The Unsolved Enigma of Manus: The Return of US$2 Billion | In-Depth Analysis

05/09 2026

05/09 2026

655

655

An acquisition deal, already funded, was abruptly cancelled with the mere press of a button. On April 27th, Meta's acquisition of Manus came to a grinding halt. Billions of dollars in received funds must now be fully refunded.

For investors, this marks a stark reversal from a 'successful exit' to 'starting from scratch.'

Through its failed deal, Manus has imparted a valuable lesson to the entire industry: Some shortcuts may seem quicker, but they come with a hefty price tag.

- 01 - Restoring Order

Manus can no longer be sold. On April 27th, Meta's acquisition of Manus was officially cancelled. What sets this case apart is that it was a deal where 'funds had already changed hands,' necessitating a complete restoration to the original state.

On Manus's official website, the phrase 'Belongs to Meta' still lingers.

According to media reports, in December last year, Meta planned to acquire Manus (parent company: Butterfly Effect) for over US$2 billion. Founder Xiao Hong (born in the 1990s) was set to become Meta's Vice President, reporting directly to the Chief Operating Officer. Meanwhile, Manus's core technical team of about 100 people would be fully integrated into Meta's Super Intelligence Lab in Singapore, maintaining independent operations.

On January 8th, the Ministry of Commerce announced a compliance assessment investigation into the acquisition, causing the deal to stall.

In April, the Office of the Foreign Investment Security Review Working Mechanism (National Development and Reform Commission) issued a ban on the investment, demanding a full refund, divestment of all data/technology, and termination of authorization.

Meta, formerly known as the social media platform Facebook, underwent a rebranding.

A source close to Manus's investors revealed to Qianbidao that during the transaction process, Meta, the acquiring party, transferred funds swiftly. At least two insiders confirmed to Qianbidao that as early as January this year, Manus and its investors had already received Meta's funds.

In other words, from a financial standpoint, the sale of Manus to Meta had already entered the execution phase. Based on the shareholding structure and valuation at the time, this was a highly profitable exit.

According to media and insider reports, multiple investment institutions in Manus achieved a paper exit through this transaction.

Based on the original transaction plan, market information indicates that Tencent holds approximately 11% of the shares, with a theoretical exit amount of about US$200 million, making it one of the largest beneficiaries. 'Tencent's investors told me they received the money very early (before mid-January this year),' the insider revealed.

Sequoia Capital and ZhenFund hold 4%-7% of the shares, with a theoretical exit amount of approximately US$80 million to US$140 million. Qianbidao reached out to Sequoia China for confirmation but did not receive a response.

It should be noted that since the relevant parties have not disclosed specific shareholding structures, the above data is based solely on public information and market estimates, and there is some uncertainty.

After the 'deal cancellation announcement' was released, the subsequent handling method became a topic of industry concern.

Liu Zhishuo, Founding Partner of Zhongguancun Dahe Capital, stated that based on historical cases, the core handling principle this time might be 'restoring the original state.' This may specifically include: cancellation of the equity transaction agreement, refund of funds, and restoration of the shareholding structure to its pre-transaction state.

'During the process of restoring the original state, if opportunity costs are incurred, they will likely need to be borne by the party at fault,' Liu Zhishuo analyzed.

Currently, the allocation of responsibility in this incident has not been clarified.

From the perspective of 'failing to declare the investment,' during the deal's progression, Manus's structural transfer and declaration arrangements, Meta's advance payment, and the exit coordination of some investors may all involve certain compliance controversies.

According to cross-border investment regulatory requirements, transactions involving data, core technologies, and sensitive fields typically require foreign investment security reviews or relevant declaration procedures.

Another insider revealed that although the details of subsequent handling are still unclear, Meta's refund of funds is highly likely.

The complexity of the matter does not end there. Before the transaction, Manus had already completed a series of structural adjustments: relocating its main body to Singapore, adjusting or even downsizing domestic companies, and having the overseas entity take over the acquisition.

From the results, risks are now concentrating on Manus's side.

On one hand, investment institutions have shifted from 'having successfully exited' to 'possibly needing to return funds.'

On the other hand, the company has simultaneously lost two critical paths: the overseas merger and acquisition exit is blocked, and due to the previous overseas structural relocation and entity adjustments, there is uncertainty about returning to the domestic financing system in the short term.

- 02 - A Bold Approach

In the eyes of some investors, Manus's path was too rapid and bold.

Before the ban was issued, Hou Jiyong, a partner at Fengyun Capital, had vaguely suspected that the deal might be cancelled. To understand the outcome of this transaction, it is necessary to trace Manus's 'identity transformation' path.

Manus is not a native overseas AI company; it started with domestic R&D (by the end of 2024), but before advancing the transaction, it completed a series of key structural adjustments:

Around April 2025: Secured US$75 million in financing led by Benchmark Capital, drawing U.S. regulatory attention;

June 2025: Relocated its global headquarters to Singapore, changing its operating entity to an overseas company;

Around July 2025: Domestic team contractions, clearing of social media accounts, and blocking of Chinese IPs began to occur;

December 30, 2025: Meta officially announced the acquisition for over US$2 billion, with the transaction advancing to substantial execution overseas.

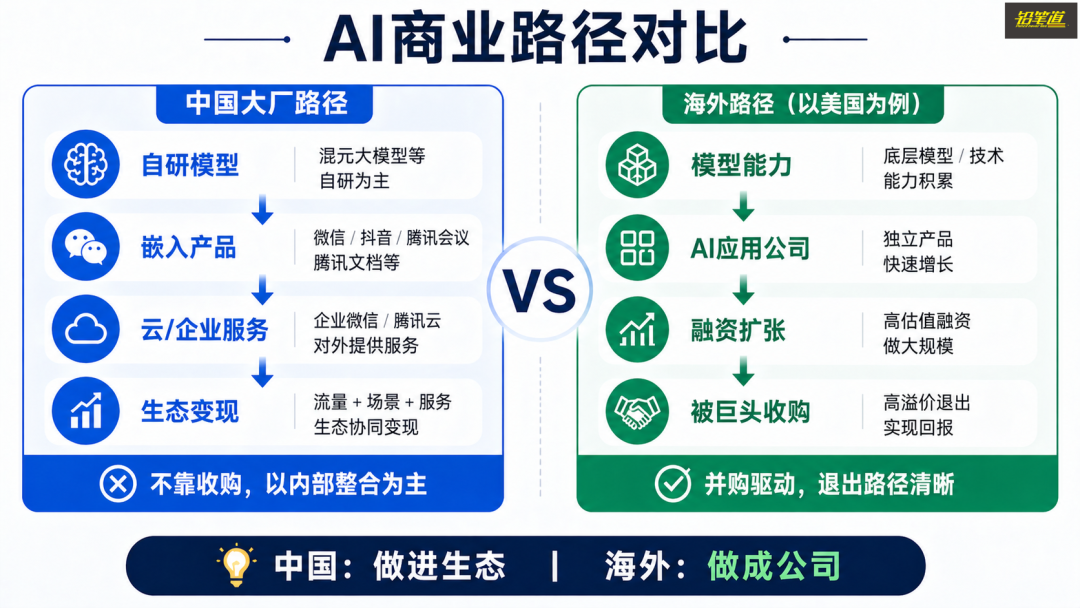

This path of 'domestic R&D, overseas shell swap, foreign acquisition' is known in the industry as 'bathing-style globalization.' Simply put, it involves transferring originally domestic businesses and teams into overseas entities through structural adjustments, allowing overseas companies to complete the acquisition.

Multiple investors stated that this path was highly attractive in the past, primarily because overseas markets valued AI application companies more highly, while the domestic market was relatively conservative.

'AI application companies are not as highly valued in China. One reason is that domestic tech giants prefer to develop in-house rather than acquire companies,' Hou Jiyong said.

Manus's functionality resembles a cloud-based 'crayfish'

This difference is closely related to the market structures in both regions. In the U.S. market, cases of AI application companies exiting through mergers and acquisitions or high-valuation financing continue to emerge.

For example, AI programming company Anysphere, whose core product Cursor was valued at approximately US$29.3 billion in 2025. The latest industry transaction agreements indicate that its potential acquisition price has risen to US$60 billion.

In contrast, the strategies of domestic AI giants are clearly different.

Taking Tencent as an example, its AI capabilities are primarily advanced through internal systems: launching the Hunyuan large model at the model layer, embedding core applications like WeChat, Tencent Meeting, and Tencent Docs at the product layer, and providing services externally through Enterprise WeChat and Tencent Cloud at the application layer.

Public information shows that Tencent has not disclosed large-scale acquisitions of AI application companies in recent years, instead focusing on self-research and internal integration. Under this model, value is more reflected in internal product and ecosystem synergy rather than achieving premium exits through acquiring external application companies.

Alibaba and ByteDance follow similar paths. Against this backdrop, some Chinese AI application companies have chosen to establish overseas structures and explore overseas exit paths.

However, regardless of policy factors, Manus's specific execution strategy is still considered overly bold.

Conventional AI global expansion in the industry mostly involves business and financing going overseas while retaining domestic R&D bases, data assets, and local entities, balancing domestic compliance with overseas development.

Manus's model, however, represents the industry's most bold 'complete whitewashing-style globalization,' achieving a full-chain relocation: domestic entities, business ports, team entities, equity control, and technological ownership.

Its 'boldness' is mainly reflected in the following aspects:

First, simultaneous entity relocation and control transfer. From a domestic company to a Singaporean entity, and then aligning with a U.S. company acquisition, the company's control underwent cross-border changes in a relatively short period.

Second, overall transfer of teams and technological capabilities.

Hou Jiyong stated that such acquisitions are essentially not based on revenue but on teams and technological capabilities, 'mainly acquiring the team.' In Manus's transaction plan, about 100 core team members were to be fully integrated into Meta.

Third, incomplete separation of data and business relationships.

The core controversy surrounding Manus is that its model's underlying training corpora, data resources, and algorithm iterations were all completed in a domestic environment. Although the company urgently cut ties with domestic businesses, its core technological assets and model foundations were all born domestically.

Fourth, misalignment between the transaction progression rhythm and regulatory approvals.

According to domestic and foreign foreign investment security review rules, such cross-border acquisitions of core AI companies must undergo declaration before the transaction. However, in January 2026, Meta completed large-scale fund transfers and initiated team handover preparations without waiting for regulatory approval results, representing a typical 'execute first, review later' violation.

- 03 - The End of Gray Areas

The first lesson Manus has taught the industry is the complete failure of 'wishful thinking.'

Hou Jiyong believes that the Manus team, 'being relatively young or having wishful thinking,' made the decision to lay off the entire domestic team, relocate the company to Singapore, and then sell it to Meta.

'They did not place concepts like nation, country, or national boundaries in a relatively important position for consideration.'

In his view, Manus originally had another path to take. 'Taking less domestic funding and leveraging algorithmic or other advantages, there was still room for survival amid giant competition—just like DeepSeek, which continuously iterates its model capabilities domestically and gains market space through technological advantages.'

However, after choosing the 'bathing-style globalization' path, the result was difficulties on both ends: facing uncertainty in financing in both the U.S. and China.

Liu Zhishuo also believes that the Manus case is not an isolated event but both a historical inevitability and a systemic transformation. 'In areas involving sensitive technologies and global technological high-ground competition, adopting control measures is an international common practice—the U.S. has been doing this much earlier than us.'

For example, the U.S. has long used CFIUS (Committee on Foreign Investment in the United States) to review cross-border investments involving sensitive technologies. CFIUS took shape as early as the 1970s and strengthened its review of sensitive technologies after 2007.

The reason the previous path of 'domestic R&D, overseas shell swap, foreign acquisition' could work was the existence of a 'gray area,' where regulations were vague, rules unclear, and evasion possible.

In 2025-2026, AI was explicitly included in national security reviews.

The Manus case is a typical example, declaring the disappearance of gray areas: changing the company's registration location does not alter the true ownership of technologies and data, which is based on 'substantive R&D location and actual control' (penetrating review).

For AI companies planning to go global, this means a fundamental change in decision-making: the previous path of 'relocating first and then deciding' is no longer feasible. Any operations involving core technologies, user data, or team relocations must incorporate regulatory frameworks from the outset.

'Rules have shifted from implicit to explicit. No one should have wishful thinking anymore,' Hou Jiyong summarized. 'AI, chips, robots, commercial aerospace, and advanced medical and pharmaceutical industries may all need to follow relevant rules.'

- 04 - Can It Make a Comeback?

Is the termination of the deal a boon or a bane for Manus? Some voices contend that Manus must face the consequences of its decisions and may forfeit the chance for a resurgence.

In an interview, Hou Jiyong expressed that, considering product windows and market competition, Manus can no longer reclaim its former standing.

Manus has wiped out its presence on domestic social media, blocked Chinese IP addresses, and halted domestic services, effectively resetting its user base and ecosystem. Meanwhile, DeepSeek, ByteDance, and others have swiftly enhanced their Agent capabilities domestically, widening the gap.

The latest post on Manus's official Weibo account (as of April 30, 2026)

The latest post on Manus's official Weibo account (as of April 30, 2026)

He noted that since the latter half of 2025, AI applications have rapidly transitioned from 'conversational abilities' to 'task execution,' with a surge of products boasting automation capabilities hitting the market, significantly intensifying competition. This includes rapid growth in AI programming and automated Agents.

Against this backdrop, Manus's opportunity to emerge as a super app has diminished.

Moreover, with escalating uncertainty in similar cross-border transactions, increased turnover within the core team is not unusual. Hou Jiyong stated that signs of team disintegration had already surfaced during the deal's progression.

However, some voices assert that this incident is not entirely detrimental to Manus. "Five to six years ago, I put forth a viewpoint: Nearly any innovative company that attains significant success will inevitably spur institutional innovation," Liu Zhishuo remarked.

In essence, the more profound and disruptive the innovation, the more likely it is to brush against institutional boundaries. In this process, comprehending and adapting to regulatory environments across different countries is becoming an essential skill for entrepreneurs. "Patriotism has also evolved into a necessary skill for entrepreneurs to achieve remarkable success today."

He emphasized that innovation and rules are not adversarial forces but rather exist in a symbiotic relationship characterized by active communication and joint evolution. What entrepreneurs need to achieve is a fundamental shift in mindset. Throughout this process, companies should progress through communication and collaboration rather than confrontation.

From publicly available information, this approach of 'collaborative advancement' is not uncommon among domestic tech companies.

In areas such as large models, autonomous driving, and medical AI, companies typically integrate new technologies into existing frameworks through continuous applications, pilot programs, and compliance-driven progress.

After Manus drew this red line, entrepreneurs have lost one avenue to 'bypass' but gained one that is 'transparent'—advancing innovation through compliant applications and ongoing communication within the existing regulatory framework.

This article does not constitute any investment advice.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!