Q1 Financial Reports Released: Cumulative Profits of Ten Automakers Lag Behind CATL

05/11 2026

05/11 2026

394

394

Ten listed automakers toiled for a hundred days, selling millions of vehicles, yet their combined profits still fell short of CATL's.

By the day after May Day holiday, the Q1 2026 financial reports of automakers were largely disclosed. Among the 10 listed passenger vehicle enterprises surveyed, only Seres and SAIC Motor maintained slight increases in net profit attributable to shareholders, while the rest experienced significant profit declines.

In Q1 2026, the domestic passenger vehicle market faced multiple pressures, including policy rollbacks, demand depletion, ongoing price wars, and raw material price fluctuations. The industry overall exhibited a development trend of 'declining volumes and profits, with a cold domestic market and hot overseas market.'

Against this backdrop, differentiation among enterprises intensified. Leading companies maintained resilience through scale and overseas advantages, while some weaker automakers fell into losses. The industry is accelerating into a critical phase of structural adjustment.

'Increasing Revenue Without Increasing Profits'

On April 30, Changan Qiyuan announced a price increase of RMB 3,000 for the Q07 Shenshu Intelligent Laser Edition; two days earlier, BYD also adjusted the optional prices for assisted driving features on some models, raising them by RMB 2,100.

According to incomplete statistics, since 2026, over 10 new energy vehicle companies have taken actions akin to price hikes, such as reducing terminal discounts, with increases ranging from RMB 2,000 to RMB 10,000. To date, only Changan and BYD have issued official announcements.

Notably, Changan and BYD are also the two companies with the most severe profit declines among those releasing Q1 reports.

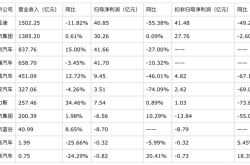

BYD reported Q1 revenue of RMB 150.225 billion, down 11.82% year-on-year, with net profit attributable to shareholders of RMB 4.085 billion, a 55.38% year-on-year decline, effectively halving. Changan Automobile's Q1 net profit attributable to shareholders was RMB 351 million, down 74.09% year-on-year.

Under immense pressure from rising raw material and memory chip prices, price hikes became imperative.

In addition to profit reductions due to increased costs, the demand depletion at the end of last year, combined with the extended Chinese New Year holiday this year, led to a sales decline in the domestic auto market in Q1, directly pressuring BYD's performance. In Q1, BYD's cumulative vehicle sales reached 700,500 units, down 30.01% year-on-year, with domestic sales halved.

However, BYD performed outstandingly in overseas markets in Q1, with passenger vehicle and pickup truck overseas sales reaching 321,200 units, a year-on-year increase of over 50%. Overseas sales now account for approximately 45% of total sales. Benefiting from overseas sales growth, BYD's Q1 gross profit margin rose to 18.8%.

Some analysts believe that BYD is intentionally sacrificing current earnings to allocate substantial funds towards R&D, production capacity expansion, and brand matrix expansion (new brands + overseas layout ). These investments represent a strategy of 'burning cash' to build moats, but the short-term pain is real and cannot be ignored.

This also presents an opportunity for Geely and Chery to surpass BYD in terms of profit. Chery reported Q1 revenue of RMB 65.87 billion, just 43.8% of BYD's, yet its net profit reached RMB 4.17 billion, growing rapidly and ranking first among the 10 companies.

Geely reported Q1 revenue of RMB 83.776 billion, up 15% year-on-year, with net profit of RMB 4.166 billion, up 31% year-on-year, surpassing BYD in profit for the first time. Its sales also reached 709,400 units, up 1% year-on-year, slightly higher than BYD's. This outcome has prompted the outside world to re-examine Geely's profit model.

In comparison, SAIC Motor's Q1 revenue and net profit remained relatively stable, demonstrating strong risk resistance within the industry. SAIC Motor reported Q1 revenue of RMB 138.52 billion, up 0.61% year-on-year, with net profit attributable to shareholders of RMB 3.026 billion, up 0.09% year-on-year.

Additionally, Seres reported Q1 revenue of RMB 25.75 billion, up 34.46% year-on-year, with net profit attributable to shareholders of RMB 754 million, up slightly by 0.89% year-on-year. Stable deliveries of the Aito series and premiumization drove profit growth, effectively offsetting R&D investment pressures. Seres' Q1 new energy vehicle sales reached 78,500 units, up 43.9% year-on-year. Among them, Aito series sales were 70,200 units, up 55.64% year-on-year. R&D expenses were RMB 1.794 billion, up RMB 743 million year-on-year, a 70.68% increase.

Overall, the Q1 passenger vehicle industry's sales profit margin was just 3.2%, far below the average for downstream industries, making profitability significantly more challenging. The industry has shifted from scale expansion to competition over profit quality.

Among the ten listed companies, excluding loss-making enterprises, the cumulative net profit attributable to shareholders in Q1 2026 was only RMB 17.497 billion.

It's worth noting that CATL, in contrast, reported Q1 revenue of RMB 129.131 billion, up 52.45% year-on-year; net profit attributable to shareholders was RMB 20.738 billion, up 48.52% year-on-year, earning RMB 230 million daily.

Ten listed automakers toiled for a hundred days, selling millions of vehicles, yet their combined profits still fell short of CATL's. Notably, these listed automakers remained robust in revenue performance, with cumulative revenue exceeding RMB 570 billion, five times that of CATL, yet their profits were far lower.

One can only say that building cars is truly not a lucrative business.

Overseas Expansion Becomes the 2026 Theme

In response to automakers' profit performance falling short of expectations, Chen Shihua, Deputy Secretary-General of the China Association of Automobile Manufacturers, stated in a media interview that the 'two new' policies introduced at the end of last year were adjusted in Q1 this year, with new energy vehicle purchase taxes shifting from tax-exempt to a 5% levy, having a certain phased impact on sales. Additionally, the continuous rise prices of raw materials like copper, aluminum, and chips began to transmit cost pressures to the terminal market by March, further compressing corporate profit margins.

Given these superposition factors, it is normal for leading automakers to experience a decline in Q1 profit performance. Companies with advantages in cost control, overseas brand premiums, and product structure upgrades are gradually establishing new competitive edges amid the pressure.

With pressure mounting in the domestic market, overseas markets have become the core growth engine for passenger vehicle companies. Recently, influenced by factors such as soaring international oil prices, many overseas consumers have started to pay attention to new energy vehicles, with rapid sales growth in Europe, Asia-Pacific, and Latin America.

Data released by the China Association of Automobile Manufacturers shows that in March, vehicle exports reached 875,000 units, up 30.2% month-on-month and 72.7% year-on-year; among them, new energy vehicle exports were 371,000 units, up 1.3 times year-on-year, while traditional fuel vehicle exports were 505,000 units, up 44.6% year-on-year.

In Q1, vehicle exports reached 2.226 million units, up 56.7% year-on-year, surpassing Japan for the first time to become the global leader. New energy vehicle exports were 954,000 units, up 1.2 times year-on-year, accounting for over 40% of total exports and serving as the core driver of export growth.

BYD's overseas sales neared 320,000 units, SAIC Motor's were 325,000, Chery Automobile's exports were 393,300 units (with exports accounting for a high 65.4%), Geely Automobile's exports were 203,000 units (up 126% year-on-year), and Great Wall Motor's overseas sales were 130,100 units. The proportion of overseas sales among leading automakers continues to rise.

Overseas business not only drives revenue growth but also serves as a crucial support for hedging domestic market risks. However, exchange rate fluctuations have emerged as a 'black hand' eroding profits, with companies having a high proportion of overseas revenue facing foreign exchange loss risks.

According to financial reports, BYD's financial expenses increased by 210% year-on-year, Geely Automobile incurred a net foreign exchange loss of RMB 497 million due to exchange rate fluctuations, and Great Wall Motor's net profit decreased by 46.01% year-on-year, with the main reasons pointing to reduced foreign exchange gains from exchange rate changes.

Geely Automobile explicitly stated that the decline in net profit was primarily affected by foreign exchange fluctuations, and after excluding non-core gains and losses such as foreign exchange, core net profit attributable to shareholders increased by 31% year-on-year.

Why do exchange rates have such a significant impact on corporate profits? For example, the RMB exchange rate was 7.2 last year, and the exchange rate for overseas orders was 7.15, but upon delivery, 1 USD could only be exchanged for 6.8 RMB, a decline of approximately 4.9%.

If a company's revenue is RMB 25.5 billion, with about 85% of it in USD, then 25.5 billion (total revenue) × 85% (USD proportion) × 4.9% (exchange rate decline) ≈ RMB 1.06 billion. Due to exchange rate fluctuations, approximately RMB 1.1 billion in actual cash 'vanished' from the company's books. This RMB 1.1 billion would have been pure profit but now serves as a 'deduction' on the financial statements.

The larger the proportion of export business, the greater the impact. However, for some companies, exchange rates merely act as an amplifier, making problems appear more severe. The root cause of the issues obviously does not lie in exchange rates.

Without mandatory foreign exchange settlement, most companies keep their USD overseas to earn interest. If the RMB continues to appreciate while the Federal Reserve cuts interest rates, the interest rate differential may not cover the exchange rate differential, prompting companies to settle foreign exchange en masse, further pushing up the RMB exchange rate and creating a vicious cycle.

It is foreseeable that exchange rate impacts will persist in the coming months and may even be reflected in mid-year financial reports. However, for these automakers, exports remain a primary profit source, and the impacts are mutually influential.

The Q1 2026 financial report data of listed passenger vehicle companies reflects the current profitability pressures and structural differentiation challenges facing the industry. In the short term, domestic market demand recovery will take time, and raw material price fluctuations and exchange rate risks will continue to affect corporate performance, with industry profitability likely remaining low.

In the long term, new energy transformation and overseas expansion remain the two core strategic focuses of the industry. Companies with technological advantages, high-end brand matrices, and overseas channel layouts will take the initiative during the industry adjustment period.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for deletion. -END-

-

![]()

Understanding 'Computing Power Inflation' in One Article: Why Is AI Getting Cheaper for You, Yet Computing Power Companies More Profitable?

-

![]()

The World is Re-evaluating China's Chips

-

![]()

Chongqing Releases 'Detailed Rules for the Administration of Expressway Testing of Intelligent Connected Vehicles (Trial)': Permitting L3+ Vehicles on Expressways: The 'Practical Examination' for Auto

-

![]()

Samsung’s Home Appliance Business: A Seemingly Inevitable Decline

-

![]()

Zhipu’s GLM-5V-Turbo ‘Crosses the Rubicon’: The Dawn of a Domestic Multimodal Agent War

-

![]()

Doubao Introduces Charges: Fewer and Fewer Purely Free Large Models

-

![]()

Q1 Financial Reports Released: Cumulative Profits of Ten Automakers Lag Behind CATL

-

![]()

Can Doubao's Paid Subscription Model Succeed?