Unitree's IPO: A Milestone in Humanoid Robot Development

03/23 2026

03/23 2026

417

417

Produced by Zhineng Technology

Unitree is going public. On March 20, the Shanghai Stock Exchange officially accepted Unitree Technology's application for listing on the STAR Market.

This marks the second project under the 'pre-review mechanism' and is seen by many as a signal: the humanoid robot sector is now entering the main stage of the capital market.

The story itself is straightforward. A company specializing in quadrupedal robots achieved global leadership in seven years. Two years ago, it pivoted to humanoid robots and, in another two years, became the world leader in shipments. From Spring Festival Gala performances to backflips and martial arts displays, the company has moved from the lab into public view.

If you only look at these milestones, the trajectory seems nearly perfect. The company is strong now, but where does its strength truly lie? More critically—what will it rely on to keep moving forward?

01

5,500 Units Sold,

But Who Are the Real Customers?

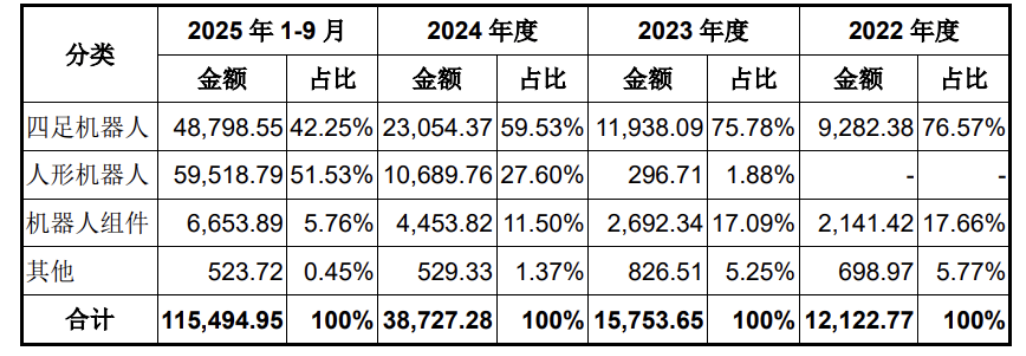

Start with the most intuitive (intuitive) data point: 5,500 units. This was Unitree's global humanoid robot shipment volume in 2025, ranking first worldwide. It sounds like a turning point.

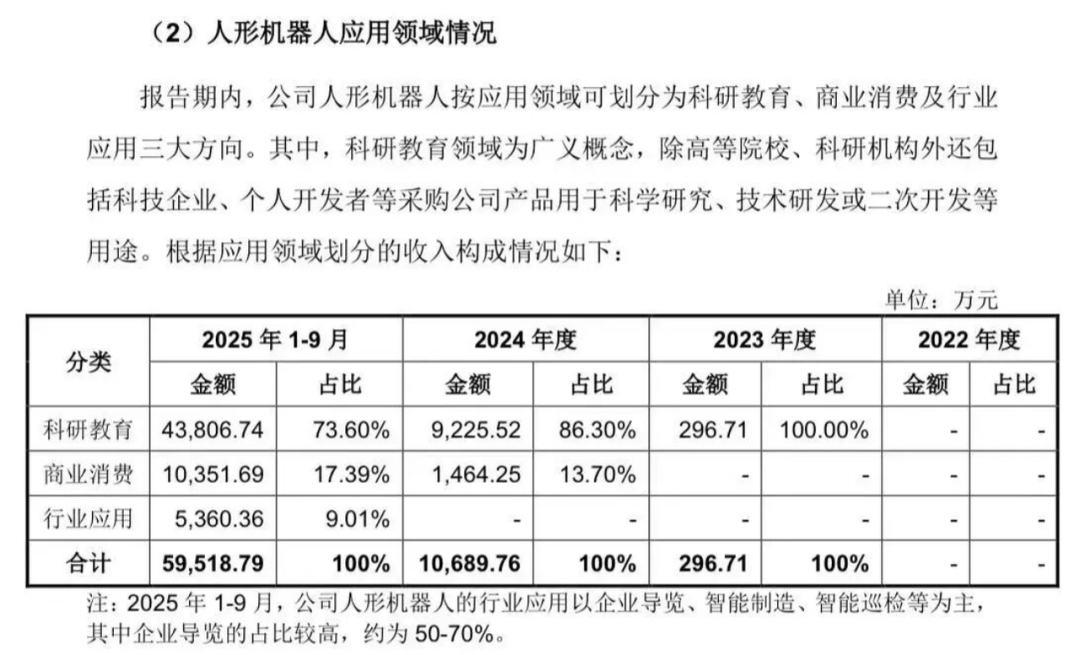

But breaking down the revenue structure reveals a gap. Research and education account for 73.6%; commercial consumption, 17.4%; and industrial applications, 9%.

Digging deeper, over half of 'industrial applications' involve exhibition hall guidance. So where are most of these 5,500 robots? Laboratories, exhibition halls, schools, competition venues, and stages.

The proportion truly entering production lines to replace human labor remains very low. This isn't necessarily bad news, but it must be clarified: stable demand for humanoid robots has not yet formed. The industry is currently more about 'demonstrating capabilities' than 'delivering value.'

You could compare today's humanoid robots to autonomous driving a decade ago—capable of operating, demonstrating, and working in specific scenarios, but still far from large-scale commercialization. The issue lies not with Unitree but with the entire industry.

However, this also exposes a risk: leading in shipments does not equate to a validated business model.

02

4.2 Billion Raised,

85% Invested in 'Unproven Directions'

The second set of numbers involves money. Unitree's IPO plans to raise 4.2 billion yuan, with approximately 85% allocated to R&D—nearly half of which goes to 'models.' It's betting heavily on robots becoming smarter.

Considering gross margins, this choice seems counterintuitive. A company with nearly 60% margins and leading shipment volumes could theoretically invest more in production capacity, distribution, or direct market expansion.

But Unitree isn't doing that. Instead, it's doubling down on an unproven direction. Its current advantages are fragile.

Because the robotics industry's core challenge isn't 'mobility' but 'environmental understanding.' In other words, the 'cerebellum' is sufficient, but the 'brain' is not.

Unitree states bluntly in its prospectus that its self-developed embodied large model has not yet achieved large-scale deployment. The message is clear: robots can perform backflips and dances but cannot yet operate stably in complex environments.

This creates a paradox: while its products have taken center stage, their most critical capabilities remain in development.

This isn't a Unitree-specific issue but a challenge for the entire embodied AI industry. However, when a company allocates 85% of its IPO proceeds to this area, failure could erase its previous advantages.

03

Leading in 'Cerebellum,'

But 'Brain' Determines the Outcome

Unitree's strength is clear: motion control. There's little dispute in the industry about this. Whether quadrupedal or humanoid robots, it excels in dynamic stability, response speed, and complex motion control. Those Spring Festival Gala ensemble routines weren't gimmicks but demonstrations of engineering prowess. However, motion capabilities alone do not constitute a sustainable competitive edge.

History offers parallels. During the feature phone era, Nokia's hardware was unmatched—even industry-leading. Then Apple redefined 'smartphones,' rewriting the competitive logic. Previous advantages didn't disappear but became irrelevant. Humanoid robots now face a similar inflection point. If 'general intelligence' becomes the core, the true barrier will shift from mechanical to cognitive capabilities.

This explains why Unitree is pursuing two parallel paths: WMA (World Models) and VLA (Vision-Language-Action). It's not due to complex strategy but because no one knows which path will succeed.

Industry experimentation is normal, but it introduces a practical issue: all current leadership comes with uncertainty.

Today's frontrunner may not remain tomorrow's, especially as the sector approaches the 'definitional' phase where uncertainties peak.

Summary

Unitree's IPO is virtually assured, with revenue, profits, products, and market attention. The process is moving swiftly, with 'pre-review' mechanisms largely mitigating risks.

The real question is its positioning at listing. This isn't a fully commercialized company but one standing at a technological crossroads. Validated 'cerebellum' capabilities coexist with unanswered 'brain' challenges.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?