The LABUBU Fridge Goes Viral with a 14x Premium, Yet Fails to Lift POP MART's Stock Price

05/07 2026

05/07 2026

578

578

POP MART Needs Time to Prove Itself

The LABUBU Fridge Goes Viral, Then Fades Quickly

At 10 PM on April 30, POP MART launched its first home appliance—the LABUBU fridge. With a global limited run of 1,998 units and over 60,000 pre-orders, it sold out instantly, leaving ordinary consumers little chance.

Image Source: Internet

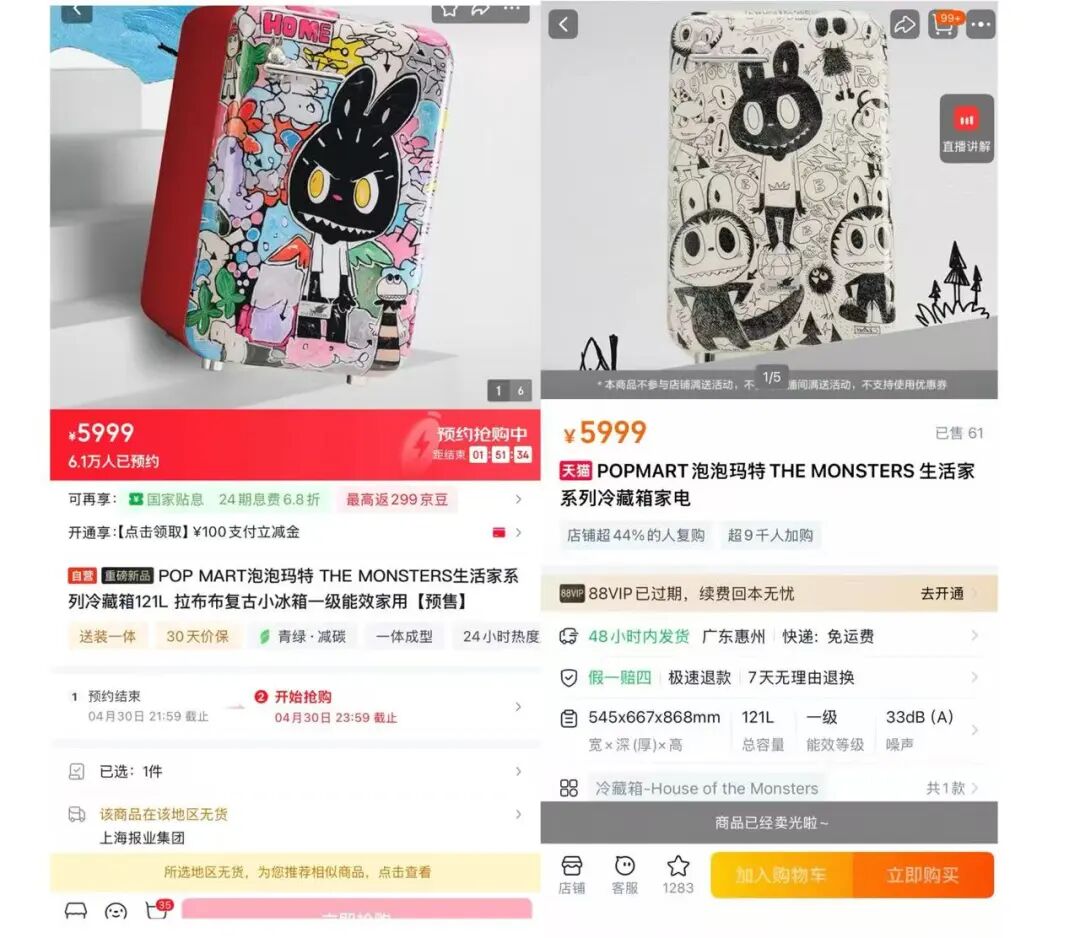

The real drama unfolded in the secondary market. At launch, prices on platforms like Dewu skyrocketed, hitting a peak of 20,999 yuan, with some listings even reaching 99,000 yuan as “bait.” The logic was cold and clear: leverage LABUBU’s “ugly-cute” IP appeal and the scarcity narrative of “limited edition + unique serial numbers” to transform an ordinary mini-fridge into a social currency with both “utility value” and “collectible value.”

Image Source: Internet

Yet the turnaround came faster than expected. The sky-high prices lasted less than three hours before plummeting, stabilizing around 7,300 yuan. By May 2, secondary market prices had settled at 6,800–6,900 yuan, erasing nearly all the premium.

Image Source: Internet

This abrupt shift left many puzzled. With only a More than ten times (dozen-fold) premium and a globally limited release, were POP MART’s consumers moving on, or had the hype simply worn off?

Supporters of the LABUBU fridge argued, “It’s not even half the price of a SMEG, and it’s a limited edition. For the wealthy, a few thousand yuan is nothing—it’s all about emotional value. With only 1,998 units worldwide, snagging one is a steal.” Others pointed out, “Vintage mini-fridges in the 3,000–4,000 yuan range sell like hotcakes. POP MART’s pricing isn’t a concern—if you think it’s expensive, you’re just not their target customer.”

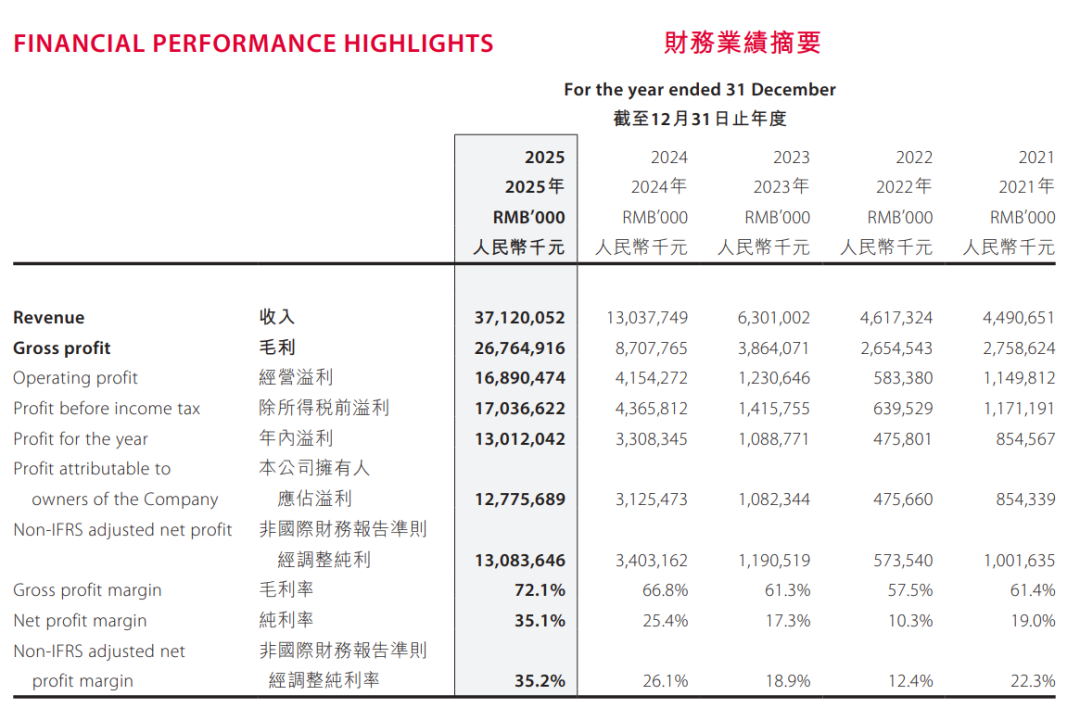

From POP MART’s 2025 annual report, there’s little sign of decline. Full-year revenue hit 37.12 billion yuan, up 184.7% YoY; adjusted net profit reached 13.08 billion yuan, soaring 284.5% YoY. Gross margin improved to 72.1%, with a net margin of 35.1%, showcasing strong pricing power and cost control.

Image Source: POP MART 2025 Annual Report

Overseas revenue accounted for nearly 44%, becoming a new growth engine. The plush toy category surged over 560% YoY, becoming the top revenue contributor for the first time.

From a capital market perspective, POP MART remains a love-hate stock. Facing skepticism, management offered a different narrative. Chairman Wang Ning dubbed 2026 the company’s “pit stop year.”

The metaphor is apt: after breakneck growth, the “race car” needs refueling and tire changes to prepare for the next leg. This isn’t a sign of weakness but a proactive strategic shift.

Led by LABUBU, POP MART is accelerating the incubation and operation of other IPs, such as Xingxingren (up over 1,600% YoY) and CRYBABY, building a deeper IP portfolio.

Image Source: POP MART Official Website

From plush toys to small appliances (like the LABUBU fridge), dessert shops, and apparel, POP MART is expanding its IP influence beyond “collector’s cabinets” into “lifestyle circles,” aiming to unlock a second growth curve.

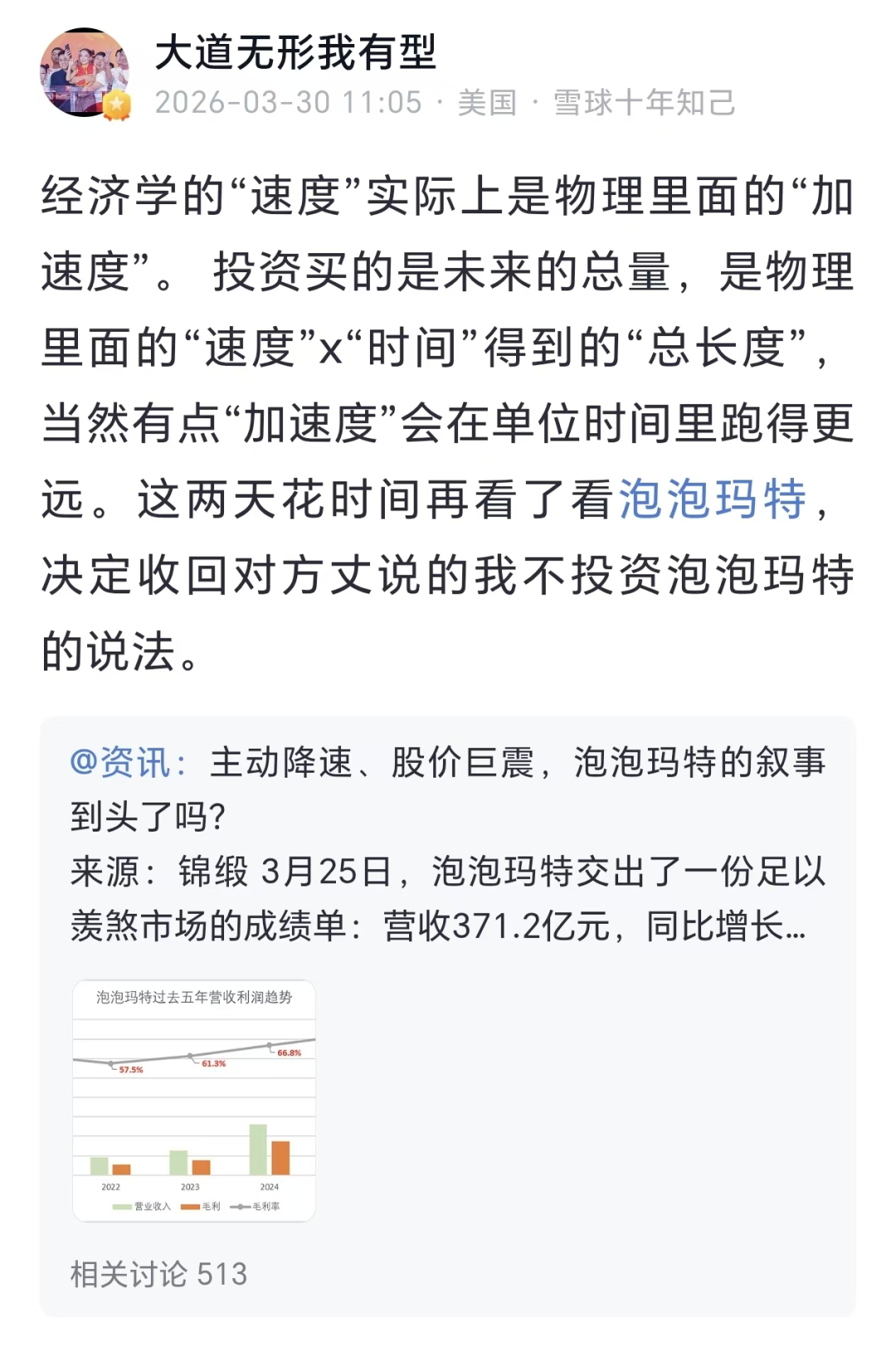

Yet the market remains unconvinced by POP MART’s transformation narrative—except for Duan Yongping, whose evolving stance on the company has become a capital market spectacle. Institutional investors led the retreat, only for Duan, once a vocal skeptic, to have an epiphany. He argued that one must look beyond “acceleration” to “total distance,” announcing the withdrawal of his earlier stance against investing in POP MART.

When Value Investors Meet the “Emotion Economy”

In August 2025, Duan first mentioned POP MART on Snowball: “The products are interesting, but I can’t see where the company will be in 10 years.” This reflects a classic value investor mindset—prioritizing long-term sustainability over short-term hype. By December, he was more blunt: “Life is busy; I skip what I don’t understand.”

Image Source: Internet

The turning point came on March 25, 2026. POP MART’s 2025 annual report revealed 37.12 billion yuan in revenue, 13.012 billion yuan in net profit, 44% overseas revenue, and a 72.1% gross margin. The report shattered Duan’s cognitive barriers.

“I’ve decided to withdraw my statement against investing in POP MART,” he wrote on Snowball on March 30. Four days later, he did something rare: visited a POP MART store at London’s Westfield Shopping Centre twice in one day. The shelves stocked with Labubu, Molly, and Skullpanda, along with young consumers lining up to check out, confirmed the overseas demand—aligning with the financial data.

Image Source: Internet

Critically, he read founder Wang Ning’s interview, *Because Unique*. “POP MART is the pioneer of Chinese product internationalization. Right business, right people!” he concluded on April 4.

Duan’s research began with a key analogy revision. Initially, he compared trendy toys to short-lived fads like Tamagotchi or hula hoops. But after studying Sanrio (Hello Kitty’s parent company), he realized IP businesses have cycles but aren’t fleeting. Founded in 1973, Sanrio’s Hello Kitty remains relevant, with 450 iconic characters. Despite volatile performance (e.g., 1,000% growth years and 80% declines), IPs endure over time.

Image Source: Sanrio Official Website

Duan’s three-step cognitive journey was clear: data validation → understanding emotional value → confirming competitive barriers. Financials were the gateway, while his gaming experience helped him grasp the sustainability of “paying for happiness.”

He ultimately identified four barriers:

1. **Brand Awareness**: POP MART is synonymous with trendy toys.

2. **Artist Signings**: Exclusive partnerships with global top designers.

3. **Global Retail Network**: Direct control over channels far exceeds licensing models.

4. **Strong Team**: Wang Ning’s business acumen was rated “top-tier” by Duan.

“These barriers don’t guarantee trendy toys will always be popular, but they ensure fans of the category will always follow POP MART,” Duan wrote on Snowball.

He opted to sell put options instead of buying shares outright, adhering to the value investing principle of “good price.” With 225,000 options, he’d acquire shares at a discount if the price fell below the strike price; if not, he’d pocket the premiums. This mirrors the “insurance company” mindset—using probability and risk-reward thinking for investments.

The core question remains sustainability. How long will demand for trendy toys last? Duan’s answer: “As a golfer, I’m often asked, ‘What’s your favorite course?’ In reality, I never ask such pretentious questions.” The subtext: Instead of predicting, observe. POP MART is already proving that emotional consumption isn’t a fleeting trend.

Image Source: Internet

Emotional Products Can’t Escape Market Cycles

Market debates over POP MART never cease.

The 2026 growth guidance of “no less than 20%” sparked controversy. Compared to 2025’s over 200% growth, the figure seemed conservative, triggering a stock sell-off. Institutions deemed a reasonable PE of 17–18x, but at 13x, the stock appeared cheap—until growth slows, potentially compressing valuations further.

Financially, POP MART ticks all the boxes for value investors: high net margins (sells expensive), high turnover (sells fast), and low leverage (minimal debt). Isn’t this a lightweight “money-printing machine”?

Yet even with mature IPs and Hatching ability (incubation capabilities), POP MART faces inevitable cyclical challenges. Nearly all IPs suffer high revenue volatility and uncertain popularity. Even top IPs like *Pokémon* and *Sanrio* aren’t immune. Founded in 1973, Sanrio’s Hello Kitty remains iconic, with 450 characters. Before 2000, Sanrio saw years of 1,000% growth but also 60–80% declines.

Image Source: Internet

Even in the pre-internet era (before 2000), Sanrio’s performance was volatile. From 2020–2025, it surged 1,922%—but could investors endure prior -79% and -94% drops? If you bought in 2013, you’d face seven years of declines (-79%), watching your portfolio shrink by three-quarters, a heart-wrenching ordeal.

Chief Business Review argues that all IP businesses revolve around community and cultural identity. Explosive growth requires expanding the fanbase, but overexpansion risks alienating core fans, diluting IP scarcity and hurting repurchase rates. Last year, POP MART’s top 20% fans averaged eight purchases, while casual fans bought two. Balancing core and casual fan revenue is a perennial challenge, with countless “expansion failures” as cautionary tales. POP MART’s current pace seems manageable, but the future remains uncertain.

Final Thoughts

POP MART offers a new blueprint for Chinese product internationalization—not through low prices but emotional value, cultural exports, and brand premiums. As Hello Kitty fades, Labubu and Molly are becoming global favorites. This story isn’t easy to tell, with no playbook to follow. Patience is key.

The hardest part of investing remains timing. How can investors hold for five or ten years instead of chasing short-term gains? The market isn’t impulsive—it’s individual investors who are. Balancing venture capital with basic financial planning, work and life, is no easy feat. Copying Duan Yongping’s strategy is unwise; he advises against investing for those with low income and limited corporate understanding. Ultimately, investing tests personal capability and cognitive edge—any shortcut risks heavy losses.

References:

“Don’t Worry About Duan Yongping and POP MART” – Source: Yuanchuan Investment Review

“Labubu Fridge Prices Collapse Overnight” – Source: Sina Finance

“POP MART Remains Too Conservative” – Source: Yuanchuan Institute

- END -

-

![]()

Lending My Face to an AI Short Film: A One-Way Journey

-

![]()

The "Midlife Crisis" of Long-Form Videos: Can AI Win Back Users?

-

![]()

The AI Industry Outlook Post-DeepSeek-V4 Launch

-

![]()

Why Manus Became the First AI Foreign Investment Acquisition to Be Suspended

-

![]()

The LABUBU Fridge Goes Viral with a 14x Premium, Yet Fails to Lift POP MART's Stock Price

-

![]()

AI Talent War: ByteDance’s Seed Emerges as the ‘Whampoa Military Academy’ of AI Amidst Rapid Talent Turnover Outpacing Model Updates?

-

![]()

Samsung's Exit from China: Will It Bounce Back Stronger Elsewhere?

-

![]()

Doubao Starts Charging, and I Actually Think It's a Good Thing