Doubao Introduces Charges: Fewer and Fewer Purely Free Large Models

05/11 2026

05/11 2026

461

461

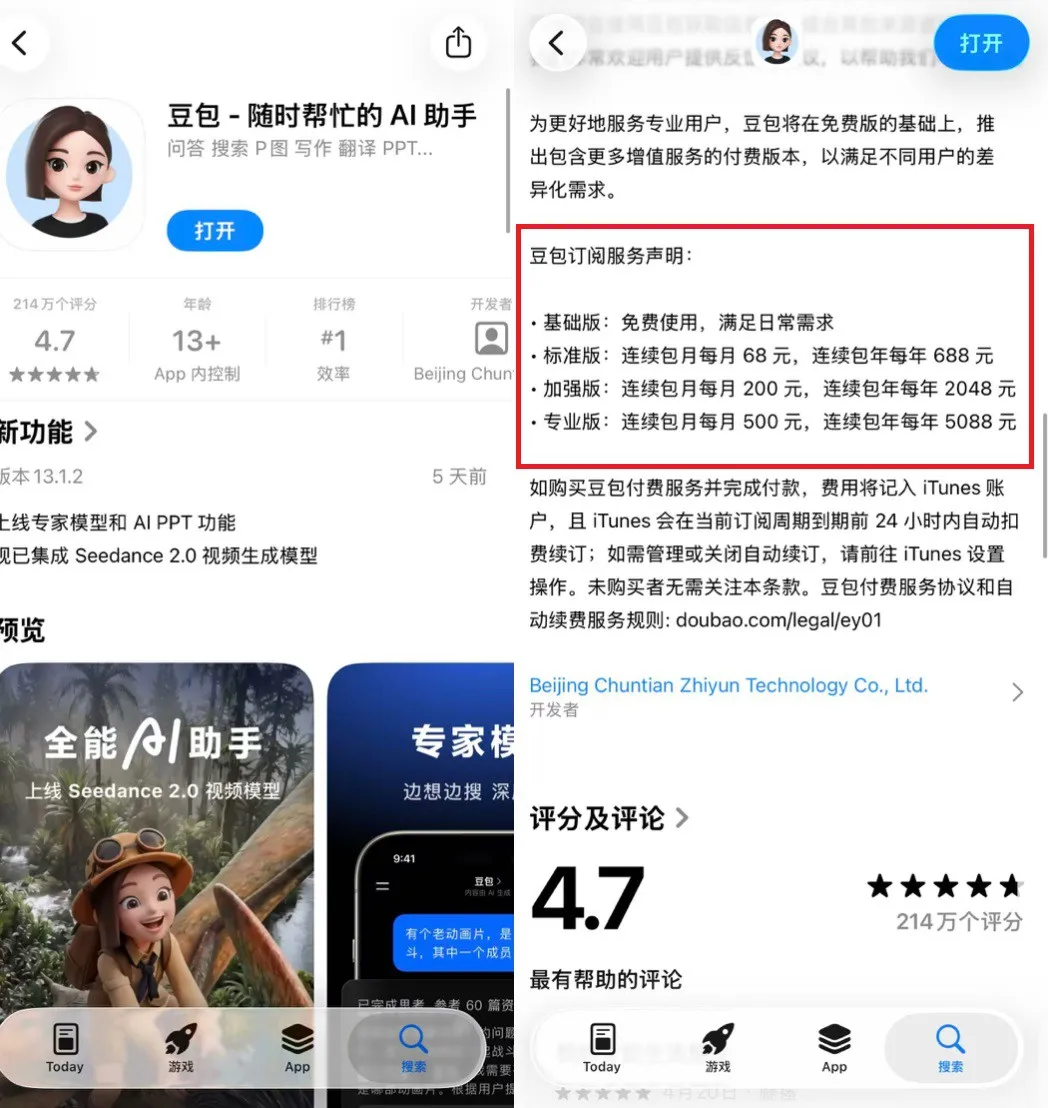

On May 4, 2026, Doubao, an AI product under ByteDance, quietly updated its paid subscription plan on the Apple App Store. With three pricing tiers—Standard at 68 yuan/month, Enhanced at 200 yuan/month, and Professional at 500 yuan/month—these options sent three clear signals, ending two years of 'free extravaganza' in China's AI large model industry.

Image Source: Internet

This is not just an ordinary business move. Doubao, backed by 350 million monthly active users as China's top AI-native application, signifies something bigger with its commercialization. When the player with the largest user base starts seriously considering how to extract money from users' pockets, the rules of the game for the entire industry are undergoing a fundamental transformation.

On Weibo's trending topics, skeptics and supporters are divided.

One faction is resolute, stating bluntly, 'I'll uninstall it if it charges,' and questioning Doubao's current functionality and user experience. The other camp is relatively calm, pointing out that overseas AI products have long implemented tiered services, and China is merely catching up with international practices. They emphasize that high-intensity AI services come with high resource consumption, and a reasonable pricing system is conducive to the healthy development of the industry.

The official promises to permanently retain free basic services, but paid features will target complex productivity scenarios such as PPT generation, data analysis, and film and television production—areas that are major consumers of computing power and where AI is heavily applied.

Image Source: Internet

Doubao's move to charge is not an isolated event but an inevitable choice for China's AI large models to shift from traffic expansion to value realization. Over the past two years, major players have used free or even subsidized models to acquire users and relied on capital narratives to support technological iteration. However, when usage scales into the billions, computing expenses transform from 'tolerable investments' into 'structural costs that cannot be ignored.' The industry must confront a harsh question: Is this the prelude to exploiting users, or a true reflection of the large model dilemma?

A New Competitive Landscape Has Emerged

As of May 2026, China's large model market has evolved from a 'hundred-model battle' into a stable pattern (pattern) of 'ecosystem-led giants + breakthroughs by tech newcomers,' with a pronounced head effect (winner-takes-all effect).

Internet Giants (Ecosystem-Based): Alibaba's Tongyi Qianwen (strong in open-source and B2B, with ~32.6% market share), ByteDance's Doubao (C-end traffic leader, with DAU exceeding 100 million), Baidu's Wenxin (search and knowledge-enhanced), Tencent's Hunyuan (social and multimodal). They rely on traffic, cloud infrastructure, and capital to build high barriers.

Image Source: Internet

Independent Tech Vendors (Specialized): DeepSeek (ultimate cost-effectiveness and open-source, with soaring valuation), Moonshot AI's Kimi (long-text and C-end experience), Zhipu AI (academic background and GLM series), MiniMax (multimodal and character AI). They often enter through technical strengths or specific scenarios.

Among the newcomers, Zhipu AI and MiniMax took the lead in listing on the Hong Kong Stock Exchange, both claiming to be the 'world's first publicly traded large model company,' with market caps reaching HK$411.5 billion and HK$257.3 billion, respectively. While these valuations are not low, they now require financial performance to justify them. For example, Zhipu AI has verifiable financial metrics, with over 240,000 paid developers and a 60-fold increase in ARR (Annual Recurring Revenue) from localized deployments for financial institutions and government units. In 2026, MiniMax is experiencing rapid growth. According to recent disclosures, its ARR surpassed $150 million in February 2026, and the daily Token consumption of its M2 series text model increased more than sixfold from the end of 2025, indicating high user stickiness and business activity.

Image Source: Internet

The only exception in this group is DeepSeek, which, despite not publicly disclosing revenue, commands a valuation in the 300 billion range due to its potential as a 'definer.' Its V3, R1, and V4 models have established a technical brand in the global open-source community. The V4 model's compatibility with domestic chips (Huawei's Ascend 950PR) has paved the way for 'independence + open-source + domestic computing power adaptation.' While companies like Meituan are also training trillion-parameter models from scratch using domestic chips, DeepSeek holds a first-mover advantage in domestic chip adaptation validation, industry standard co-creation, and open-source ecosystem implementation.

Image Source: Internet

Despite their advantages in traffic, technology, and cost, giants still face challenges in commercialization. No matter how compelling the AI narrative is, the marginal costs of large models continue to rise, with each conversation consuming expensive computing and electrical power—a money-burning game that is ultimately unsustainable.

Internet commercialization once relied on the 'three engines' of value-added services, advertising, and e-commerce. However, in the AI industry, value-added services may be the most fitting commercial approach. By first accumulating users and cultivating habits for free, then monetizing through tiered services, this classic commercialization path is now playing out in the large model sector.

The Commercialization of Large Models Faces a Major Test

Doubao has long focused on C-end scenarios, with relatively weak B-end applications for work-related use. C-end consumers generally have low willingness to pay; convincing such users to open their wallets will not be easy for Doubao with its current product and feature offerings. For Zhang Yiming to make Doubao profitable, he must first help it find its true 'selling point.'

In the domestic market, Doubao's main competitors, Qianwen and Yuanbao, are both free. Qianwen even publicly stated last November, 'Ordinary people can use it anytime, for free. We're not considering charging at all right now.' DeepSeek, which has the second-largest user base after Doubao, also lacks a paid membership.

Doubao has not disclosed its revenue. However, in January this year, the Financial Times cited data from market research firm IDC, stating that Volcano Engine has become China's second-largest AI infrastructure and software provider, holding a 13% market share. In the first half of 2025, ByteDance's revenue in China's AI cloud services market reached $390 million.

Image Source: Internet

Compared to quarterly revenue of about $50 billion, ByteDance's income from this market is less than 1%, almost negligible. Moreover, only a portion of this revenue is related to Doubao's large model, meaning its actual revenue is even smaller.

Like other major players, Doubao's costs primarily include infrastructure such as chips, cloud computing power, and data centers; technology R&D for large model training and app development; daily operations for large model inference and app maintenance; and market promotion, personnel salaries, and bonuses.

Reports indicate that ByteDance's capital expenditures in 2025 exceeded 150 billion yuan (~$21.6 billion), with most concentrated in the AI sector. Additionally, ByteDance allocated 85 billion yuan (~$12.2 billion) this year for AI chip procurement. Compared to revenue in the hundreds of millions, investments in the tens of billions are two orders of magnitude higher—and this is just part of ByteDance's AI spending.

A massive user base also corresponds to higher inference costs. In April this year, Doubao's daily Token calls exceeded 120 trillion. Unlike the internet, where more users lead to thinner cost amortization (amortization), in AI, more users mean exponentially higher computing (power and hardware depreciation) expenses. Based on Doubao Seed 2.0 lite's API pricing (0.6 yuan/million tokens for input, 3.6 yuan/million tokens for output), full commercialization could generate daily revenue in the hundreds of millions, with costs in the tens of millions.

Image Source: Internet

In the domestic market, startups like Zhipu, Kimi, and Minimax, facing greater revenue pressure, have long targeted developers, creators, and other groups more willing to pay. Meanwhile, Doubao, Qianwen, and Yuanbao continue to pursue user breadth. This year's AI battle during the Spring Festival Gala was essentially a fight for a national-level AI gateway. The risk of Doubao charging at this juncture is that if its model capabilities do not significantly outperform free competitors, it may lose high-value users in the short term.

Of course, ByteDance is aware of this risk. According to Jiemian News, subsequent versions of Doubao will see significant improvements and changes in productivity and Agent scenarios. At ByteDance's first all-hands meeting in late January this year, CEO Liang Rubo explicitly made 'Doubao/Dola' AI assistant the company's current core objective—a peak to scale in the short term.

Inference Costs Are Rising, Not Falling

While the unit cost per generated Token has indeed dropped sharply from a technical standpoint (e.g., some model API prices have fallen to 1% of previous levels), total AI bills for enterprises and users are soaring. This is primarily due to several core factors:

Traditional AI conversations are 'question-and-answer,' consuming limited Tokens. Modern AI agents (Agent), however, must autonomously plan, search for information, call various tools, execute steps, and repeatedly verify results to complete complex tasks. This cycle may repeat dozens or even hundreds of times, resulting in Token consumption per task 10 to 100 times higher than ordinary chats. As AI evolves from a 'chatting tool' to a 'digital worker,' massive concurrent calls drive exponential growth in computing consumption.

Image Source: Internet

The foundation of computing costs is hardware. Currently, high-end GPUs for AI inference (e.g., NVIDIA H200, Blackwell series) remain in short supply, with rental prices surging. Additionally, AI inference demands high-bandwidth memory (HBM), but HBM production cannot keep pace with explosive demand, causing prices to double and supply to remain tight. From chips and storage to data centers, the entire supply chain is seeing price hikes, ultimately raising inference service pricing.

Cost pressures are further amplified by price increases across the industry. Tencent Cloud announced a 5% price hike for AI computing products starting May 9 this year. Alibaba Cloud raised prices across the board, with increases up to 34%. Zhipu AI has raised prices three times this year, yet API call volumes still surged 400%—demand outstrips supply, and even price hikes cannot curb it. From chips to servers to cloud services, AI infrastructure pricing is being reshaped across the board.

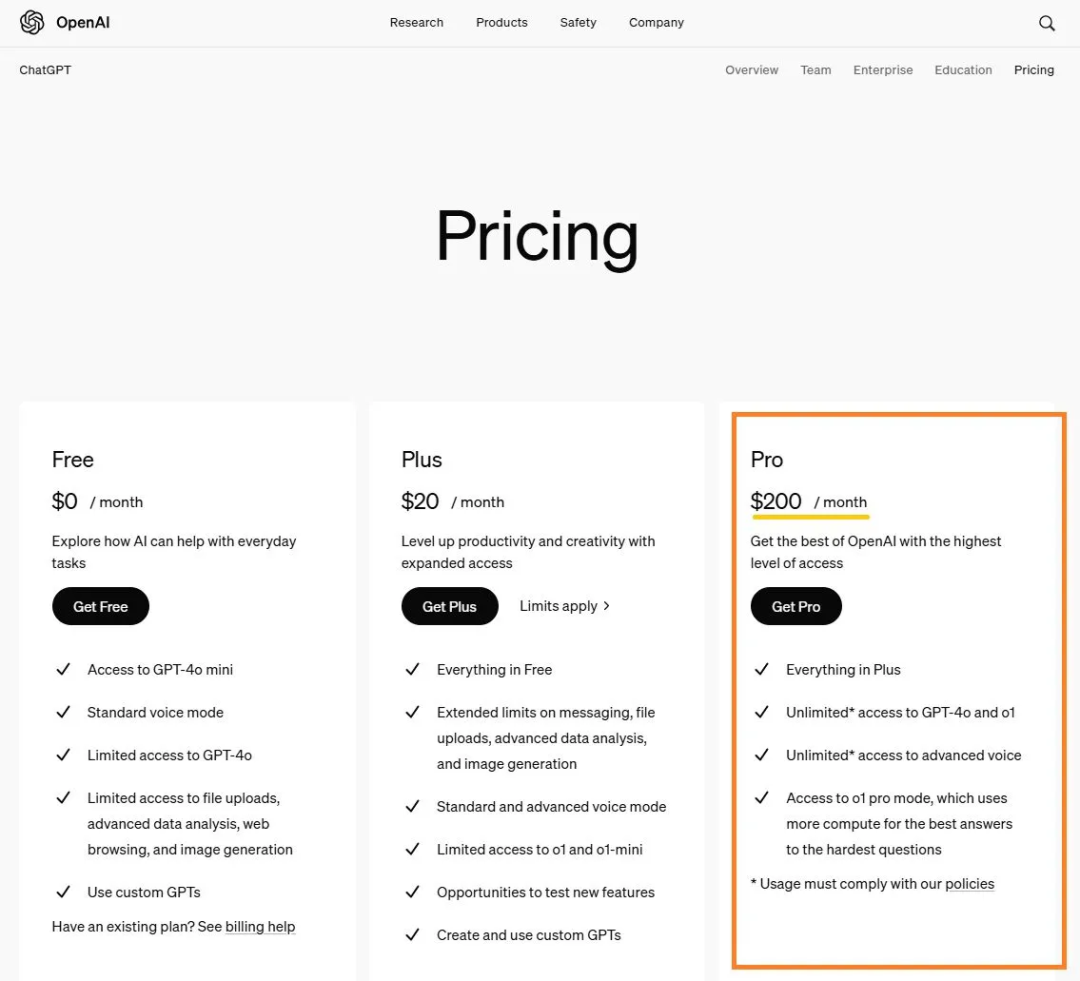

In the U.S., ChatGPT Plus's $20 monthly subscription has become a benchmark, with OpenAI also offering a $200 Pro version. Despite these fees, OpenAI remains unprofitable. In the first half of 2025, it generated $4.3 billion in revenue but lost $13.5 billion, with losses expected to widen to $14 billion in 2026.

Image Source: Internet

To bridge the persistent gap between revenue and costs, ChatGPT even began showing ads to free users in early 2026—a move OpenAI executives had previously publicly opposed. This further confirms that subscription revenue alone cannot fill the large model's computing power black hole.

If even the more mature U.S. market struggles, China faces even greater challenges. Data shows Chinese users' willingness to pay for AI is just 1/3 to 1/4 that of U.S. users. Over 90% of AI market growth in the U.S. comes from SaaS enterprise subscriptions and individual memberships, while Chinese large models generally follow a free model.

What intensifies competition among large models is that mainstream players are all ramping up computing investments. AI competition has shifted from 'whose model is smarter' to 'who can organize cheaper, more stable, and larger-scale computing power.' Future winners must master chips, HBM, advanced packaging, networking, data centers, power, and financing. This is why Google, Amazon, Microsoft, and Meta are all developing custom chips. AI companies are transforming from model firms into computing power orchestrators.

Doubao's shift from free services to tiered revenue models may not generate substantial profits initially, but at least it marks the beginning of self-sustaining commercialization. With 350 million monthly active users, it has essentially reached its domestic ceiling, making further free user acquisition less meaningful.

In the long run, purely free large models will become increasingly rare, or the focus of free components within large models will gradually diminish.

In Closing

The competition among China's large models has shifted from 'who can train a larger model' to 'who can create real commercial value at lower costs across more scenarios.' The global expansion of open-source ecosystems and the ability to deeply cultivate vertical scenarios will be the two main factors determining the final outcome.

Market data from the first quarter of 2026 shows that corporate spending on AI application layers reached $19 billion, with AI-native startups achieving a median annual growth rate of 100%, far exceeding the 23% growth rate of traditional SaaS companies. Legal AI firms like Harvey and enterprise search AI companies like Glean have secured substantial funding and valuations.

The distribution of AI value is shifting from foundational models to upstream applications. Companies operating at the application layer that can solve specific problems and deliver clear ROI are gaining greater bargaining power.

References:

'Doubao's Pricing Strategy: Avoiding the Pitfalls of Grok' - Source: Zimu Bang

'Why Doubao is Experimenting with Paid Services' - Source: Jiemian News

'Under Computational Pressure, Even Doubao May Resort to Charging' - Source: Economic Observer Report

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!