Micron MU: AI Drives Storage 'Skyrocketing,' Can It Break the 'Tightening Spell' of Cycles?

03/23 2026

03/23 2026

486

486

Micron (MU.O) released its earnings report for the second quarter of fiscal year 2026 (ending January 2026) after the market closed on March 19, 2026, Beijing time. Key points are as follows:

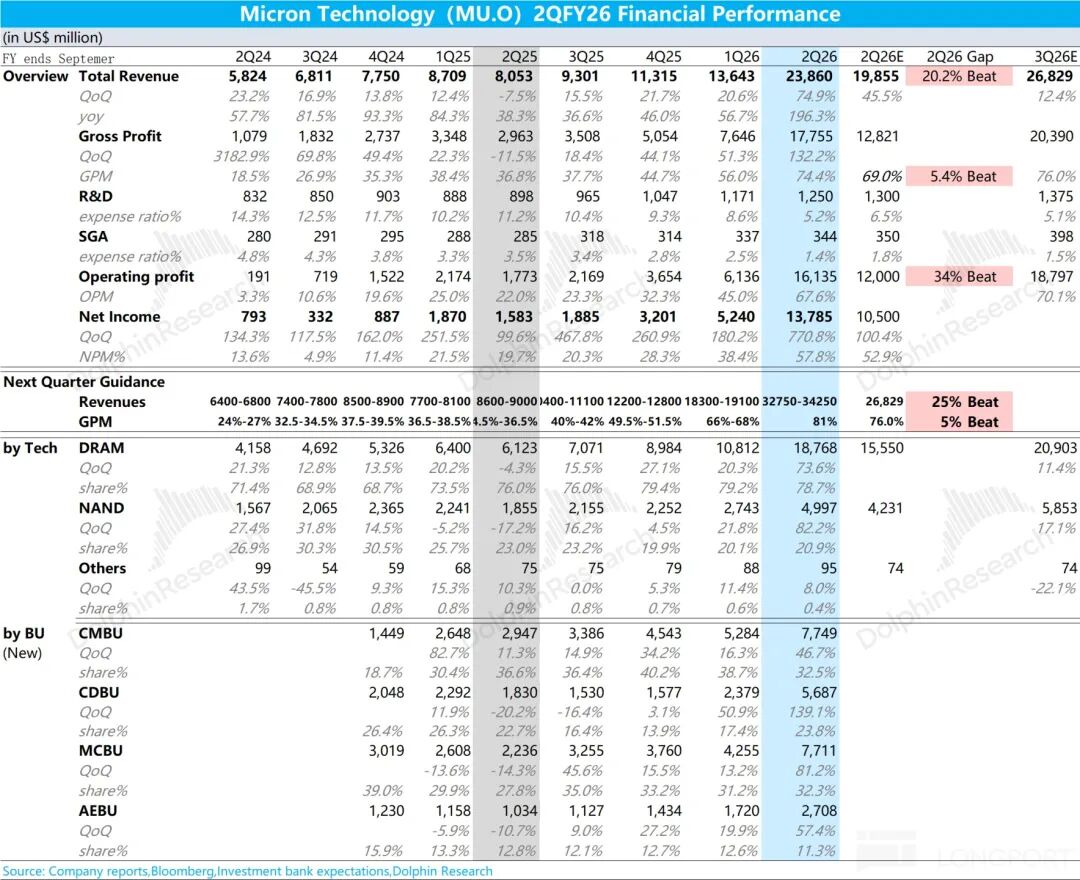

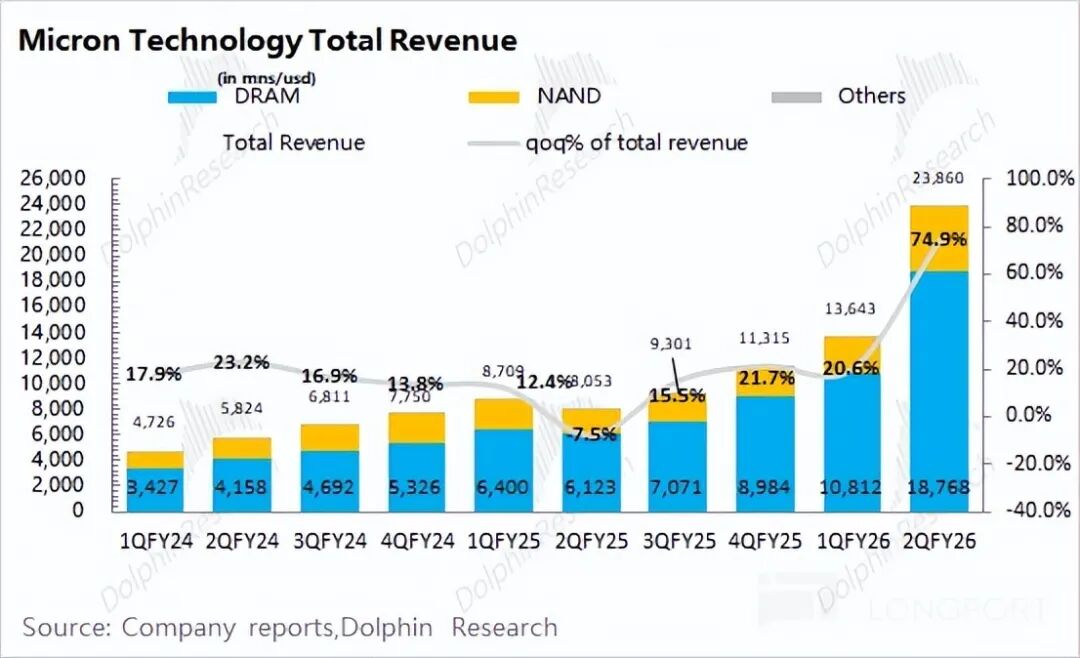

1. Overall Performance: Micron's revenue for this quarter was $23.86 billion, up 75% sequentially, outperforming the raised buyer expectations ($19.9 billion). The revenue growth was primarily driven by the dual contributions from the DRAM and NAND businesses, both of which saw sequential growth exceeding 70%.

The company's gross margin for this quarter reached 74.4%, outperforming the raised buyer expectations (69%). Affected by the significant increase in storage prices, the average prices of DRAM and NAND both rose by over 60% sequentially this quarter.

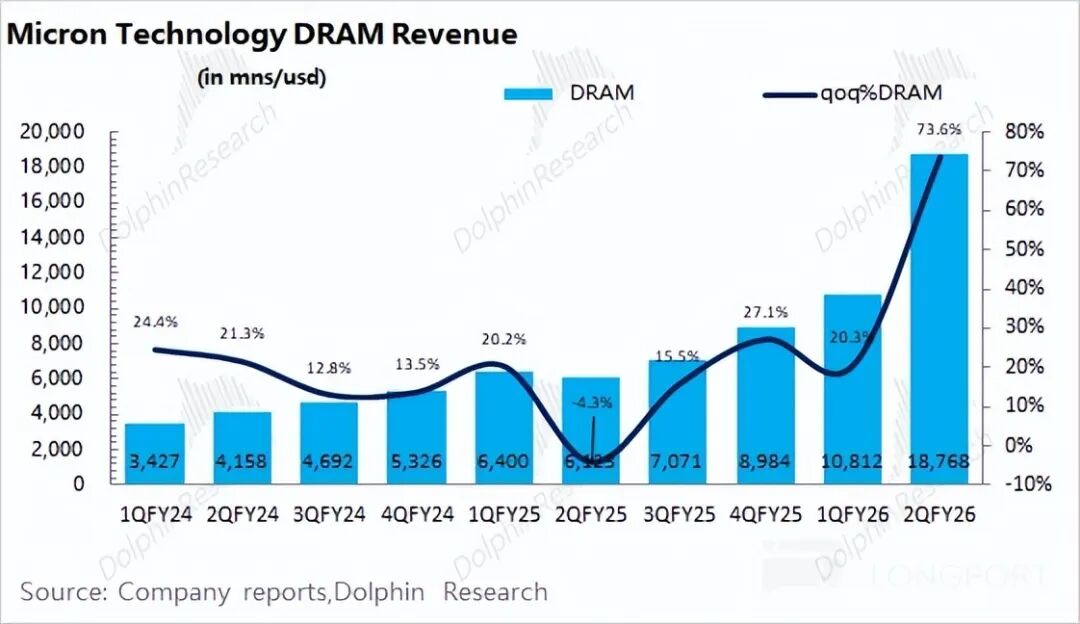

2. DRAM Business: This quarter, DRAM revenue reached $18.8 billion, up 73.6% sequentially, primarily driven by rising storage prices. The company's average DRAM price increased by approximately 65% sequentially this quarter, while shipments rose by 5%.

Specifically: ① Traditional DRAM contributed the largest increase, with estimated revenue of approximately $16 billion this quarter, up over 80% sequentially. AI demand is beginning to drive a rebound in DDR product demand; ② Dolphin Research estimates HBM revenue at approximately $2.7 billion this quarter, up about $500 million sequentially, mainly benefiting from the mass production and shipment of HBM3E and HBM4;

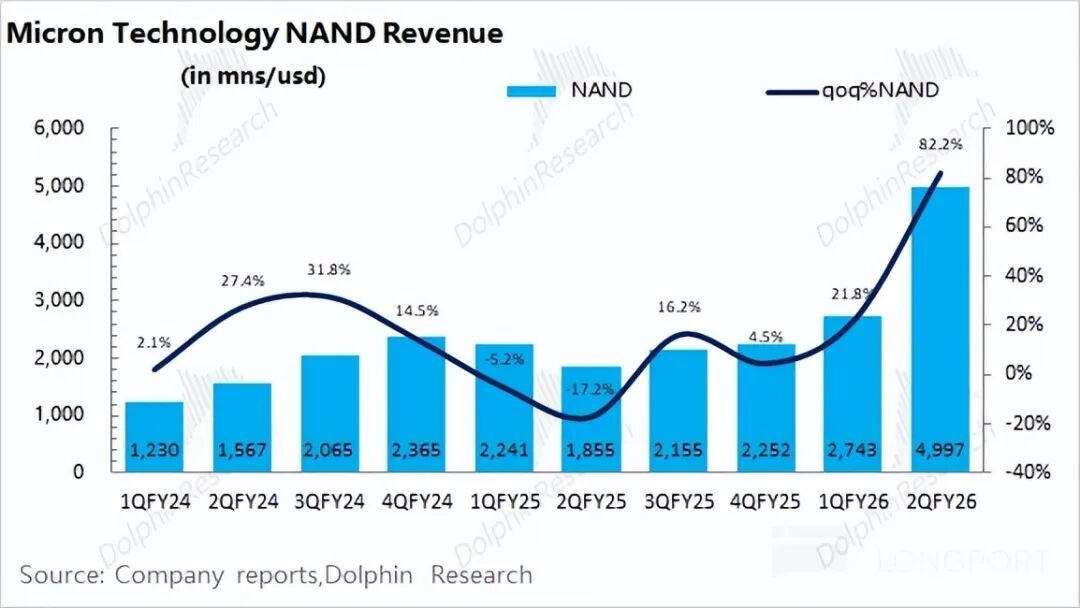

3. NAND Business: This quarter, NAND revenue reached $5 billion, up 82% sequentially. The company's NAND revenue was also primarily driven by price increases, with shipments rising approximately 2% sequentially and average prices increasing by about 78% sequentially this quarter.

Previously affected by the prolonged downturn in the NAND market, the industry had reduced some NAND production capacity. However, as AI demand extends to the NAND sector, a supply-demand mismatch has driven a significant increase in NAND prices.

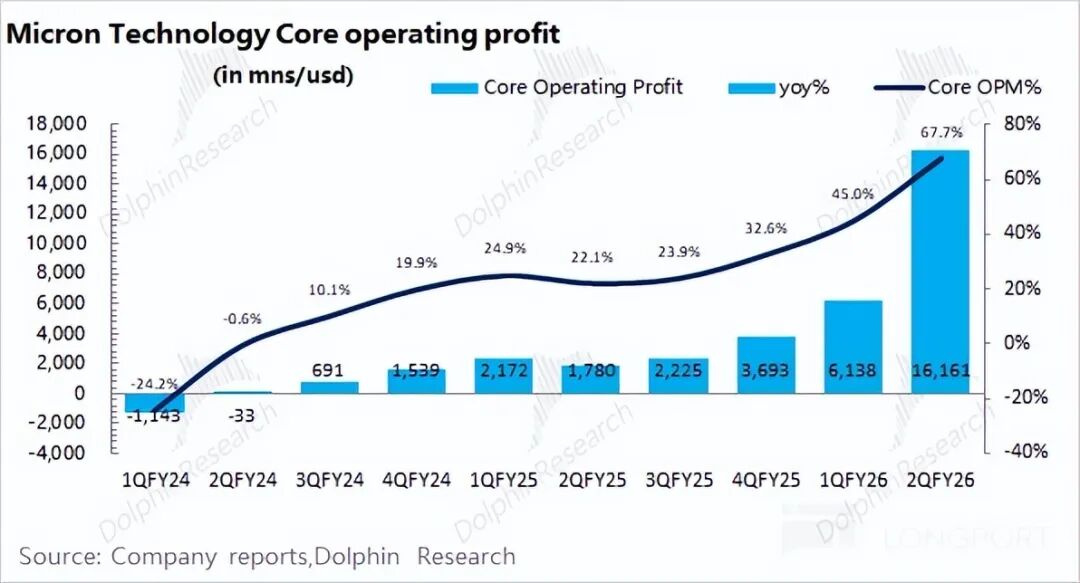

4. Operating Expenses: Influenced by revenue expansion, the company's R&D expense ratio and sales & administrative expense ratio continued to decline. The company's core operating profit for this quarter was $16.1 billion, with the core operating profit margin increasing to 67.6%. The key drivers of the company's operating profit improvement were revenue and gross margin. Driven by significant increases in the average prices of DRAM and NAND, the company's gross margin will exceed 74%.

5. Micron Technology's Performance Guidance: For the third quarter of fiscal year 2026, revenue is expected to be approximately $32.75-34.25 billion, outperforming market expectations ($26.8 billion). The company expects a gross margin of around 81% for the third quarter of fiscal year 2026, outperforming market expectations (76%). The company's guidance for next quarter significantly exceeds market expectations, still driven by continued price increases in traditional storage products.

Dolphin Research's Overall View: Despite 'Explosive' Performance, Management Communication Falls Short of Expectations

Micron's revenue and gross margin for this quarter significantly outperformed market expectations. With only a slight increase in shipments, the performance growth was primarily driven by significant increases in storage prices.

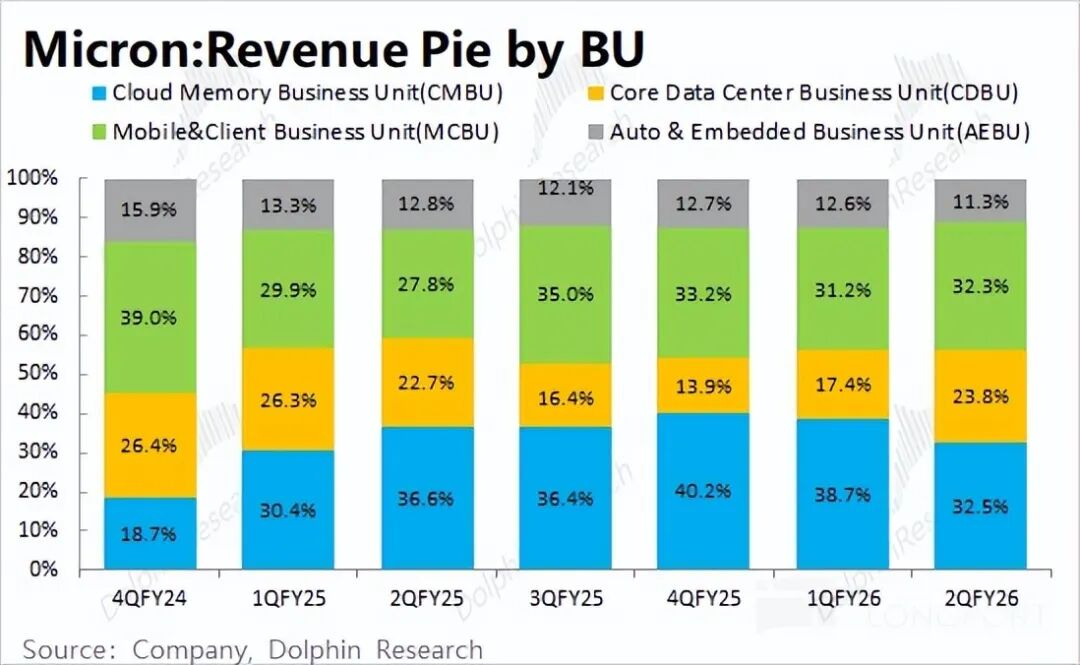

The company previously reclassified its business segments. In addition to the accelerated growth in the Cloud Memory Business Unit (CMBU), the Core Datacenter Business Unit (CDBU) and Mobile & Client Business Unit (MCBU) were the main drivers of high growth this quarter, propelled by significant price increases in traditional storage products.

The company's guidance for next quarter greatly exceeds market expectations. Micron expects revenue of $33.5 billion (±$750 million) next quarter, up $9.6 billion sequentially, surpassing market expectations ($26.8 billion). The gross margin is expected to reach around 81%, significantly exceeding buyer expectations (76%), indicating another substantial price increase for storage products next quarter.

Beyond recent performance, the main areas of focus for Micron include:

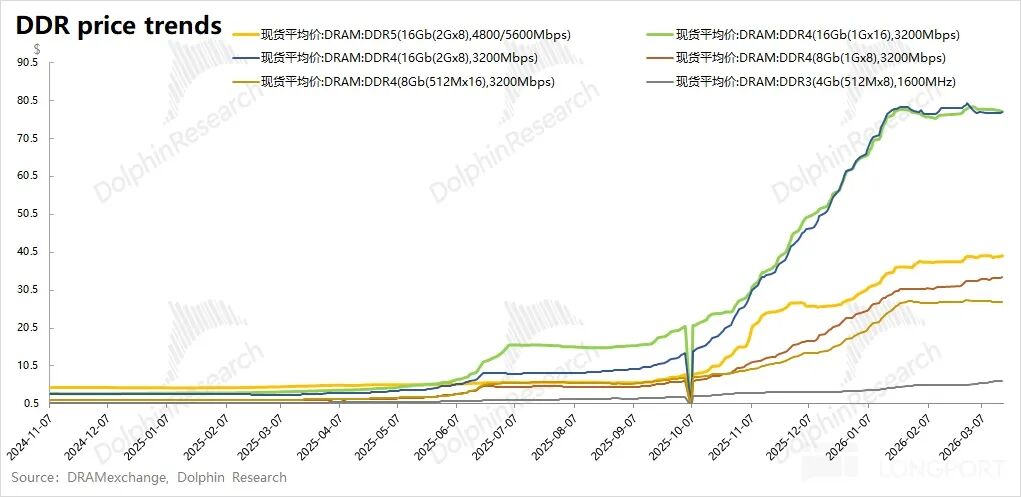

a) The Major Cycle of Traditional Storage: Nearly 80% of Micron's revenue comes from the DRAM business, with most contributions from non-HBM DRAM products. The significant increase in DDR product prices has a more pronounced impact on the company's performance, as it is still in a broad cycle of comprehensive price increases.

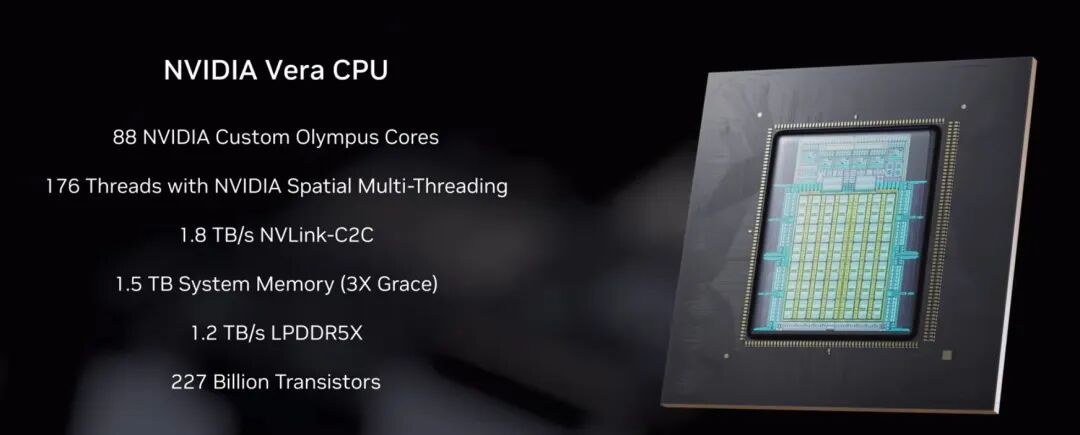

As the focus of AI large models shifts from training to inference, demand for DDR and other products has increased: ① The demand for DDR on the CPU side, with a single Vera CPU's DDR demand increasing to 1.5TB (three times that of Grace) compared to Grace; ② Rubin CPX directly chose GDDR7 instead of HBM.

b) Certainty of AI Storage Capacity: This round of the storage cycle is primarily driven by incremental AI demand, while the traditional PC and smartphone end markets remain sluggish. Cloud service providers are the ultimate 'buyers.' Based on the outlooks of major companies, capital expenditures will continue to grow at a high rate in 2026-2027.

Combined with NVIDIA's product layout (product layout translates to 'product strategy' or 'product layout' in this context, but keeping ' layout ' as it's a term often used in tech industry analyses in Chinese), the main contradiction ( contradiction translates to 'contradiction' or 'challenge,' but in this context, it refers to the primary challenge) in data centers has shifted from 'computing power' to 'storage.' From Blackwell to Rubin, newly introduced DPU (NAND) and LPU (SRAM) are targeted at the storage sector.

On one hand, Google's TPU can already support FP8, meeting most inference demands, and the computing power advantage is narrowing. On the other hand, computing power is advancing too quickly, while memory access speeds cannot keep up, creating a 'memory wall' issue. Therefore, when models shift from training to inference, storage capacity becomes more important than computing power.

c) Capital Expenditures and Outlook: The company has again raised its capital expenditures for fiscal year 2026 to $25 billion (up from $20 billion last quarter), outperforming market expectations of around $22.5 billion.

Management provided a significantly increased outlook for capital expenditures in fiscal year 2027 but mentioned in a subsequent analyst briefing that capital expenditures might decline after fiscal year 2027.

① Short-term perspective: Currently in a broad cycle of storage price increases, compounded by the recent Samsung strike, performance is expected to continue exceeding expectations.

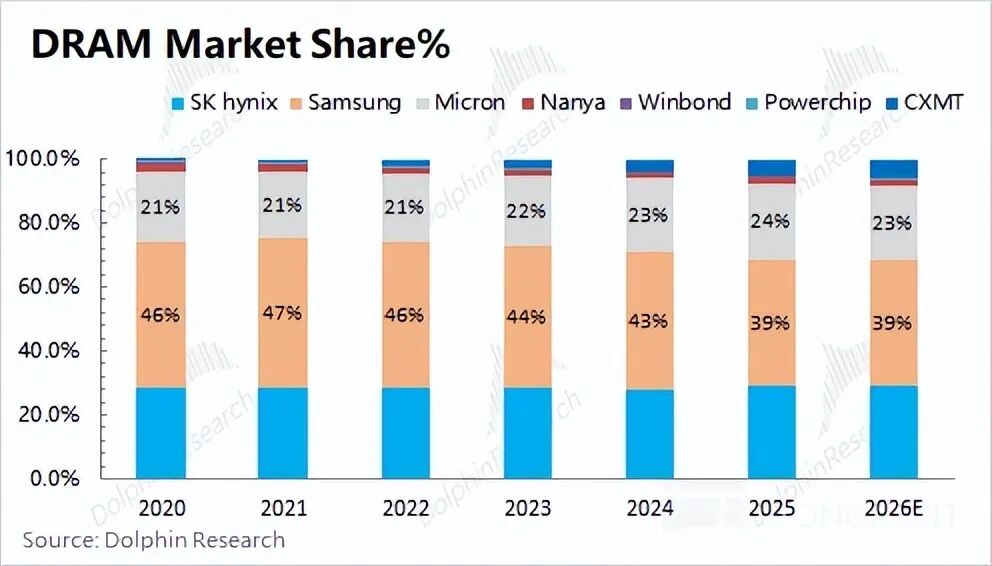

Samsung strike: Samsung holds nearly 40% of the DRAM market share. Recently, Samsung Electronics employees have become increasingly dissatisfied with the salary gap compared to SK Hynix, and union members voted to strike for 18 days starting May 21. Once production halts, restarting production lines could take up to two months.

② Medium to long-term perspective: Compared to performance exceeding expectations, the market is more concerned about 'sustained profitability,' including long-term agreements (lock-in orders), customer demand assurance, and the outlook for fiscal year 2027 and beyond. If cloud service providers are willing to sign long-term agreements to secure supply, it can further increase the certainty of the company's subsequent performance growth.

Regarding the market's main concerns, management provided some responses during communications:

1) Long-term agreements: Upgraded from long-term agreements (LTAs) a year ago to 5-year strategic customer agreements (SCAs), with the first major customer already signed. This appears more like deepening cooperation rather than a lock-in order form.

2) Customer demand assurance: Micron can only meet 50% to 2/3 of the medium-term demand from core customers, with no significant change in this proportion compared to three months ago;

3) Outlook for fiscal year 2027: The company believes that the supply-demand gap in the storage industry will persist in 2027 but cannot predict the gap beyond 2027. The company will significantly increase capital expenditures in fiscal year 2027 but also mentioned in a subsequent analyst briefing that 'capital expenditures might decline after fiscal year 2027.' (Detailed meeting notes can be viewed on the Longbridge App).

From the company and industry outlooks, the company's growth in 2026-2027 is relatively certain. Currently, there is no change in customer demand assurance, and the company is relatively cautious about performance beyond 2027, also mentioning the possibility of 'capital expenditure declines after fiscal year 2027' in communications.

Compared to 'short-term explosive' performance, the market is more eager for the storage industry to 'break free from or smooth out' cyclical constraints. Based on the company management's outlook on capital expenditures, Micron's valuation must still be viewed from the perspective of a 'cyclical stock,' which will still limit the company's upside potential.

Below is a detailed analysis:

I. Overall Performance: Revenue & Gross Margin Greatly Exceed Expectations

1.1 Revenue

Micron's total revenue for the second quarter of fiscal year 2026 was $23.86 billion, up 75% sequentially, outperforming market expectations ($19.9 billion). The sequential revenue increase was driven by both DRAM and NAND.

From a downstream perspective, data centers and networks contributed the most significant increase, while departments like mobile phones and PCs also saw noticeable growth due to price increases in traditional storage products.

Based on the company's guidance for next quarter, revenue is expected to be approximately $32.75-34.25 billion, up about 40.4% sequentially, outperforming market expectations ($26.8 billion). Dolphin Research believes the company is still in a storage price increase cycle, with next quarter's revenue growth primarily driven by price increases in traditional storage products.

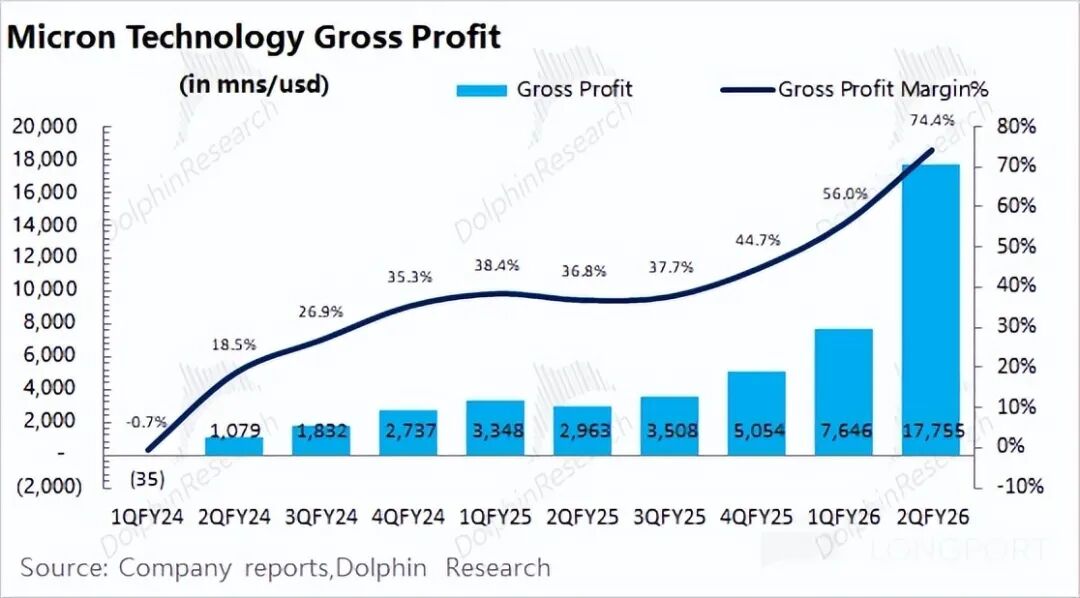

1.2 Gross Profit

Micron achieved a gross profit of $17.8 billion in the second quarter of fiscal year 2026, with a gross margin of 74.4%, up 18.4 percentage points sequentially. The gross margin improvement was primarily driven by price increases in traditional storage products.

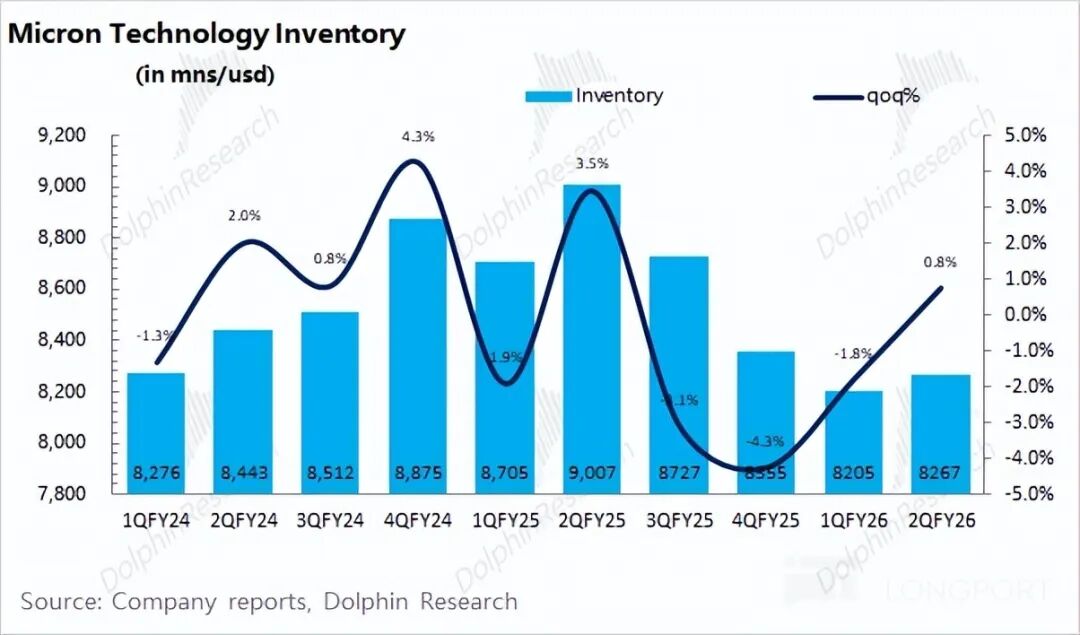

Although the company's current inventory is $8.27 billion, up 0.8% sequentially, driven by data center and related demands, the current inventory turnover days have decreased to 121 days, a relatively low level.

The company expects a gross margin of around 81% next quarter, up another 6.6 percentage points sequentially, indicating continued price increases for traditional DRAM and NAND products next quarter. Considering the possible Samsung factory strike, the company's gross margin next quarter has the opportunity to exceed guidance again.

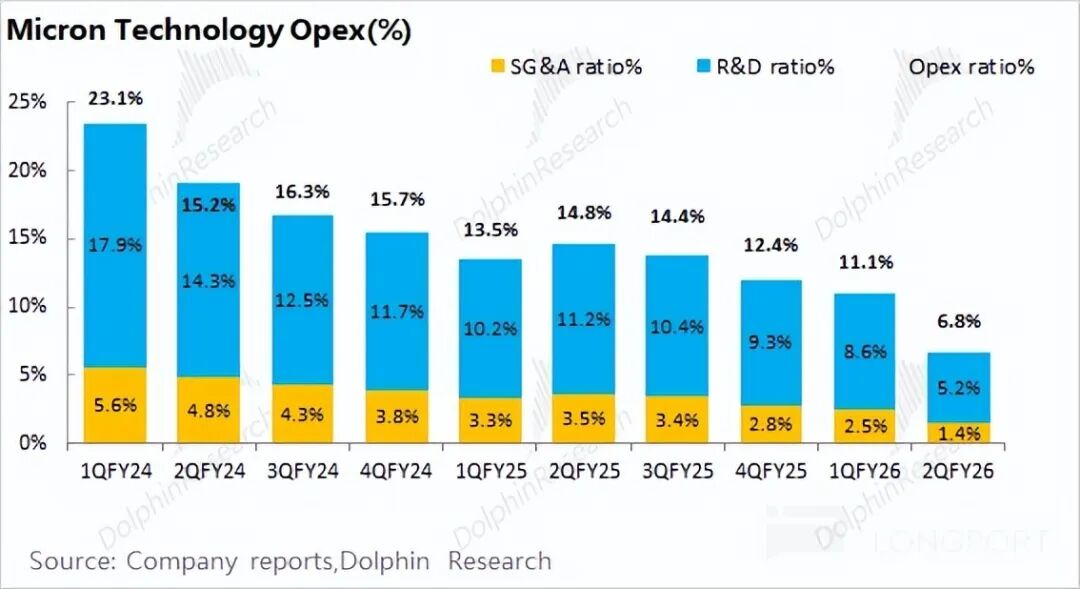

1.3 Operating Expenses

Micron's operating expenses for the second quarter of fiscal year 2026 were $1.62 billion, up 7.3% sequentially. Due to faster revenue growth, the company's operating expense ratio decreased to 6.8% this quarter.

The company's core operating profit for this quarter was $16.16 billion, with sequential growth primarily driven by revenue growth and gross margin improvement. Overall, since the company's operating expenses remained relatively stable, the profit improvement was mainly influenced by the two core indicators: revenue and gross margin.

II. Segment Performance: Significant Price Increases in Traditional Storage Drive Performance

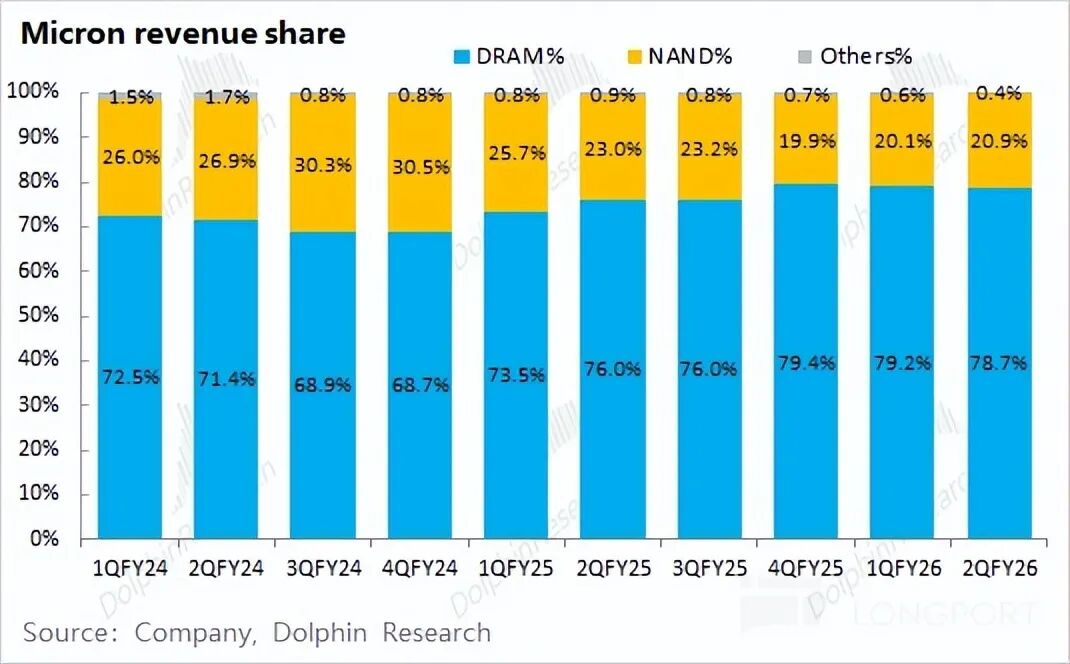

From the latest earnings report, DRAM and NAND remain the company's most important revenue sources, with DRAM accounting for around 80% of revenue.

Additionally, Micron previously adjusted its disclosure categories (revenue breakdown by downstream markets), reclassifying the original CNBU, SBU, MBU, and EBU into four categories: CMBU, CDBU, MCBU, and AEBU. Currently, data centers and cloud services account for over 50% of revenue, and the business category adjustment highlights the company's emphasis on related businesses.

2.1 DRAM

DRAM is the company's largest source of revenue, accounting for nearly 80% of the total. In this quarter, the company's DRAM business revenue grew to $18.77 billion, a 74% increase quarter-over-quarter. The average DRAM price in this quarter increased significantly by about 65% quarter-over-quarter, while shipments also saw a 5% increase quarter-over-quarter.

Breaking it down, Dolphin Research estimates that the company's HBM revenue for this quarter was approximately $2.7 billion, an increase of about $500 million quarter-over-quarter. Revenue from products such as DDR was around $16 billion, with a quarter-over-quarter growth of over 80%.

DRAM is the company's core business, primarily consisting of products such as HBM and DDR.

1) HBM:

The company announced that it will not disclose HBM quarterly figures separately. Considering industry and company conditions, Dolphin Research expects the company's HBM business revenue for this quarter to be approximately $2.7 billion, an increase of about $500 million quarter-over-quarter.

The company's HBM products are in the second-supplier position for NVIDIA, lagging behind SK Hynix in terms of product progress. With Samsung's HBM3E passing NVIDIA certification, the HBM market will be redistributed, bringing the three manufacturers back to the "same starting line."

As NVIDIA's Rubin GPU and AMD's MI400 will both feature HBM4, the focus will now be on the progress and shipments of each company's HBM4 products to gain a larger share in the HBM market.

2) Products such as DDR:

From the business breakdown, the company's revenue from products such as DDR in this quarter was around $16 billion, an increase of over 80% quarter-over-quarter. Although demand from traditional end markets such as mobile phones remains relatively weak, data centers and AI have impacted the original supply-demand landscape, driving significant price increases for products such as DDR.

As the focus of AI large models shifts from training to inference, demand for products such as DDR has increased:

① The demand for DDR on the CPU side will increase to 1.5TB per Vera CPU (three times that of Grace) compared to Grace; ② NVIDIA's Rubin CPX has directly chosen GDDR7 over HBM, which will also drive increased demand for DDR products;

2.2 NAND

NAND is the company's second-largest source of revenue, accounting for about 20%. In this quarter, the company's NAND business revenue was $5 billion, an 82% increase quarter-over-quarter. While NAND shipments in this quarter saw a slight 2% increase quarter-over-quarter, the average product price increased significantly by about 78% quarter-over-quarter.

Previously, the impact of AI Capex on the storage sector was mainly in the HBM area, causing NAND to underperform DRAM significantly. However, as the focus of large models shifts from training to inference, the impact of AI capital expenditures is beginning to extend outward, benefiting NAND as well.

Supply and demand changes: On the supply side, the previous downturn in the NAND market led some manufacturers to cut NAND production lines. The three major manufacturers prioritized DRAM over NAND in their expansion plans. On the demand side, the AI industry chain has increased demand for NAND, such as the addition of a NAND layer in NVIDIA's Rubin.

NVIDIA has added an "Inference Context Memory Storage Platform" (ICMS platform) to the Rubin architecture: The newly added ICMS dedicated context memory will shift KV Cache from HBM to a more cost-effective storage medium, freeing up HBM bandwidth for computation, thereby reducing costs during the inference phase.

Each Rubin GPU can additionally support 16TB of NAND (as "external memory"), allowing a single NVL72 to expand its NAND demand by 1152TB.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is permitted only with authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any person receiving this report. Investors must consult with an independent professional advisor before making any investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibility or loss that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions mentioned in this report may not be regarded or construed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction, nor do they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials in this report are not intended for distribution to or for use by citizens or residents of jurisdictions where such distribution, publication, provision, or use of the information, tools, and materials would conflict with applicable laws or regulations or would subject Dolphin Research and/or its subsidiaries or affiliated companies to any registration or licensing requirements in such jurisdictions.

This report only reflects the personal views, insights, and analytical methods of the relevant contributors and does not represent the position of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

May Auto Sales Insight: Joint Ventures Falter, New Entrants Rise, with Exports Lending Support?

-

![]()

Model Substitution, Data Vending, and Remote-Control Backdoors! Ministry of State Security Alerts to Risks in 'AI Relay Platforms'

-

![]()

Zhao Ming Departs, IPO Postponed, AI Phones Underperform—Can Honor Still Live Up to Its Name?

-

![]()

Explosion of Recording Hardware! Four Major Product Categories Compete for New AI Entry Points, with Agent Capabilities Becoming Standard

-

![]()

China’s LEO Satellite Internet Achieves Strategic Progress: Over 100 Additional Satellites Set for Launch

-

![]()

Musk Sustains $88 Billion Loss in AI Pursuit, Now Rents GPUs to Rivals, Anticipating $500 Billion Revenue Over Three Years

-

![]()

Report | Token Economics: Envisioning a New Path for RMB Internationalization

-

![]()

Trends丨Gartner's Latest Forecast: These Seven Transformations Will Reshape the Technology Landscape Over the Next Five Years