Huawei's Entry Reshuffles the AI Smart Glasses Market

04/23 2026

04/23 2026

539

539

Amidst the hype and harsh realities, Huawei's entry and the strategic moves of major players have propelled the smart glasses market into a high-stakes competition for survival.

Content/Sophisticated

Edited by/Goose Chant

Proofread by/Rustic

The fierce competition in AI smart glasses has just seen a new contender: Huawei.

On April 20, Huawei unveiled its first HarmonyOS AI smart glasses, featuring a 12-megapixel ultra-light-sensitive camera, 0.7-second AI quick capture, built-in Xiao Yi AI assistant, and support for Alipay payment with a glance, priced starting at 2,499 yuan. While not revolutionary, their launch signifies the entry of another major player with strong branding, distribution channels, and ecosystem capabilities into the smart glasses arena.

This adds further pressure to vertical hardware manufacturers like XREAL and Rokid, already engaged in a protracted "Battle of a Hundred Glasses."

Previously, the smart glasses market had already been experiencing a strange dichotomy of hype and cool-headed assessment. On one hand, the unexpected global success of Meta's collaboration with Ray-Ban fueled illusions of a hardware revival. On the other, major players like ByteDance and vivo, after calm (jìnglěng, meaning "calmly") assessing their return on investment, chose to hit the pause button.

The divergent strategies of these giants reflect underlying industry anxieties, as smart glasses have yet to experience their "iPhone moment." The current market is characterized by a coexistence of conceptual hype and commercial pragmatism, far from reaching a decisive turning point.

However, a consensus has solidified: the barriers to entry have risen, and the potential rewards have become more diluted. As communication giants like Huawei and Xiaomi shift the competitive focus from mere optical modules to underlying system ecosystems and offline channel expansion, the industry's tolerance for error has sharply decreased.

For small and medium-sized manufacturers attempting to thrive during this period of trial and error by major players, the logic of relying solely on supply chain assembly for volume and profit is no longer viable. In this new phase of life-or-death competition, finding an irreplaceable survival model that avoids direct confrontation with major players has become a more urgent imperative than simply iterating hardware specifications.

Part.1

Calculations of Giants and Anxieties of Grassroots Players

The Hidden 1.0 War Masked by the Gateway Narrative

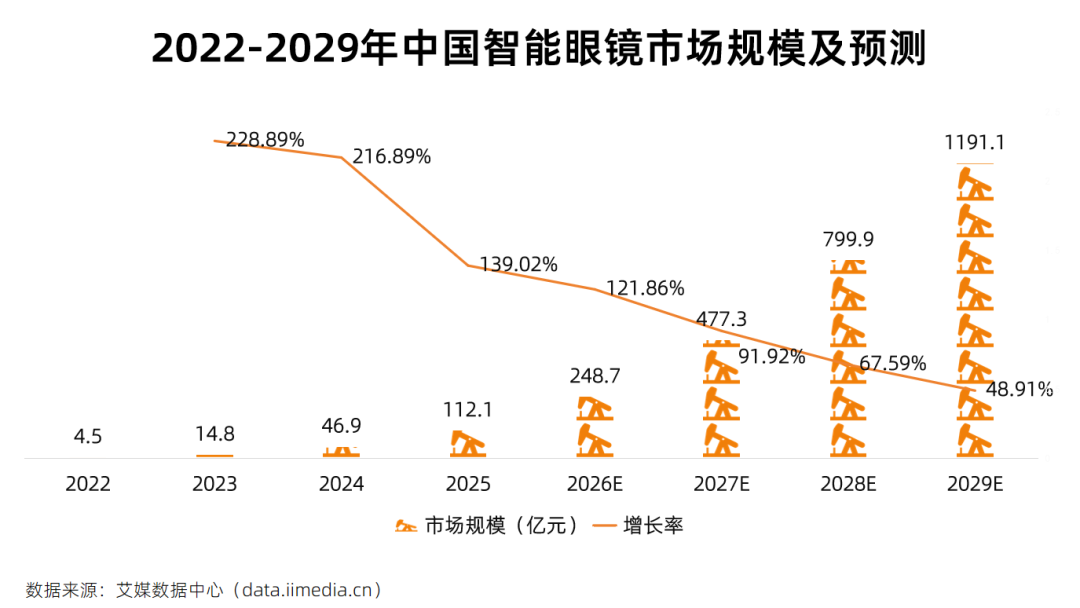

Despite iResearch's optimistic projection of the smart glasses market size approaching 120 billion yuan by 2029, a closer look at the market's commercial dynamics reveals that the so-called "Battle of a Hundred Glasses" is actually a gathering of players with vastly different objectives, all playing different games at the same table.

Currently, three main forces dominate the table:

1. Communication giants like Huawei and Xiaomi, with mature supply chains, extensive retail networks, and strong brand influence;

2. Cross-industry players such as Alibaba, Baidu, and even NIO, entering with capital and large-scale AI model technologies;

3. Vertical hardware manufacturers like Thunderbird Innovation, Rokid, and XREAL, who seized the window of opportunity when giants were still hesitant, achieving breakthroughs in niche markets through extreme single-point innovations.

The clustering of these players is often interpreted as a race to secure the next generation of human-computer interaction gateways. However, in the eyes of seasoned consumer electronics industry insiders, "gateway" is often just a narrative facade. The true calculations of the giants extend far beyond merely selling hardware.

In this 1.0 phase of bounded competition, when giants create smart glasses, they multiply their core business strengths.

Smart glasses are not isolated profit tools but carriers that support and feed back into their core businesses. Alibaba's e-commerce and local life ecosystems, Huawei's HarmonyOS "human-vehicle-home" full-scene strategy all require a physical touchpoint constantly attached to users' noses.

More pragmatically, for giants equipped with AI models like Baidu's ERNIE or Alibaba's Tongyi Qianwen, glasses represent the best testbed for acquiring first-person multimodal data and validating AI large model deployment capabilities.

However, for vertical players, manufacturing glasses is a life-or-death struggle with single-choice questions: shipment volume and profit margins are their sole indicators of survival.

This creates a stark dichotomy within the market. Aggressive giants spare no expense in resources to break into the track (sàidào, meaning "market segment"), while anxious vertical manufacturers face cash flow black holes from heavy R&D investments. Iterating optical modules and developing high-end molds all burn money relentlessly.

Take XREAL as an example: despite its leading position, it has accumulated losses exceeding 2 billion yuan over three years. When giants launch ecosystem-driven attacks, small and medium-sized players must resort to storytelling to capital markets and seeking IPOs for survival funding, becoming their essential options to weather industry cycles.

On the other side of the market lies extreme pragmatism. Previously, major players like ByteDance and vivo, based on commercial calculations, successively suspended their related projects. When products cannot form absolute experiential differentiation and easily fall into spec and price wars, cutting losses and focusing on AI software ecosystems or core smartphone businesses represents a rational strategic contraction.

This chaotic mix of players sprinting, retreating, and holding firm is directly reflected in the currently misleading market share rankings.

If we consider "AI glasses" as the statistical category, Omdia data shows Meta as the global leader, followed by domestic manufacturers Rokid and Xiaomi. Switching to the "AR glasses" category, XREAL claims in its prospectus to be the global leader for four consecutive years, with Thunderbird Innovation and other domestic "AR Four Dragons" also ranking highly. However, according to IDC's broad definition of "smart glasses," Meta alone captures 75.7% of the market, followed by Xiaomi, Thunderbird, XREAL, and Viture.

These conflicting data points under different statistical definitions precisely highlight the industry's pain point. Before the market establishes a unified aesthetic standard and usage habit, akin to smartphones or TWS earbuds, there will be no absolute winner in the Battle of a Hundred Glasses.

The current hype merely represents giants defining standards while small and medium-sized manufacturers desperately prove their existence value. Who can endure this prolonged hidden war without an "iPhone moment" remains an open question.

Part.2

Entering the Life-or-Death Competition Phase

The Three-Dimensional Meat Grinder of Products, Ecosystems, and Offline Channels

As the stakes on the gaming table rise, the smart glasses market has completely bid farewell to the era of relying on single selling points for attention, sliding into a life-or-death competition phase with extremely low tolerance for error.

The core of this competition is ruthlessly condensed into three dimensions: high-frequency product iteration, ecosystem barrier construction, and heavy investment in offline channel expansion.

First comes the reemergence of the product supply-side "flood tactics."

Today's smart glasses market increasingly resembles smartphones years ago or new energy vehicles now. Whoever can launch frequent saturation attacks can forcibly occupy user mindshare.

From public movements, overseas giants like Meta, Google, and Apple all have new hardware launch plans this year. Domestically, besides Huawei's major entry, players like Baichuan Qianwen, XREAL, Thunderbird Innovation, Xiaodu, and Rokid have all flexed their muscles at the 2026 Shanghai Home Appliances Expo.

In this war of attrition (xiāohào zhàn, meaning "war of attrition") of competing on supply chain responsiveness and R&D capacity, vertical dark horses like Rokid have demonstrated strong resilience, but signs of fatigue and cost pressures are quietly accumulating.

If product iteration tests physical stamina, then breaking through ecosystem bottlenecks directly exposes the genetic divides between different player types.

In ecosystem construction, capabilities have become extremely differentiated among players.

Internet giants like Alibaba and ByteDance rely on soft service closures based on e-commerce, local life, mapping, navigation, and payments. Communication giants like Huawei and Xiaomi wield underlying operating systems and interconnected "human-vehicle-home" full-scene hardware matrices as their killer weapons.

In contrast, vertical hardware manufacturers like XREAL face fatal shortcomings—they lack inherent ecosystem genes. Their so-called ecosystems often exist only by compromising and integrating with open APIs from major players, such as for mapping and large models.

From a long-term business perspective, lacking an ecosystem means losing secondary monetization capabilities like traffic distribution and content commission, creating an insurmountable moat for vertical players.

However, when the battle extends to offline retail, the situation presents another paradoxical balance.

Smart glasses are not just 3C digital products but wearable devices with optometric properties. Fitting trials, facial shape adaptation, and wearing experience all necessitate heavy reliance on offline channels.

In this special battlefield, giants' advantages have not fully materialized. Huawei and Xiaomi, despite having hundreds of thousands of stores, primarily focus on smartphones and cars, currently lacking professional optometric zones and refraction capabilities. Alibaba has no offline presence, while NIO's automotive store atmosphere clashes naturally with glasses retailing.

This paradoxically forces vertical manufacturers to explore entirely different survival strategies offline.

Some choose brute force, like Rokid setting a 2028 sales target of 10 million units and rapidly achieving nationwide offline coverage across 34 provincial-level administrative regions with high execution. Others choose leveraged approaches, like Thunderbird Innovation realizing TCL's home appliance channels cannot be directly reused, instead partnering with the three major carriers to force open lower-tier markets (xiàchén shìchǎng, meaning "lower-tier markets") through phone recharge-bundled glasses and cloud service packages. Players like Meizu, lacking traditional offline store foundations, have no choice but to retreat online, be caught in (xiànrù, meaning "falling into") the red ocean of traffic purchasing.

Cyclical patterns don't lie. When smart glasses become a core window of opportunity (fēngkǒu, meaning "market trend") that tech giants cannot afford to lose, their systematic investments will rapidly level the hardware playing field.

In this red ocean game, the living space (shēngcún kōngjiān, meaning "survival space") of small and medium-sized manufacturers is being squeezed from both ecosystem and capital perspectives by giants. The window for their trial and error is rapidly closing.

Part.3

The Low-Barrier Trap and Searching for a "Xiaotiancai"

The Final Breakthrough for Small and Medium-sized Players

Compared to the vast and complex automotive industry, smart glasses are rapidly becoming a low-barrier market segment. This is not derogatory but an inevitable byproduct of the consumer electronics supply chain's high maturity and rapid industry standardization.

As modules, chips, and lenses become standardized, even automakers like NIO can easily cross over into the field, stripping away early players' blue ocean advantages at an accelerating pace.

This industrial chain spillover effect represents a dangerous trap for small and medium-sized manufacturers, plunging competition directly into a homogeneous red ocean and dramatically raising the implicit costs of staying in the game.

At this stage, the competition's core has shifted—it's no longer about purely comparing hardware product strength but about who can first establish a viable business model for survival.

Just as the new energy vehicle sector spawned Huawei's HI mode and self-developed factions, while the learning tablet market differentiated into pedagogical and hardware factions, the children's wearables field even produced Xiaotiancai, which built absolute barriers through a closed social network.

For smart glasses' small and medium-sized manufacturers trapped between giants, constructing their own "Xiaotiancai model" in niche scenarios before complete giant domination represents a life-or-death imperative.

Objectively speaking, tactical breakthrough attempts have already emerged within the industry. For example, Rokid's collaboration with traditional eyewear giant BOLON signifies the industry's entry into a co-definition era, where tech firms provide algorithms and modules while traditional optics players contribute channels and branding. However, this remains merely transitional.

In the eyes of seasoned consumer electronics operators, the current core task remains scaling up ST (shipments from manufacturers) and SO (retail activations) to amortize high optical and sensor costs.

But from a terminal perspective, meager hardware profits are not the endpoint. Once AI glasses truly become constant visual and voice super-nodes on human faces, first-person navigation, food delivery, payments, and ad distribution will follow.

At that point, the true moats and profit pools will inevitably belong to those controlling traffic distribution and transaction commissions—precisely what vertical players most lack.

So, besides directly confronting the ToC consumer market, do small and medium-sized manufacturers have retreat paths? Avoiding giants' saturation attacks and sinking into the B2B market might offer an outlet.

Vertical scenarios like industrial manufacturing, smart logistics, and precision healthcare place extremely high demands on device customization and adaptability. Although fraught with non-standard integration challenges, these fields can provide long-term survival security through customer stickiness and high unit prices.

Looking at today's smart glasses market, clashes between old and new forces are at a cyclical point of chaos. Giants' sudden surges and decisive retreats all signal impending industry reshuffling.

How this "Battle of a Hundred Glasses" will ultimately conclude remains an open box today.

But business history repeatedly proves that in a Dividend track (hónglì sàidào, meaning "profit-rich market segment") paved with both gold and thorns, the survivors are often not those with the most dazzling specifications but those who first discern the commercial essence and build moats.

END

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?