Google Sets a Benchmark for Chinese AI Enterprises

05/09 2026

05/09 2026

532

532

From the close of last year up to now, the idea of an 'AI bubble' has become a hot topic in the investment community. This is due to worries that companies' aggressive investments in AI infrastructure might diminish significant profits in the near term, with depreciation costs alone posing a substantial financial strain. Whenever companies unveil major investment strategies, the AI sector typically celebrates, yet stock prices often fluctuate rather than consistently climb.

As you may remember, since late last year, discussions about the 'AI Bubble' in major global financial media outlets have surged, which has, to some extent, shaped the perspectives of Chinese tech firms. For instance, Tencent mentioned in its Q2 2025 earnings call that it would actively invest in computing power. However, by Q3, its capital expenditures were notably lower than anticipated by the market, mainly due to concerns over maintaining ROI.

So, is there an AI bubble in the short run? Google in the U.S. has already begun to offer some insights.

Let's briefly recap the highlights from Google's Q1 2026 financial report:

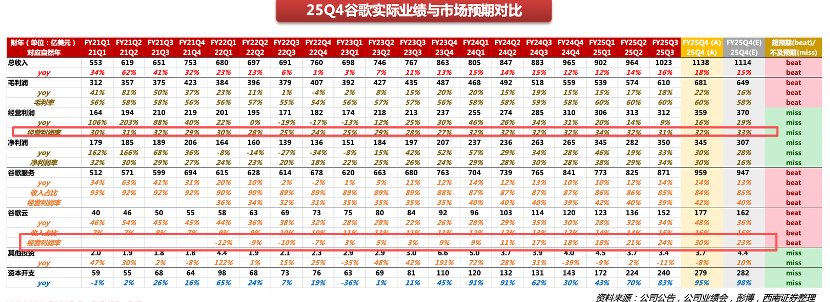

Total revenue soared to $110 billion, with net profit reaching $62.6 billion, both surpassing analysts' forecasts;

Significant investments in the AI sector are yielding results, with enterprise-level AI solutions and demand for computing power fueling cloud business expansion. The company reported that its cloud business backlog jumped from $240 billion in the previous fiscal quarter to $460 billion;

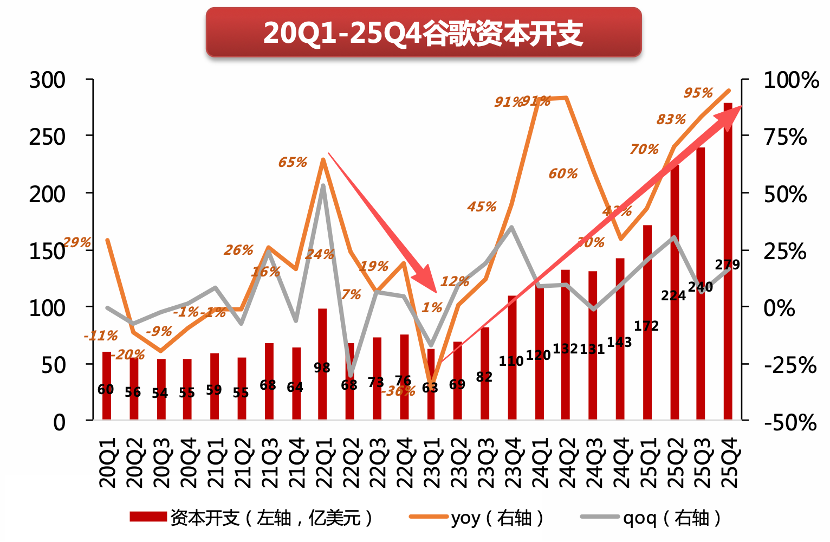

Full-year capital expenditures are projected to be revised upwards from $175-$185 billion to $180-$190 billion.

It's safe to assert that an AI bubble has not emerged at Google, and the likelihood of an AI bubble among leading U.S. tech firms is quite low.

Prior to 2023, the allure of U.S. tech companies began to wane, with growth rates plummeting. Google's capital expenditures also ceased to grow, and the entire sector largely adopted a 'wait-and-see' stance (akin to the situation faced by Chinese tech firms during the same period).

After ChatGPT successfully implemented large language model technology, the business community quickly took notice, rapidly catching up technologically with large language models on one hand and immediately boosting capital expenditures to stockpile computing power and reconstruct competitive advantages on the other.

Google's capital expenditures in 2025 were nearly triple those of 2022, yet its operational efficiency improved rather than declined.

Over the past three years, operating profit margins across various business segments have significantly risen, indicating that the depreciation costs from substantial investments have not adversely affected the income statement. The AI bubble theory appears somewhat overblown when applied to Google.

So, what has Google done correctly?

Previous market discussions have primarily centered on Google's 'full-stack AI technology strategy': Google's AI business encompasses everything from chips (TPUs) to models (Gemini) and numerous applications, representing a comprehensive approach that leverages technology to safeguard its business moat, making Google Cloud a growth engine once again in the AI era.

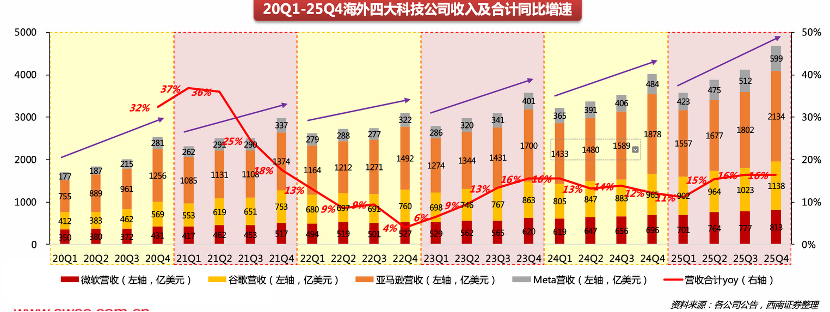

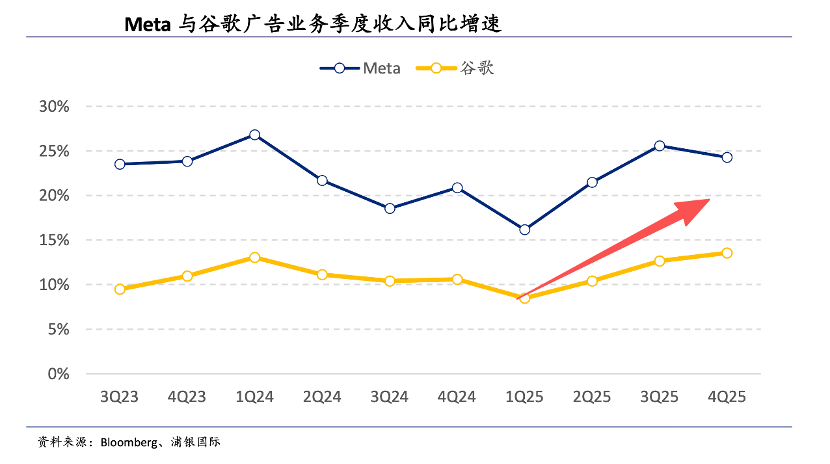

This perspective is logically sound and empirically supported, which is understandable. However, paradoxically, Google's search advertising revenue has also experienced a 'renaissance.' In Q1 2026, Google's search and other revenues surged by 20% year-on-year to $60.4 billion. Previously, there was a widespread belief that large model tools would diminish the importance of search, with users shifting their information acquisition channels (a trend notably evident with Baidu). But why has Google's search advertising not declined but instead increased?

We can explore reasons both externally and internally:

External factors: Overseas large models predominantly adopt a subscription-based pricing model (free models often come with limitations and cannot utilize the optimal models), which contrasts sharply with the primarily free C-end large model operation strategies in China. For users, search remains the premier free channel for obtaining information;

Internal factors: Following substantial investments in the AI sector, the company's product capabilities have been comprehensively enhanced, boosting the precision and efficiency of advertising. Advertisers have started to flock back to Google. In this context, AI is not merely a standalone chat tool but a comprehensive lever for optimizing corporate operations.

At this juncture, some may still be puzzled: Why has Baidu's search advertising performed so poorly amid the same AI transformation? Apart from the fiercer competition among C-end large models in China, the primary reason lies with Baidu itself.

Unlike Google, which still relies on global web pages as information sources, Baidu Search predominantly depends on Baijiahao content, which not only leads to inconsistent search quality but also easily taints AI output with low-quality content (as highlighted on the 315 Gala). Therefore, while Google's AI Overview may be a boon, Baidu's situation is markedly different. Baidu's current state can be attributed to a confluence of factors.

While the outside world continues to debate the AI bubble, Google's stock price has hit an all-time high.

Google's profitability narrative offers inspiration for Chinese concept stocks: the market is not primarily concerned with the magnitude of investments but whether ROIC (Return on Invested Capital) can be sustained (Google's ROIC remains above 30%). Currently, the AI investment approach in the U.S. capital market is also evolving, with a focus on maintaining strategic allocations to computing power and infrastructure while increasing the emphasis on software and platform companies that have demonstrated AI monetization capabilities.

Drawing from the U.S. market, Chinese concept stocks are likely to follow suit. Which companies do you favor?

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!