From Buying GPUs to Competing for Electricity: China's AI Industry Makes a Critical Pivot

05/09 2026

05/09 2026

642

642

By Xiaofeng

Source: Bowang Finance

In late April, China's AI industry reached a watershed moment. The preview version of the domestic large-scale model DeepSeek-V4 officially launched, its 1.6 trillion parameters and million-level context window sparking excitement across the tech sector.

However, what truly rewrote the industry's competitive rules was that 'V4 fully operates on Huawei Ascend chips.' This marked China's top open-source large-scale model officially breaking away from NVIDIA's ecosystem.

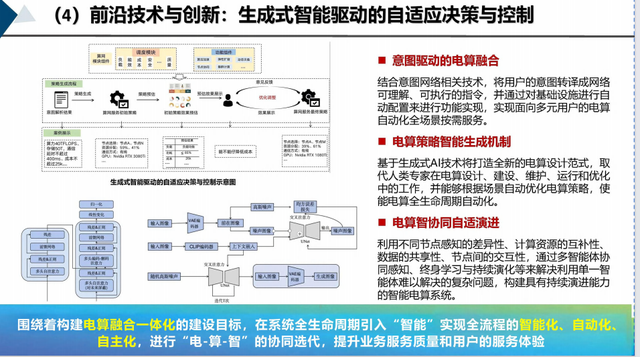

As China achieves self-sufficiency in both models and chips, the main battleground of the global computing power race is irreversibly shifting toward the more fundamental layer of energy supply.

Jensen Huang once proposed the 'five-layer cake theory of AI,' placing energy at the base. This power revolution, triggered by AI computing demand, will not only reshape China's power market supply-demand dynamics and valuation systems but also create a trillion-dollar strategic opportunity spanning the entire chain of power generation, transmission, distribution, energy storage, and digitalization.

01

Repositioning Power Value Under 'Compute-Power Synergy'

DeepSeek-V4's full compatibility with Huawei Ascend is not an isolated technical event.

On the same day, Cambricon completed similar adaptations, while tech giants Alibaba, ByteDance, and Tencent submitted massive orders for Ascend chips, collectively outlining a clear industrial path: China's AI 'model-chip' ecosystem is rapidly closing the loop.

Once this closed loop is complete, the dimensions of competition will fundamentally shift.

Previously, the core of the computing power race was acquiring the most advanced NVIDIA GPUs—essentially a 'renting' model. Now, China's AI industry is 'buying property and settling down' to build its own computing infrastructure.

With a stable foundation, the key to determining how high and stable the building can rise shifts from architectural blueprints (chip design) to land bearing capacity and material supply (energy and infrastructure).

During a debate with moderators, Jensen Huang rarely pointed out China's core advantage: abundant energy. He clearly recognized that China could leverage its massive power system and economies of scale to offset single-card performance gaps by expanding chip clusters.

He even bluntly stated, 'Assuming DeepSeek is optimized for Huawei, that would put us at a disadvantage.' The deployment of DeepSeek-V4 precisely confirms this judgment. The focus of competition is sliding toward the most fundamental layer of energy that Huang mentioned.

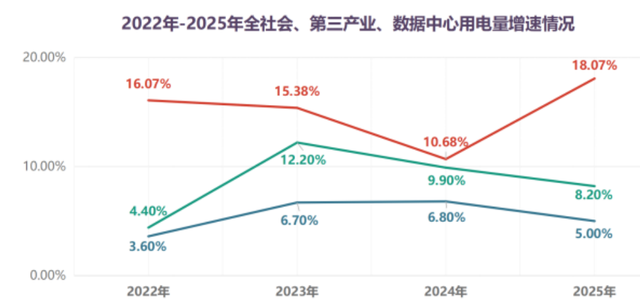

AI data centers are veritable 'electricity guzzlers.' According to industry data, by 2025, China's data centers consumed 193.3 billion kWh, accounting for 1.9% of total societal electricity use, with a year-on-year growth rate of 18.0%.

From January to February 2026, data center electricity consumption growth surged to 46.2%, nearly ten times the rate of total societal electricity growth.

China Merchants Securities' projections paint an even more astonishing future: assuming 5.2% average annual growth in China's total electricity consumption from 2026 to 2030, under different computing power growth scenarios, data centers could account for 2.9% to 6.1% of total electricity consumption by 2030.

This means that over the next decade, AI data centers will become the absolute main driver of growth in China's total electricity consumption.

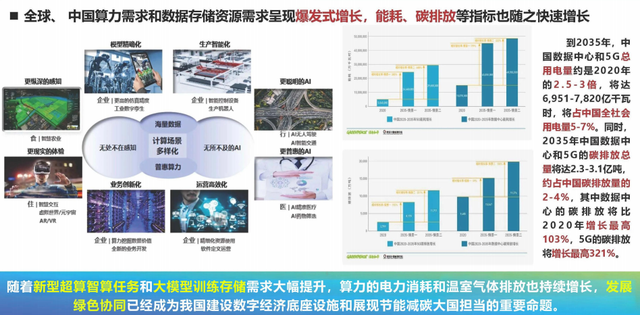

Huawei's 2026 target of shipping 750,000 Ascend chips, along with massive orders from internet giants, corresponds to the establishment of dozens of medium-sized data centers, adding hundreds to thousands of megawatts of new power load, and driving full-chain capacity expansion needs for power grids, substations, energy storage stations, and ultra-high-voltage lines.

The industry's focus is rapidly shifting from 'computing power anxiety'—whether enough chips can be purchased—to 'power anxiety'—whether sufficient, stable, and economical electricity can be provided for these chips.

Moreover, this industrial logic has received strong endorsement from national top-level design.

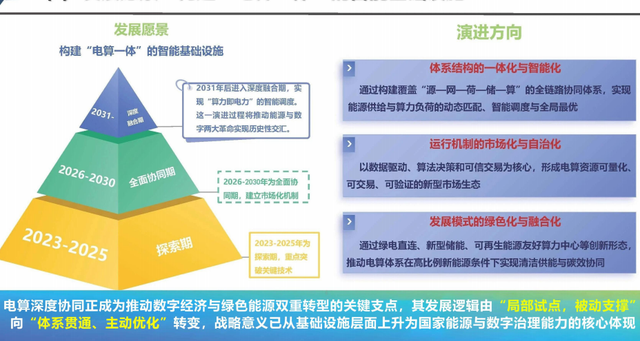

The 2026 government work report explicitly included 'compute-power synergy' for the first time, elevating it to the same level as the 'East Data, West Computing' project as a national-level new infrastructure strategy.

This requires systematically integrating China's resource endowments in wind and solar energy with its globally leading ultra-high-voltage transmission technology, while planning AI industry computing demand and energy power system development in an integrated manner.

By the first quarter of 2026, China's total computing power had reached 3,800 EFLOPS, with intelligent computing power growing at 58.7%—the core growth engine.

Meanwhile, data centers' annual electricity consumption exceeded 200 billion kWh, creating unprecedented demand for 'compute-power synergy' technologies like direct green power connections, smart dispatching, and energy storage peak shaving.

A growing 'scissors gap' between supply and demand is opening up a vast market space. Among the newly approved AI data center energy assessment indicators nationwide in 2025, projects with access to over 80% stable green power resources accounted for less than 30%, while 2026 indicator supplies tightened further.

Under severe supply-demand imbalance, green power resources, grid access capacity, and energy storage peak-shaving capacity—once overlooked factors—are now becoming critical scarce resources determining whether and where an AI data center project can be implemented.

A new energy resource competition has begun, with all orders and value ultimately flowing to power equipment and operation companies capable of providing these solutions.

02

The Main Themes Exploded by AI's Power Demand

The explosion in AI-driven power demand is not uniformly benefiting all power-related companies but is creating structural differentiation.

Value across the power industry chain is being systematically restructured along a clear path: 'ensuring power supply → regulating fluctuations → optimizing management → matching at the source.'

First, primary power equipment and power supply/distribution systems are seeing a RMB 10 billion-scale SST market lead a revolution in power supply architecture.

Huajin Securities estimates that by 2030, domestic AIDC New installed capacity (new installed capacity) will reach 17.7 GW, corresponding to a solid-state transformer (SST) market space of approximately RMB 13.27 billion, with a 2024-2030 CAGR of 64.9%.

When considering Supporting high-voltage direct current (HVDC), Panama power supplies, and AI server power supplies, the total power supply equipment market will far exceed this scale.

The key technology here is solid-state transformers, seen as the ultimate solution for next-generation intelligent computing centers. Their core value lies in boosting system efficiency to 98.5%, achieving single-cabinet power density of 1 MW, and perfectly handling AI load fluctuation rates of up to 50%.

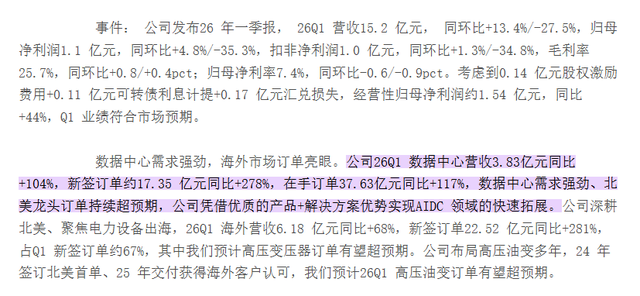

Key companies include Sifang Automation, China XD Electric, Jinpan Technology, and TBEA. The market has begun validating their high-growth logic: industry leader Jinpan Technology saw data center business revenue grow 104% YoY in Q1 2026, with new orders surging 278% YoY and order visibility extending beyond 2027.

Second is the high-voltage direct current (HVDC) power supply system, a key transitional technology evolving toward SSTs with over 96% efficiency. Key companies include Hzh Electric, Kehua Data, and Hopewind Electric.

AI server power supplies must meet higher power density, conversion efficiency, and dynamic response requirements. Key companies include Megmeet, Eurotech, and Aikesaibo.

Next is energy storage systems, shifting from 'optional' to 'mandatory,' with a RMB 100 billion-scale market welcoming strong policy drivers.

According to the 'Special Action Plan for Green and Low-Carbon Development of Data Centers,' by the end of 2025, over 80% of electricity used by newly built data centers in national hub nodes must come from green sources.

Guojin Securities projects 438 GWh of new global installed capacity in 2026, with AI data center energy storage becoming the core growth pole and opening a RMB 100 billion-scale market.

Third is power digitalization and intelligent dispatching, which focus on mining 'algorithmic premiums' in power marketization. Electricity costs typically account for 60-70% of operating center costs.

Soochow Securities estimates that the 2026 compute-power synergy scale could reach approximately 110 TWh, creating vast opportunities for digital services like virtual power plants (VPPs), intelligent power trading, and load forecasting.

VPP platforms aggregate data centers' flexible loads, enabling them to participate as a whole in grid ancillary service markets for peak shaving and frequency regulation. Key companies include GridSolutions, Nanfang Grid Technology, Longshine Technology, State Grid Information & Telecommunication, YGSOFT, and Acrel.

Finally, regarding ultra-high-voltage transmission, as of February 2026, 84 green power direct-connection projects including computing centers had been approved nationwide, with 32.59 GW of new energy installed capacity—indicating sustained growth in UHV/flexible DC transmission construction.

Key companies include traditional power transition firms like Jinkai New Energy, Yunneng Holding, and GCL-Poly Energy, as well as green power operators like Fuling Electric Power.

03

Industrial Coordinates and Growth Logic Through Cycles

As 'compute-power synergy' moves toward large-scale implementation, low-cost green electricity gives China's AI models global competitiveness: million-token invocation costs ($0.5-1.5) are far lower than European and American competitors (European and U.S. counterparts) ($2.5-10).

This enables 'power stays within borders, computing value crosses borders' as a new form of trade. The following five leading companies occupy core links from green power sources to end-user terminals, making them the most direct beneficiaries of this trend.

First is Jinpan Technology, whose Q1 2026 data center business revenue grew 104% YoY, with new orders surging 278% YoY and order visibility extending beyond 2027.

The company's leading solid-state transformer (SST) solution achieves 98.5% efficiency, becoming standard equipment for next-gen intelligent computing centers. The 104% revenue growth and 278% order surge in Q1 reflect not industry beta but alpha from its technological leadership translating into market exclusivity.

The company has deep bindings with top internet and intelligent computing clients, serving as a 'shovel seller' to first capture industry dividends with strong growth certainty.

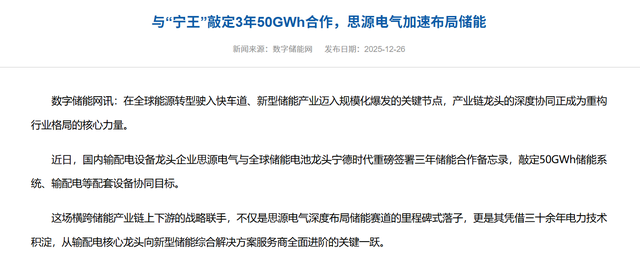

Second is Sieyuan Electric, which signed a 2026-2028 strategic cooperation agreement with CATL for 50 GWh of energy storage business, locking in massive future demand.

This directly quantifies the energy storage market space created by AI data centers and proves the company's absolute leadership in large-scale energy storage system integration. The agreement ensures high growth floors for the company's future performance, making it one of the most certain beneficiaries of 'compute-power synergy' policy dividends.

Third is Longshine Technology, whose AI-powered electricity trading products benefit from deepening market reforms. Leveraging its deep grid-side expertise, the company's 'Jiugong' AI electricity trading agent successfully serves large power users.

As the national unified power market accelerates, demand for such digital, productized services will grow exponentially. The company's business model is shifting from project-based to product-based, featuring high margins and strong customer stickiness—a rare asset in the power digitalization track (sector).

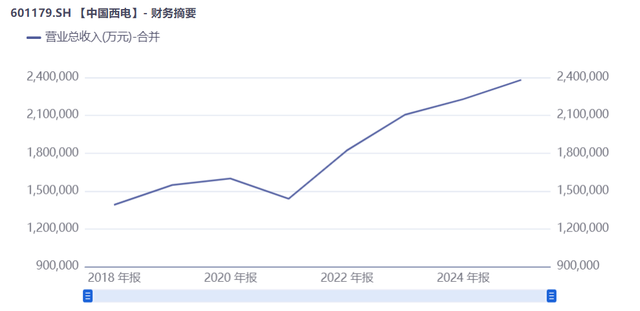

Fourth is China XD Electric, a main force in UHV construction benefiting from accelerated green power transmission channels. By February 2026, 84 green power direct-connection projects had been approved nationwide, with 32.59 GW of new energy installed capacity—indicating a new round of construction peaks for UHV and flexible DC transmission projects.

As a core national team member, the company's orders and performance will steadily release with accelerated grid investment, featuring high growth certainty.

Finally is Megmeet, a core AI server power supplier whose Q1 power business revenue surged 66.52% YoY. It has become NVIDIA's sole AI server power supplier listed in A-shares, securing bulk orders for GB300 power supplies.

Its Vera Rubin architecture power supplies have also been sent for testing to top North American cloud providers. Soochow Securities reports that the company's AI server power market share in NVIDIA racks could exceed 10% by 2026.

04

Conclusion: Value Reassessment at the Eye of the Storm

Looking back at April 2026, capital markets cheered breakthroughs in domestic chips. However, more profound industrial transformations were unfolding after powering up those chips.

For investors, this is no longer a story about cyclical fluctuations but one about growth and scarcity.

The companies providing the most fundamental, solid support for China's computing power—beneath UHV towers, inside energy storage stations, and within smart grid control centers—are standing at the peak of a massive wave shaped by both technological revolution and national strategy. The eye of the storm has formed, and value reassessment may have only just begun.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!