Doubao and OpenAI: Following the Old Path of Internet Monetization

05/08 2026

05/08 2026

439

439

The internet has fully documented the changing attitudes of OpenAI founder Sam Altman toward advertising from 2024 to 2026.

"I hate advertising."

"Advertising + AI makes me particularly uneasy. I see advertising as a last resort for our business model."

"We haven't built an advertising product yet, but I'm not entirely opposed."

"Maybe advertising isn't always so bad."

This buildup finally reached a clear milestone in May 2026: OpenAI launched the beta version of the ChatGPT self-service advertising management tool, Ads Manager, allowing advertisers to register and run campaigns independently. With this move, the AI company that claims to "ensure artificial general intelligence benefits all of humanity" has taken one step closer to becoming a "mature" commercial enterprise.

Around the same time, the topic of "Doubao's paid subscriptions" trended on Chinese social media. According to Doubao's updated paid service statement on the App Store, in addition to the free basic version, it will introduce paid Standard, Premium, and Professional versions with monthly fees of 68, 200, and 500 yuan, respectively.

Once again, the question of how AI companies can make money has entered the public spotlight. People are reminded that this technology wave, perhaps the most capital-intensive in human history, has yet to answer this most fundamental business question. From the United States to China, from OpenAI to Doubao, nearly all AI products are still copying the commercialization playbook of the internet era.

PART01

Advertising, Again

The United States is the birthplace of the internet subscription economy. Tech companies like Salesforce, Adobe, AWS, Netflix, and Spotify have trained countless Americans to pay monthly fees. Data shows that the average American household spends $273 per month and maintains 8.2 to 15 active subscriptions. In the second season of the hit American TV series *BEEF*, Ashley, a financially strapped country club employee, cancels all her paid subscriptions immediately after a medical procedure leaves her in dire financial straits.

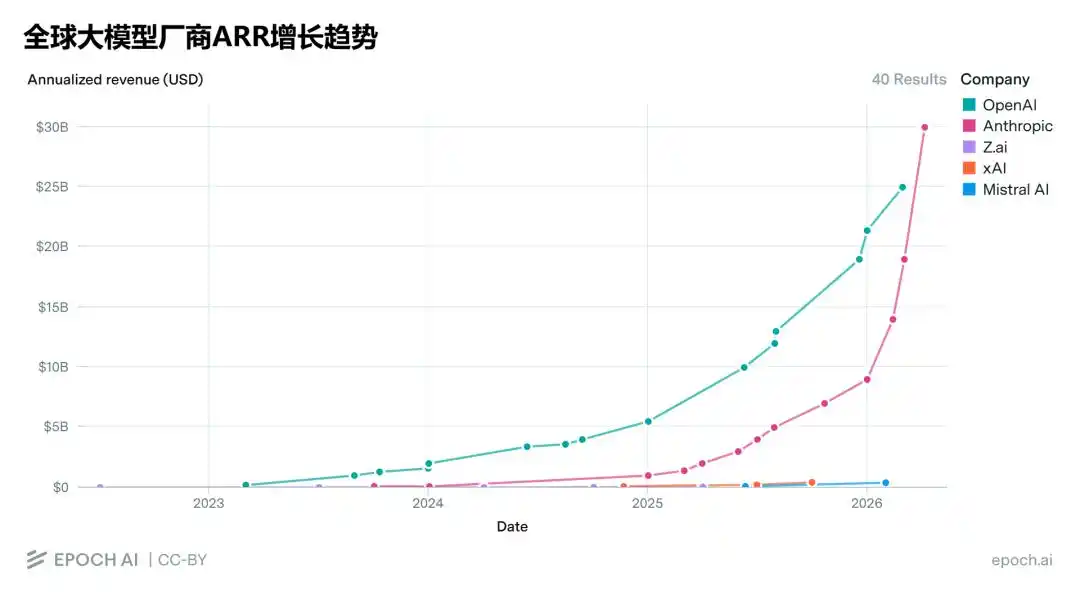

This may be where Sam Altman's disdain for the advertising business comes from. ChatGPT has 900 million weekly active users, with personal paid subscribers accounting for about 5.5%. Additionally, it has over 9 million paid enterprise users. From 2023 to the end of 2025, OpenAI's annual recurring revenue (ARR) surged from $2 billion to over $20 billion, a tenfold increase in two years.

Global LLM Vendors' ARR Growth Trends

However, computing expenses have grown almost in tandem. This creates an awkward situation: the more users, the heavier the losses. Sam Altman has compared data showing that ChatGPT's cost per word query is several cents, while Google Search's cost per query is just 0.2 cents.

Unlike internet businesses with diminishing marginal returns, AI is a capital-intensive industry. Every user conversation consumes computing power, and heavy users are even more expensive. Some users pay $200 per month in subscription fees but actually consume $5,000 worth of computing resources—pushing AI companies to their limits.

Thus, when it comes to computing pressure, Chinese and American AI companies share a common plight:

OpenAI's capital expenditures are expected to reach $50 billion in 2026 and $600 billion cumulatively by 2030. Meta has also adjusted its 2026 capital expenditure forecast to $145 billion, a record high. ByteDance and Alibaba have announced costly capital spending plans, while smaller LLM companies like Zhipu and Kimi, with limited "ammunition," can only shift pressure by raising API call prices.

More challenges lie ahead for OpenAI. Many subscribers are downgrading from the $20-per-month ChatGPT Plus to the $8-per-month ChatGPT Go, increasing user volume but reducing average revenue per monthly active user from $23 to less than $12. Additionally, Anthropic is aggressively poaching OpenAI's enterprise clients.

Advertising, the business Sam Altman once despised, suddenly looks appealing.

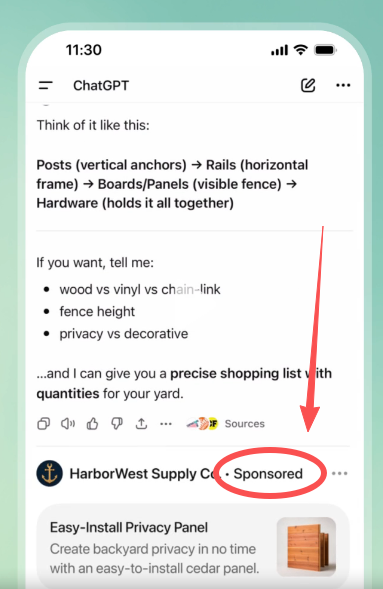

In February 2026, OpenAI launched a ChatGPT advertising pilot in the United States. By late March, it announced annualized advertising revenue of $100 million. Subsequently, Ads Manager went live on May 5. In advertising, AI's value lies in its deep understanding of user intent, enabling more precise targeting than social media feeds. Internal projections suggest OpenAI could achieve approximately $2.4 billion in advertising revenue in 2026, nearly $11 billion in 2027, and by 2030, advertising could become its largest revenue stream, surpassing $100 billion.

OpenAI Ads Sponsored Label

OpenAI is, in fact, copying homework. The path from subscriptions to advertising has already been paved by Netflix. In 2022, Netflix hit a subscription revenue growth bottleneck: its most valuable users had already converted, leaving either price-sensitive users or seasonal users willing to pay only for hits. So, at the end of the year, it launched a lower-priced, ad-supported subscription tier, "Basic with Ads," at $6.99 per month.

Netflix's Basic with Ads Plan Announced in 2022

The results were impressive. By May 2025, Netflix's ad-supported tier had 94 million monthly active users. In 2025, its advertising revenue exceeded $1.5 billion, more than 2.5 times higher than in 2024. Notably, nearly half of new subscribers from January to May 2025 chose the ad-supported tier.

Between saving money and saving time, ordinary Americans clearly prioritize the former.

However, for AI products, the negative impact of advertising on user experience may be more pronounced. At this stage, they remain utility tools—users engage briefly and leave. Tolerance for ads is likely lower than for time-killing internet products like Netflix. If ChatGPT fails to strike the right balance between ads and informational value, it could face declining retention and engagement, undermining ad performance.

Rival Anthropic seized this opportunity to mock OpenAI. During the 2026 Super Bowl, it aired an ad directly attacking ChatGPT. The preview version was blunt: "Advertising is coming to AI, but not to Claude." The final version was slightly more diplomatic: "There’s a time and place for ads. AI conversations aren’t it."

Anthropic's founder left OpenAI precisely because he disapproved of its commercial compromises. Ironically, Anthropic is now reportedly pursuing a massive $50 billion funding round, aiming for a $900 billion valuation—surpassing OpenAI for the first time. At least in this round, capital markets deem it more commercially valuable.

PART02

Survive First, Then Thrive

With OpenAI as a precedent, Doubao's paid subscription model makes sense: use subscription revenue to offset computing costs from its 345 million monthly active users while filtering out deep-pocketed users with higher AI demands. This is the path OpenAI took in its early years.

QuestMobile's *2026 Q1 AI App Insights Report*

Jack Ma said in 2012 that failing to make money is immoral. Businesses should feel ashamed if they can't turn a profit.

Doubao can afford to avoid shame for now, thanks to its massive user base and ByteDance's deep pockets. But pressure is mounting. By March 2026, Doubao's daily token usage had surpassed 120 trillion, making it one of the world's top three token consumers. Third-party estimates suggest ByteDance spent about 160 billion yuan on capital expenditures in 2025, with 90 billion allocated to AI computing procurement.

Currently, Doubao appears to be replicating Douyin's (TikTok's Chinese counterpart) playbook: first drive growth through free offerings, then monetize via traffic. The key difference lies in monetization methods. Douyin relies on value-added services like advertising and e-commerce, while Doubao has chosen subscriptions. This reflects their identities: Douyin is a content platform, making it a natural fit for ads and e-commerce; Doubao is an AI tool, addressing efficiency needs.

Will Doubao introduce an advertising platform in the future? That may depend on OpenAI's success and whether new AI business models emerge.

AI companies in both China and the U.S. are still feeling their way forward. To date, none have generated AI business revenue commensurate with their valuations or market caps. Yet capital markets are ablaze. PitchBook data shows that in Q1 2026, five AI companies secured nearly 70% of global AI funding. Meanwhile, OpenAI and Anthropic have taken turns becoming the world's most valuable companies—despite neither being profitable. This fuels conservative investors' fears of a bubble.

However, history shows that many internet monetization models were pioneered during downturns by brilliant minds.

Google's advertising system, AdWords, launched in 2000, was a product of the dot-com bubble. The founders nearly sold the company in 1999 to return to school, but no buyer—including Excite, Yahoo, or Lycos—valued their technology, rejecting offers even when the price dropped from $1 million to $750,000.

With no choice, they embraced advertising, abandoning their purity about technology.

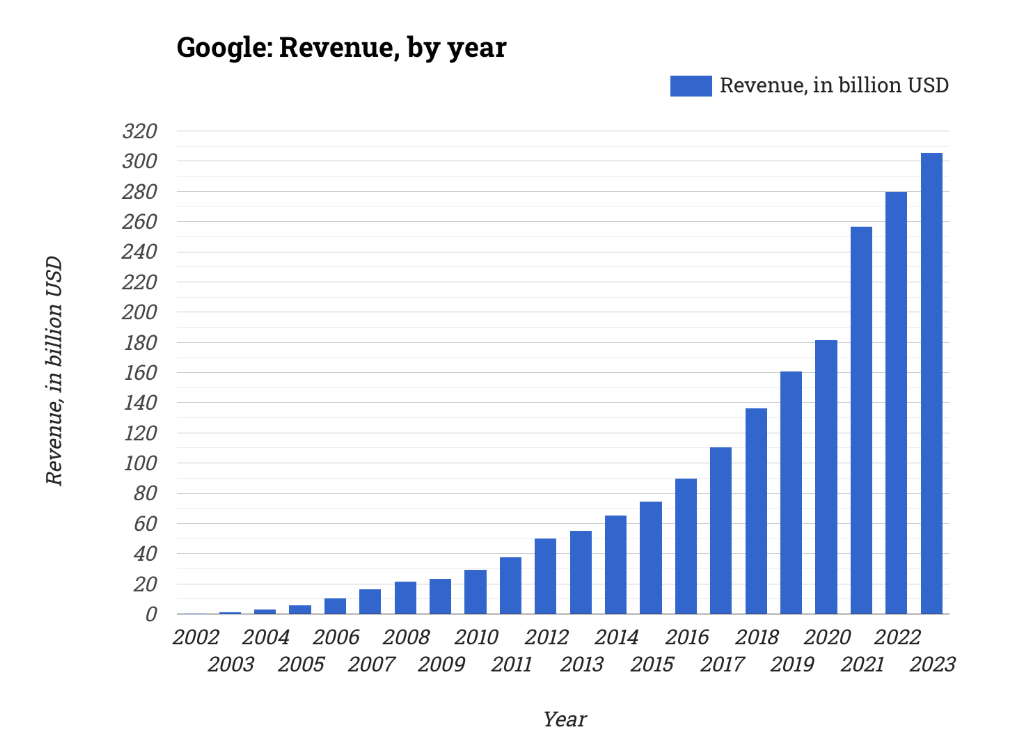

By 2003, advertising generated $600–700 million in annual revenue for Google. By 2010, that figure exceeded $28 billion, accounting for 96% of total revenue—making Google the world's largest digital advertiser.

Google's Revenue Growth from 2003 to 2023

Another historical pattern: in the internet industry, most disruptive business model innovations emerge from "killer apps." These apps most broadly lower user barriers, even creating entirely new usage scenarios and willingness to pay. WeChat Pay, Alipay, and Douyin's information feed all exemplify this.

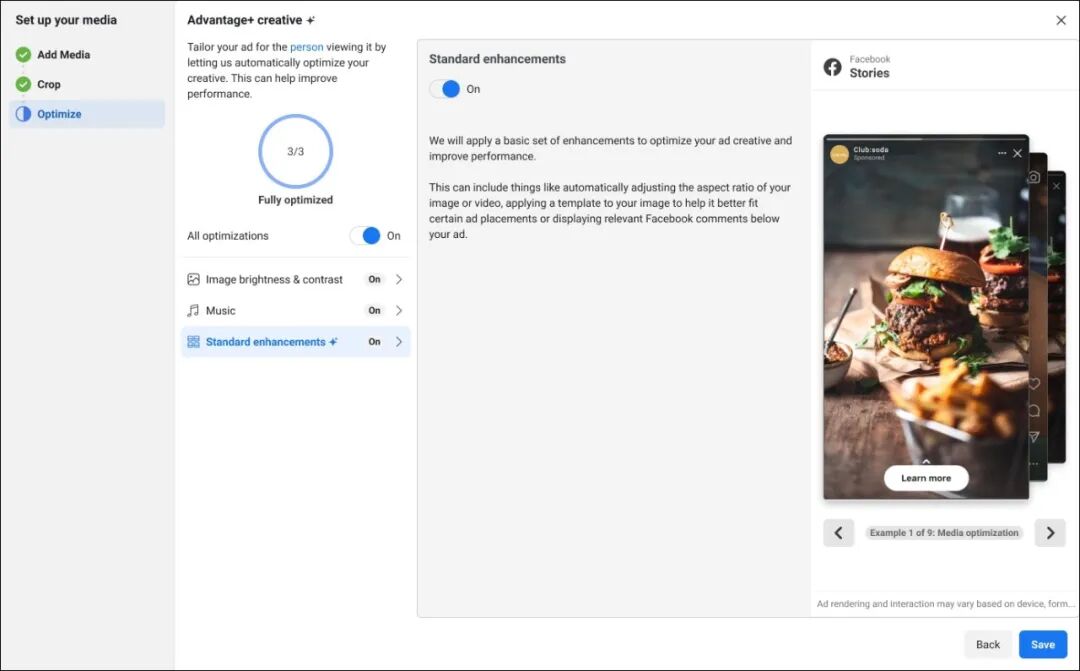

Such changes also drive shifts in market leadership. Market forecasts suggest Meta's ad revenue will surpass Google's in 2026, making it the world's largest digital advertiser. A key factor is Meta's AI-powered automated advertising tool, Advantage+, which generates creatives, matches audiences, and optimizes conversions, boosting ROI by an average of 22% and attracting many advertisers.

Advantage+ Automated Ad Generation Example

From this perspective, Doubao's future monetization models are even more intriguing—it is currently closest to becoming a "killer app."

The other pillar of China's AI duo is Alibaba, which has taken a different path. By establishing ATH and focusing on tokens, its direction is clear: it aims to profit from infrastructure—high-investment, capital-intensive, with low but stable margins. However, its Qianwen App is aggressively expanding scenarios to compete for AI gateway status, likely driven by inertia (inertia). In internet logic, traffic precedes all stories.

Will this traffic-driven approach be disrupted by new AI technologies? Could AI make smartphones obsolete? Many questions remain unanswered, as AI technology continues to evolve.

For now, AI businesses may merely be "parasitizing" old internet monetization models temporarily, as AI products lack irreplaceability. Until they become indispensable to modern society, AI companies must rely on subscriptions and advertising to stay afloat.

In both the internet and AI eras, survival remains the top priority.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!