Dissecting Alibaba's Earnings Report: Legacy Businesses Stabilize, New Growth Narratives Emerge

03/22 2026

03/22 2026

678

678

By Liang Tian

Source / Node AI

On March 19, Alibaba released its Q4 2025 financial results.

This is a classic earnings report from a company in transition: legacy businesses show weak growth, while new ventures are still scaling up.

In Q4, Alibaba achieved RMB 284.8 billion in revenue, up 2% YoY. Excluding the impact of divested businesses like Sun Art Retail, revenue grew 9% YoY on a like-for-like basis.

However, in stark contrast to modest revenue growth, profitability came under significant pressure: operating profit fell 74% YoY to RMB 10.65 billion; adjusted EBITA declined 57% YoY to RMB 23.4 billion, primarily due to increased investments in instant retail, user experience, and technology.

The numbers may not look impressive, but we must analyze long-term value. In Node AI's view, instant retail and AI are becoming Alibaba's new growth engines, making these investments worthwhile.

Legacy Businesses Stabilize as Instant Retail Takes Off

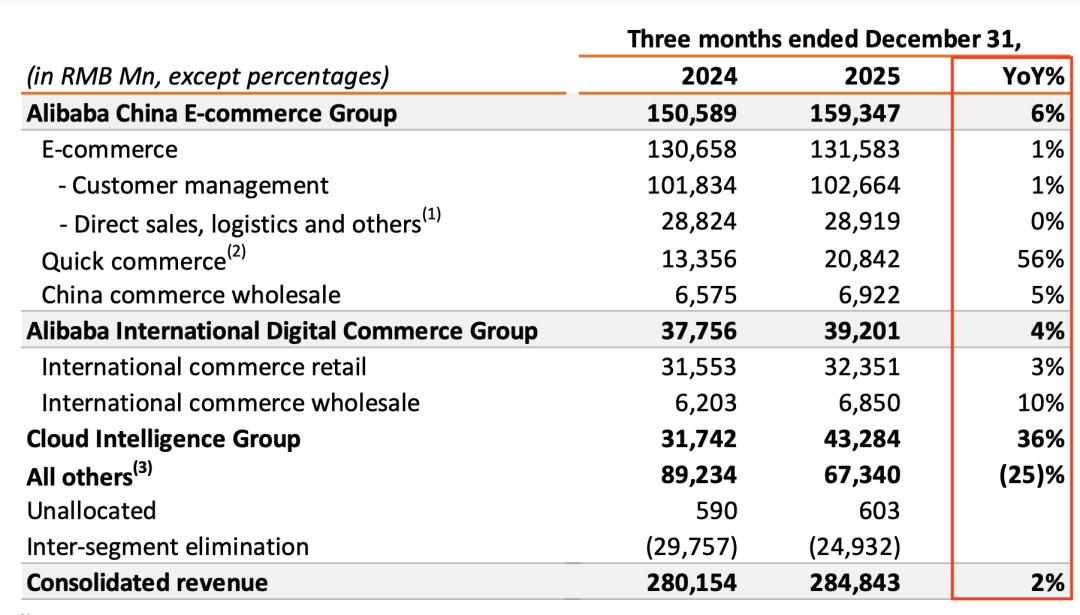

First, let's examine the legacy businesses. In Q4, Alibaba's China e-commerce group generated RMB 159.35 billion in revenue, up 6% YoY.

Breaking it down, overall performance remained stable.

E-commerce revenue reached RMB 131.58 billion, up just 1% YoY; customer management revenue grew 1% YoY to RMB 102.66 billion. For comparison, customer management revenue grew 10% YoY in the previous quarter.

While many may view this growth rate negatively, we believe it reflects three factors: the phase-out of China's 2025 consumer subsidies, a high base in 2024, and the later Chinese New Year, which delayed shopping demand to Q1 2026.

While the former cash cow remains stable, new businesses are shining.

In Q4, instant retail revenue (including Taobao Flash Sales) surged 56% YoY to RMB 20.84 billion. Alibaba also signaled positive trends in its earnings report: user engagement in instant retail continues to strengthen, scale keeps growing, UE (unit economics per delivery) is improving, and monthly active consumers on the Taobao app achieved double-digit YoY growth.

Notably, instant retail claimed the top market share in Q4. Analysys data shows Taobao Flash Sales captured 45.2% of the instant retail transaction market in Q4 2025, narrowly leading Meituan (45.0%) by 0.2 percentage points, with JD trailing at 8.4%.

However, this market share partially reflects Alibaba's subsidy strategy.

Adjusted EBITA fell 57% YoY to RMB 23.4 billion, which the earnings report attributed primarily to investments in instant retail, user experience, and technology. Heavy subsidies also impacted free cash flow, which declined 71% YoY to RMB 11.35 billion from RMB 39.02 billion in Q4 2024.

Management signals continued investment.

Daniel Zhang stated on the earnings call: "We maintain our FY28 target of over RMB 1 trillion in total transaction volume for instant retail. At this scale, we believe we can achieve Scale positive cash flow (scalable positive cash flow). We also expect the instant retail business segment to turn profitable in FY29."

This strategy makes sense. With traditional e-commerce nearing saturation, betting on instant retail—a trillion-RMB market—is Alibaba's logical choice. It warrants continued investment, as patience may yield long-term rewards.

AI: Not Just a Chat Tool, But a New Gateway

Beyond instant retail, Alibaba is using AI to reshape lifestyle services and consumer entry points.

A key disclosure in the earnings report: the Qianwen App integrated Taobao Flash Sales on January 15, with platform-wide MAU exceeding 300 million in February. 140 million users completed tasks like shopping, food delivery, and flight bookings via Agent functions.

This data suggests Alibaba believes C-end AI Agents have reached initial viability within its ecosystem.

Clearly, Alibaba aims beyond chatbots—it wants AI to connect the entire consumption ecosystem. By linking AI with real-life service scenarios, it can convert "traffic" into "transaction closures."

This differentiates Alibaba from pure-play model companies.

Cloud and AI: Fueling Imagination?

Unlike the pressure on e-commerce, let's examine the cloud business with the most imagination.

According to the earnings report, Alibaba Cloud revenue grew strongly by 36%, with AI-related product revenue achieving triple-digit growth for the tenth consecutive quarter.

These are impressive figures. Eddie Wu stated on the earnings call: "AI is one of our primary growth engines. Our commercial goal for the group's AI strategy is to exceed $100 billion in cloud and AI commercialization revenue (including MaaS) over the next five years."

This confidence stems from Alibaba Cloud's market position, as highlighted in the earnings report:

In Gartner's 2025 Magic Quadrant for Cloud Database Management Systems, Alibaba Cloud ranked as a Leader for the sixth consecutive year. In Gartner's Emerging Market Quadrant for Generative AI Technology, Alibaba Cloud was again named an Emerging Leader across all four assessment quadrants, the only cloud provider in Asia-Pacific to achieve this. Meanwhile, IDC's November 2025 China Hybrid Cloud Market Share report shows Alibaba Cloud maintaining its leadership in China's hybrid cloud PaaS and services market.

Impressive as these accolades are, some caveats remain.

We note that cloud profit growth lagged at 25%, significantly below the 36% revenue growth, indicating substantial spending on customer acquisition and capacity expansion.

However, high-margin AI revenue could sustain cloud growth long-term. The earnings report revealed AI-driven revenue achieved "triple-digit growth for ten consecutive quarters."

While specific figures were undisclosed, organizational moves suggest Alibaba is reaping rewards and doubling down on AI commercialization.

On March 16, Alibaba announced the establishment of the ATH Business Group, led directly by CEO Eddie Wu. Focused on "creating Tokens, delivering Tokens, and applying Tokens," it integrates five business units: Tongyi Labs, Bailian MaaS, Qianwen, Wukong, and AI Innovation into an independent organization.

Post-restructuring, Alibaba's business structure consists of: Alibaba China E-Commerce Group, Alibaba International Digital Commerce Group, Cloud Intelligence Group, Alibaba Token Hub (ATH) Business Group, and other businesses.

This restructuring's significance lies in aligning upstream model R&D, midstream computing power, and downstream applications within one organizational framework, facilitating technology R&D and product demand alignment.

Products are Alibaba's next focus—the day after announcing the ATH Business Group, it launched the enterprise-grade Agent platform "Wukong," directly closing the loop with its existing ecosystem.

For example, Taobao's B2B department can integrate Skills, enabling merchants to outsource finance, design, development, product management, and marketing to Agents.

This adjustment also signals Alibaba's shifting focus toward operations.

The coexistence of Cloud Intelligence Group and ATH suggests Alibaba is categorizing infrastructure and AI commercialization into two clearer systems: the former focuses on computing power and enterprise deployment, while the latter emphasizes Token monetization.

From Eddie Wu's earnings call remarks, Alibaba now prioritizes not just Qwen's model capabilities but how to integrate them into enterprise and consumer scenarios, converting them into MaaS revenue and cloud resource demand.

Alibaba Aims to Replicate Google's Success

Both AI-to-B and AI-to-C development require computing power support. To achieve hardware-software synergy, Alibaba is pursuing China's "Google narrative."

Google's "trinity" is well-known: Gemini (model) + Google Cloud (platform) + TPU (self-developed chips).

Alibaba's equivalent is "Tongyunge": Tongyi Labs (Qwen large model) + Alibaba Cloud + T-Head (self-developed chips like Hanguang, Yitian, and PPU).

Good news emerged in the earnings call: Eddie Wu mentioned T-Head's progress, with cumulative chip shipments exceeding 470,000 units and annual revenue reaching tens of billions, 60% serving external clients. Unlike external chip companies, T-Head emphasizes deep co-design (collaborative design) with Alibaba Cloud infrastructure and Tongyi Qianwen models to enhance cost-effectiveness.

The earnings report described T-Head as "now making significant contributions to our cloud infrastructure supply." If self-developed chips indeed reduce inference costs, long-term profitability should benefit.

Post-earnings, markets and media reacted cautiously. However, at Node AI, we believe turning an elephant requires patience—pain is almost inevitable.

The value of this earnings report lies not in short-term numbers but in Alibaba's clear bet on instant retail and AI as new growth engines.

The narrative holds imagination, but ultimate success depends on subsequent data validation.

-

![]()

WeChat Collaborates with Huawei/Honor/Xiaomi on A2A: Is This the Dawn of AI Integration?

-

![]()

NVIDIA RTX Spark: Powerful, Yet Not the Ideal Choice for the Agent Era

-

![]()

NVIDIA RTX Spark: Powerful, but Is It the Right Fit for the Age of Agents?

-

![]()

A Genuine Threat or Just a Publicity Stunt? World's Premier AI Firm Warns: AI Evolving Autonomously, Slipping Beyond Human Control

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital