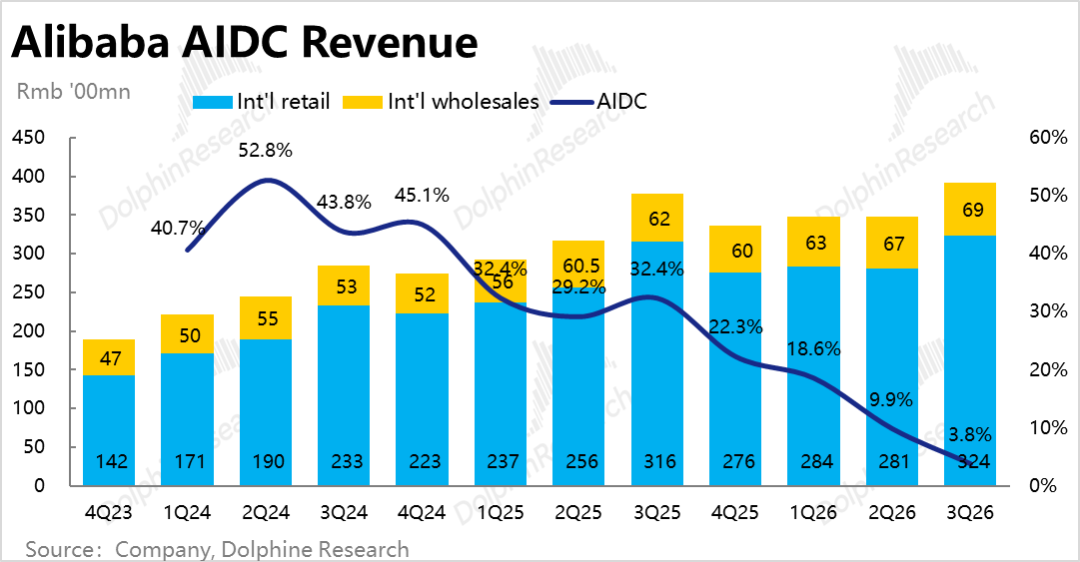

4. International E-commerce Growth Slows, Returns to Loss: International e-commerce revenue growth slowed to under 4% YoY this quarter, lower than the already reduced market expectations (around 7%), primarily dragged down by Lazada's negative YoY revenue growth. Facing expansion-phase competitors like Sea and TT Shop in Southeast Asia, Alibaba International faces significant competitive pressure.

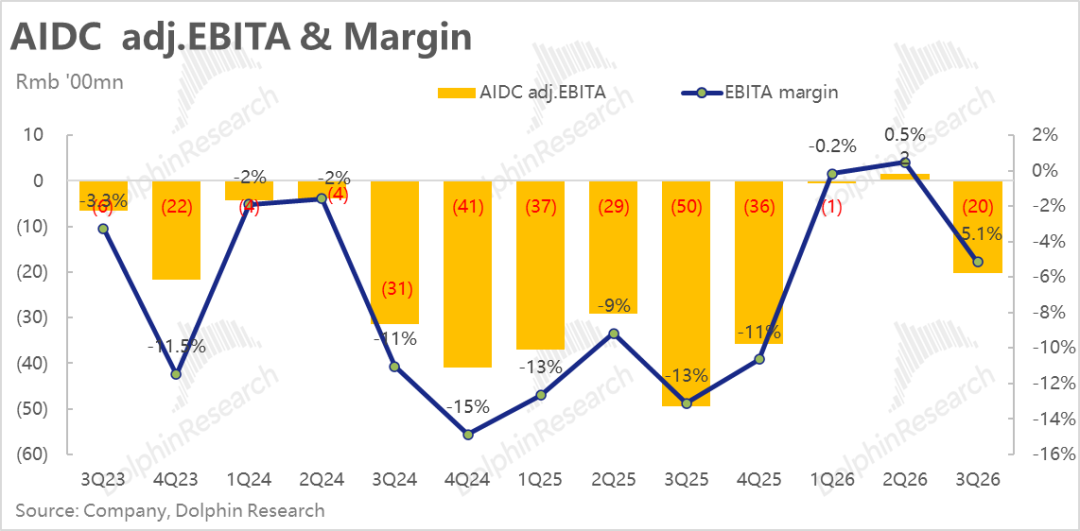

Meanwhile, international e-commerce's adjusted EBITA returned to a loss of RMB 2 billion. However, this was mainly due to seasonal effects from major shopping seasons (e.g., Black Friday), and losses narrowed YoY, not indicating a renewed investment cycle. Fine-tuned operations will continue.

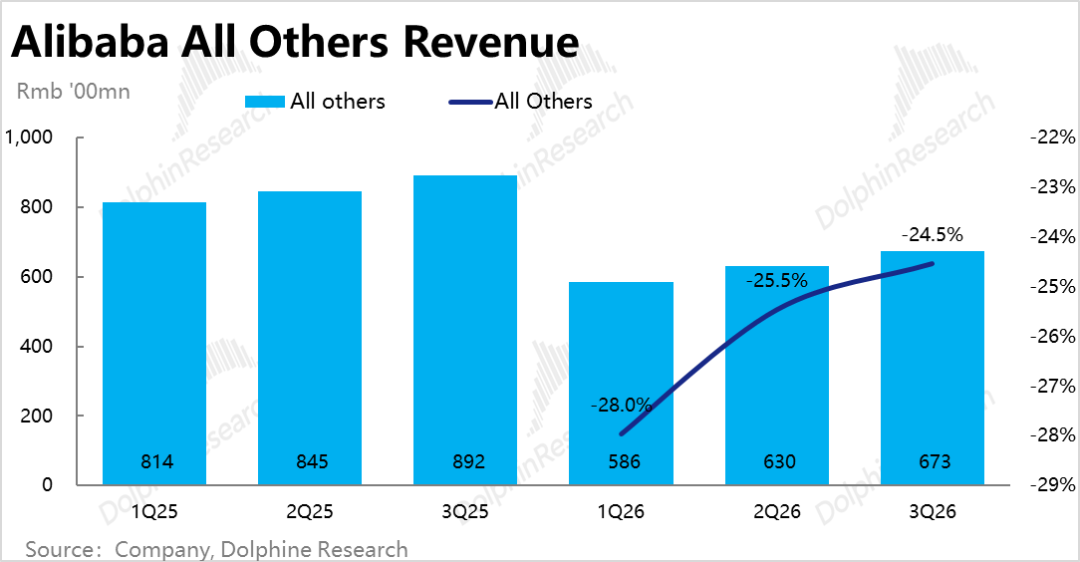

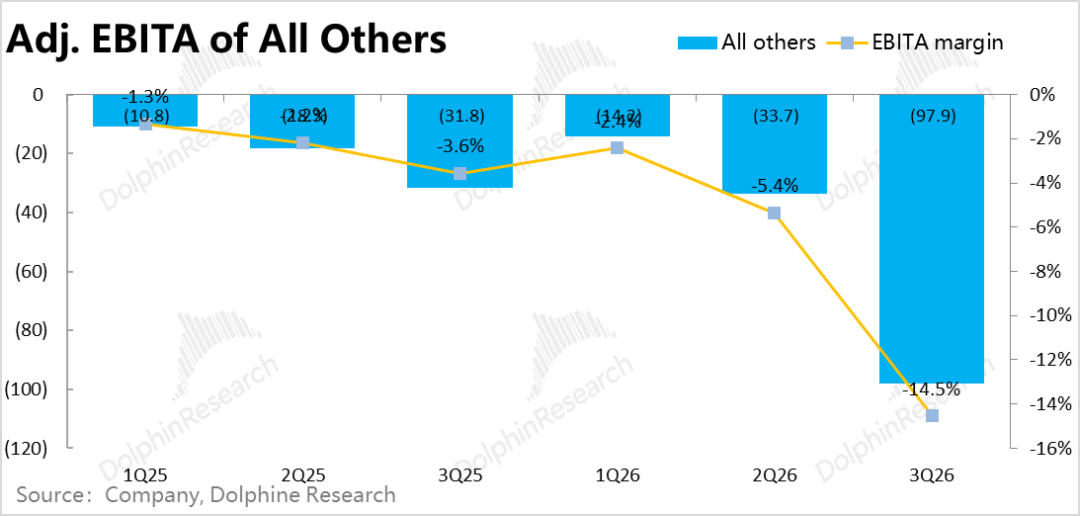

5. Other Businesses Also Ramp Up Investments: Losses from other businesses widened significantly to about RMB 9.8 billion this quarter, exceeding major banks' upgraded expectations of RMB 8.5 billion. Investments in AI applications like Gaode Street Rankings, QianWen/Quark Apps for customer acquisition and development contributed to this, though the magnitude was larger than expected.

Considering QianWen had not yet fully ramped up in December and the presence of red envelopes and free order cards during the Chinese New Year, losses from other businesses are unlikely to be low next quarter.

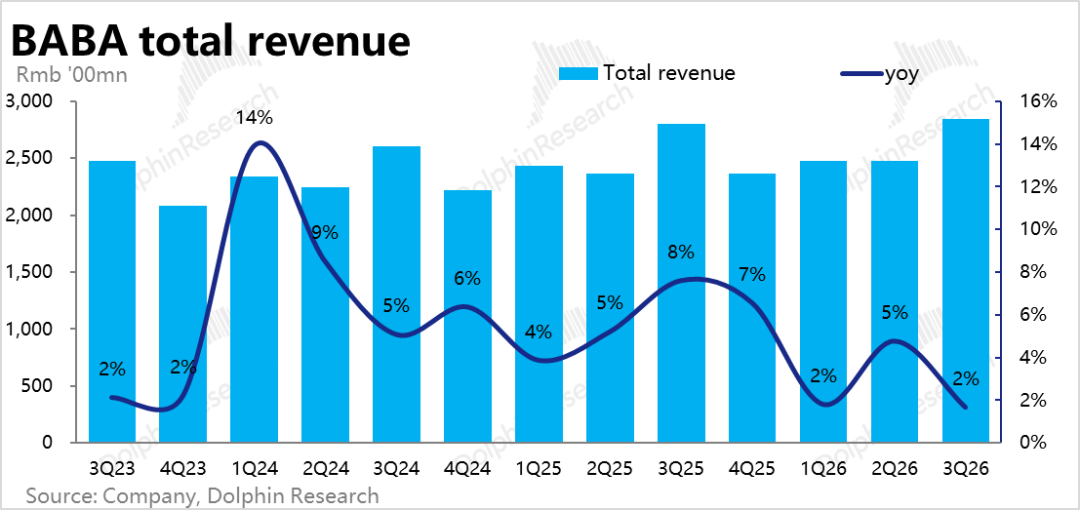

6. Overall Performance: Alibaba's total revenue grew by about 1.7% YoY this quarter. Excluding the impact of divesting Intime and Sun Art, comparable growth was 9% versus 15% last quarter, primarily due to sharply slowed growth in domestic and overseas e-commerce.

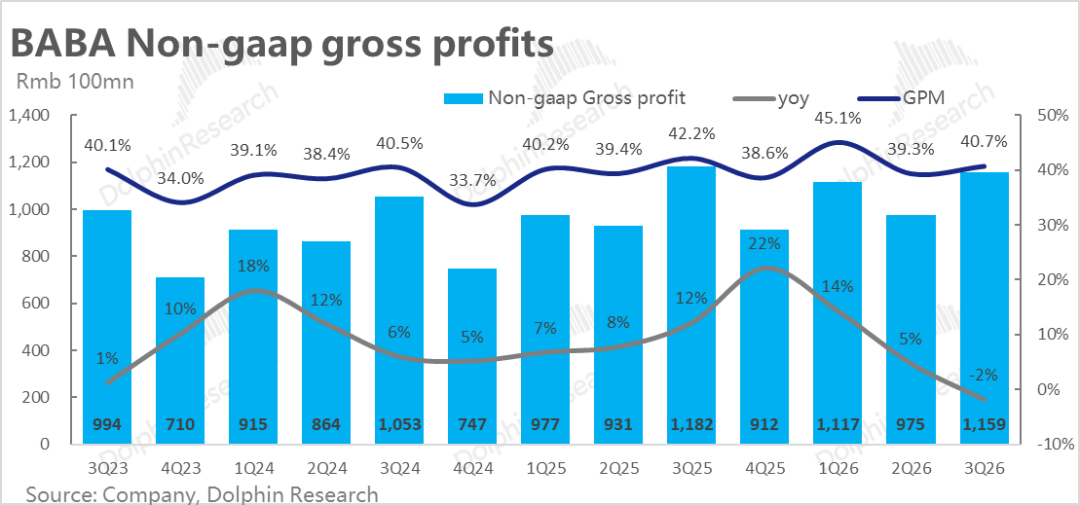

Gross profit, after adding back stock-based compensation, declined by 2% YoY, with the gross margin down 1.5 percentage points YoY, with the decline widening. Delivery costs for instant retail likely served as the main drag, with widened losses from other businesses also contributing.

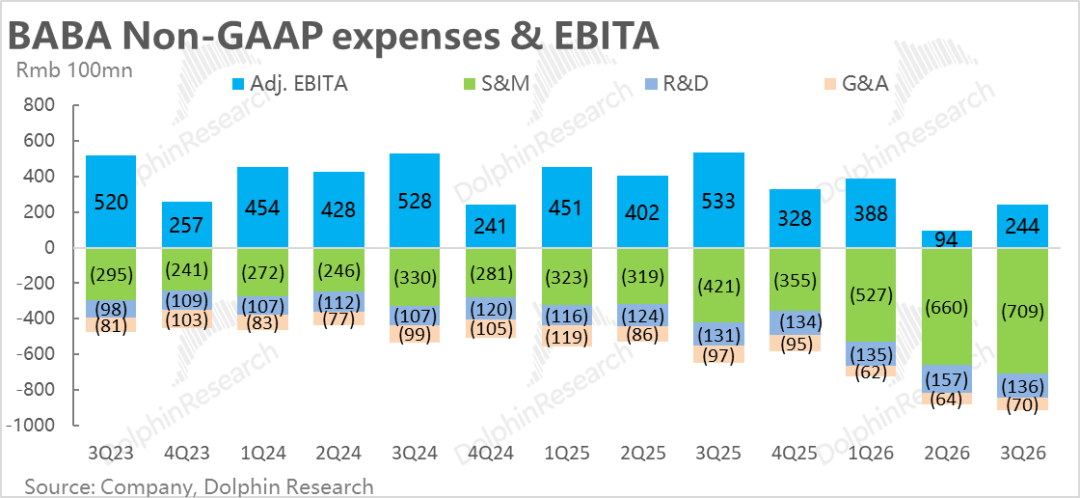

Marketing expenses, the most noteworthy cost item, reached RMB 70.9 billion this quarter, up RMB 28.8 billion YoY—exceeding losses from flash sales and clearly reflecting significant growth in customer acquisition investments across other business segments.

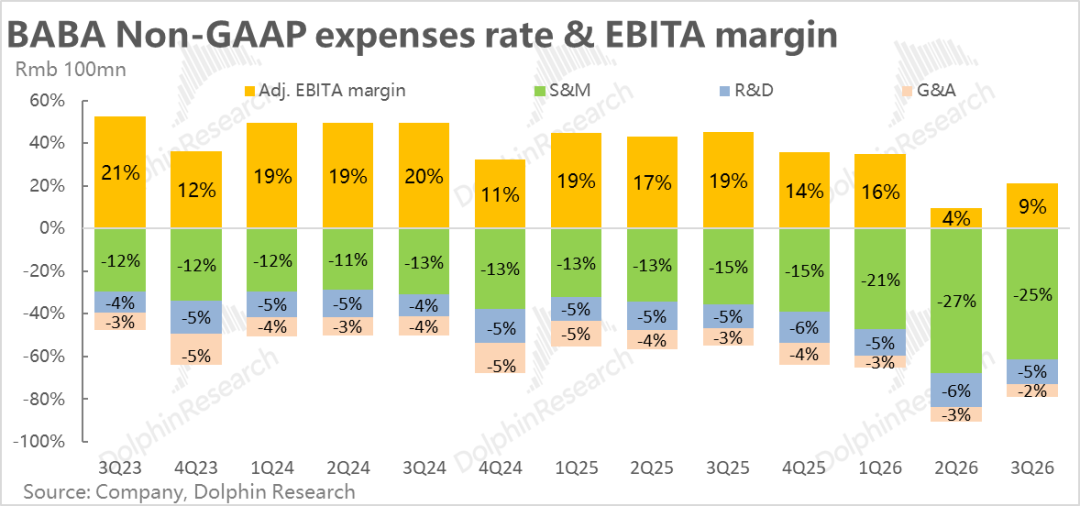

Ultimately, the group's adjusted EBITA was RMB 23.4 billion. While improved from last quarter's sub-RMB 10 billion profit due to narrowed food delivery losses, core Taobao and Tmall business profits likely declined YoY, international e-commerce returned to loss, and losses from other new businesses widened more than expected, indicating poor overall profit trends.

Dolphin Research's View:

1. Current Quarterly Performance: Alibaba's performance this quarter was clearly subpar:

1) The core long-distance e-commerce business saw stalled revenue growth due to overall industry weakness in Q4 and the exhaustion of its monetization rate improvement cycle, naturally leading to poor profitability.

While Taobao Flash Sales is indeed reducing losses, progress remains slow.

2) Meanwhile, international e-commerce growth slowed and returned to a quarterly loss of over RMB 2 billion, albeit due to seasonal effects, still indicating less-than-ideal refinement results, with underperformance in both revenue growth and profit release.

With declining profitability in the core Taobao and Tmall business, other business lines have entered investment phases. Despite flash sales starting to reduce losses, the group's overall profitability has significantly declined.

3) The only support comes from AI and cloud businesses, where Alibaba Cloud, as a domestic leader, performed decently in both growth and profitability. However, it lacked the blockbuster, exceed expectations (better-than-expected) performance seen last quarter to momentarily overshadow deficiencies in other businesses.

2. Outlook:

1) Long-Distance E-commerce: First, for the "ballast" long-distance e-commerce business, government subsidies in 2026 are unlikely to match the scale of 2025, creating high base pressure. Additionally, the recent narrative of AI computing power replacing human labor in China may impact the consumption capacity of "optimized" employees, leading Dolphin Research to maintain a cautious outlook on domestic e-commerce growth in 2026.

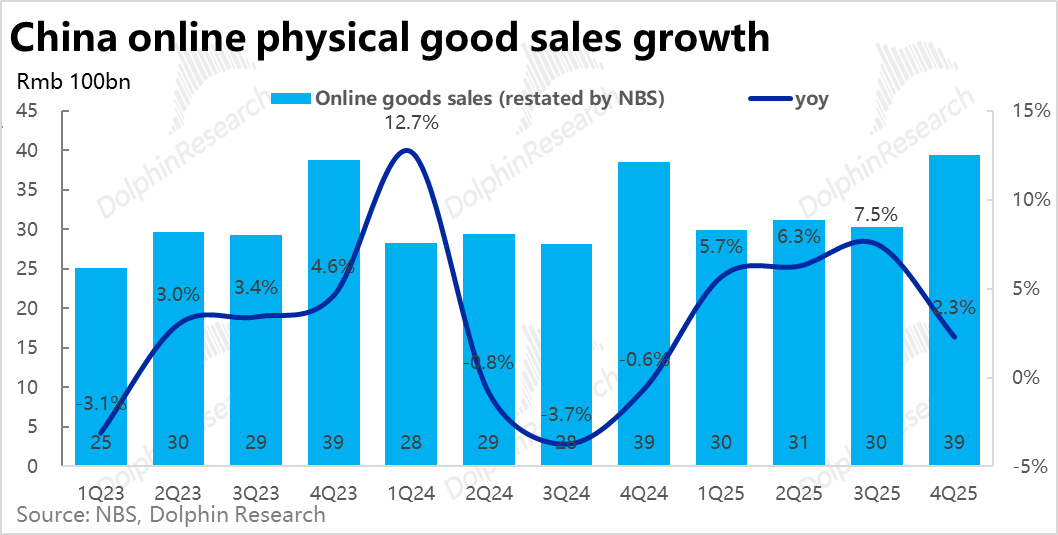

However, one incentive (contributing factor) to Q4's weak e-commerce growth was delayed consumption due to a later Chinese New Year. Recently released online commodity sales (commodity sales) growth exceeded 10% in January-February, showing a clear rebound. Combined, Q4 2025 + 2M 2026 online retail sales grew around 5.4% YoY—slowing but not as bad.

Thus, Dolphin Research is not overly optimistic about e-commerce sales growth in 2026 but believes Q4 2025 may have been the trough, with the worst phase likely over.

Moreover, the favorable cycle from the 0.6% service fee and full-site advertising tools has largely ended. Additionally, stricter tax collection on e-commerce merchants starting October 2025 (shifting from self-reporting to platform-assisted tax reporting) implies higher tax/profit pressure, especially for SMEs, potentially reducing their advertising spending capacity.

Both factors suggest that Taobao and Tmall's path to boosting revenue through monetization rate improvements may face challenges ahead.

2) Instant Retail: While subsidy intensity in instant retail has eased compared to Q3 2025 for Alibaba and Meituan, market attention has shifted from "food delivery wars" to "AI wars."

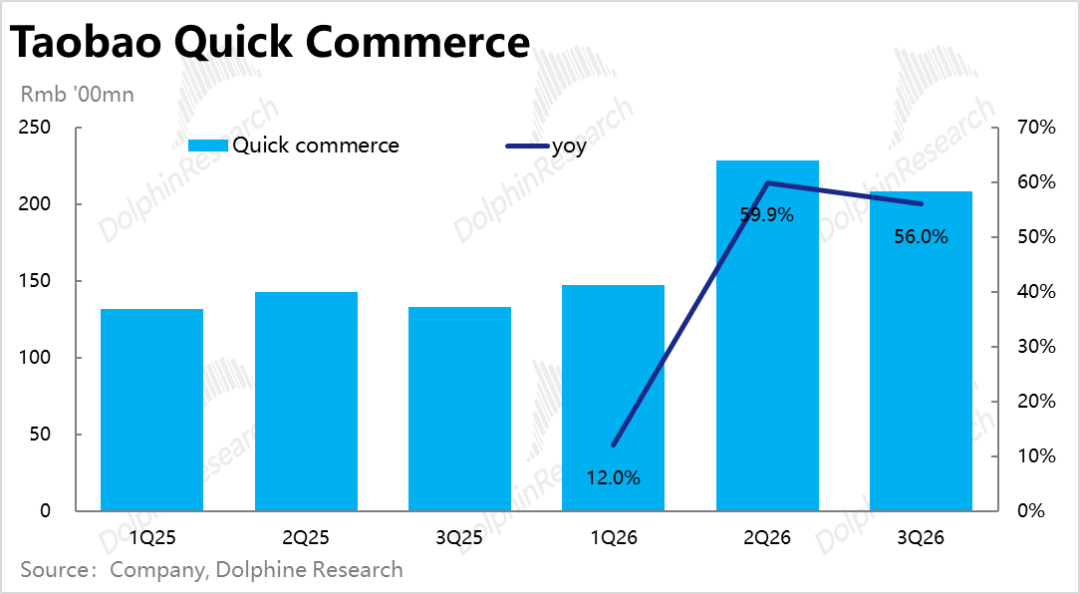

However, order volumes and subsidy levels remain tightly contested between the two. Alibaba management previously stated the goal of "becoming the market leader in instant retail," implying that competition and subsidy reductions in the food delivery war will not end shortly. This quarter's flash sales losses nearing the upper limit validate this expectation.

Additionally, while survey data suggests an improving order mix for Taobao Flash Sales (higher proportion of high-ticket meal and non-meal flash sales), results have not yet materialized this quarter.

According to recent surveys (for reference only), Taobao Flash Sales' total investment budget for 2026 is RMB 50+20 billion, with RMB 50 billion fixed and RMB 20 billion dynamically determined based on conditions. Given this quarter's trend, the final budget may lean toward the upper limit.

If actual spending reaches RMB 70 billion, it will be similar to 2025's total investment. However, considering 2025's budget was spread over 2.5 quarters, quarterly investments and losses in 2026 will still decline.

3) Chip + Cloud + Model Trinity: Best Vehicle for China's AI Story: Similar to Google's logic, Alibaba, with Pingtouge (self-developed chips), Alibaba Cloud (cloud services), and QianWen model & App family (model and software capabilities), is among China's most well-positioned companies for AI with the fullest stack layout—making it a top pick for funds bullish on AI in China. This narrative remains largely unchanged despite this quarter's performance.

Regarding recent key developments:

First, in the previous AI C-end entry point battle, during the Chinese New Year, Doubao, QianWen, and Yuanbao engaged in a "red envelope war" to acquire C-end users, but user retention was poor, with daily active users (DAUs) for apps other than Doubao declining significantly from peaks. While QianWen fared better than Yuanbao, the gap with Doubao widened. Thus, Alibaba achieved limited success in capturing C-end entry points.

With OpenClaw's spread in China, the industry's frontier has shifted from AI chatbot-based C-end traffic acquisition to agent development and user acquisition. Dolphin Research believes this shift may lead to:

a. Agents require several times more computing power than chatbots, stimulating further rapid growth in computing power/token demand and benefiting computing power suppliers. Recently, Alibaba Cloud's price hikes for some products likely reflect supply-demand imbalances in computing power.

b. As limited computing power shifts from C-end apps like QianWen and Doubao (initially cost centers, free or subsidized to drive traffic, with monetization still exploratory) to agents (more office or B2B-oriented, with stronger user willingness to pay and immediate revenue generation via token-based pricing), relevant cloud/model companies may see earlier actual revenue and profit from AI businesses.

4) Impact of Establishing the ATH Business Group:

Another major recent development is Alibaba's announcement to consolidate Tongyi Lab, the MaaS business line under Alibaba Cloud, QianWen Business Unit, Wukong Business Unit, and AI Innovation Business Unit into the Alibaba Token Hub (ATH) Business Group. Part of the rationale is that tokens have become the primary growth direction after the shift from chatbots to agents.

Dolphin Research believes this restructuring's main significance lies in aligning upstream model R&D, midstream computing power/model sales, and downstream C/B-end applications within one organizational structure, facilitating technical R&D and product demand alignment and enabling internal communication and goal consistency. This prevents model R&D from solely pursuing model sophistication while end-user application teams focus on KPIs like user volume without long-term vision.

Another less critical but near-term impactful factor is that as Alibaba Cloud transitions from selling raw computing power (or "bare metal," where users build their models) to selling MaaS or tokens (with pre-configured models on underlying hardware), it can theoretically achieve higher revenue and profit margins—potentially reflecting as accelerated Alibaba Cloud revenue and better-than-expected profitability.

3. Valuation Analysis: Dolphin Research employs a SOTP valuation approach. For China E-commerce Group, given cautious expectations for traditional e-commerce growth in 2026, we forecast only low single-digit % YoY growth in adj. EBITA for the original Taobao and Tmall Group (excluding flash sales and Fliggy) in FY27, assuming RMB 70 billion in instant retail losses for the year, totaling about RMB 110 billion in post-tax profit.

Considering Taobao and Tmall's relative resilience in the e-commerce industry and significant potential for instant retail losses to narrow, this segment could drive overall growth in China's e-commerce sector.

For Alibaba Cloud, given its chip + cloud + software trinity advantage, we assume FY27 revenue of about RMB 220 billion (accelerating to 40% YoY growth) and a valuation multiple of 4x PS.

For international e-commerce, we assume revenue of about RMB 156 billion (conservatively expecting 7% YoY growth). Given slowing growth momentum and the return to loss this time, we significantly reduce the valuation multiple to just 1x PS.

More detailed valuation analysis is available in the same name (same-titled) article in the "Insights - Deep Dive (Research)" section of the Longbridge App.

Below is a detailed performance analysis:

I. Alibaba's New Financial Reporting Framework

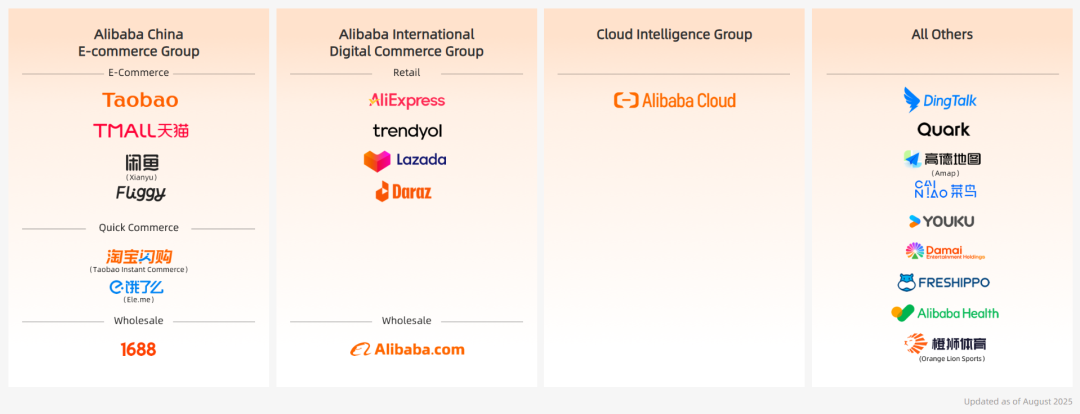

In FY26, with Ele.me's instant retail and Fliggy's travel businesses merged into the original Taobao and Tmall Group to form the new China E-commerce Group, Alibaba's organizational structure and financial reporting framework have been updated again. As shown below, Alibaba Group's new structure comprises four segments:

1) China E-commerce Group: Includes the original Taobao and Tmall Group + Fliggy + Taobao Flash Sales/Ele.me businesses;

2) Original International E-commerce Group remains unchanged;

3) Alibaba Cloud Group remains unchanged;

4) All other businesses, including previously independently disclosed Cainiao, China Local Services, and Alibaba Entertainment Group, are consolidated into the "Other Businesses" segment.

II. Core E-commerce Growth Remains Steady

1. Core Business - Key Metric for Long-Distance E-commerce: CMR was RMB 102.7 billion this quarter, up just 0.8% YoY, a significant slowdown. Similar to JD.com, this reflects the waning impact of 2025 government subsidies, a high base in 2024, and a later Chinese New Year, resulting in only 2.3% growth in Q4 online physical retail overall, with Taobao and Tmall's GMV growing slightly slower than the industry.

Additionally, the favorable base period for the 0.6% service fee and the Whole Site Push advertising tool, which began to be charged in September 2024 and contributed to the monetization rate improvement, has now passed. Consequently, the extent to which CMR outpaces GMV growth will significantly narrow, representing another drag factor.

Fortunately, despite the subpar absolute performance, the company has adequately communicated with the market, lowering expectations. The actual performance was largely in line with these adjusted expectations.

2. Taobao Flash Sales + Ele.me: Taobao's instant retail revenue for the quarter approached RMB 20.8 billion, up 56% YoY. More critically, on a quarter-on-quarter basis, it declined by 9%, slightly worse than Dolphin Research's expectations.

While the order volume in Q4 is indeed lower than in Q3 due to seasonality (colder weather), we had anticipated that the optimization of Taobao Flash Sales' order structure (more high-value meals and non-meal retail) would drive up the average revenue per order. However, the increase appears to be less than expected.

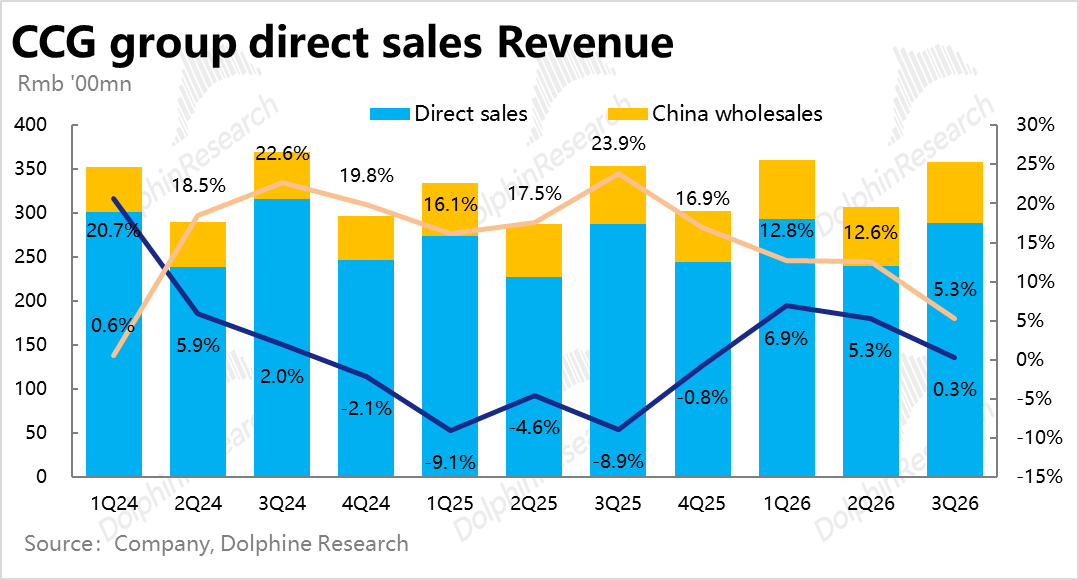

3. Self-operated Retail (including related fulfillment revenue): Revenue for the quarter grew by 0.3% YoY, a significant deceleration similar to CMR, primarily due to the overall slowdown in domestic e-commerce growth in Q4.

The 1688.com wholesale business, one of the main focal points of the "cost-effectiveness" strategy, maintained relatively higher growth at 5.3% for the quarter. According to the company, this growth was primarily driven by revenue from additional member services.

Overall, as growth in CMR and other business lines slowed in line with the weaker industry trends, the rapid growth in flash sales revenue helped the domestic e-commerce group achieve an overall revenue growth rate of 5.8% for the quarter.

III. Slower-than-expected progress in reducing losses from food delivery

While market attention has shifted away from the "food delivery wars" and more toward AI businesses, the scale of investment/losses in flash sales still has a significant (or even the largest) impact on the company's profits.

The adj. EBITA for China's e-commerce group was RMB 34.6 billion this quarter, a decrease of approximately RMB 26.5 billion YoY. Considering that revenue from CMR and other sources showed little to no growth this quarter, and assuming conservatively that, excluding flash sales, the original Taobao and Tmall Group's profits declined slightly YoY, it can be inferred that flash sales incurred a net loss of approximately RMB 25 billion this quarter (for reference only).

Although this represents a significant reduction from the RMB 36 billion loss estimated by Dolphin Research in the previous quarter, indicating an improvement in flash sales' unit economics (UE), it falls at the upper end of the market's expected loss range of RMB 20-25 billion, suggesting that the pace of improvement may not be as fast as anticipated.

Combining relevant research summaries, we estimate that the average loss per order for Taobao Flash Sales narrowed from just over RMB 5 in the previous quarter to around RMB 3.5 this quarter (no official data available; estimates are for reference only).

IV. The biggest highlight - Alibaba Cloud continues to accelerate beyond expectations

On another front—AI/Cloud business—Alibaba's performance this quarter remained impressive. Alibaba Cloud's revenue grew by 36%, in line with market expectations and accelerating slightly from 34.5% in the previous quarter.

While it did not exceed expectations again and the acceleration seems limited, Alibaba Cloud's external revenue grew by 35% this quarter compared to 29% in the previous quarter, representing a significant acceleration. This indicates substantial growth in actual external demand, with the company disclosing that AI-related business revenue continues to maintain triple-digit % growth.

Considering that domestic AI is currently transitioning from Chatbots to Agents (which will double the demand for tokens and computing power), the company disclosed that over the past three months, token consumption in the public model service market on the BaiLian MaaS platform has increased sixfold. It is expected that MaaS revenue will become Alibaba Cloud's largest revenue product, leading Dolphin Research to maintain a long-term bullish view on cloud computing demand.

In terms of profitability, Alibaba Cloud's adj. EBITA margin reached 9% this quarter, unchanged from the previous quarter. Although AI's higher requirements for equipment and energy logically suppress profit margins, this may be offset by the current high demand for computing power (Alibaba Cloud recently announced price hikes for some products) and an optimized product mix (abandoning low-margin businesses and focusing on high-margin businesses like MaaS). Thus, the stable profit margin is still commendable.

Additionally, Capex spending for the quarter was RMB 29.9 billion, with cash Capex at RMB 25.3 billion, a decline from the previous quarter. Since FY26, investments have continued to narrow, possibly influenced by the ban on Nvidia chips.

However, the market's attitude toward Capex for cloud service providers is no longer that higher is better; instead, there is a greater emphasis on ROI and a desire to avoid excessive pressure on profits and cash flow. Therefore, given Alibaba's relatively aggressive investments in the past, a slowdown in investment may not necessarily be negatively interpreted by the market. Attention can be paid to whether management provides guidance on the pace of future Capex investments during the earnings call.

V. International e-commerce slows down and incurs losses? Fine-tuned operations remain unchanged

Alibaba's international e-commerce business performed relatively poorly this quarter. Revenue growth slowed to less than 4% YoY, lower than the already adjusted market expectations (around 7%). It was one of the few indicators that truly fell short of market expectations this quarter. According to the company, the main drag was Lazada's negative revenue growth YoY.

Given that Sea is currently in an investment phase of "spending to drive growth," it can be inferred that Alibaba International faces significant competitive pressure in Southeast Asian markets.

Additionally, it was surprising that the international e-commerce adj. EBITA incurred a loss of RMB 2 billion again this quarter. However, this was primarily due to seasonal effects from major sales seasons (e.g., Black Friday), representing an improvement compared to the approximately RMB 5 billion loss in Q3 FY25.

The company also stated that this was purely a seasonal fluctuation and does not indicate a return to an investment cycle. They will maintain a fine-tuned operational approach.

VI. Increased losses in new businesses, including Gaode Street View & QianWen Quark

Apart from the three major segments mentioned above, businesses including Cainiao, Alibaba Entertainment, Gaode, QianWen, and those previously classified under other categories generated revenue of approximately RMB 67.3 billion this quarter, down 25% YoY. This was primarily due to the divestiture of Intime and Sun Art Retail, as well as the transfer of some logistics functions to corresponding front-end business departments (e.g., self-operated retail and international e-commerce).

Meanwhile, investments in customer acquisition and development for AI applications like Gaode Street View rankings and the QianWen/Quark App significantly increased losses in other businesses to approximately RMB 9.8 billion this quarter. This exceeded the already raised expectations of major banks, which had anticipated a loss of RMB 8.5 billion.

Considering that QianWen had not yet fully ramped up its efforts in the December quarter and that there were red packet and discount card promotions during the Spring Festival, losses in other businesses are expected to remain high next quarter as well.

VII. Overall performance largely meets lowered expectations, but absolute performance is relatively poor

Overall, Alibaba's total revenue for the quarter was approximately RMB 284.8 billion, up 1.7% YoY. Excluding the impact of divesting Intime and Sun Art, the comparable growth rate was 9% vs. 15% in the previous quarter, primarily due to the significant slowdown in domestic and overseas e-commerce growth this quarter.

Gross profit, after adding back share-based compensation expenses, declined by 2% YoY this quarter, with the gross margin continuing its downward trend and the decline widening to 1.5 percentage points YoY. The main contributing factor was likely the drag from delivery costs associated with the instant retail business.

In terms of expenses (excluding share-based compensation), the most noteworthy was the marketing expense, which reached RMB 70.9 billion this quarter, an increase of approximately RMB 28.8 billion YoY. This was significantly higher than the estimated losses from the flash sales business, clearly reflecting a substantial increase in customer acquisition investments across other business segments.

Regarding other expenses, R&D spending increased by nearly 4% YoY, while administrative expenses declined by 25% YoY (likely due to the divestiture of Intime and other businesses). Alibaba remains relatively restrained in its internal spending.

Overall, the group's adjusted EBITA was RMB 23.4 billion, down approximately 43% YoY. While the significant reduction in food delivery losses this quarter represents a notable improvement from the less than RMB 10 billion profit in the previous quarter, the core Taobao and Tmall business profits may have declined YoY, international e-commerce incurred losses again, and losses in other new businesses expanded more than expected. Overall, profit performance remains relatively poor.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. For reprint authorization, please obtain approval.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report assumes all risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from using the data in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions mentioned in this report shall not be considered or construed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction. They also do not constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to or use by individuals or residents in jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or subjects Dolphin Research and/or its subsidiaries or affiliated companies to registration or licensing requirements in those jurisdictions.

This report reflects only the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. No institution or individual may, without the prior written consent of Dolphin Research, (i) make, copy, reproduce, duplicate, forward, or distribute any form of copies or reproductions in any way, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

WeChat Collaborates with Huawei/Honor/Xiaomi on A2A: Is This the Dawn of AI Integration?

-

![]()

NVIDIA RTX Spark: Powerful, Yet Not the Ideal Choice for the Agent Era

-

![]()

NVIDIA RTX Spark: Powerful, but Is It the Right Fit for the Age of Agents?

-

![]()

A Genuine Threat or Just a Publicity Stunt? World's Premier AI Firm Warns: AI Evolving Autonomously, Slipping Beyond Human Control

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital