Tencent Music Reports 11 Billion Yuan in Earnings, Yet Its Stock Price Plummets by 30%. What Concerns the Market?

03/22 2026

03/22 2026

629

629

A dramatic surge in profits juxtaposed with a sharp decline in stock price—this is the stark contrast witnessed following the release of Tencent Music's financial report.

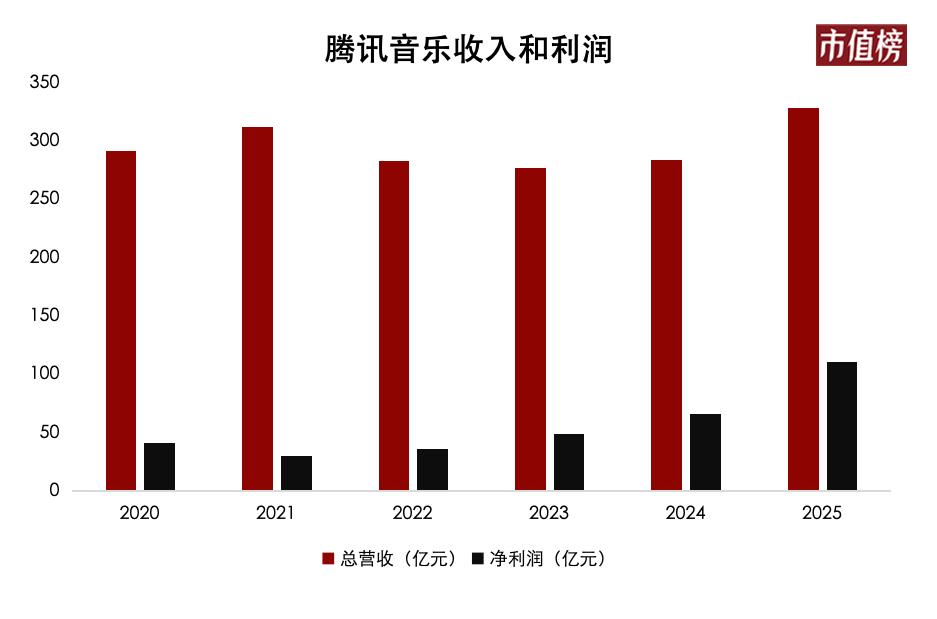

On March 17, Tencent Music unveiled its financial results for the fourth quarter and the entire year of 2025. On the surface, the performance was quite impressive: total annual revenue soared to 32.9 billion yuan, marking a 15.8% year-on-year increase; online music service revenue climbed to 26.73 billion yuan, up 22.9% from the previous year; and net profit reached 11.06 billion yuan, surging by 66.4% year-on-year.

However, the day after the financial report's release, Tencent Music's shares listed in the U.S. plummeted by 24.65%, while its Hong Kong-listed shares dropped by over 20%, culminating in a more than 30% decline in stock price over two days.

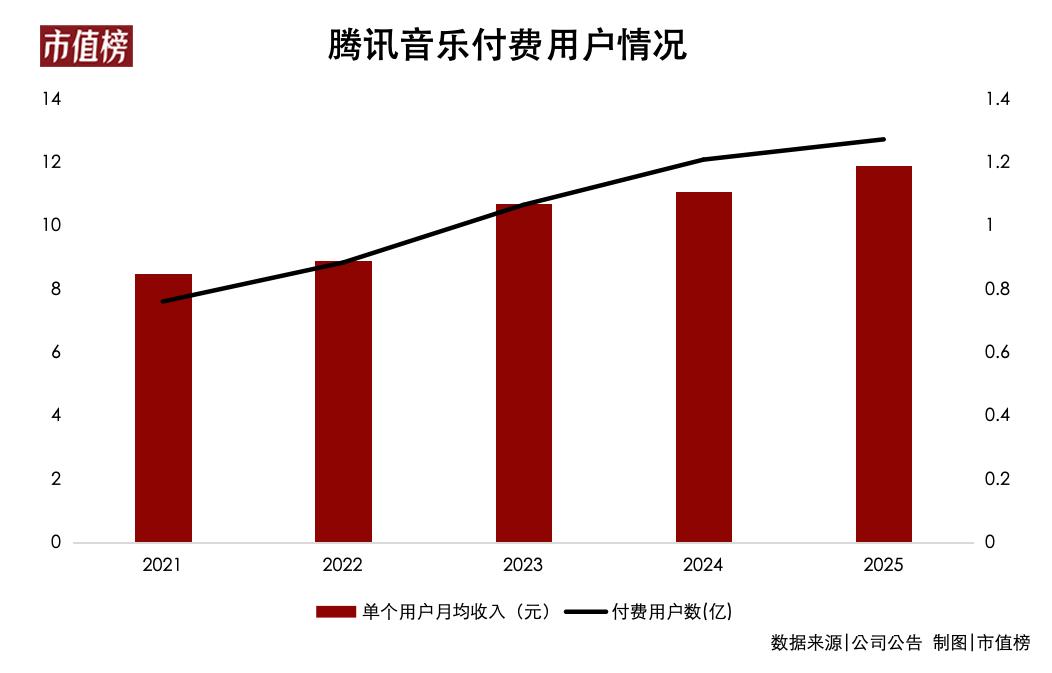

The disparity between performance and stock price may be linked to another set of figures in the same financial report: in 2025, Tencent Music's mobile monthly active users (MAU) declined by 5% year-on-year to 528 million, indicating a downward trend over multiple consecutive quarters.

More intriguingly, Tencent Music also announced that starting from the next quarter, it would cease disclosing core operational metrics such as MAU and the number of paying users on a quarterly basis, opting instead for annual disclosures.

Despite improving profits, the user base is shrinking. While more revenue is being generated, listeners are quietly departing. What structural anxieties in the capital market are reflected behind Tencent Music's impressive profits?

I. Impressive Profits, but an Unconvincing Future

The "decline in quantity, increase in price" among users is the primary characteristic reflected in Tencent Music's financial report, as well as the biggest point of contention.

On one hand, the 528 million monthly active users represent a 5% decrease from the level in the fourth quarter of 2024.

On the other hand, while the total user base continues to dwindle, Tencent Music's number of paying users grew by 5.3% to 127.4 million, and the average revenue per paying user (ARPPU) increased by 7.2% to 11.9 yuan. The number of super members also surpassed 20 million in 2025.

From a gross margin perspective, Tencent Music's gross margin improved from 42.3% to 44.2% in 2025. The decline in user numbers did not become a negative factor affecting profits.

However, looking ahead, this growth model will eventually reach its limit.

As the user pool shrinks and the number of paying users increases, Tencent Music's paying user penetration rate has reached 24%. This means that one out of every four users is a paying user, which is already a very high proportion in the Chinese content market, where consumers are generally reluctant to pay.

If revenue growth is to be sustained, price increases will be inevitable.

On one hand, while ARPPU in the fourth quarter increased year-on-year, it remained flat compared to the third quarter, whereas the market had originally expected it to exceed 12 yuan. The failure to meet this expectation by just 0.1 yuan reflects the difficulty in breaking through the ceiling.

On the other hand, with ARPPU reaching 11.9 yuan, the annual membership fee now exceeds 140 yuan. In the Chinese content market, where consumers are reluctant to pay, further price increases may face scrutiny from users' "value anchor points." In 2022, a certain video platform's average monthly membership fee per user was between 13 and 15 yuan, and users are likely to make comparisons.

JPMorgan believes that Tencent Music's decision to stop disclosing quarterly MAU, paying user numbers, or ARPPU after this quarter is the clearest signal yet that the relevance of the past KPI-driven valuation basis is declining.

This poses a challenge to Tencent Music's narrative of user growth. It also presents a challenge in convincing investors in the capital market.

During the post-financial report conference call, Tencent Music's management, in response to questions, stated that looking ahead to 2026, subscription revenue may face some short-term pressure due to intense market competition. However, they believe that with a three-tier membership system and continuously improving non-subscription services, healthy, comprehensive, and sustainable growth can be achieved.

At the same time, management expects gross margins in 2026 to remain roughly in line with those in 2025 or to decline slightly.

II. Online Music: Sliding into Uncharted Territory

Compared to periodic declines, what worries Tencent Music more is that lost users may not return.

Qishui Music, with its logic of "zero-frame start, switch songs if unsatisfied," has emerged as a strong competitor in the online music market.

As of January 2026, the monthly active users of Qishui Music, ByteDance's first music app, have surged from 120 million to nearly 140 million, ranking fourth in the industry.

Qishui Music's user acquisition path has a low overlap with Tencent Music's. According to QuestMobile data, as of June 2025, 82.1% of Qishui Music's traffic came from Douyin. This means that Qishui Music is not siphoning away Tencent Music's core users, especially the younger generation accustomed to passively receiving music recommendations through short videos.

The loss of tail-end users is one of the reasons for Tencent Music's shrinking user base.

Over the past decade, Tencent Music has built its core competitive barrier around copyright. The underlying assumption of this logic is that users are willing to pay to listen to authentic, high-quality songs.

Qishui Music's emergence directly bypasses this assumption. Its strategy is to first use Douyin's traffic to attract users and then retain them with a model of "watching 80 seconds of ads for 24 hours of free listening."

Even if users choose to pay, the pricing of "monthly membership for around 8 yuan, annual membership for 88 yuan" is far lower than Tencent Music's. For users who have never developed a habit of paying or are highly price-sensitive, this is almost a zero-barrier choice.

Price is just the surface; the deeper crisis lies in the fact that the online music market is sliding into uncharted territory for Tencent Music.

Tencent Music is built on the logic of "people find songs": users open the app with a clear purpose to search for or play songs from their favorites.

Qishui Music, on the other hand, is entirely about "songs find people": with recommendations at its core and listening duration as a metric, it allows users to "keep scrolling even if they don't know what to listen to." This is a product of ByteDance's algorithm and community operations.

When ByteDance controls the most fragmented time of users, it can continuously cultivate user habits and even redefine what constitutes "good music"—for example, the 15-second chorus must be catchy, or emotions matter more than the artist.

Tencent Music can use the growth of SVIP members and the increase in ARPPU to prove that its existing users remain loyal. However, in this new phase, listening duration has become a more ruthless metric than user numbers or activity levels.

If young people form their "listening habits" within Qishui Music's ecosystem before developing a habit of paying, the cost for Tencent Music to win them back will be much higher than it is now. This user acquisition battle is about intergenerational shifts in mindset.

Beyond Qishui Music, there is an even more fundamental variable—AI.

In 2025, the volume of AI-generated music on major platforms surged. Users can simply input an emotional description and receive a song that "fits their current mood" within seconds, without the need for artists, record labels, or copyright payments.

Tencent Music CEO Liang Zhu stated during the financial report conference call that in the past three months, AI-created songs have begun appearing on music charts and are experiencing explosive growth.

However, for music, beyond production, the core remains the consumption scenario. For original songs, especially on the consumption side, no fundamental changes have occurred yet. Therefore, under the current circumstances, Tencent Music still hopes to allocate a portion of traffic to promote AI songs while ensuring that the traffic distribution for authentic original content remains unaffected.

This is also where Tencent Music's core user base lies. As previously analyzed when discussing NetEase Cloud Music, for core users who demand high sound quality and authenticity, Qishui Music is unlikely to win them over in the short term.

But for Tencent Music, the more important question is: After Qishui Music redefines some users' listening expectations with "free" and AI gradually erodes music production and distribution models, what can Tencent Music use to convince the next generation of users to pay for music?

III. New Growth: From Subscription to Project-Based Model

In 2025, non-subscription revenue from online music (offline performances, merchandise, etc.) became Tencent Music's "lifesaver." This segment's revenue surged by 39.2% to 9.07 billion yuan in 2025.

In 2025, Tencent Music led the operation of G-DRAGON's Asia-Pacific tour, spanning eight cities with 20 performances and attracting a cumulative audience of 260,000; collaborations with Ed Sheeran on merchandise also launched during the same period. This was a concentrated demonstration of Tencent Music's attempt to transform its online copyright assets into offline consumption scenarios.

This is also a clear direction Tencent Music is trying to pursue.

Tencent Music CEO Liang Zhu interpreted during the financial report conference call that many offline music experiences, including concerts, fan economy, and various merchandise products, are currently difficult to be fully replaced by AI. Therefore, Tencent Music will continue to intensify its efforts to develop high-quality IP and leverage AI to enhance content creation efficiency.

However, this seems more like a desperate move after online music subscriptions and social entertainment have peaked.

Moreover, the offline operations model is significantly "heavier" than online subscriptions, involving multiple influencing factors such as project planning, execution, user feedback, and merchandise sales, each requiring substantial investment. This conflicts with Tencent Music's long-standing "asset-light" model reliant on paid subscriptions.

Additionally, this model is highly susceptible to macroeconomic conditions, artist schedules, and unexpected events, resulting in unstable revenue. Relying on "selling merchandise" and "hosting concerts" to support Tencent Music's growth narrative seems somewhat flimsy.

JPMorgan's research report believes that Tencent Music is shifting from an obvious subscription compounding theme to a broader, low-visibility multi-engine monetization theme. The continuous expansion of this monetization mix is strategically positive, but these revenue sources are highly execution-dependent and event-driven, with much lower recurrence and profitability compared to subscription revenue.

In simple terms, an increase in project-based revenue will make growth in the next stage more difficult to predict and less likely to support the previous premium multiple framework.

Tencent Music, now in its middle age, remains the most profitable music company in China.

However, what the capital market truly wants to see is not a financial report proving that it can still reap past successes, but an answer on how it will win the future.

-

![]()

WeChat Collaborates with Huawei/Honor/Xiaomi on A2A: Is This the Dawn of AI Integration?

-

![]()

NVIDIA RTX Spark: Powerful, Yet Not the Ideal Choice for the Agent Era

-

![]()

NVIDIA RTX Spark: Powerful, but Is It the Right Fit for the Age of Agents?

-

![]()

A Genuine Threat or Just a Publicity Stunt? World's Premier AI Firm Warns: AI Evolving Autonomously, Slipping Beyond Human Control

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital