BBA's Final Stand

05/09 2026

05/09 2026

572

572

Edited by Sun Jing

BBA, long considered the stalwarts of the luxury car market, are now under unprecedented pressure.

Domestic newcomers are making a full-fledged push into the high-end market with a slew of '9-Series' flagship models.

In recent years, BBA's pure electric vehicle (EV) endeavors have faced hurdles: price reductions have had limited impact, brand prestige has diminished, and some consumers now dismiss them as just another 'generic EV.' Meanwhile, new players are swiftly redefining luxury car value standards with intelligence, comfort features, and localized experiences.

Faced with a surge of new competitors, BBA no longer concerns itself with whether their successors are 'paying homage' to luxury car designs and has begun adopting similar strategies—ranging from extended wheelbases, 800V high-voltage systems, and ultra-long ranges to localized smart cockpits, 'fridge-TV-sofa' configurations; and from 'fixed pricing' models in their sales systems to even exploring range-extender technologies they once disdained.

Moreover, at the Beijing Auto Show in April this year, the three brands chose Beijing as the global launch site for their latest, core pure EV models.

To some extent, by 2026, BBA has finally grasped the fundamentals of EVs and is entering an offensive phase.

However, in a market where the rules have been rewritten, merely catching up to the average level may not suffice to maintain their former standing.

01

BBA's Pivotal Year of Transformation

The past two years have been tumultuous for BBA.

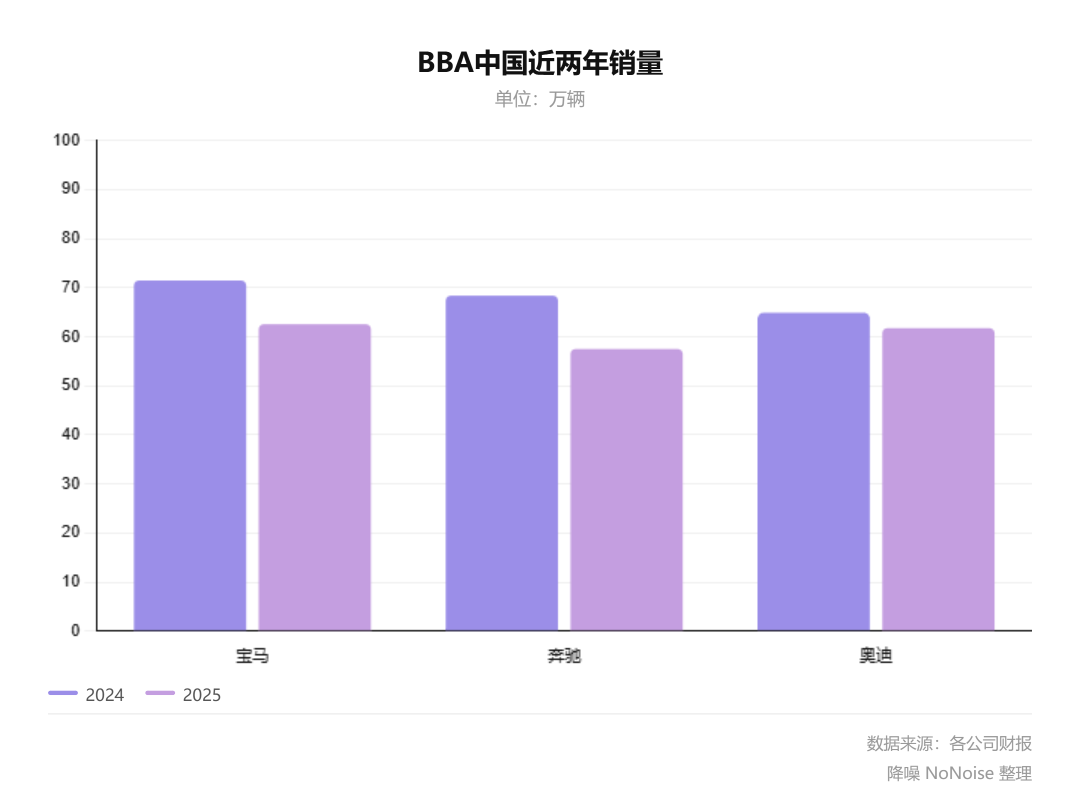

Starting in 2024, BBA's China sales have collectively declined. By 2025, Mercedes-Benz China sales fell 19% year-on-year to 575,000 units; BMW to 625,500 units, down 12.5%; and Audi to 617,500 units, down 5%. Their overall sales plummeted to levels not seen in seven or eight years.

The downward trend accelerated in the first quarter of this year.

The situation is even more precarious in the new energy market. Among the top 10 best-selling pure EV models priced above 300,000 yuan in 2025, newcomers like NIO, AITO, and Li Auto dominate, while BBA is conspicuously absent.

The reasons are straightforward: BBA's EV product competitiveness has long lagged—early attempts to 'retrofit combustion cars into EVs' resulted in inherent flaws in spatial layout, range performance, and intelligent experiences.

Faced with newcomers' strategy of 'large quantities and satisfying features' paired with 'high specs at low prices' or even market-share-at-all-costs pricing, BBA's brand advantages quickly eroded.

After setbacks with the Audi e-tron series, Mercedes-Benz EQ series, and BMW i series, BBA gradually came to their senses.

First, they bid farewell to 'retrofitting combustion cars into EVs.' After various setbacks, all three launched truly new pure EV platforms.

In product design, BBA has adopted a 'if you can't beat them, join them' approach, using newcomers' tactics against them—such as focusing on smart cockpits, ultra-long ranges, extended wheelbases, and 'fridge-TV' configurations.

Behind this lies BBA's full embrace of the Chinese ecosystem, from R&D and supply chains to ecological cooperation.

▲Chart by NoNoise

Specifically, the three brands are progressing at different paces.

BMW is gearing up for launch.

Currently, BMW's pure EV i series sold in China are based on the CLAR combustion car platform, relying mainly on 'pricing for volume.' For example, the BMW i3 once dropped below 200,000 yuan.

BMW's bet, the 'Neue Klasse' platform, will reach a critical delivery phase in 2026. BMW will launch the pure EV iX3 long-wheelbase and pure EV i3 long-wheelbase models in China, built on the 'Neue Klasse' platform, with plans to launch in the second half of the year.

The new models feature extended wheelbases tailored for China, with CLTC ranges exceeding 900 km and 1,000 km, respectively. They integrate BMW's sixth-generation eDrive technology and other in-house tech, while collaborating with local tech firms like Huawei, Alibaba, and Momenta to develop smart cockpits and assisted driving systems.

Audi is fighting a last-ditch battle.

Audi is 'fighting on two fronts': one is the FAW-Audi 'Four Rings' system, relying on the PPE pure EV platform and emphasizing traditional luxury quality; the other is the new 'AUDI' brand launched by SAIC Audi, actively embracing intelligence and youthfulness.

In 2025, Audi launched the Q6L e-tron and E5, but due to pricing and brand perception issues, both models underperformed in sales, with cumulative six-month sales of just over 6,000 units each.

For Audi, 2026 has become a critical year to validate its transformation. Currently, the Audi A6L e-tron and Q6L e-tron family are rolling out new models, while the E7X is targeting the large luxury pure EV SUV market.

In terms of intelligence, Audi's PPE platform models feature Huawei's ADS with urban NOA functions; the AUDI brand jointly developed an intelligent driving system with Momenta, specifically trained for China's complex road conditions.

As for Mercedes-Benz, the EQ series retrofitted from combustion car platforms has gradually been marginalized. By late 2025, Mercedes-Benz launched the pure EV CLA based on the new MMA platform; in 2026, it will roll out six EV models, including the pure EV GLA, C-Class, and GLC.

Among them, the Mercedes-Benz pure EV GLC is seen as 'a product clearly larger and closer to China's mainstream market.' Its wheelbase is extended to 3,027 mm, offering a six-seat layout for the first time; its intelligence suite integrates an assisted driving system jointly developed with Momenta and a cockpit AI assistant powered by ByteDance's Doubao large model.

However, current market feedback suggests that winning in the second half of the new energy era requires more than just 'copying homework.'

02

Desperate Need for a Blockbuster Model

This spring, a string of resignations among BBA's China executives underscores how desperately the German luxury trio wants to reinvent themselves in China.

BBA once set ambitious goals for their EV transformation, but in reality, product definition remains controlled by German headquarters, while the dealer system is slow to adapt to market changes in China.

Admittedly, in the market segment above 300,000 yuan, pure EV penetration has not yet formed an overwhelming advantage, with many consumers still choosing combustion cars, hybrids, or range-extenders.

However, with shortened automotive R&D cycles and declining supply chain costs, profit margins in the low-to-mid-end market are thinning, prompting many new energy manufacturers to charge into the high-end market collectively.

This year, a wave of '9-Series' models has flooded the market, making large new energy SUVs the most crowded battleground in the industry.

▲Chart by NoNoise

Faced with competitors' saturation attacks, BBA's defense has become tougher. The competitive landscape in China forces BBA to deliver in the pure EV space.

For automakers seeking a quick turnaround, launching a flood of new models is a suboptimal strategy; creating blockbusters is the way to go. For example, the SU7 made Xiaomi Motors famous; the all-new ES8 became NIO's comeback hero; XPENG emerged from crisis with the MONA M03 and P7+; and Li Auto's i6 'saved the day,' completing its low-to-high rise in the pure EV segment.

These blockbusters each have their unique value propositions, whether it's unexpected cost-effectiveness or product definitions that resonate with niche audiences. For instance, the all-new ES8, with over 100,000 units sold, not only priced lower than its predecessor but also dropped the luxury car price to 298,800 yuan through a battery-leasing model.

▲NIO unveils the all-new ES8 Aurora Gold Special Edition at the Beijing Auto Show

From currently available information, even after mastering the fundamentals of the EV era, BBA's products still lack 'blockbuster potential.'

Take BBA's three newly launched EV models last year as examples:

The core issue with the Audi E5's underperformance lies in the disconnect between its product design and user perception.

Despite Audi's efforts in chassis tuning and brand design, the E5 shares many core components with the IM L6, leading to accusations of being a 'rebadged IM.' With a significantly higher starting price than the IM L6, this 'same quality, higher price' approach deterred some consumers.

The Audi Q6L e-tron's poor sales stem from mismatched pricing and product strength.

Built on the PPE pure EV platform and equipped with Huawei's ADS system, it offers a range of 668-672 km. However, in today's Chinese market, its core selling points heavily overlap with models like the NIO ES6 and Tesla Model Y; while it introduced Huawei's intelligence solution, its overall strategy remains conservative, with limited urban NOA coverage and a less localized infotainment ecosystem than newcomers.

Priced at 348,800-398,800 yuan at launch, competing newcomer models offered more complete core configurations at similar prices.

Ultimately, Audi resorted to its familiar tactic—price cuts. By April 2026, the Q6L e-tron's refreshed version started at 269,800 yuan.

▲Weibo comments under Q6L e-tron-related posts

The Mercedes-Benz pure EV CLA, launched in November last year, faces a similar dilemma.

Dubbed by Mercedes-Benz CEO Ola Källenius as 'ushering in a new era for Mercedes,' it sold 1,369 units in its debut month but only 21 units domestically in February this year.

Mercedes-Benz poured nearly all its understanding of next-gen EVs into the pure EV CLA—800V high-voltage architecture, 320kW fast charging, 866 km range, and ultra-low energy consumption of 10.9kWh/100km...

▲Pure EV CLA China launch party on November 5, 2025

On paper, the specs look impressive. But the problem is, 800V architectures are now standard in EVs priced above 200,000 yuan in China; while the CLA has advantages in range and energy efficiency, they're not enough to create a generational gap.

More critically, today's Chinese new energy market sells far more than just specs. For example, Tesla owns the 'pioneer of EVs' brand perception, Xiaomi leverages its 'human-car-home ecosystem' and online influence, and Li Auto is known as the 'family car,' appealing to middle-class households.

Every player is trying to define its unique label.

Conversely, BBA's EVs now face the awkward issue of seeming increasingly ordinary.

03

A Last-Ditch Battle

We surveyed owners who bought BBA's newly launched models last year and found their purchasing reasons mainly centered on chassis quality, product reliability, etc.

Mr. Wei, who replaced his AITO M7 with an Audi E5 sedan last October, was aware of the similarities between the E5 and IM L6 but chose the Audi for its superior chassis damping over bumps like manhole covers, offering a better driving experience—worth the 50,000 yuan premium.

Ms. Gloria, who traded her 10-year-old BYD Qin EV for an Audi Q6L e-tron in January, trusts traditional automakers' 'safety.' She believes century-old brands better understand assembly quality, safety redundancy, and long-term reliability.

However, among broader consumer groups, BBA's brand perception has become severely fragmented.

According to McKinsey's 2025 China Automotive Consumer Insights Report, while German luxury brands maintain high recognition in the combustion car market, their brand premium acceptance in the EV market has declined significantly. About 50% of consumers explicitly stated they would not pay extra for

The A6 series has consistently stood as the cornerstone of FAW-Audi's sales strategy. Presently, with the pricing of the A6L e-tron closely mirroring that of its fuel-powered counterpart, the A6L (priced between RMB 322,900 and RMB 435,900), there looms a potential for market cannibalization between the two models. Furthermore, this price bracket also encompasses competitors such as the Mercedes-Benz EQE, BMW i5, Xiangjie S9, and NIO ET7.

Following the revamp of the Audi Q6L e-tron lineup, prices now span from RMB 269,800 to RMB 419,800, markedly reducing the threshold for entry compared to its predecessor. Noteworthy additions include the quattro ADS variant and a long-range version, bolstering both all-wheel-drive and assisted driving functionalities. Its rivals in the market include sought-after models like the NIO ES6 and Seres M7.

SAIC-Audi is set to unveil its inaugural all-electric SUV, the Audi E7X, this year, with industry insiders projecting its price to fall between RMB 300,000 and RMB 400,000, thus directly penetrating the mainstream luxury all-electric SUV sector. This market segment underscores the importance of holistic competitiveness, with lateral competitors including models such as the Tesla Model Y and NIO ES6.

▲The Audi E7X makes its debut at the Beijing Auto Show.

Mercedes-Benz has slated the launch of six models for this year, encompassing the all-electric GLC, all-electric C-Class, all-electric VLE, refreshed EQS sedan/EQS SUV, and all-electric GLA.

The all-electric C-Class shoulders the crucial responsibility of facilitating Mercedes-Benz's transition from a combustion engine system to an electric one. However, venturing into the mid-size all-electric sedan market, it not only contends with the BMW i3 but also faces stiff competition from established players like the Tesla Model 3, which have long held sway over market perceptions.

Within this price spectrum, consumers typically seek a well-rounded balance of range, space, charging efficiency, and smart experience. Mercedes-Benz must demonstrate its prowess not merely as an 'electric vehicle from a luxury brand' but as a genuinely competitive offering.

The all-electric GLC epitomizes Mercedes-Benz's resurgence in the luxury all-electric SUV arena. This marks the first instance where Mercedes-Benz has integrated flagship-level chassis capabilities into a pure electric platform within the mid-size SUV segment. From a competitive vantage point, the all-electric GLC will go head-to-head with the aforementioned BMW new-generation iX3 and Audi Q6L e-tron.

▲The Mercedes-Benz all-electric GLC showcased at the Beijing Auto Show. Photo credit: Liu Shiyu.

In essence, the battle for supremacy among BBA (Benz, BMW, Audi) will be no easy feat. The automotive brand landscape has entered a phase of consolidation, and as NIO's founder, William Li, recently remarked, 'The competitive edge in the automotive industry often hinges on a mere 3-5 percentage points, where even the slightest differential can spell the difference between success and failure.'

Whether BBA can capitalize on its brand equity and systemic strengths to solidify its position and strive for breakthroughs, 2026 may well prove to be a pivotal juncture.

-

![]()

Total Investment Hits Nearly 3.28 Billion! Goertek Launches Mass Production of 12-Inch Transparent Substrate Wafer for AR Glasses’ Micro-Nano Optical Components

-

![]()

Why Is This Precision Optical Film Leader Worth Reevaluating with a Tens of Millions Procurement?

-

![]()

AI Costs Plummet by 90% Over Nine Years: Key Insights from Davos You Shouldn’t Miss

-

Doubao, Your Late-Night AI Companion, Now Eyes Profitability

-

![]()

SRC Empowers SEER Intelligence to Reach a Market Cap of Tens of Billions, Yet Fails to Sustain Profitability

-

![]()

China’s Embodied AI Industry Faces Fierce Domestic Competition, Making Overseas Expansion Essential for Survival

-

![]()

32.8 Billion Yuan Investment! Goertek’s 12-Inch AR Glasses Optical Wafer Base in Lingang Begins Operations

-

![]()

How Far is the All-New Li Auto L8 from Being the Best Five-Seat SUV with In-House Full-Stack Development?