Ali Health Streamlines Operations: Is AI the Key to Filling Gaps?

05/18 2026

05/18 2026

436

436

Proceed with Caution and Self-Care

After eight years on the public market and surpassing RMB 34 billion in annual revenue, Ali Health is finally consolidating its healthcare sector.

On May 15, during the FY2026 earnings analyst call, Shen Difan, Chairman and CEO of Ali Health, announced that Alibaba will centralize its pharmaceutical business operations within the Group and entrust them to Ali Health for enhanced coordination and synergy.

Specifically, Alibaba has formed a dedicated pharmaceutical business unit within the Group, fully integrating B2C and O2O sales at both organizational and reporting levels, with Ali Health taking the helm.

In essence, all medical and health-related businesses within Alibaba are being reorganized under Ali Health.

Meanwhile, Ali Health's FY2026 results revealed that as of March 31, 2026, the company recorded RMB 34.255 billion in revenue, up 12% year-over-year (YoY); net profit reached RMB 1.936 billion, up 35.2% YoY; and adjusted net profit hit RMB 2.326 billion, up 19.3% YoY.

With both revenue and profit on the rise, Shen Difan chose this moment to unveil a channel integration plan. What lies ahead for Ali Health?

01

B2C and O2O: No Longer at Odds

Looking back two years, few could have predicted that Kuaishou, a short-video platform known for its "bro" (lao tie, close friends) culture and live streaming, would emerge as a global leader in AI video generation.

Since its official launch in June 2024, Kling has received top-tier support within Kuaishou's ecosystem.

Internal competition among business lines is common in large corporations. Previously, Ali Health faced hidden rivalry between its B2C and O2O operations.

Under the old structure, a single user purchasing medicine on Alibaba's platforms was unwittingly funneled into two distinct channels:

One was the B2C model, exemplified by online shopping platforms like Tmall Pharmacy, offering a wide range of medicines at competitive prices, catering to users with chronic conditions or household stockpiling needs, emphasizing "comprehensiveness" and "cost-effectiveness." The other was the O2O instant sales model, built on local life networks, prioritizing emergency response and convenience, focusing on "speed," where delivery personnel could bring urgent medicines within an hour.

Differences in these sales channels and models also led to disparities between the two teams.

The B2C team focused on leveraging the traffic pools of Taobao and Tmall, monitoring metrics like average order value, conversion rates, and Double 11 stockpiling GMV. In contrast, the O2O team was more "ground-level," focusing on Taobao Flash Sales and offline promotions, competing on delivery speed and order acceptance rates.

On the surface, B2C and O2O complemented each other, covering user scenarios from chronic disease medication stockpiling to acute fever emergencies. However, in practice, these two businesses operated under separate organizational structures with distinct reporting lines and KPIs.

This led to "friction" between teams. When a user opened Tmall or Taobao Flash Sales, the B2C and O2O teams were effectively competing, each trying to lure the user to their channel with subsidies to meet their respective KPIs.

This is a classic example of a channel-driven mindset. When traffic dividends were abundant, such "internal competition" could be masked by rapid growth.

However, as the growth rate of the pharmaceutical e-commerce industry slowed from 37.09% in 2021 to 9.4% in 2025, the logic of inventory competition began to dominate. One team's growth often came at the expense of the other's space.

Thus, integrating B2C and O2O sales at both organizational and reporting levels is less about Ali Health expanding its territory and more about dismantling the walls between sibling business lines under the Group's directive.

Notably, this organizational adjustment aligns with Alibaba Group's broader strategy. In August 2025, Alibaba completed a major restructuring, integrating Ele.me and Taobao Flash Sales into an instant retail business. Ali Health's consolidation of the pharmaceutical sector follows the Group's strategic contraction pace.

02

Can Hydrogen Ion Win Over Prescribing Doctors?

Just two days before announcing the integration, on May 13, Ali Health launched its first AI product, "Hydrogen Ion," in Hangzhou. Targeting clinicians and researchers, Hydrogen Ion is positioned as a "GPT for doctors" and represents the first commercial application of Ali Health's medical AI model.

According to previous reports by Jianwen Consulting, Ali Health CTO Xiang Zhi stated that the biggest challenge in developing Hydrogen Ion was avoiding a traffic- and internet-driven mindset when discussing scalability. "With 5 million doctors in China, if we only focus on traffic, the ceiling will inevitably be low. The key is how much we can influence medical decision-making."

A former Alibaba employee told Super Focus that Ali Health's move may aim to target doctors first, hoping to secure advertising budgets from pharmaceutical companies by "winning over" doctors.

In his view, advertising to 5 million doctors is still a relatively small market. This move seems more about validating Ali Health's newly proposed "pharmaceutical full-stack + medical AI" dual-drive strategy. By analyzing doctors' searches and questions through the AI model, it can not only obtain regional disease information but also preemptively grasp prescribing preferences for various medications.

This B-end prescription information will directly feed into the newly integrated B2C and O2O business lines. Tmall Pharmacy's central warehouse can prepare inventory in advance, while same-city flash sales' front warehouses can optimize stock structures, maximizing medication sales efficiency.

However, this is not the entirety of Alibaba's health ecosystem. If "Hydrogen Ion" is Ali Health's hidden stake in the doctor community, on the C-side, Alipay's AI health app "Ant Afu" has already achieved significant user growth.

During the 2025 Spring Festival, "Ant Afu" completed its cold start through large-scale red packet subsidies and ground promotion teams. By the end of 2025, "Ant Afu" had over 30 million monthly active users, answering over 5 million health questions daily, with 55% of users from third-tier and lower cities.

For the general public, Afu is like an always-available family doctor but also serves as a massive patient data collector.

Hydrogen Ion on the B-side connects with doctors, while Ant Afu on the C-side reaches patients. The B2C + O2O business lines handle transaction fulfillment, gradually forming a closed-loop medical commercial data ecosystem. Information on medication preferences and disease trends obtained by Hydrogen Ion from doctors can theoretically be fed back to Tmall Pharmacy's central warehouse for advance stocking and help same-city flash sales' front warehouses optimize inventory structures.

Data supports this strategy: The number of transactional merchants on Tmall Health increased by 26% YoY to 47,500, with online SKUs growing 25.8% to 27.5 million. Ali Health Pharmacy's SKUs surged 79% to 2.2 million. Self-operated member ARPU grew over 14% YoY.

However, Hydrogen Ion operates in a still "niche" sector. Current AI products for doctors generally face small user bases. Ali Health's move resembles installing a monitoring system at the industry's upstream, using the AI model to analyze doctors' searches and questions, obtaining regional disease information and prescribing preferences, and feeding this data back to the transaction side.

03

Inventory Competition Cycle

The Market Doesn't Want Long-Term Stories

While Kling has achieved success, its sector is rapidly becoming crowded and challenging.

The blueprint looks beautiful, but Ali Health faces the same issue as Alibaba Group: AI remains an investment without immediate commercialization.

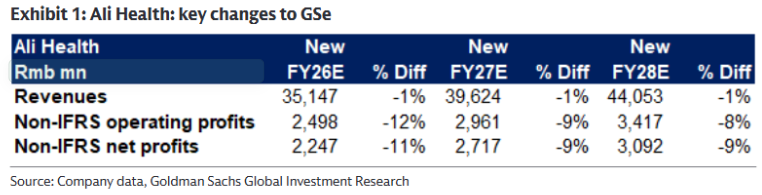

In an April 2026 research report, Goldman Sachs downgraded Ali Health's target price from HK$5.2 to HK$4.8, maintaining a "Neutral" rating. One core reason for the downgrade was profitability: Increased AI and pharmaceutical category investments will impact profitability. The bank lowered its adjusted net profit forecasts for Ali Health by 9% to 11% for FY2026-2028.

Goldman Sachs' judgment is supported by specific data. Ali Health's R&D spending reached RMB 788 million in FY2026. Given the long AI model development cycle and uncertain returns, this investment is unlikely to translate into revenue in the short term and will directly drag down profits.

Moreover, profit pressure comes not only from AI investments but also from long-standing business challenges.

Goldman Sachs noted that Ali Health expects profits to decline slightly in the second half of the year, reversing the first half's profit expansion trend. One key reason is increased discounts on branded drugs to counter competition. However, Ali Health's gross margin for FY2026 already declined to 24% YoY.

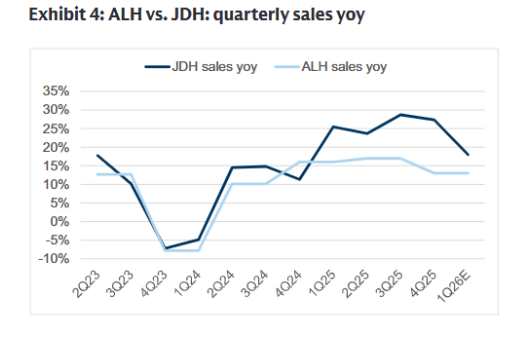

Specifically, Ali Health faces a situation where JD Health has already gained the upper hand.

In terms of revenue, JD Health reported total revenue of RMB 73.44 billion in 2025, with pharmaceutical and health product sales reaching RMB 60.9 billion and net profit of RMB 6.53 billion, up 36.3% YoY. In comparison, Ali Health's FY2026 revenue of RMB 34.255 billion shows a clear gap with JD Health.

HSBC Research data also indicates that JD Health and Ali Health's projected pharmaceutical sales growth rates for 2026 are 18% and 13%, respectively, both slowing from the previous year, but JD Health's lead continues to widen.

Additionally, the rise of Douyin Health and Meituan Medicine is eroding the existing market. In 2025, Douyin Health's GMV exceeded RMB 100 billion, while Meituan Medicine's GMV reached approximately RMB 60 billion, becoming formidable latecomers.

Beyond external competition, a more hidden obstacle lies in Ali Health's path: data compliance. Under the "Hydrogen Ion + Ant Afu + B2C + O2O" closed-loop vision, Ali Health needs to integrate three sets of underlying data from doctors, patients, and transactions. However, Ali Health, Alibaba Group, and Ant Group are three separate legal entities, and cross-enterprise personal data transfers face strict legal constraints.

According to Article 28 of China's Personal Information Protection Law, medical health information is classified as sensitive personal information, which can only be processed under specific purposes, with sufficient necessity, and with individual consent.

In April 2025, the National Cyberspace Administration further released the "Data Security Technology - Security Requirements for Sensitive Personal Information Processing," which took effect in November of the same year, providing more detailed boundaries for medical health information processing.

This means that to integrate full-chain data without violating regulatory red lines, Ali Health needs mature privacy-preserving computation technologies and strict compliance designs.

For a giant with over RMB 34 billion in annual revenue, this is not technically infeasible, but the compliance costs and implementation timelines remain significant variables.

The next question is whether Ali Health, after consolidating its operations under Shen Difan, can achieve incremental growth through B2C-O2O synergy, sustain itself through the long AI investment return cycle, and defend its position amid pressure from JD Health and Meituan.

The answer may lie not in the blueprint but in the data of the coming fiscal quarters.

- END -

-

![]()

Focus | CCCC’s Takeover of Greentown Comes to Fruition: Why Did the 11-Year ‘Control Without Authority’ Era End?

-

![]()

Final Verdict: The 2026 China Auto Forum Shines with Unique Characteristics at a Pivotal Moment

-

![]()

Tencent Maintains Matrix Approach, Alibaba Merges Entry Points: Tech Titans Initiate AI Agent Consolidation

-

![]()

Geely Secures Portion of Ford’s Spanish Production Capacity

-

![]()

Tesla Stalls This Second

-

![]()

Elon Musk's 'Money-Burning' Spree: All Car Sales Profits Poured into AI

-

![]()

Why Did Tesla’s Profits Drop and Cash Flow Go Negative?

-

![]()

AI Titans Are All in the Red: Time for Intelligent Driving Car Buyers to Reassess?