Will Qianwen Follow in Doubao's Footsteps and Implement ROI-Based Charging?

05/09 2026

05/09 2026

581

581

Doubao is gearing up to introduce user fees: Alongside a free version, it plans to roll out several paid tiers, with monthly subscription fees set at 68 RMB, 200 RMB, and 500 RMB. Following this announcement, numerous individuals approached me for discussions, primarily focusing on two key questions:

1) While it's evident that Doubao needs to charge due to the computational expenses involved, how substantial can the revenue actually be?

2) Should the charging model prove successful, what implications will it have for the industry landscape?

Viewing Doubao as a standalone entity, its current app boasts over 300 million monthly active users. In March of this year, it processed 120 trillion Tokens daily, incurring electricity and hardware costs alone of 200-400 million RMB per month (including amortization and R&D expenses, monthly outlays could reach 500-900 million RMB). According to Volcano Engine data, these figures are projected to double every three months.

If Doubao were to remain entirely free, its annual expenses could conservatively range from 15 to 20 billion RMB. Given ByteDance's emphasis on return on investment (ROI), this is not a sustainable long-term strategy.

So, what financial prospects can we anticipate for Doubao post-charging?

Guolian Minsheng has developed a predictive model, which we present below:

As of March 2026, Doubao had approximately 345 million monthly active users, with an average of 54.8 uses per user in the first quarter. Assuming a payment rate akin to ChatGPT's (~5.6%), Doubao could potentially have around 19.3 million paying users. Drawing from GPT's subscription structure (90% low-tier, 8% mid-tier, 2% high-tier), Doubao's weighted average revenue per user (ARPU) would be approximately 87.2 RMB/month, translating to an annualized revenue of around 20.2 billion RMB.

From an ROI standpoint, if Doubao manages to keep the average monthly inference cost per paying user between 25-50 RMB, the "revenue/inference cost" ratio would range from 1.8 to 3.5 times.

Considering the relatively low payment willingness among Chinese users, these figures should be viewed with caution. A conservative estimate for annualized revenue would be around 15 billion RMB, which could largely offset the previously estimated operational losses. If all proceeds as planned, Doubao's ROI could reach break-even by then.

So, why is Doubao implementing charges now?

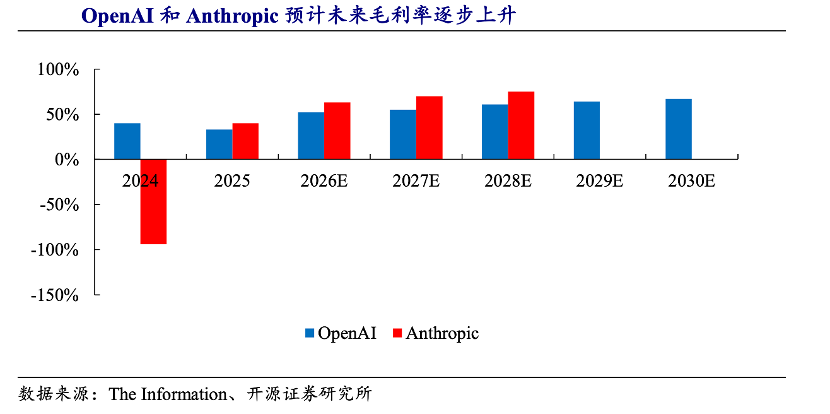

Let's examine the examples of OpenAI and Anthropic across the ocean. The former primarily targets C-end users, while the latter focuses on B-end clients.

While OpenAI deserves recognition for popularizing large language models, its commercialization journey has been tumultuous. Not only has its annual recurring revenue (ARR) growth trailed behind Anthropic's, but its gross margin gap with Anthropic has also widened. In 2025, OpenAI's performance fell short of management expectations.

Beyond well-known factors such as "OpenAI's broader research scope (encompassing multimodal, hardware, search, etc.)" and "significant investment in backup servers," the primary issue lies in market positioning:

User demographics differ. Anthropic primarily serves B-end enterprises, where maintaining free users is relatively cost-effective. In contrast, OpenAI has a substantial free user base (with only 5% paying).

In the realm of large language models, while numerous companies abound, those targeting TO C generally lag behind TO B counterparts in terms of operational quality. The latter inherently enjoy lower costs, higher growth rates, and stronger profitability.

With this industry backdrop in mind, let's analyze Doubao through two key data points.

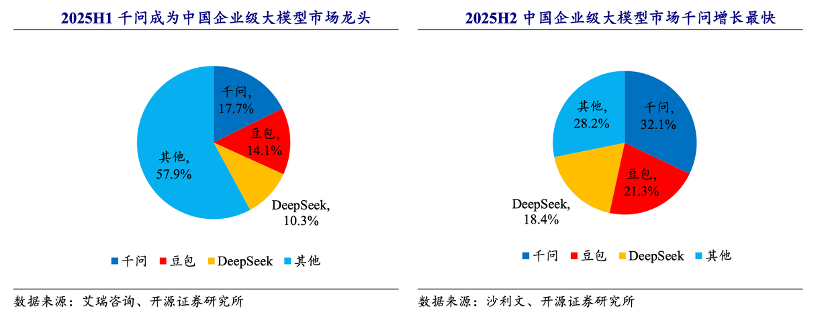

The above data from Frost & Sullivan only accounts for enterprise clients directly utilizing large model APIs (excluding internal use by cloud providers and resale/agency). While Doubao's market share increased in the second half of 2025, its gap with Qianwen widened.

However, IDC data (encompassing Doubao API + internal usage + some resale to partners) indicates Doubao's market share for the same period at 49%.

These conflicting statistics reveal two insights: Doubao's App excels on the C-end, and ByteDance provides substantial support. Nevertheless, its external market penetration lags behind that of rival Qianwen.

This suggests that subsidizing C-end free models with high-margin B-end profits (akin to Anthropic) is not a viable short-term strategy for Doubao. The stronger the C-end presence, the greater the burn rate.

Doubao's decision to implement charges now stems partly from market exploration but is primarily driven by financial necessity.

Regarding the future industry landscape, two key points emerge:

Doubao's charging model aims to offset losses, but AI giants with robust B-end revenue streams (like Alibaba Cloud) possess greater financial tolerance for C-end operations. If competitors delay or reduce charging, can Doubao maintain its C-end market share?

Doubao has undoubtedly conducted rigorous financial calculations for this move, targeting ROI break-even. However, acting prematurely may provide competitors with more strategic options. Whether this constitutes a strategic misstep remains to be seen—we will continue to monitor the situation.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!