DJI VS Insta360 Two-Way Game: Intense Competition in the Handheld Camera Track, Disruption by Mobile Phone Giants

04/24 2026

04/24 2026

396

396

©New Game

Recently, the DJI Pocket4 sold out immediately after its launch.

On the evening of the product's debut, over 1.1 million people flooded into the official Tmall flagship store. As soon as sales began, all major online channels were completely sold out, and subsequent restocks were quickly snapped up. Long lines formed at offline stores, making the device hard to come by both online and offline.

Image source: Xiaohongshu user @Travel Diary

The market enthusiasm remains high, largely due to DJI's strategy of ultimate cost-effectiveness with the Pocket4. Building on multi-faceted upgrades in product functionality, DJI has priced the standard version of the Pocket4 at 2,999 yuan, with the all-inclusive set at 3,799 yuan, representing reductions of 500 yuan and 700 yuan, respectively, compared to the initial prices of the Pocket3.

Image source: DJI official website

It's important to note that the Pocket series is one of DJI's flagship products, with the Pocket3 having long dominated its segment and helped establish DJI's absolute leadership in the global handheld smart camera market. Following the release of the Pocket3, major mobile phone manufacturers like OPPO and vivo accelerated their entry into the handheld smart camera market.

But times have changed. If the Pocket3's role was to "expand DJI's territory," then, with the company's core drone business growth plateauing and the urgent need to solidify a second growth curve, the Pocket4 now carries a heavier burden. The latter must not only stabilize the market captured by the Pocket3 but also help DJI break through growth anxieties in a more complex competitive environment and hold its own in the new round of positioning battles.

DJI Faces Increasing Passivity Amid 'Internal and External Challenges'

From a corporate development perspective, despite the Pocket4's impressive sales, DJI's current passive situation remains unchanged.

As is widely known, DJI's greatest strength has always been its technology. The company's pillar industry is not the handheld smart cameras (action cameras) represented by the Pocket4 but consumer drones. The industry's mainstream view is that DJI's drone business accounts for over 70% of its revenue.

In its main segment, DJI has gone from entering the drone industry to securing an unshakable position in the consumer drone market by leveraging its absolute advantages in three key areas: flight control systems, gimbal stabilization technology, and image transmission technology. Benefiting from technological dividends, DJI's core drone products have maintained a market share of over 70% in the global consumer drone market for an extended period, driving the company's annual revenue to reach 80-90 billion yuan.

Image source: DJI official website Mini5 Pro

However, every coin has two sides. A significant premise (premise) is that the overall growth of the consumer drone market has gradually plateaued. According to Statista data, the global consumer drone market is expected to reach approximately $4.27 billion in 2025, representing a 7% year-over-year increase, with a projected compound annual growth rate of around 3.4% over the next five years. This means that DJI, which holds a substantial market share, also faces narrower growth prospects.

DJI's adjustments in product positioning also reflect this reality. Based on technological breakthroughs, DJI's initial product positioning for drones was mid-to-high-end and quasi-professional, falling into the category of light luxury products. The company could even extend the update cycle for its flagship products to 3-4 years. However, since the second half of 2024, DJI has accelerated its drone product release rhythm, rapidly covering entry-level, professional, mid-to-high-end, and other segments, while also introducing more segmentation (niche) product lines in various fields. This reflects the overall shift in the consumer drone market from high growth to Stock competition (stock competition).

At the same time, the standardized development of the consumer market and accompanying relevant policies are advancing in tandem.

In January of this year, China's newly revised "Public Security Administration Punishment Law of the People's Republic of China" came into effect, further tightening control over unauthorized drone flights, with compliance requirements increasing at all levels. It is understood that drones weighing under 250 grams and light drones are restricted to flying below 120 meters, while all other models require advance notification one and a half days prior.

This undoubtedly raises the consumption threshold for the mass market to a significant extent.

In overseas markets, DJI's near-monopolistic position in the consumer drone market has also begun to face "obstacles" at the national level. For instance, in the North American market, by the end of 2025, the U.S. FCC had placed DJI and others on a "regulated list," banning the approval of new drone models for import or sale in the United States.

Amid 'internal and external challenges,' DJI has no choice but to explore new growth avenues. Especially after 2025, the company has increasingly focused on multiple segments. According to publicly available information on its official website, in addition to drones, DJI is currently involved in businesses such as handheld smart cameras, outdoor power supplies, and robotic vacuums. In November of last year, DJI also invested in Smart Tech, a consumer-grade 3D printing manufacturer.

Core Territory Under Erosion

Insta360 Begins to Fight Back

However, expanding into more business lines requires time. Currently, aside from drones, DJI's most formidable asset is handheld smart cameras. Yet, venturing into this segment is not without resistance, as Insta360 is undoubtedly its biggest competitor at present.

From an industry development perspective, both DJI and Insta360 can be considered "game-changers" in the handheld smart camera industry. Initially, this industry was dominated by GoPro, which once monopolized the global market at its peak. As latecomers, DJI and Insta360 took entirely different approaches.

DJI entered the market because the technology required for action cameras is closely aligned with that of aerial photography drones. The company's earliest products focused on gimbal stabilization and professional handheld shooting, essentially transferring its aerial photography technological advantages to the ground. In this dimension, DJI truly captured market mindshare in 2023 when its Action4, designed for outdoor sports scenarios, and the Pocket3, focused on daily Vlog recording, both penetrated the market with ultimate cost-effectiveness.

According to LoCTech data, during this year's Spring Festival, after multiple product iterations, the DJI Action4 remained among the top 5 best-selling models in China's traditional action camera online market. By the second half of 2025, cumulative sales of the DJI Pocket3 alone had surpassed 10 million units.

On the other hand, Insta360 chose to enter the more niche segment of 360-degree cameras. At the time, this segment was still a blue ocean, and Insta360 quickly opened up the market due to its leading technological advantages. Its self-developed dual-lens stitching and FlowState stabilization technologies are its core competitive edges.

Image source: Insta360 official website Insta360 X5

Since 2018, Insta360 has even held the top position in the global 360-degree camera market for eight consecutive years. In many users' minds, Insta360 is nearly synonymous with 360-degree cameras. According to financial data, under this strong market mindshare, Insta360's 360-degree camera performance contributes over 55% of its total revenue for an extended period. Data released by Qianzhan Midtai shows that as of Q1 2025, Insta360 still held a 91% share in the global consumer 360-degree camera market.

During this phase, DJI and Insta360 each reigned supreme, together propelling the handheld smart camera market toward a duopoly, while the once-glorious GoPro continued to decline. However, this situation did not last long. As DJI shifted its focus toward the handheld smart camera segment, direct competition between the two began.

In July 2025, Insta360 officially launched its drone brand, "Yingling," directly targeting DJI's core territory. That afternoon, DJI announced it would release a 360-degree camera, striking at Insta360's "lifeline." Soon after, the DJI Osmo360 was released at a price of 2,999 yuan, adhering to a cost-effectiveness strategy and undercutting the comparable Insta360 X5 by 800 yuan.

The low-price strategy yielded immediate results. According to Qianzhan Midtai data, in Q3 2025, the DJI Osmo360 captured 43% of the global market share, while Insta360's market share plummeted from 91% to 49%. However, this data leans more toward the GMV perspective of e-commerce platforms. During its Q3 2025 earnings call, Insta360 also questioned the third-party data, citing another report by Frost & Sullivan, which showed that in the 360-degree camera market, Insta360 still held a 75% global market share in Q3 2025, with DJI at 17.1%.

What is certain is that Insta360's position in the 360-degree camera market is no longer as stable as before. The reason is that, based on its technological first-mover advantage, DJI's strong positioning in the drone market has gradually transformed into supply chain and ecosystem barriers. For example, in addition to its lower price, the DJI Osmo360 benefits from DJI's complete image transmission ecosystem. In contrast, Insta360's foray into the drone market has not been as smooth, but the company has not halted its efforts, and the competition between the two continues.

While Insta360 counters the price war, it is also focusing on marketing, leading to an increase in related public opinion. In December last year, Insta360 founder Liu Jingkang forwarded "The Supply Chain War Between DJI and Insta360" with the caption, "Fight to the end, until death." Entering 2026, the competition between DJI and Insta360 has further extended to products, supply chains, talent, and other areas. Recently, the two companies even faced off in court over patent disputes.

Additionally, in the handheld smart camera market, Insta360 has also launched a "counteroffensive." Less than a week after the DJI Pocket4's release, the Insta360 Luna series of pocket gimbal cameras debuted at the 2026 International Broadcasting Convention in the United States. The Luna is Insta360's first three-axis mechanical gimbal pocket Vlog camera, directly competing with DJI's best-selling Pocket series.

Chaos Looms as More Players Enter the Fray

Of course, the intensifying competition between DJI and Insta360 is not only about consolidating their respective market positions but also due to the growing size of the handheld smart camera market.

According to the latest IDC statistics, in 2025, global shipments of handheld smart cameras reached 16.65 million units, soaring by 83% year-over-year, with sales exceeding 46.1 billion yuan, up 86% year-over-year. IDC projects that by 2030, the global handheld smart camera market could exceed 40 million units, with a five-year compound annual growth rate of nearly 20%.

The expanding market is attracting more players.

As early as 2017, Xiaomi experimented with action cameras but did not expand further. However, in November 2024, Hohem iSteady Tech, a leading domestic gimbal manufacturer, secured investment from Xiaomi, leading to a partnership to jointly develop pocket cameras, also emphasizing cost-effectiveness.

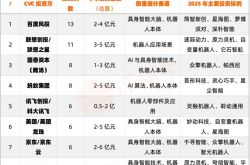

Additionally, in late 2024, vivo announced that it had initiated projects related to handheld gimbal cameras. A year later, OPPO also launched similar product development, with the project led by its core Find product planning department and personally overseen by OPPO Senior Vice President Liu Zuohu. The product is positioned to compete with handheld smart imaging devices from brands like DJI and GoPro and is expected to be officially released in 2026.

At the 2026 Mobile World Congress in Barcelona, the Honor Robot Phone made its debut. This product integrates mechanical motion, an AI brain, and professional imaging into one, featuring embodied AI technology applications, a robotic arm gimbal, support for 90°/180° intelligent camera movement, Super Steady stabilization, and single-handed filming of cinematic-quality Vlogs—functions highly similar to those of current handheld smart cameras.

It is worth noting that the entry of leading domestic mobile phone manufacturers into this market is not entirely a crossover. These companies have long-standing technological accumulations in sensors, imaging algorithms, video stabilization, and low-light shooting, coupled with advantages in hardware, supply chains, and product ecosystems. The entry of these mobile phone giants will undoubtedly pose a threat to established players like DJI and Insta360.

Now, with DJI launching the Pocket4 and proactively initiating a price war based on its existing product performance and market advantages, the goal is to raise the entry barrier for more players and gain an edge in the new round of positioning battles. This also corroborate from a different angle (indirectly confirms) DJI's anxieties, which are shared by Insta360, as both are under attack from multiple fronts. The reason is that, with more players entering the market, the handheld smart camera segment is facing an even more complex competitive environment, and neither DJI, mired in growth anxieties, nor Insta360, having lost its core territory, has any room for retreat.

-

![]()

The ‘White Glove’ Phenomenon at Auto Shows: Far from Over This Year

-

![]()

DeepSeek Strikes Again, Domestic Large Models Can't Sit Still

-

![]()

DeepSeek V4 Is Finally Here! What Do We Know?

-

![]()

DJI VS Insta360 Two-Way Game: Intense Competition in the Handheld Camera Track, Disruption by Mobile Phone Giants

-

![]()

From iQIYI to AIQIYI: A 'Cost-Reducing Marvel' or a 'Crisis of Trust'?

-

![]()

Big Tech Companies Throw Their Weight Behind Robots

-

![]()

Apple’s New CEO: The Perfect Blend of ‘Jobs + Cook’

-

![]()

Behind Oracle's Global Layoff of 30,000: AI Bubble or AI Replacement?