Huaqin Financial Report Released: Revenue Exceeds 170 Billion, Profit Grows Nearly 40%

03/24 2026

03/24 2026

451

451

From ODM to a Smart Product Platform: A Breakdown of Huaqin Technology's 2025 Financial Report

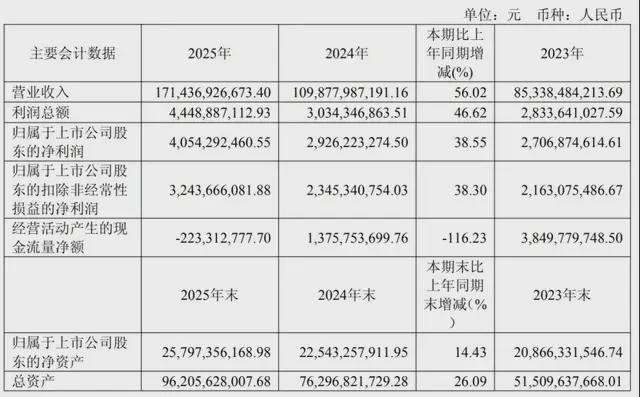

On March 23, Huaqin Technology released its 2025 annual report. Revenue reached 171.437 billion yuan, up 56.02% year-on-year. Net profit hit 4.054 billion yuan, a 38.55% increase.

Amid a moderate recovery in consumer electronics and an explosion in AI computing demand in 2025, Huaqin delivered a standout performance. The company is leveraging its '3+N+3' platform strategy to address an industry question: Where are the boundaries of ODM?

Industrial Signals Behind the Data: Balance as a Moat

While exceeding 170 billion yuan in revenue is impressive, those familiar with electronics manufacturing services know scale isn't the sole metric. The real story lies in the evolving revenue mix.

By 2025, Huaqin's three core businesses—smartphones, personal computers, and data centers—had achieved balanced revenue contributions. During the reporting period, the company maintained its leadership in mobile devices with sustained growth in shipments and revenue across categories. Its PC business saw continuous growth in shipments and revenue, with improved market share and industry ranking. Data center operations experienced rapid revenue growth across all product lines, with expanding market share among major clients. This balance means PCs and data centers act as stabilizers when smartphone markets plateau, while smart devices provide steady cash flow during AI server supply crunches.

Such balance is rare in the ODM sector. Historically, domestic ODM players have specialized in single categories—smartphones, notebooks, or servers. Huaqin, however, chose a 'multi-track' approach, achieving market leadership in nearly every segment.

From an industry perspective, this reflects the reusability of platform-based R&D capabilities. Technological boundaries between consumer, automotive, and industrial electronics are blurring, with transferable core competencies and potential supply chain synergies. Global players like Qualcomm and Xiaomi exemplify this multi-track strategy. Qualcomm leveraged ARM architecture to expand from smartphones to PCs and automotive, launching multiple generations of automotive cockpit platforms. Xiaomi started with smartphones and radiated outward with its 'Smartphone × AIoT' ecosystem, encompassing tablets, notebooks, wearables, smart speakers, and automotive AIoT, all sharing users and scenarios to form a 'human-vehicle-home' ecosystem. With Qualcomm and Xiaomi as precedents, Huaqin's '3+N+3' strategy becomes more comprehensible. The power optimization, refined design, supply chain management, and quality control capabilities honed in smartphone mass production are not product-line-specific but universal engineering experiences. When applied to PCs and automotive electronics, these capabilities offer low marginal costs and high synergistic value.

This is perhaps the true essence of the '3+N+3' strategy—not mere business aggregation but lateral capability transfer and resource integration.

The Second Growth Curve: The 'Substance' and 'Form' of Data Centers and Automotive Electronics

Data Centers: From 'Following' to 'Running Alongside'

Huaqin's data center business was the market's focal point in 2025's AI boom, with computing and data operations generating 75.475 billion yuan in annual revenue. However, focusing solely on growth rates overlooks a more critical shift: product mix upgrades. Early on, Huaqin focused on general-purpose servers and L10-level components, with limited value-add. In 2022, the company pivoted to AI servers, triggering explosive growth. As AI server shipments rose, 2025 saw full-category deployments across major CSPs, followed by high-value products like integrated racks and liquid cooling systems in 2026, steadily improving gross margins.

Huaqin's data center breakthrough validates the ODM model's viability in computing hardware. While the market once viewed servers as custom, low-volume products unsuitable for ODM scale advantages, the standardization of AI servers now plays to Huaqin's strengths.

Super-nodes have surged in popularity, with Huaqin making early strategic layout (Chinese term meaning 'strategic layout ' or 'forward-looking deployment') two years ago. NVIDIA pioneered the concept, and this year's GTC clarified the path for integrated chip-to-system solutions, forging industry consensus: liquid cooling + super-nodes will dominate hyperscale data centers. Key competitive dimensions for super-nodes are now clear: (1) system integration rising, with deep fusion of computing, networking, storage, and liquid cooling; (2) interconnection complexity soaring, with low-latency, high-bandwidth networks becoming cluster efficiency cores; (3) architecture customization for scenarios, with heterogeneous combinations like GPU+LPU adapting to diverse AI workloads. The global landscape is sharply divided—while China has computing hardware foundations, gaps persist in high-speed interconnection, unified architectures, and full-stack collaboration, hindering end-to-end delivery capabilities. Future computing competition will hinge on systemic strengths: full-stack R&D autonomy, continuous technical iteration, deep product optimization, and large-scale engineering delivery.

Huaqin began building super-node capabilities two years ago and is now among the few firms with computing and networking prowess, maintaining leading-edge technologies. Its in-house factories ensure stable delivery efficiency, with advantages in rapid tuning and component sourcing, adding significant value for domestic GPU vendors. Huaqin's super-node products are expected to ramp up production in Q2, scale significantly in H2, and the company is actively developing next-gen super-nodes.

Automotive Electronics: Key Breakthroughs Achieved

In 2025, Huaqin secured critical breakthroughs and scale deliveries across smart cockpits, intelligent driving assistance, body domains, and displays. Focusing on core products like smart cockpits, intelligent driving assistance, body domain controllers, and vehicle displays, the company leveraged its R&D design capabilities and software ecosystem advantages from years of technical deepening to strengthen product competitiveness and innovation. It upheld high-quality delivery and reliability while rapidly responding to diverse customer needs.

Robotics: A Longer-Term Vision

Robotics emerged as Huaqin Technology's key second growth curve starting in 2025.

In robotics, Huaqin completed first-generation debugging of its self-developed bipedal humanoid robot in 2025. While this may seem like a footnote in the financial report, it gains significance in the industrial context: as global tech giants bet on humanoid robots, Huaqin, as an ODM leader, aims not to miss a potential market larger than automotive.

In 2025, Huaqin established an independent subsidiary (Yiren Intelligent Robotics) and built a dedicated R&D team. Current progress spans three scenarios: securing batch shipments for data collection robot projects from leading domestic LLM companies; advancing R&D on wheeled robots for 3C manufacturing, with mass production expected this year; and completing debugging of the first-generation self-developed bipedal humanoid robot, with second-generation planning underway. Technologically, key components like actuators and motion control boards will be self-developed, while integrating NVIDIA's latest Jetson Thor platform to deepen ecosystem synergy.

The 'Gold Content' Driven by Technological R&D

How can ODM firms avoid becoming mere 'contract manufacturers'?

From R&D investment, Huaqin spent 6.38 billion yuan in 2025, up 23.3% YoY. More critical is the R&D organizational shift: publicly, Huaqin has adopted a two-tier system combining 'forward-looking technology research institutes (e.g., X-LAB) + business unit R&D.' X-LAB handles cutting-edge technology reserves, while business units focus on rapid product commercialization.

This structural adjustment reflects Huaqin's redefined self-positioning. During the smartphone era, ODMs excelled at 'rapidly translating customer demands into mass-producible designs.' In the AI and automotive era, where customers often lack clear requirements, ODMs must possess 'product definition' capabilities. Take AIPC as an example—Huaqin's technical accumulate (Chinese term meaning 'accumulation' or 'buildup') in high-performance NPU adaptation, on-device inference optimization, and low-power design enables it to participate in customers' product definition processes, rather than merely executing blueprints.

Standing above 170 billion yuan, Huaqin's challenge is no longer 'can it grow?' but 'how should it be valued?'

If the market still views it as a smartphone ODM, valuations may anchor to consumer electronics cyclicality. But if it recognizes Huaqin as a 'smart product platform enterprise,' valuation logic should align with tech firms capturing multi-sector dividends—a benchmark with no direct precedent.

Indeed, Huaqin is proving its worth through performance. Its balanced business structure, sustained R&D investment, forward-looking strategy, and robust global delivery capabilities collectively underpin its long-term value.

The '3+N+3' strategic framework is in place; execution will determine the rest.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?