Observation | ByteDance's 842 Billion Baht AI Data Center Investment in Thailand: Facing a Funding Gap, Why Double Down?

05/08 2026

05/08 2026

777

777

With an approved investment of 842 billion baht (approximately RMB 177.8 billion) for ByteDance's large-scale data center project in Thailand, market sentiment has split into two extremes. Some hail it as a milestone for Chinese tech companies going global, while others call it a typical high-stakes, asset-heavy gamble.

Most current analyses focus on superficial factors such as location advantages, computing power applications, and geopolitical risks. Few delve into the most straightforward yet critical question: With ByteDance's projected net profit of just RMB 65 billion in 2025 against capital expenditures of RMB 160 billion, leaving a nearly RMB 95 billion funding gap—where will the money come from?

Compared to policy incentives, this funding challenge is the true crux of the matter.

■ Let's First Examine the Three-Year Financials

Since ByteDance is not publicly traded and lacks audited financial reports, the following financial data is sourced from industry estimates, intended solely to assess operational trends and not for precise conclusions.

2023: The Era of Effortless Profits. Net profit reached RMB 223 billion, with capital expenditures of RMB 49 billion, resulting in an annual surplus of RMB 174 billion. With nearly RMB 200 billion in cash on hand, ByteDance expanded with confidence.

2024: The Safety Net Thins. Net profit rose slightly to RMB 238 billion, but capital expenditures surged to RMB 80 billion, shrinking the annual surplus to RMB 158 billion. Profits continued to grow, but spending accelerated noticeably.

2025: A Complete Revenue-Expenditure Reversal. Net profit plummeted to RMB 65 billion, while capital expenditures soared to RMB 150 billion, creating an RMB 85 billion funding gap. Simply put: This year's earnings barely cover a fraction of the spending.

The most alarming trend over these three years is not the slight decline in surplus in 2024 but the complete reversal of profit and expenditure in 2025. ByteDance enters a phase where earnings no longer cover expenses.

■ How Will the Gap Be Filled?

Companies typically address funding gaps through three avenues: drawing on past cash reserves, external financing, or divesting non-core businesses.

For ByteDance, which remains unlisted and has long relied on self-financing, this marks the end of an era where it could comfortably "earn effortlessly from advertising and spend freely."

The most straightforward speculation is that ByteDance will rely on its substantial cash reserves built up over previous years to fund this round of AI-related capital investments. Another possibility is foreign bank loans, though ByteDance has never disclosed its debt levels, making it impossible to gauge true financial pressure. Some argue that the RMB 100 billion-plus investment will not be spent in a single year but rolled out in phases to smooth financial strain.

Regardless of the approach, one fact remains: In 2025, ByteDance's spending will far outpace its earning capacity.

The long-held belief in the internet circle that "ByteDance never runs short of cash" no longer holds water in light of these figures.

■ Why Such a Sharp Profit Decline?

Over two years, net profit collapsed from RMB 223 billion to RMB 65 billion, a drop exceeding 70%. Many attribute this simply to "the high cost of buying AI chips," but this explanation lacks nuance.

From a financial perspective, chip purchases are classified as fixed assets and depreciated over multiple years, rather than impacting annual profits all at once. The real profit killers are the cumulative effects of multiple business costs:

1. Domestic Advertising Plateau. Douyin's traffic growth has peaked, advertisers are tightening budgets, and industry competition has intensified, slowing growth in ByteDance's core revenue engine.

2. Overseas E-Commerce Bleeding. TikTok Shop's expansion in Southeast Asia involves heavy spending on logistics infrastructure, merchant subsidies, and team expansion, with no clear path to profitability yet.

3. Sustained High AI Costs. Large-scale model training, computing power maintenance, R&D, and hiring top talent all represent ongoing cash outflows.

4. Drag from Domestic Diversification. Local services and self-operated e-commerce have long been unprofitable; the shutdown of earlier education initiatives resulted in significant asset write-downs.

5. Rising Operational Costs. Employee compensation packages have increased, along with global compliance risks, cross-border taxes, and equity investment valuation fluctuations, further squeezing accounting profits.

With these multiple pressures, profit declines have become inevitable. Attributing the downturn solely to "chip purchases and AI investments" oversimplifies the complex business dynamics and lacks rigor.

■ Where Will the Returns Come From for This Asset-Heavy Investment?

With RMB 100 billion earmarked for overseas computing infrastructure, the market's primary concern remains: How will this asset-heavy investment generate returns?

Consider these public data points:

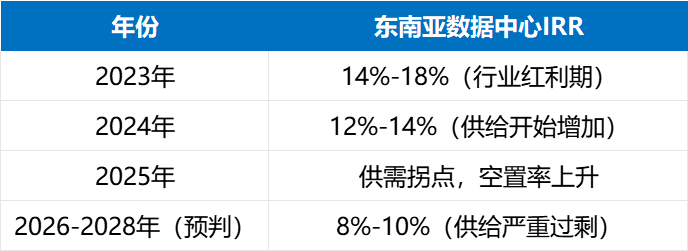

Monitoring data from CBRE and Knight Frank shows that Southeast Asian data center rental prices began declining in 2024, with cabinet rents in Peninsular Malaysia dropping 8%-12% year-on-year, leaving many mid-to-low-end cabinets vacant. Industry forecasts suggest that from 2026 to 2028, as Southeast Asian computing capacity comes online, oversupply will likely drive rents even lower.

The industry outlook is not optimistic. However, it is crucial to distinguish between civilian-use colocation facilities and corporate self-use computing infrastructure.

ByteDance's overseas data centers are not primarily built to rent out cabinets for profit. Their core purpose is to support TikTok's global operations, self-developed large model training, and algorithm iterations; secondarily, they may sell AI computing power, cloud services, and private deployments for government and enterprises.

The value of this asset lies not in short-term rental income but in cost reduction, regulatory compliance, technological autonomy, and geopolitical risk mitigation.

Fundamentally, this is a strategic investment, not a short-term business play. The high upfront capital, ongoing maintenance costs, and extended return cycles of asset-heavy infrastructure are well understood trade-offs.

■ Why Thailand?

Among Southeast Asian nations, no location is perfect—each has strengths and weaknesses.

Singapore lacks land and electricity to support ultra-large-scale computing clusters; Peninsular Malaysia has a mature power grid but faces electricity shortages, while East Malaysia lags in infrastructure; Indonesia and Vietnam suffer from policy volatility, making heavy asset investments too risky.

By contrast, Thailand offers ample land and policy inclusiveness, with generous BOI investment incentives. However, its drawbacks are equally clear: an unstable power mix dependent on imported hydropower, with thermal power backfills driving up electricity prices; frequent government changes raising doubts about policy continuity.

In May 2025, Thailand's BOI approved six data center projects in one go, with ByteDance securing 842 billion baht—nearly 90% of the total allocation. By approval standards, this represents exceptional privilege.

Notably, Thailand has quietly tightened computing policies since 2024, raising clean energy thresholds and adding power guarantee clauses, effectively cooling the overheated sector. Against this industry downturn, ByteDance's counter-cyclical bet remains controversial.

To mitigate risks, ByteDance has secured top-tier tax and land incentives, pre-locked high-quality power plots, and bound itself to long-term clean energy agreements. With the project primarily for self-use and minimal colocation rentals, it avoids the industry's cutthroat competition over idle mid-sized facilities.

■ How Does the Industry View This Investment?

When asked, several Southeast Asian IDC insiders responded with consistent "caution":

"We're also expanding data centers in Southeast Asia, but we wouldn't adopt ByteDance's aggressive model of heavy assets and extra large (ultra-large) scale. Their approach suggests either deep internal drivers we don't grasp or a pure bet on the industry's future."

"The challenge with asset-heavy data centers isn't construction but long-term operations. These are energy beasts—Thailand's electricity price volatility, unstable grid loads, and rising maintenance costs mean any single variable out of control could force a complete recalculation of the RMB 100 billion investment's returns."

"BOI officials have long warned about computing overcapacity. The new regulations raising thresholds are essentially a gentle cap. ByteDance's major move at this juncture raises timing questions."

While all acknowledge real risks, none are certain the investment will fail. Objectively, this is neither a surefire win nor a blind gamble.

■ Conclusion

The confirmed facts are clear: ByteDance's profits have collapsed over two years while capital expenditures have surged; Southeast Asia's civilian computing sector faces imminent oversupply; and the industry broadly doubts short-term returns.

Yet much remains unknown: internal fund allocation details, underlying decision-making logic, and long-term computing commercialization paths are all opaque to outsiders.

This article neither dismisses nor glorifies the investment. Until more official information surfaces, any definitive judgment would be premature.

The die is cast, but success or failure remains uncertain. One trend is undeniable: Global internet competition has shifted from traffic acquisition to foundational computing power.

For Chinese internet companies going global, the era of light-asset, effortless profits is over.

- END -

-

![]()

AI Giants Start Borrowing to Fuel Computing Power Race

-

ByteDance Initiates Largest B2B Structural Adjustment, This Time It's Truly Different

-

![]()

Let's Talk About Kingsoft Office's Mid-Year Outlook and the True Strength of Its AI-Powered Office Solutions

-

Despite 150 Million Users, Struggles Persist: AIShige Faces Tough Competition from Seedance and Kling in AI Video Monetization

-

![]()

Ensuring Safe Gear Shifting in the Automotive Industry: Transitioning from 'Product Oversight' to 'Full-Chain Governance'

-

![]()

Net Profit Soars to $133.7 Billion! Azure Revenue Tops $100 Billion, with AI Fueling Microsoft's Growth

-

![]()

Before 6G Hits the Market, the U.S. Forges a 'Rules Alliance': What Challenges Await Chinese IoT Enterprises?

-

![]()

Intelligent Driving's 'Little Blue Light' Faces Ban: Night Glare and Cut-in Risks Prompt Official Action