Xiaomi Mobile Phones: Vanishing Market Share

05/18 2026

05/18 2026

472

472

Editor: Captain Timo

In the first quarter of 2026, China's smartphone market underwent a ruthless industry reshuffle.

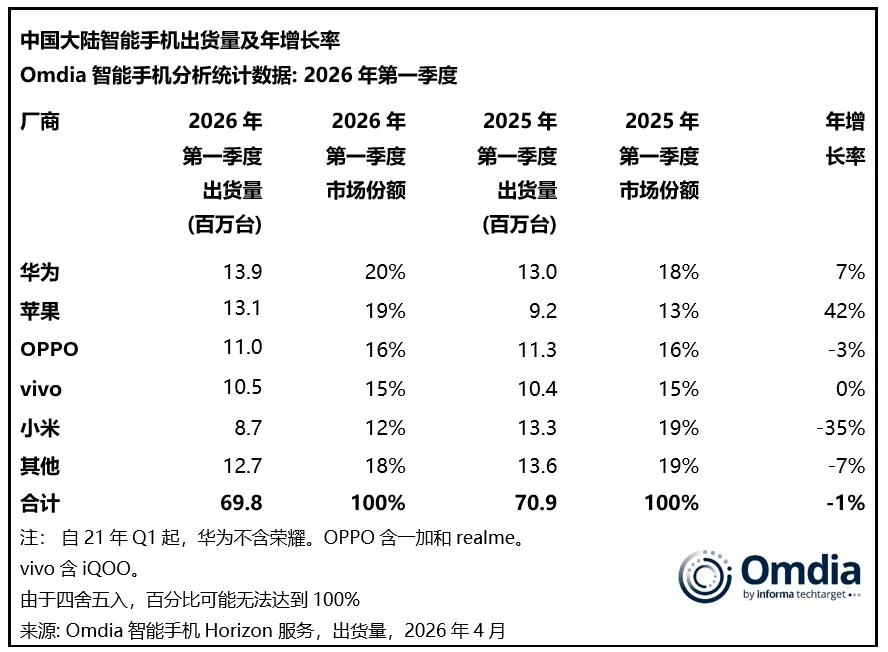

Data from two industry reports, one by IDC and the other by Omdia, have been cross-verified: Xiaomi, a former longstanding leader in the domestic market, recorded its poorest performance in nearly a decade during Q1 2026. Domestic shipments plummeted by 35% year-on-year, while global shipments dropped by 19.1%. In IDC's Q1 domestic ranking, Xiaomi fell out of the top five and was lumped into the 'Others' category.

IDC Ranking

IDC Ranking

Just a year earlier, Xiaomi had topped China's smartphone sales charts. In a mere twelve months, the rankings have completely reversed. Xiaomi's 'cost-effectiveness' model, which it relied on for survival, is now on the brink of obsolescence, leading to a rapid decline in market share and necessitating a reshaping of its industry position.

Is the collapse in Xiaomi's smartphone sales a result of industry-wide trends? Can it regain its former glory?

01

Vanishing Market Share

Starting in early March of this year, brands like OPPO, OnePlus, vivo, and iQOO have already announced price hikes, with Honor and Samsung also raising prices on some models. By April 11, Xiaomi adjusted the suggested retail prices of some in-stock products, indicating that all mainstream smartphone brands, except Apple and Huawei—which focus on the high-end market—have joined the price increase trend.

Omdia data offers a clear picture: In Q1 2026, China's smartphone market sales only declined by 1% overall. However, Huawei experienced a 7% year-on-year increase, while Apple surged by 42%.

Omdia Ranking

Notably, Xiaomi did not implement price hikes domestically in Q1, yet its shipments plummeted. This seems to defy the logic observed with Huawei and Apple, which gained market share without raising prices.

So, why has Xiaomi's market share vanished? And where has it gone?

The sharp decline in Xiaomi's smartphone sales this time appears to be due to rising storage chip prices on the surface, but at its core, it is a result of a product launch cycle gap.

Firstly, storage chip prices: According to Counterpoint's Q1 2026 industry supply chain data, DRAM memory contract prices rose by 55%-60% quarter-on-quarter, while NAND flash memory increased by 33%-38%. This significantly raised core hardware costs for smartphones. For Android manufacturers with a high proportion of low-end models, rising material costs directly compressed profit margins.

Xiaomi Group President Lu Weibing admitted at MWC 2026 that the cost of a 12GB+256GB memory combination had surged from a low of over $30 to $120-$130. Omdia also pointed out that over half of Xiaomi's shipments were concentrated in the sub-$200 price segment, making it more directly impacted by cost increases.

Secondly, the product launch cycle gap: In Q1 2026, Xiaomi released almost no major new products, with the only new model being the Redmi Turbo 5 series launched in late January. Shipments relied heavily on nearly all previous year's models (Xiaomi 17 series, Redmi K90 series, and Turbo series), naturally lacking market momentum.

AI tech self-media Houchangcun believes that as an internationally renowned smartphone manufacturer, Xiaomi, facing dual pressures of rising industry hardware costs and a new product gap, has chosen to selectively scale back low-margin entry-level models to protect profits rather than market share. This has led to a significant loss of domestic base sales, not due to a decline in user recognition of its product value.

02

Profit Protection in a Shrinking Market

Facing the dual pressures of cost squeezes and declining sales, Xiaomi's choice appears more like a forced contraction.

Guohai Securities research estimates that Xiaomi's smartphone business revenue in Q1 2026 was approximately 43.1 billion yuan, down 15% year-on-year, with a gross margin of around 9%. The contraction in shipments coincided with an increase in ASP (average selling price)—by reducing low-end model shipments, the smartphone ASP approached 1,300 yuan, achieving year-on-year and quarter-on-quarter growth. This means Xiaomi has, to some extent, traded shipment scale for average unit price and gross margin.

According to Zaker, Xiaomi internally expects smartphone business sales to decline by 13% this year and has begun adjusting its offline store strategy, halting offline expansion and shifting revenue focus to major appliances. According to Caijing, the focus has shifted from smartphones to higher-margin appliance businesses, with major appliances now accounting for over 20% of overall store performance. Internally, the message is clear: 'Smartphones are no longer the top priority; the real money is in major appliances.'

Throughout 2025, Xiaomi's smartphone gross margin declined from 12.6% in 2024 to 10.9%, while IoT and consumer product business gross margin reached a record high of 23.1%. In 2025, smart electric vehicle revenue was 103.3 billion yuan, up 221.8% year-on-year, accounting for 23.2% of total group revenue. This business structure means the smartphone business no longer holds priority in resource allocation.

03

Who’s Still Willing to Pay for Xiaomi?

Xiaomi currently operates two major brands: the Xiaomi digital series, positioned as high-end, and REDMI, targeting mid-to-low-end cost-effectiveness. However, in Q1 2026, the boundary between the two brands has blurred. The REDMI K90 series' Pro Max version starts at 3,999 yuan, with the champion edition reaching 5,299 yuan, directly competing with the Xiaomi 17 series.

Xiaomi Official Website

Xiaomi Official Website

From a consumer demographic perspective, Xiaomi's shipment decline this time is not due to a mass exodus of core loyal users but rather a structural user loss amid consumer segmentation and iteration.

Xiaomi's current consumer base can be clearly divided into two groups: core existing users with brand loyalty and casual consumers who flow based on price fluctuations.

Among them, users demanding high-performance machines, tech enthusiasts, and heavy users of the Xiaomi ecosystem still retain strong loyalty, valuing hardware configuration, system compatibility, and IoT ecosystem synergy, and are less affected by short-term price adjustments. Meanwhile, the vast base of casual consumers continues to drift away.

04

Conclusion

Xiaomi faces a choice: continue multi-line expansion, betting on automotive, AI, and major appliances, or refocus on its core smartphone business, streamline its product lineup, and reinforce its high-end barriers?

The era of rapid rise through cost-effectiveness is over. Before the next industry reshuffle arrives, Xiaomi must make a choice—rather than just growing larger, it needs to go deeper.

-

![]()

The 'Shenzhen Pavilion' at the Xiamen Smart Transportation Expo: 2,400 Roads, 2,000 Vehicles, 8.66 Million Orders—How Does Pengcheng Define the 'Chinese Approach' to Autonomous Vehicles?

-

![]()

Shenzhen's April Report on Driverless Vehicles: 1,259 Vehicles on the Road, Shifting from 'Running' to 'Running All Night'—What Is This City Doing Right?

-

![]()

Xiaomi Mobile Phones: Vanishing Market Share

-

![]()

Ali Health Streamlines Operations: Is AI the Key to Filling Gaps?

-

![]()

Yuanbao Is 'Leaking,' Tencent Secures Just a 'Standing Ticket' in the AI Race

-

![]()

Rebuilding a Pinduoduo in Three Years: Temu Encounters Overseas Regulatory Challenges

-

![]()

Latest Exclusive Interview with Anthropic CEO: Claude's New Features Developed Almost Entirely by AI, Software Heading into a Free Era

-

![]()

Baidu AI: Pioneering Solo in the Entrepreneurial Landscape