Where Has Roborock's Profit Gone?

03/22 2026

03/22 2026

548

548

By Dong Xuan

Source / Node AI

For Roborock, 2025 was a dramatic year.

The national 'trade-in' subsidy policy catalyzed demand, invigorating the industry. However, intense internal competition remained the norm, with battles over specifications, marketing, pricing, and more. Incumbents struggled to defend their positions while new entrants continued to join the fray, creating an unprecedented level of rivalry.

Amid this atmosphere, Roborock surged ahead globally, solidifying its position as the industry leader and achieving remarkable revenue growth.

Yet, on the profit front, Roborock faced its steepest decline since going public, presenting a scenario of 'revenue growth without profit increase.'

Where did the problem lie?

A 'Report Card' of Scaling Up

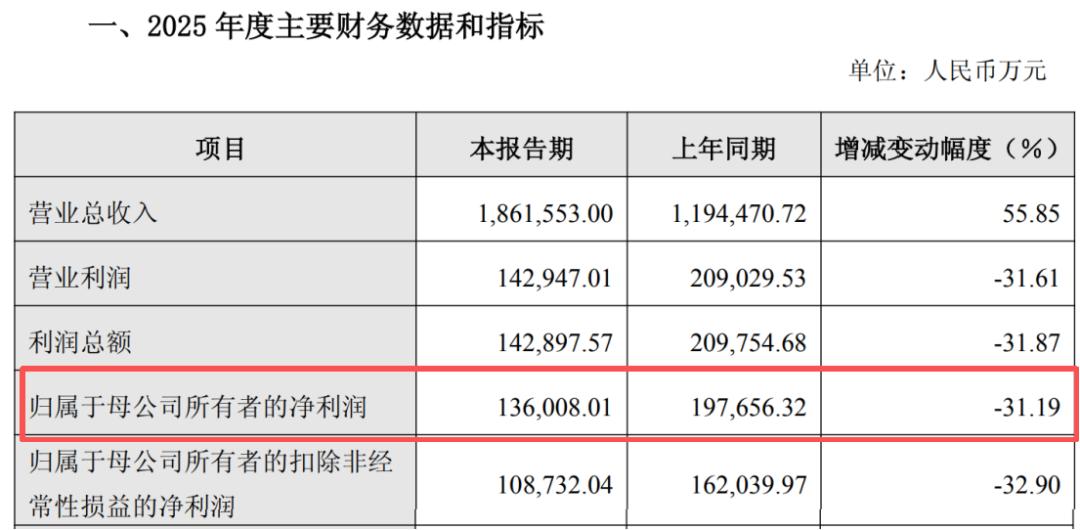

In 2025, Roborock (688169.SH) delivered a 'report card' marked by significant scaling.

Performance highlights showed the company achieving RMB 18.616 billion in annual revenue, up 55.85% year-on-year, setting a new historical high. This growth rate ranked among the highest among leading home cleaning appliance companies, showcasing strong upward momentum.

Simultaneously, Roborock achieved a milestone leap in market share.

According to IDC's latest report, global shipments of smart robot vacuums reached 32.72 million units in 2025. Roborock secured a 17.7% share with 5.8 million units, firmly holding the top spot. Rivals Ecovacs, Dreame, Xiaomi, and Narwal followed with 14.3%, 10.5%, 6.7%, and 5.3% shares, respectively.

Behind its global dominance lay Roborock's 'technology + marketing' dual-drive strategy.

On the technology front, the company maintained intense R&D investment, with R&D expenses reaching RMB 1.028 billion in the first three quarters of 2025, up 60.56% year-on-year and accounting for 8.52% of revenue—significantly higher than the industry average.

This investment translated into product innovations, including the world's first bionic robotic vacuum with a manipulator—the G30 Space Explorer Edition—along with the self-cleaning sweep-and-mop P20 Hydro Edition, A30 Pro Steam 5-in-1 Edition, and all-terrain lawn mower RockMow Z1/RockNeo.

At the recently concluded AWE 2026, Roborock showcased its technological prowess with the wheel-legged robotic vacuum G-Rover, the 'all-round flagship' G30S Pro, and the popular P20 Max, sparking industry buzz.

On the channel front, the company refined its product lineup across all price segments, from flagship premium to entry-level models, while advancing brand building, advertising, and refined operations. It engaged top influencers like Xiao Zhan, Zhou Ye, and Cyndi Wang as spokespersons and frequently appeared in live streams by Li Jiaqi.

In the first three quarters of 2025, Roborock's selling expenses surged to RMB 3.18 billion, up RMB 1.616 billion (103.42%) year-on-year, far outpacing overall revenue growth.

These multi-pronged strategies bore fruit: overseas revenue exceeded 50% of total revenue, with products available in over 170 countries and regions, serving over 20 million households. Market penetration exceeded 50% in core markets like South Korea and Northern Europe.

Where Has the Profit Gone?

Behind the market share triumph lay daunting challenges for Roborock.

Performance highlights revealed net profit attributable to shareholders of RMB 1.360 billion in 2025, down 31.19% year-on-year—the largest annual decline since its 2020 IPO—and marking a second consecutive year of decline, with the 2025 drop widening significantly.

Source: Roborock Performance Highlights

The disappointing results reverberated in the capital markets. The ' Sweeping Grass ' (a nickname referring to Roborock's dominance) saw prolonged declines. By March 20, 2025, its share price closed at RMB 126.49, with a total market cap of RMB 37.076 billion, having evaporated over RMB 60 billion from its peak.

Why the 'revenue growth without profit increase'? Node AI identifies three key pressures.

Strategically, Roborock pursued a scale-oriented approach since Q3 2024, aggressively expanding markets to capture global share.

While this strategy lifted revenue to new heights and secured the top global spot, it also eroded net profit.

Data confirms the impact: the company's gross margin fell from 55.13% in 2023 to 44.56% in H1 2025, with the core 'smart robot vacuums and accessories' margin dropping from 56.15% to 44.59%, slashing premium brand pricing power.

Gross margin stood at 43.73% in the first three quarters of 2025, down 10.13 percentage points from 53.86% in the same period of 2024.

Cost pressures were equally significant. As mentioned, hefty R&D and selling expenses consumed most of the gross profit space.

Third, short-term disruptions from new businesses. Roborock's 'second curve' ventures—washing machines, floor scrubbers, and lawn mowers—were all in investment phases, acting as major profit drains.

Kaiyuan Securities estimates that in 2025, Roborock's washing machine division lost RMB 500-600 million, floor scrubbers lost about RMB 200 million, and lawn mowers lost about RMB 100 million, collectively dragging net profit down by RMB 800-900 million.

In June 2025, reports surfaced of mass layoffs at Roborock's washing machine division in Nanjing, casting a shadow over its highly anticipated second curve.

Meanwhile, declining profitability weakened the company's cash-generating ability.

In the first three quarters of 2025, net cash from operating activities turned negative for the first time, at -RMB 1.06 billion. Inventories surged to RMB 3.716 billion, up about 150% from the start of the year, with inventory turnover days extending to 103.5.

Against this backdrop, Roborock rushed to list in Hong Kong just five years after its A-share debut, submitting a prospectus to the HKEX in June 2025 for an 'A+H' dual listing.

A Crossroads Decision

At the pinnacle of global dominance, Roborock faces a tough balancing act between 'scale' and 'profitability,' as well as 'long-term vision' and 'short-term pain.'

Its future trajectory and capital market reception hinge on effectively addressing internal and external challenges.

Internally, over-reliance on a single category remains a concern. In H1 2025, over 95% of revenue still came from smart cleaning products and accessories, with diversification still underway.

This concentrated revenue structure limits growth potential and leaves the company vulnerable to cyclical downturns. Any slowdown in the sector or intensified competition could impact performance.

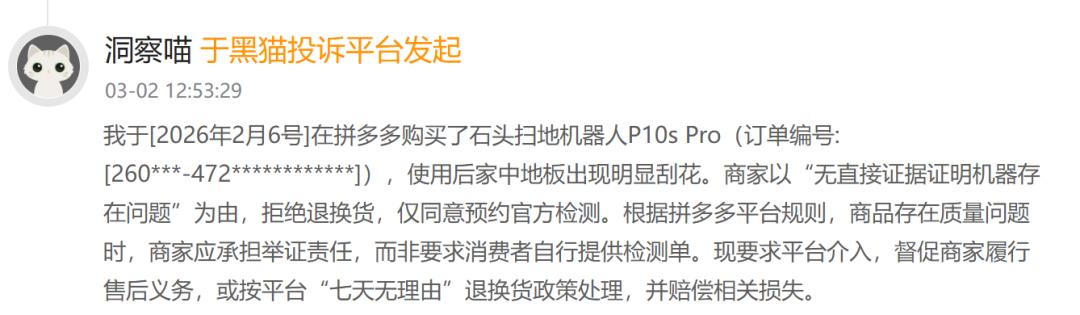

Quality control and after-sales issues also frequently arise, damaging brand reputation.

On the Black Cat Complaints platform, over 3,200 complaints relate to Roborock, covering the entire product lifecycle.

For instance, some consumers reported that their RMB 2,000+ Roborock sweep-and-mop machine required four factory repairs within two months. Others complained that their newly purchased P10s Pro vacuum scratched floors, with after-sales refusing returns or exchanges, citing 'no direct evidence of machine defects.'

Source: Black Cat Complaints

Externally, the environment remains challenging.

Traditional rivals are closing in. Ecovacs projected 2025 net profit of RMB 1.7-1.8 billion, up over 110% year-on-year, demonstrating a steady 'efficiency-for-profit' path. Dreame, ranked third globally, is gaining momentum.

More notably, cross-border giant DJI entered the robot vacuum market in August 2025, armed with deep technological reserves and poised to disrupt. Newcomer MOVA is also gaining traction with disruptive innovations like 'flying robot vacuums.'

Facing these challenges, Roborock has begun self-correction.

At its Q3 2025 earnings briefing, the company outlined three improvement measures: upgrading product mix; optimizing supply chains and channels by integrating global supply chains to cut costs and deepening DTC channel development to reduce intermediaries; and refining operations through technology-driven cost reductions and expense controls to solidify profitability.

Roborock's 2025 was both a global market leader and a company navigating 'growing pains.'

Its ability to rebuild investor confidence hinges on whether it can forge deeper technological barriers, strike a new balance between scale expansion and profit quality, and drive volume growth in its second curve.

For Roborock, a tough battle may just be beginning.

*Cover image generated by AI

-

![]()

WeChat Collaborates with Huawei/Honor/Xiaomi on A2A: Is This the Dawn of AI Integration?

-

![]()

NVIDIA RTX Spark: Powerful, Yet Not the Ideal Choice for the Agent Era

-

![]()

NVIDIA RTX Spark: Powerful, but Is It the Right Fit for the Age of Agents?

-

![]()

A Genuine Threat or Just a Publicity Stunt? World's Premier AI Firm Warns: AI Evolving Autonomously, Slipping Beyond Human Control

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital