Liang Wenfeng’s Top Priority: Navigating DeepSeek’s Strategic Financing

04/21 2026

04/21 2026

506

506

According to a recent report from The Information, DeepSeek is in negotiations to secure external funding, aiming to bolster its resources in the intensifying AI arms race.

The report revealed an intended valuation of at least $10 billion and a financing scale of no less than $300 million.

This valuation appears modest. Zhipu’s latest market capitalization on the Hong Kong Stock Exchange stands at $50 billion, while MiniMax’s is $35 billion. Moonshot AI, after securing $700 million in financing two months ago, also surpassed a $10 billion valuation.

Considering Kimi’s earlier lavish spending on user acquisition and the continued support from venture capitalists, the scarcity of high-quality large model targets becomes evident.

The valuation of AI startups primarily hinges on two aspects: models and products.

At the model level, further division includes two dimensions: the capability to develop a foundational model and the ability to reduce token costs.

Although DeepSeek’s new V4 model has yet to be released, it is reasonable to assume that its model development and cost optimization capabilities are on par with, if not superior to, those of the other three companies.

The valuation contribution from this fundamental aspect should be no less than that of its competitors.

Now, let’s delve into the product level.

Oh, sorry, except for DeepSeek, the other companies have yet to launch notable consumer-facing products.

Therefore, when it comes to the product aspect, DeepSeek is far ahead compared to its competitors in terms of valuation.

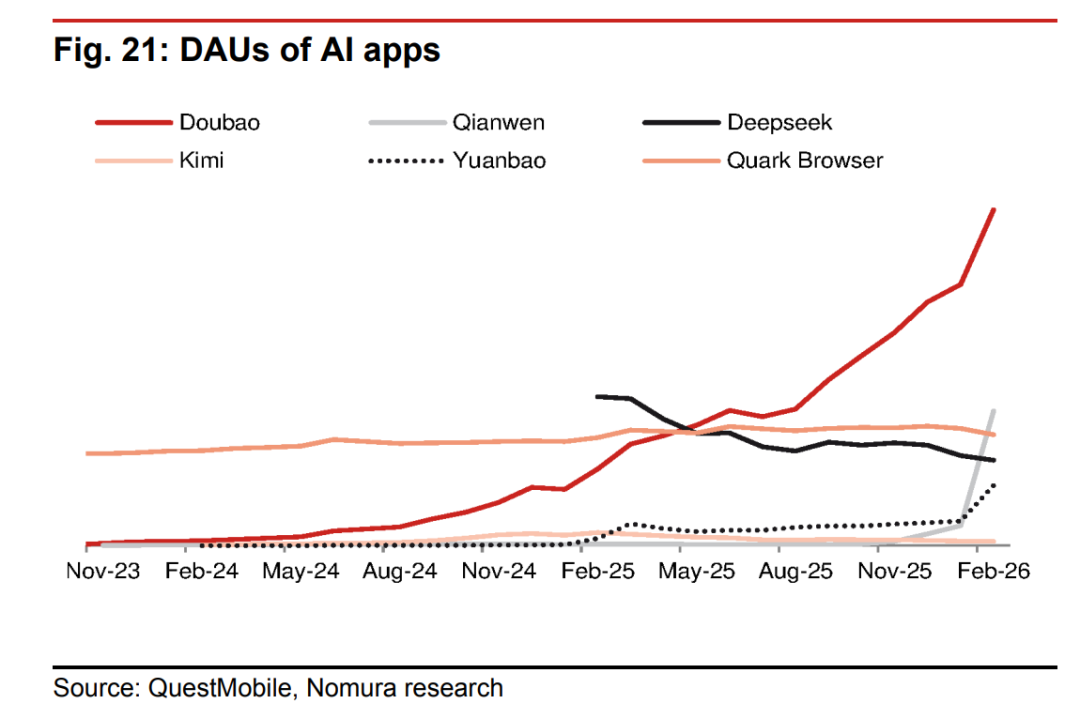

How much is the DeepSeek product worth? According to a QuestMobile report released last month, the domestic AI-native app market exhibits a significant “duopoly” pattern.

As of December 2025, Doubao and DeepSeek ranked first and second with 226 million and 135 million monthly active users, respectively, leading the industry by a wide margin.

Moreover, DeepSeek achieved this feat without any promotional expenses.

One caveat is that QM’s report did not provide the latest data post-Spring Festival.

During the Spring Festival, Alibaba invested heavily in the Qianwen App, disclosing in its financial report that the MAU exceeded 300 million in February. However, this is currently insufficient to challenge the aforementioned “duopoly” judgment.

Given Qianwen App’s relatively low initial MAU and the questionable effectiveness of aggressive user acquisition through subsidies, especially regarding long-term retention rates, which are difficult to improve.

According to a summary from a self-proclaimed expert I encountered, after Qianwen’s Spring Festival hosting event, the proportion of new users aged 60 and above reached 32%.

This demographic primarily consists of young people using their grandparents’ phones to access the app, and it is unrealistic to expect them to become long-term users.

Authentic and loyal AI users are extremely valuable.

DataEye Research Institute estimates that the marketing campaigns for all AI products, including Yuanbao, Doubao, and Qianwen, before and after the Spring Festival, are expected to cost over $10 billion in total.

Among them, Yuanbao accounts for about $1 billion, Doubao about $1.5 billion to $2 billion, and Qianwen about $6 billion (including the “$3 Billion Free Orders” campaign).

Earlier, Tencent Yuanbao’s aggressive user acquisition efforts spanned almost the entire year of 2025.

AppGrowing estimates that Yuanbao’s user acquisition spending in 2025 reached $15 billion, with $5.763 billion spent in the third quarter alone.

Although these budgets are mainly consumed within Tencent’s ecosystem and do not involve actual cash expenditures, Yuanbao’s occupation of ad inventory is real, as is the potential revenue that could have been generated from this ad inventory.

However, despite Tencent’s significant investments, the user base it acquired is very limited.

Before the Spring Festival’s pulsed marketing push, Yuanbao’s DAU was far lower than DeepSeek’s. After the pulsed marketing push, Yuanbao’s DAU remained significantly lower than DeepSeek’s.

Therefore, when compared, DeepSeek’s “angel round” financing, starting at $10 billion, offers better value for money than Pinduoduo.

Major companies have spent heavily and learned a valuable lesson.

The user mindset for consumer-facing AI products cannot be simply bought with money.

You can lure someone in with subsidies, but you cannot make them think your product is good with subsidies alone.

DeepSeek has not spent a dime on promotion and has 135 million monthly active users, securely sitting in second place. Under normal circumstances, if you were an investor, you would not think this valuation starting at $10 billion is expensive; you would think it is too cheap.

Therefore, the core issue of this financing is not whether DeepSeek is worth $10 billion, but why it is only asking for $10 billion.

Liang Wenfeng is backed by High-Flyer Quantitative, which has always been considered well-funded.

Since its establishment, DeepSeek has relied on High-Flyer’s own funds and has never taken a penny from external sources.

This time, breaking with tradition to introduce external capital, according to The Information’s source, is for talent.

The competition for AI talent has become fierce.

Talent needs two things: first, cash for the present, and second, shares and options for the future.

Cash addresses immediate certainty, while shares and options address imagination about the future.

High-Flyer’s money can pay salaries, but High-Flyer’s shares cannot be used to dangle carrots in front of DeepSeek’s employees.

External financing achieves both goals: the raised money is used to pay competitive salaries, while the valuation established by the financing becomes the anchor for the value of options.

A valuation of $10 billion means that the options in your hands are priced based on a $10 billion market cap. This figure is crucial for recruiting and retaining talent.

ByteDance serves as a reference.

On April 16, Beijing time, ByteDance sent out an internal email announcing the first repurchase of “Doubao shares” at a price of $13.08, 30% higher than the previous grant price of $10.

ByteDance confirmed the value of the options in employees’ hands through a tangible repurchase.

According to LatePost, Luo Fuli, a core contributor to the DeepSeek V3 model, has joined Xiaomi to lead its newly established AI department.

Another core researcher, Guo Daya, who previously participated in model development, also jumped ship to ByteDance at a salary level far higher than before.

Since the core objective of the financing is to motivate the team and retain talent, logically, the valuation should be negotiated as high as possible.

The higher the valuation, the more valuable the same proportion of options become, and the stronger the attraction to talent. If you raise the same $300 million, you only need to cede 3% at a $10 billion valuation, whereas at a $20 billion valuation, you only need to cede 1.5%.

The latter is much better for both the founder’s control and the space for subsequent financing rounds.

So why is the actual valuation so “cheap”?

Financial and Non-Financial Logic

One factor is that this financing is not purely a financial transaction.

The new incoming shareholders provide not just funds but also strategic resources in other dimensions.

If so, the $10 billion valuation can be understood as a “base valuation.” The true consideration includes things other than money, but those things are not reflected in the valuation figure. In other words, the implicit participation threshold would be much higher.

However, there is also another factor: the capital market is indeed pricing DeepSeek based on purely financial return logic.

And when you examine DeepSeek with this logic, you find an awkward truth: this company is simply not worth much according to conventional logic.

It’s not that the model is not worth much, nor that the users are not worth much, but that Liang Wenfeng, to some extent, does not intend to turn these things into money at all.

Liang Wenfeng has a very stubborn AGI ideal.

He hopes that DeepSeek will focus on longer-term foundational research goals and has therefore been striving to maintain the company’s independence as much as possible.

DeepSeek is called “DeepSeek” (Deep Seeking) in Chinese, and the full company name is “Hangzhou Deep Seek Artificial Intelligence Foundational Technology Research Co., Ltd.” Please note the key phrase in the name: foundational technology research. Not “technology,” not “intelligence,” but “foundational technology research.”

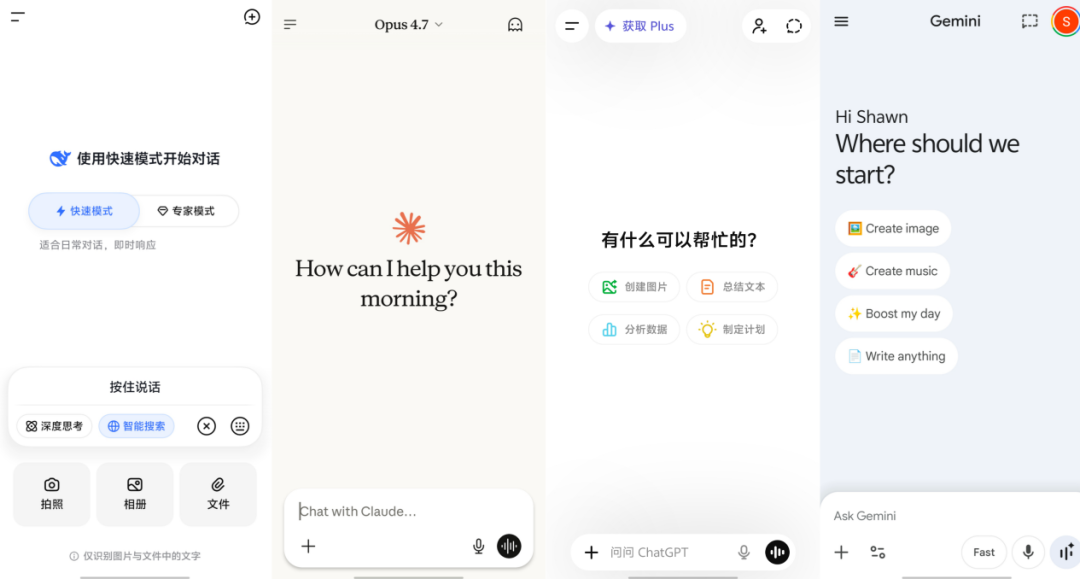

What best reflects Liang Wenfeng’s attitude is the DeepSeek App.

The DeepSeek interface is very simple, not only simpler than domestic counterparts like Doubao and Qianwen but also simpler than foreign counterparts like ChatGPT and Gemini.

The default interface lacks user prompts for writing, creating images, generating PPTs, etc., nor does it offer features like in-depth research, real-time dialogue, or personality customization.

Even today, it still does not support multimodality; uploaded images and files only have their text recognized.

Moreover, the upload process completely disregards the issue of user churn. For example, after selecting an image, you must go through three steps—upload, wait, and extract—before you can send the image.

Google previously conducted research showing that if a mobile page takes more than 3 seconds to load, 53% of users will leave directly.

Both Qianwen and Doubao allow direct image sending, and while you wait, they provide a sense of progress and control by showing “how much data has been found in the search.”

Both also directly display album photos below the input box, making it much more convenient.

Of course, this sacrifices some privacy, but that is not the focus here. The point is that Doubao and Qianwen have spent more time polishing their products.

Another detail is that even if you completely exit the app, when you reopen it, Doubao and Qianwen will continue the previous conversation, which aligns better with general user usage scenarios.

Because general users’ questions within a period are usually related, and a reasonable design is that you should not make them feel the need to manage or segment the context; they neither can nor need to.

There may be some practical considerations behind DeepSeek’s choices.

For example, by keeping the frontend restrained, precious GPU resources can be saved and fully invested in model development.

This logic makes sense, but it can only explain part of the story.

My personal impression is that Liang Wenfeng is not just avoiding promotion; he gives me the feeling that he is not particularly eager for users to use this product.

Because even if GPU resources are extremely scarce and computing power is the biggest bottleneck, this does not affect making the product experience better.

Interaction design, feature polishing, and user guidance do not consume GPUs.

It’s understandable that Nvidia’s Blackwell is unavailable, but fresh graduates for product development are easy to recruit.

The root of DeepSeek’s valuation paradox is that it possesses a consumer-facing entry point that major companies cannot replicate even with billions of dollars, yet it is almost indifferent to the commercial value of this entry point.

It has 135 million monthly active users but lacks even basic product polishing.

If you were a VC, what you see is a gold mine with someone sitting on it who doesn’t want to mine.

When valuing this gold mine, you fear that he will never mine if you value it too high, but you also feel guilty for undervaluing its reserves if you value it too low.

The starting valuation of $10 billion is probably a compromise born out of this ambivalence.

Major companies are now competing for consumer-facing AI entry points at any cost.

Since DeepSeek already possesses a user-validated entry point, it should take the commercial value of this entry point seriously.

By operating this product with normal business logic and a normal VC framework, I believe DeepSeek can achieve a far more respectable valuation than $10 billion.

And now might be a good time.

DeepSeek V4 is rumored to be released soon. If the new model is equally comparable to closed-source SOTA, I suggest not handing over the opportunity and heat to Yuanbao or others as last year.

It is said that Huawei and domestic computing power hardware were used this time.

If DeepSeek can truly run a model service supported by domestic computing power, it means that the issue of consumer-facing products squeezing research and development computing power will also be significantly alleviated.

At that point, only one question remains for DeepSeek: Is Liang Wenfeng willing to turn this gold mine into a business?

-

![]()

More Car Models, Quicker Demise? Global Automakers Are Abandoning the 'Car Sea' Tactics", "Automakers, Model Streamlining, Profit Pressure, Universal Platform, Brand Management", "Global automakers ar

-

![]()

Model AB Price Reduction Controversy: Is Ninebot Losing Its Friendly Touch?

-

![]()

Computing Power Supplier Bags Orders Worth Over 600 Million Yuan, Yet Receives Only 4.5 Million Yuan in Actual Payments!

-

Alibaba Is Just Five Months Away from Securing Two Consecutive AI Coding Titles

-

![]()

Less Investment Isn't Apple's Get-Out-of-Jail-Free Card

-

![]()

The 'King of Africa' Tecno Mobile: What Is the Market Hesitating About After Its 'V-shaped' Rebound?

-

![]()

ByteDance Restructures Feishu, What Signals Does It Send?

-

![]()

ByteDance Overhauls Feishu: What Strategic Signals Are Being Sent?