Reddit: Reaping the Rewards of Accelerated Commercialization

05/07 2026

05/07 2026

445

445

Reddit delivered a solid Q1 performance. On one hand, as a key data source for AI, Reddit—with its strong sense of 'human presence'—is enjoying referral traffic from entry points like Google. On the other hand, Reddit is still in the early stages of commercialization and is advancing its monetization of performance advertising beyond brand ads.

The shift from Search ('people finding content') to Feed ('content finding people') will be a new driver of growth for the company. Additionally, the platform's ad load rate remains relatively low compared to peers, suggesting a period of attractive performance growth ahead. However, profit margins may see a gradual slowdown in improvement due to increased investment in feature development.

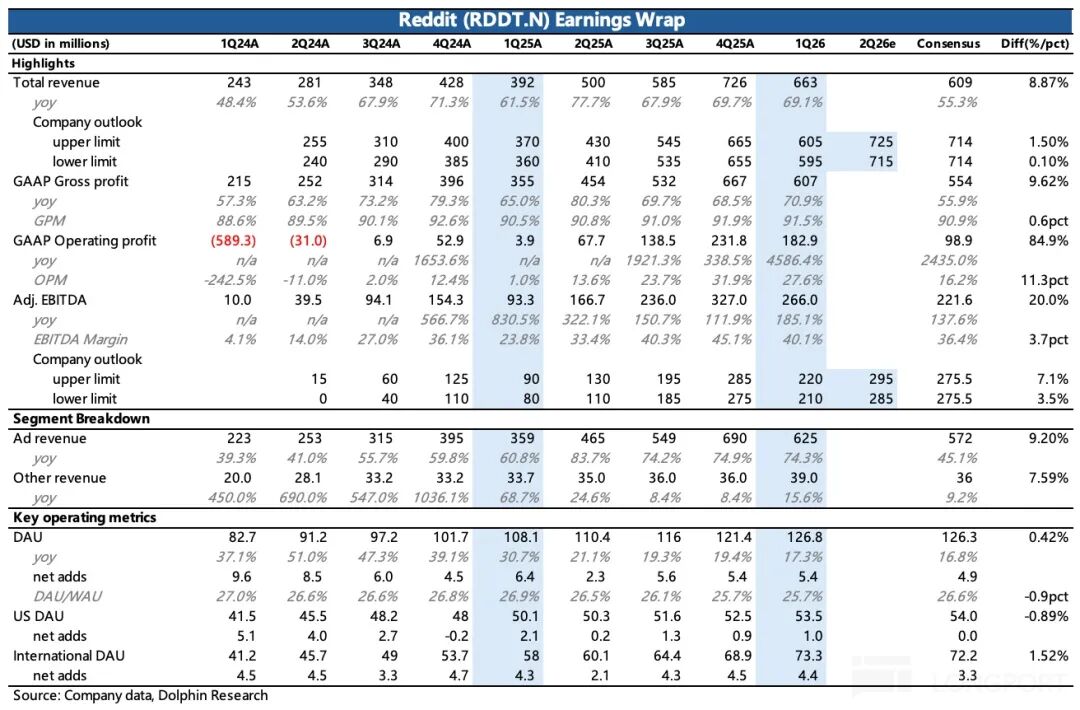

Prior to the earnings release, market adjustments were made to Reddit's growth expectations based on Cleveland Research, which indicated that 'due to macroeconomic fluctuations, advertisers have been cutting brand ad budgets since late March, shifting to top-tier platforms with higher ROI.' This contributed to recent downward pressure on Reddit's stock price and a correction of its high valuation. Therefore, a solid Q1 performance without signs of slowing growth can effectively alleviate market concerns.

However, the earnings report was not without flaws. One issue is the persistent slow growth of U.S. users, while the other is the Q2 revenue guidance, which implies a deceleration in growth from Q1's 69% to 45%. This may indirectly confirm the insights from the aforementioned industry research. However, management has a history of conservative guidance, and the Q2 rollout of Reddit Max, an automated ad tool (launched in beta in January and already used by thousands of advertisers), is expected to drive continued growth above guidance.

Starting in Q3 this year, Reddit will no longer separately report logged-in and non-logged-in users because management believes that 'while logged-in users certainly see more ads due to longer session durations, there is not much difference between logged-in and non-logged-in users from a commercialization perspective.'

However, Dolphin Research believes there is a clear distinction based on whether users log in. Management's view that commercialization is similar may stem from the early focus on brand advertising. As performance advertising expands, logged-in users' personalized data and profiles will be richer than those of non-logged-in users, facilitating personalized ad distribution, improving conversion rates, and enhancing commercial value.

Therefore, the subsequent growth performance of U.S. users (tracked through high-frequency app data) will also influence investor confidence and sentiment toward Reddit. A more detailed value analysis has been published in the same name article under the 'Insights - Deep Dive' section of the Changqiao App.

Below are the detailed charts:

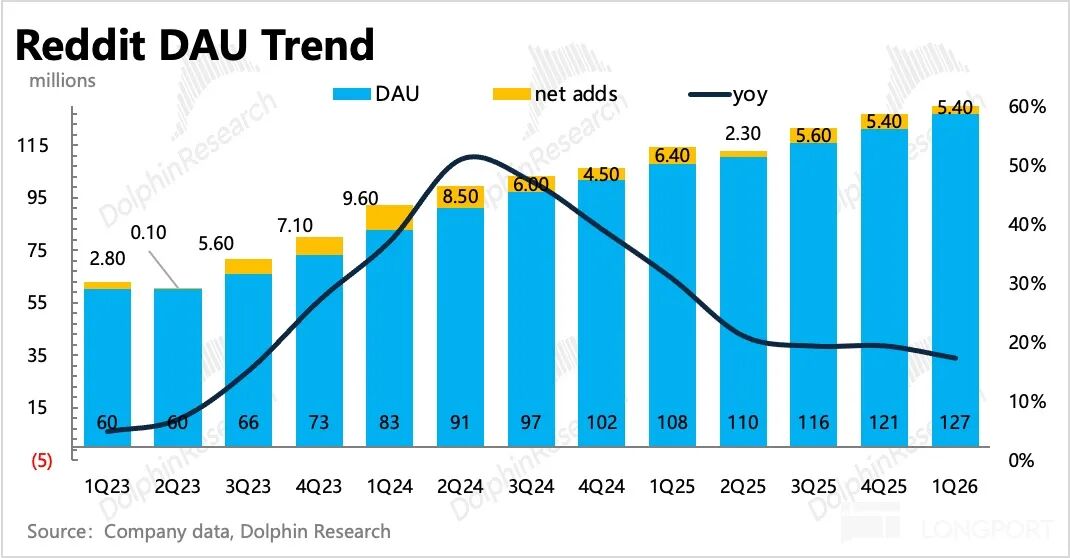

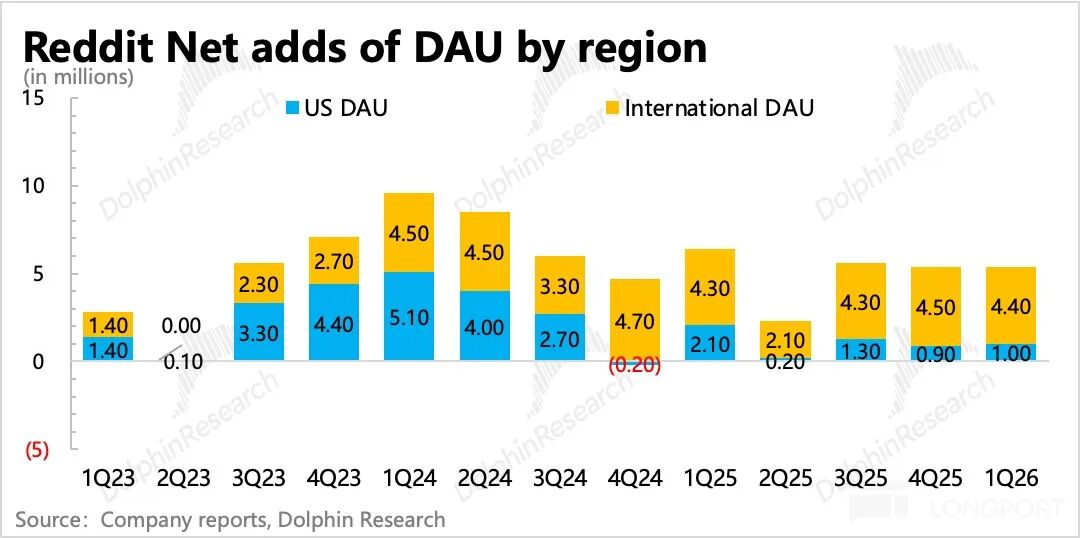

1. User Metrics: Slow Growth in the U.S. Region

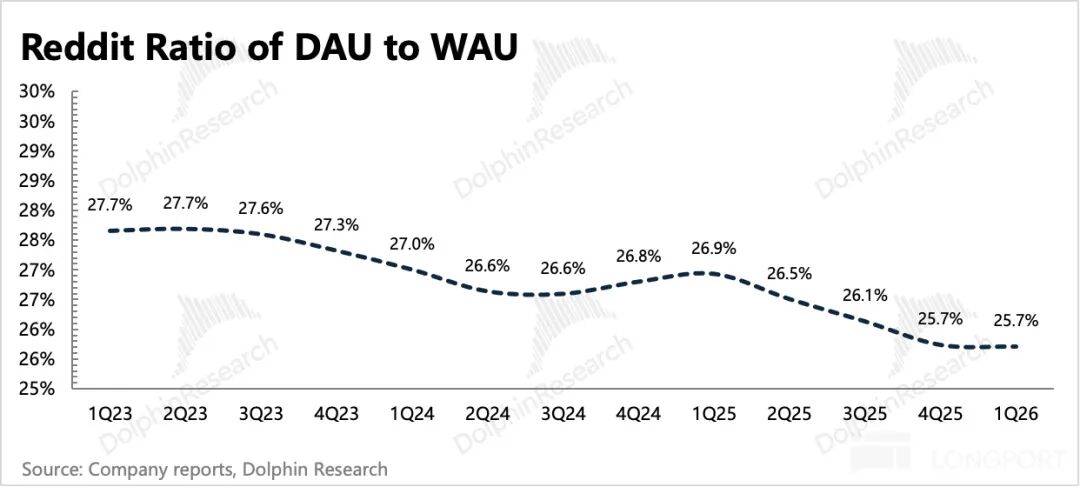

Q1 platform DAU grew to 127 million, a net increase of 5.4 million quarter-over-quarter. Weekly active users (WAU) increased by 23% year-over-year, with a net increase of 21.5 million. User engagement (DAU/WAU) stood at 25.7%, remaining stable quarter-over-quarter.

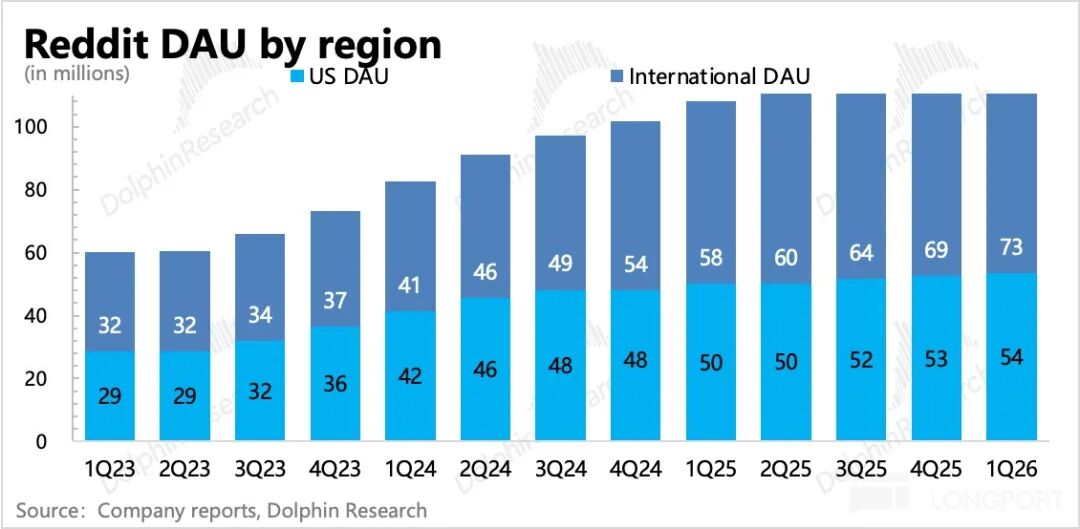

Regionally, the U.S., which contributes the most to commercialization, continues to see slowing user growth. International DAU grew by 26%, with the platform's machine translation now covering over 30 languages globally.

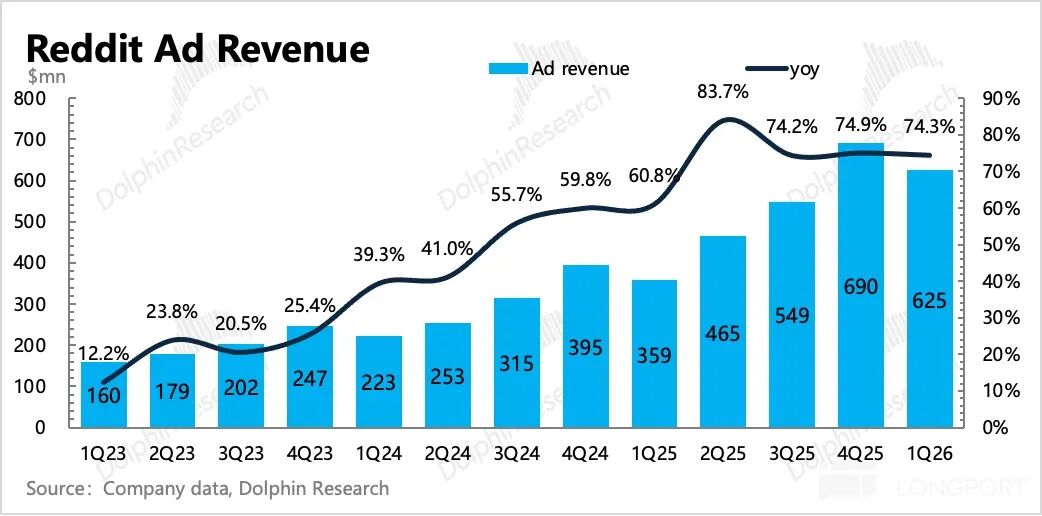

2. Continued Commercialization, Q2 Guidance Indicates Slowing Growth, Potentially Due to Macro Factors and Conservative Guidance

Q1 total revenue reached $730 million, up 69% year-over-year and roughly flat quarter-over-quarter, significantly exceeding expectations. Management guided for Q2 revenue growth to slow to 45%, which we attribute to high base effects, macroeconomic disruptions from geopolitical tensions, and management's habitual conservative guidance.

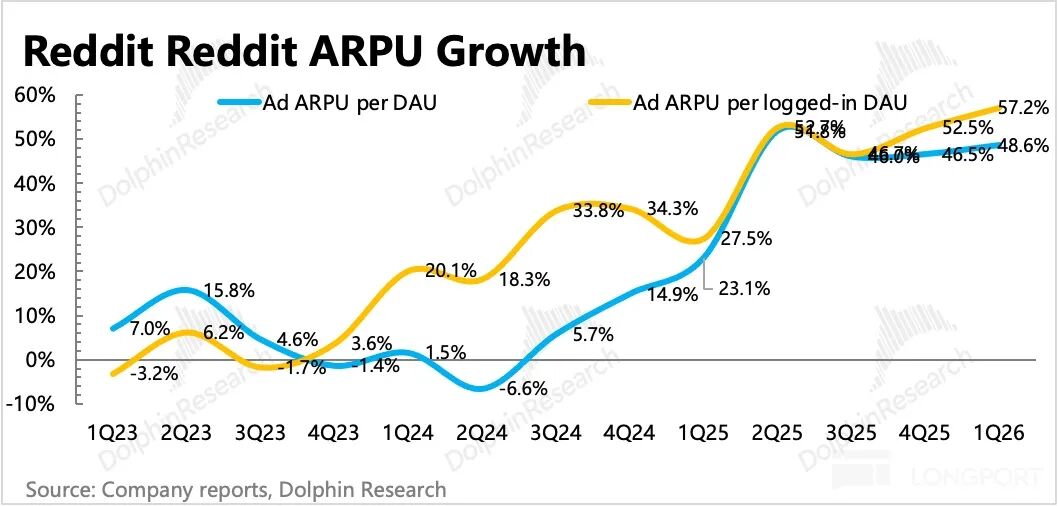

Revenue growth is primarily driven by advertising, including the shift from traditional brand ads to performance ads, which achieve higher CPM through improved ROI and increased ad load rates. Performance ads are rapidly penetrating advertisers in e-commerce and retail through DPA products (allowing advertisers to directly connect their product catalogs to Reddit, with the platform's AI automatically matching and dynamically displaying relevant products based on user interests and community context), contributing significant incremental revenue this quarter. Feed ads will also be rolled out in the future.

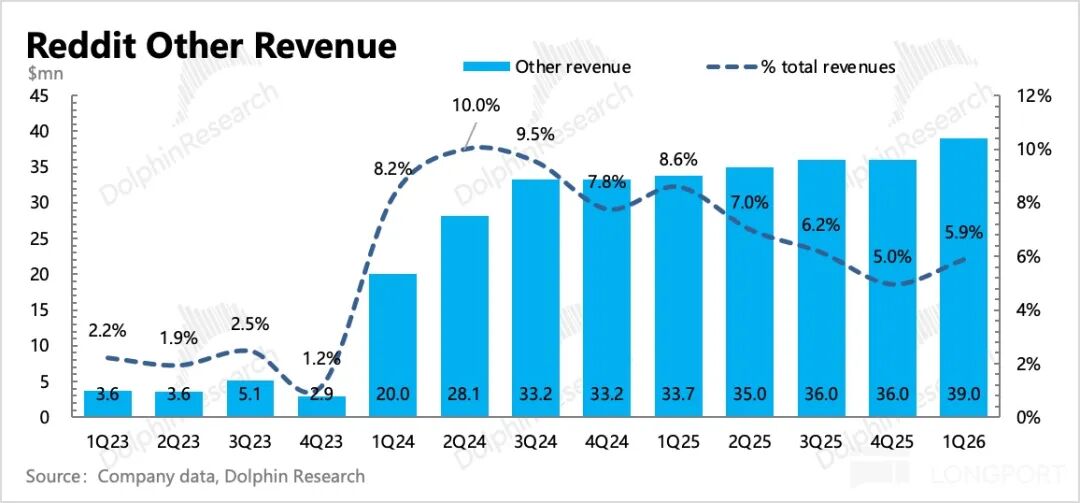

Data licensing revenue is recognized over time under contracts and remains stable (primarily from clients like Google, OpenAI, and Perplexity for AI model training). Google and OpenAI's three-year contracts expire at the end of this year and are likely to be renewed, with Reddit also seeking deeper collaboration, such as having AI answers cite Reddit content and negotiating for greater revenue sharing.

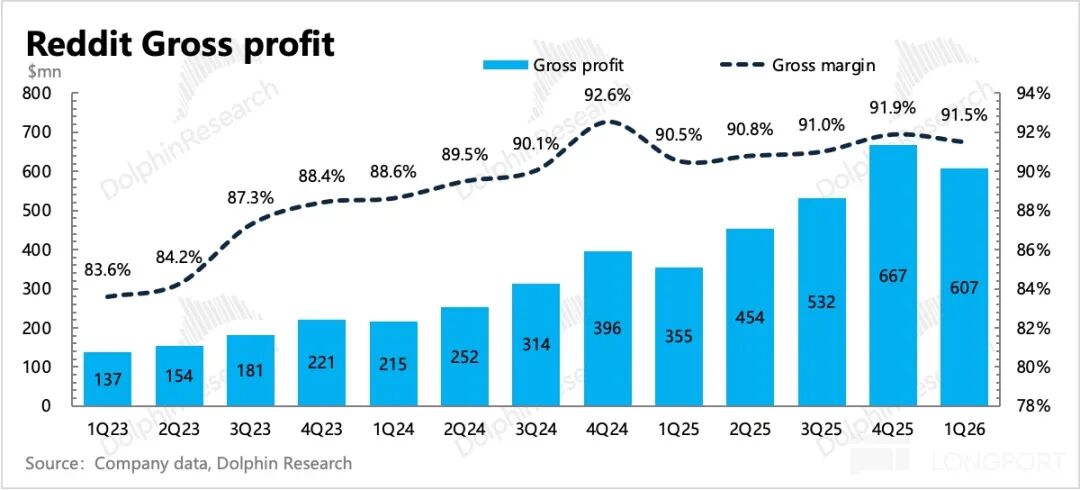

3. Profit Margins Continue to Improve

Gross margin improved by 1 percentage point year-over-year in Q1, with a slight quarter-over-quarter decline due to seasonal fluctuations, essentially peaking compared to peers.

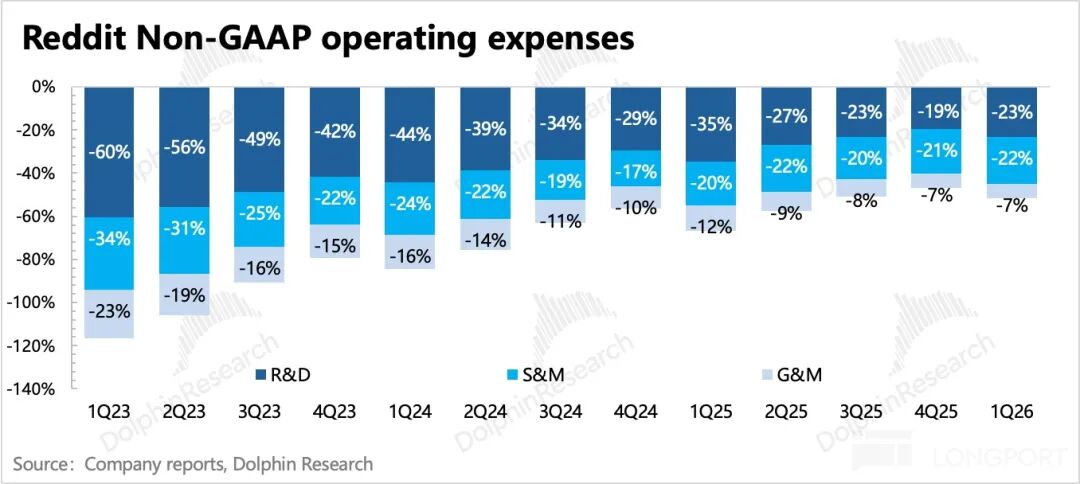

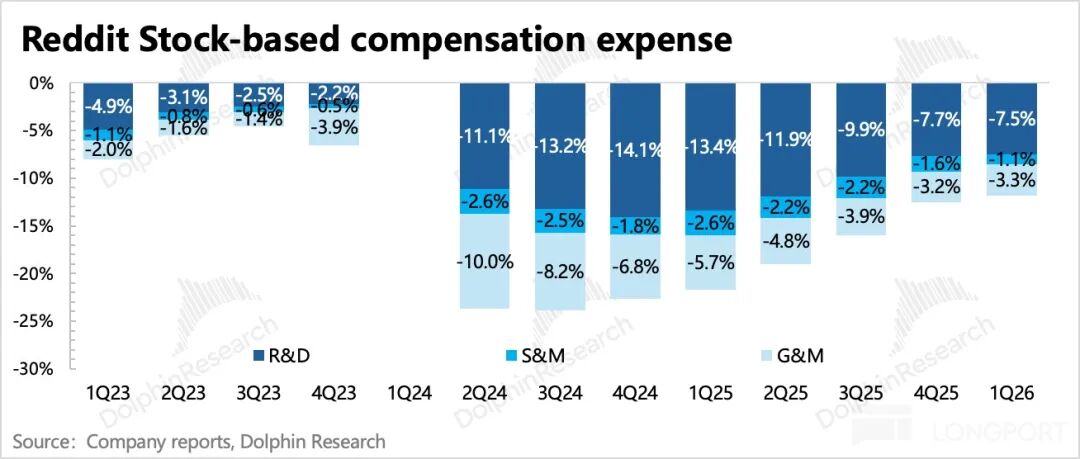

Operating expenses remain dominated by high sales expense growth, up 80% year-over-year, though slowing from the previous quarter. This likely reflects continued efforts to promote ad products and acquire users. Overall expenses continued to see significant optimization, down 14 percentage points, while equity incentive expenses as a percentage of revenue declined from 22% to 12% year-over-year.

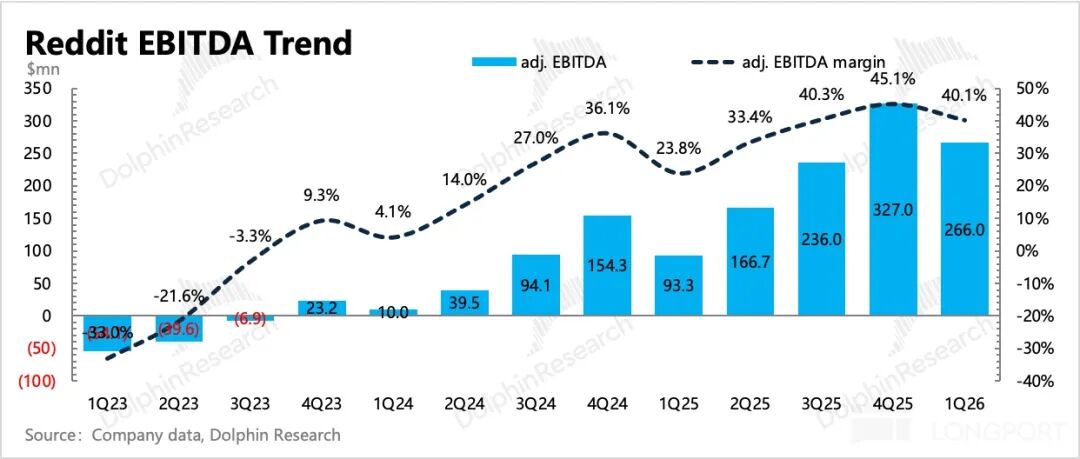

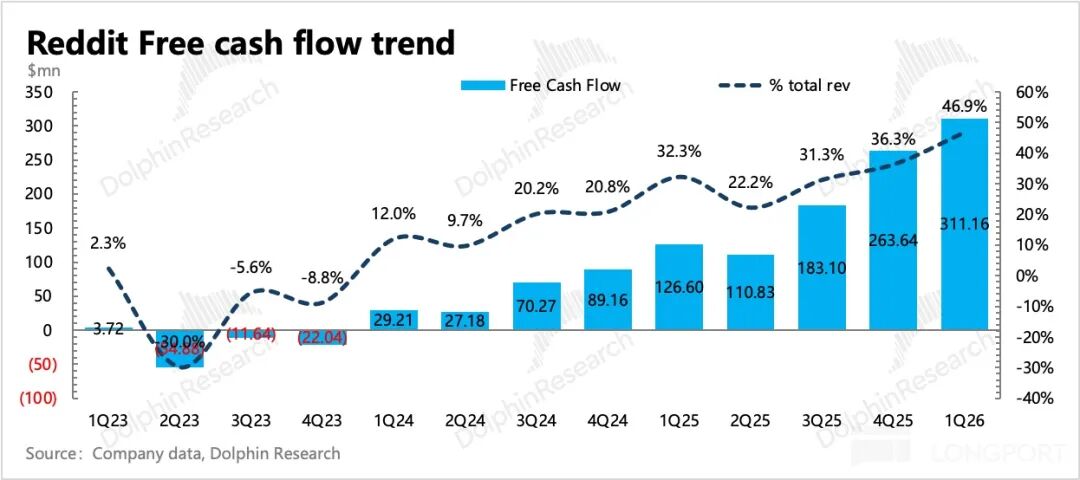

The company's profitability target—an adjusted EBITDA margin of 50%—stood at 40% in Q1, reflecting seasonal fluctuations (Q1 is typically a slower season compared to Q4), but remains on an upward trend overall. Free cash flow continued to reach new highs, accounting for 47% of revenue, aligning with the asset-light, cash-generative nature of the advertising industry.

The $1 billion share repurchase program announced last quarter officially began in Q1, with only $5 million spent to repurchase 35,000 shares. Net cash on hand reached $2.7 billion at the end of Q1, with quarterly free cash flow now at $300 million, making it relatively easy to sustain the repurchase program. However, the repurchase pace remains slow, and with no fixed expiration date for the $1 billion program, shareholder return calculations are not yet possible.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Authorization is required for reprinting.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for general viewing and data reference by users of Dolphin Research and its affiliates. It does not consider the specific investment objectives, product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are undertaken at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are provided for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be construed or deemed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of securities or related financial instruments. The information, tools, and data in this report are not intended for distribution to or use by individuals or residents of jurisdictions where such distribution, publication, provision, or use would contravene applicable laws or regulations or subject Dolphin Research and/or its affiliates or subsidiaries to registration or licensing requirements in those jurisdictions.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliates.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized parties. Dolphin Research reserves all related rights.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!