Big Tech Companies Throw Their Weight Behind Robots

04/24 2026

04/24 2026

606

606

Source | Bohu Finance (bohuFN)

Author | Kaikai

The excitement from the Spring Festival Gala hasn't died down yet, and the Beijing Yizhuang Humanoid Robot Half Marathon has catapulted robotics to new heights of public interest. This time, it's not just robotics unicorn companies making waves—tech behemoths are also jumping in with both feet.

The Glory humanoid robot 'Lightning' clinched the robot group championship in just 50 minutes and 26 seconds, nearly 7 minutes faster than the world record for the men's half marathon. Alibaba's Gaode showcased a quadrupedal robot 'Tutu,' adept at autonomously guiding visually impaired individuals through dynamic and static obstacle avoidance, narrow passages, and other urban road-level challenges.

Internet giants have long been the powerhouses in the robotics industry. Since 2014, companies like Alibaba, Baidu, Xiaomi, Meituan, and Tencent have frequently shown their commitment by investing in robotics-related enterprises, with 62 investments made in 2025 alone.

However, as the robotics industry matures, these tech titans are no longer content with just being investors—they're stepping into the limelight. This transition from behind-the-scenes financiers to frontline players signals that robotics has shifted from 'concept validation' to 'real-world application.' The competition now revolves not just around technological prowess but also securing a prime position in the future commercial robotics landscape.

Since last year, the field of embodied AI has seen a surge in investment.

According to the Embodied AI Development Report (2025), by the end of 2025, China witnessed 744 investment events in the embodied AI and robotics sectors, with a total financing volume reaching RMB 73.543 billion.

Internet and tech giants are undoubtedly the driving forces behind this boom. According to IT Juzhen's 2025 CVC Investment Landscape Analysis in the Embodied AI Sector, eight key big tech firms made a combined 62 investments throughout the year, with total amounts ranging from RMB 1.45 billion to 3.4 billion.

Yet, the strategic investments in robotics by big tech firms began even earlier. Since 2014, companies like Alibaba, Baidu, Xiaomi, Meituan, and Tencent have been highly active in the robotics sector.

According to 'New Strategy Embodied AI,' Meituan leads in the number of companies invested in, with over 20, followed by Alibaba (17+), Tencent (15+), ByteDance (10+), JD.com, and Baidu, each investing in 6+ enterprises.

Beyond internet giants, smartphone manufacturers and new energy vehicle companies have also emerged as significant players.

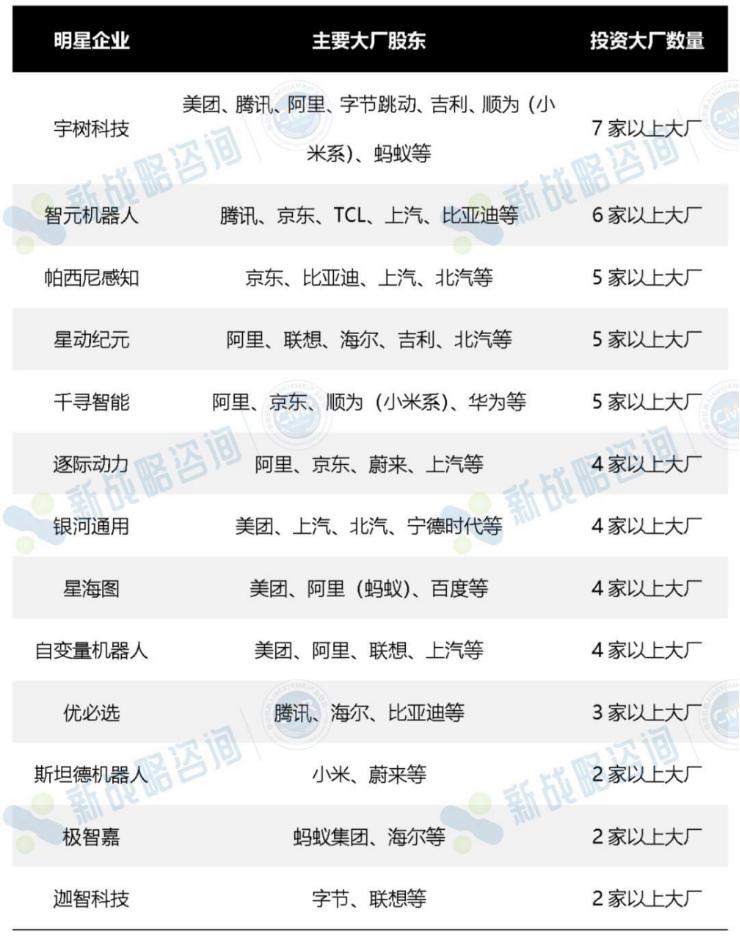

Xiaomi and Lenovo have each invested in 18+ enterprises, SAIC Motor in 7+, and NIO and BYD in 4+ each. The fierce competition among these big players has left star robotics companies with a crowded roster of major backers.

For instance, Autovariable Robotics, which secured nearly RMB 2 billion in Series B funding in April this year, is backed by Alibaba, ByteDance, Meituan, and Xiaomi. The celebrity unicorn Unitree Robotics boasts over seven major backers.

Why are these big tech firms so 'aggressive'? The answer is straightforward: it's better to over-invest than to miss out.

In the early days, the technological path for robots was uncertain. No one knew if bipedal designs were the way to go or whether the 'brain' of embodied AI should reside in the cloud or on the device itself. Faced with high R&D costs and long validation cycles, the industry was rife with uncertainty.

For cross-border entrants like these big tech firms, the safest strategy was a 'horse race' mechanism—concentrating resources on leading robotics companies to secure a 'ticket' to the future of robotics.

But this differs sharply from past internet investment logic.

Traditionally, beyond early-stage investments, few overlapping big tech firms would back the same star application, as each had its own ecological niche. Once a firm heavily invested or strategically acquired a company, it would integrate it into its own ecosystem, providing traffic and resource support, leading the investee to align accordingly.

However, as competition among big tech firms shifts from the digital to the physical world, this rule has quietly been broken—not because they’ve stopped competing, but because they’re competing differently.

In the real world, traffic logic alone won't determine success. Robots, as intelligent hardware, cannot survive solely on data and large models. Supply chains, manufacturing capabilities, and real-world adoption scenarios are key to shaping their 'physical form.'

Thus, big tech firms in robotics are no longer 'kings who avoid each other.' Instead, they're bringing their unique 'commercial DNA' to deeply integrate robotics applications into their respective business ecosystems.

With different adoption paths, strategic divergences among big tech firms are inevitable. Even when investing in the same robotics company, they're betting on different commercial futures.

Currently, big tech firms’ robotics investments generally align with their strategic goals, industrial experience, and technological accumulations. With different 'cards' in hand, their learning curves and paths naturally diverge.

Some firms are heading toward clear 'wealth-creation' goals, treating robots as tools to address immediate business needs. JD.com and Meituan exemplify this approach.

JD.com focuses on developing intelligent products for home scenarios and applying embodied AI technologies in supply chain contexts. At last year’s Robotics World Conference, it showcased robot applications in unmanned shelving and logistics.

Meituan emphasizes robotics’ empowerment of retail. Its drones and autonomous vehicles have already completed scenario validations:

Meituan’s drone meal delivery has opened 64 routes, completing over 600,000 orders. Its self-developed autonomous delivery vehicles have begun regular trial operations in some regions.

According to Tianfeng Securities estimates, the total operational cost of a drone over its lifecycle is RMB 84,500, with a monthly cost of around RMB 1,400—75%-90% lower than existing rider wages. If widely adopted, this could save Meituan tens of billions in rider costs.

JD.com and Meituan’s businesses inherently involve extensive interaction with real-world environments, allowing robots to rapidly deploy in specific scenarios without waiting for a 'perfect form,' enabling continuous optimization and iteration through daily use.

These players, driven by 'wealth-creation' motives, can accelerate their business flywheels accordingly.

Another group of firms is striving to 'build dreams.' Starting from their own capabilities, they invest more resources in robotics software and operating systems, constructing the underlying infrastructure for the robotics era. Examples include Alibaba, Baidu, ByteDance, and Tencent.

Their logic is straightforward: while robots remain 'physically advanced but mentally slow,' enabling them to truly understand the world requires a 'brain'—and that’s what they aim to provide.

Alibaba invests in hardware companies like LimX Dynamics and Star Era while opening its QianWen large model to offer full-stack solutions for robot development.

In February this year, Alibaba DAMO Academy open-sourced the embodied AI robot RynnBrain foundational model, outperforming multiple top models across 20 embodied benchmarks.

The recently unveiled Gaode quadrupedal robot 'Tutu' is supported by a complete embodied technology architecture called 'ABot,' including Gaode’s years of accumulated physical world data, two embodied operation foundational models (ABot-NO and ABot-M0), and an Agent operating system layer (ABot-Claw) capable of continuously organizing information, decomposing tasks, and executing them by priority.

Baidu, ByteDance, and Tencent follow similar strategies but with different focuses.

Baidu emphasizes 'technology + ecosystem,' leveraging its Baige GPU computing platform, Wenxin large model, and Baidu Intelligent Cloud to drive robot adoption across scenarios. For example, Baidu Intelligent Cloud has formed a strategic partnership with Zhiyuan Robotics to build a robot development platform for research and education.

ByteDance fully utilizes its algorithmic strengths, introducing the visual-language-action model Seed GR-3. Unlike traditional VLA models reliant on extensive robot trajectory training, GR-3 adapts to new tasks with minimal demonstration data, significantly reducing deployment costs.

Additionally, ByteDance has built interfaces like a general robotics model API and hardware SDK, attempting to foster a developer ecosystem for embodied AI.

Tencent’s strategy leans conservative. Ma Huateng has explicitly stated a desire to partner with all robotics manufacturers rather than replace them by making hardware.

In July last year, Tencent’s RoboticsX Lab released the embodied AI open platform Tairos ('Titan Screw'), the first modular embodied AI software platform in China to provide large models, development tools, and data services, serving as a linking platform between robot 'bodies' and 'brains.'

Notably, besides Tencent, Alibaba, ByteDance, and Baidu have all started building their own robots.

This suggests that 'building brains' is just their starting point. With robotics technology paths still evolving, these big tech firms also hope to stay abreast of technological advancements through hardware-software integration, keeping 'dream-building' uncertainties in their own hands.

The final group of players is heading straight toward 'building humans,' such as cross-border players like XPeng and Xiaomi.

Their supply chain DNA highly overlaps with the robotics industry, making the transition from 'building cars' to 'building humans' a natural progression.

More importantly, these players already possess mass-production capabilities for robots. Investing in robotics companies to acquire technology and future 'factory access' rights also represents a cost-effective financial investment.

It’s clear that in the robotics era, internet giants’ positions are subtly shifting.

While they remain strong in model capabilities and scenario data, they no longer naturally occupy the industry’s center—instead, they must develop synergistically with the entire industrial chain.

From dimensions like capital advantages and algorithmic capabilities, big tech firms still hold significant positions in the robotics industrial chain. By open-sourcing large models, providing simulation training environments, and offering cloud-edge collaboration solutions, they’ve become the 'utilities' of the robotics industry.

This path has a high ceiling but also high uncertainty.

After all, infrastructure can only truly add value when a large number of robots connect and use it. Big tech firms must actively seek partnerships to validate and iterate their platform capabilities in others’ production lines and scenarios.

Meanwhile, robotics unicorns like Unitree, Zhiyuan, and Galaxy General will continue to dominate the robotics industry’s top tier. They’re advancing faster in hardware-software integration and possess unique hardware or software strengths—a moat that’s hard to bridge in the short term.

However, while some firms have achieved commercial closure, selling robots is just the first step. How to make robots move beyond the stage to perform real tasks and expand into more application scenarios remains a common challenge for the entire industry. This requires big tech firms to continuously deepen their efforts in foundational technologies, ecological standards, and commercial scenarios to jointly unlock breakthroughs in large-scale robotics adoption.

Additionally, cross-border players with rich supply chain experience like Xiaomi and XPeng, along with firms specializing in vertical robotics supply chains, will accelerate the localization of core robotics components.

After the Glory 'Lightning' robot won the marathon, the stock prices of its multiple suppliers surged—a clear signal that capital markets now recognize that the robotics industry’s future hinges not just on complete machine manufacturers but also on supply chain maturity.

Thus, rather than trying to dominate industry trends, big tech firms must find their own ecological niche—whether by deeply cultivating a specific vertical scenario, becoming industry infrastructure, or serving as ecological connectors. This is a more pragmatic survival strategy.

Ultimately, the winners in this long race won’t be those who invest in the 'first IPO' or whose robots run the fastest but those who can root themselves deepest in the industrial chain’s cracks and cover the broadest soil.

Different ecological partners need to empower each other to go further together.

The cover image and illustrations belong to their respective copyright holders. If copyright owners believe their works are unsuitable for public browsing or free use, please contact us promptly, and our platform will immediately make corrections.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!