Surging by 2000%, Market Value Breaks Through Trillion Yuan! Behind the Glory of AI 'Leader'

06/23 2026

06/23 2026

464

464

On the first trading day after the Dragon Boat Festival holiday, Zhipu's stock price ("GU" pronounced similarly to "stock," using letters to avoid sensitive terms) briefly surged past HK$2,900, with its total market value historically exceeding the HK$1 trillion mark.

From its debut on the Hong Kong Stock Exchange on January 8 at an issue price of HK$116.2, the stock price has multiplied over 20 times in less than six months.

HK$1.14 trillion. Rivaling Baidu and surpassing Xiaomi, Meituan, and JD.com. It ranks first in valuation among domestic AI enterprises, firmly establishing itself as the "leader."

This milestone comes just nine days after Zhipu released the GLM-5.2 model.

Everyone thinks it's overpriced. Yet the price keeps rising.

Why?

Triple Catalysts

A stock price surge is never due to a single factor. Zhipu's rally results from the convergence of three forces: technological breakthroughs, geopolitical events, and capital inflows.

Technological prowess shines. On June 17, Zhipu released and open-sourced its new flagship large model, GLM-5.2. With 744B total parameters and a 40B activated MoE architecture, it supports 1 million token lossless context.

It ranked first in Code Arena's global front-end development evaluation; topped Design Arena's web design assessment; and in FrontierSWE's real-world software engineering task evaluation, it trailed only Claude Opus 4.8 by about 1 percentage point.

Scoring 51 on Artificial Analysis's comprehensive leaderboard, it ranks as SOTA among open-source models. For the first time, a Chinese open-source large model stands alongside flagship models from Anthropic and OpenAI in programming—a high-commercial-value capability.

Geopolitical timing is impeccable. On June 12, the U.S. government issued an order demanding Anthropic immediately disable its flagship models, Fable 5 and Mythos 5, cutting off global non-U.S. users instantly.

Twenty-four hours later, Zhipu announced GLM-5.2's full availability to all users. The timing seemed scripted. Shortly after, Zhipu founder Tang Jie engaged in a public dialogue with Elon Musk on X. Musk predicted Chinese models would catch up to Fable by Q1 2027; Tang retorted, "Not that long." This clash ignited market sentiment.

Capital inflows resonate. On June 8, Zhipu was officially included in the Hang Seng Tech Index and Stock Connect. With no pure large model leader in China's A-share market, Zhipu became a "scarce outlet" for mainland capital to allocate to AI core assets.

Meanwhile, Zhipu's "return to A-shares" accelerated. On June 1, it announced plans to issue A-shares on the STAR Market, raising up to RMB 15 billion; on June 17, its IPO counseling status changed to "completed." The room for imagination of "A+H dual valuation mapping" fully opened.

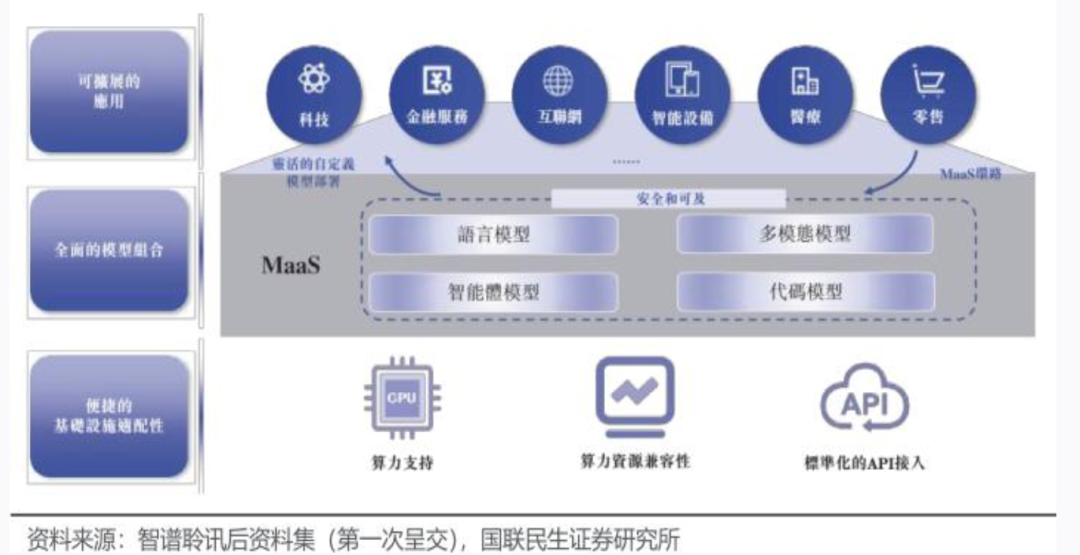

Zhipu's MaaS Business Model:

These three catalysts propelled Zhipu to one of the fastest market cap growth curves among global AI enterprises.

AI 'Leader's' True Fundamentals

Amid the hype, let's examine the numbers.

Data Source: Tonghuashun

Zhipu's 2025 full-year revenue reached RMB 724 million, up 131.9% YoY. Tripling for three consecutive years, the growth rate is impressive.

But on the flip side: Full-year net loss hit RMB 4.718 billion, widening by 59.5% YoY. Adjusted net loss was RMB 3.182 billion. R&D spending reached RMB 3.18 billion, 4.4 times revenue.

For every RMB 1 earned, RMB 6.5 was lost.

Currently, this is not a profitable company but a research-driven one reliant on financing.

Cash flow tells the story. In 2025, Zhipu's operations consumed about RMB 2.246 billion in cash, plus RMB 376 million in investments, totaling RMB 2.622 billion in outflows.

Its January 2026 Hong Kong IPO raised RMB 4.516 billion, with RMB 2.614 billion net inflow as financing. Without this, its cash reserves might not last long.

This explains Zhipu's urgency to launch a STAR Market IPO, planning to raise another RMB 15 billion, with RMB 12 billion earmarked for general-purpose large model R&D. Essentially, it's extending its "capital lifeline."

Now, business structure. Zhipu has two legs: Local deployment revenue was RMB 534 million (73.7% of total); cloud MaaS revenue was RMB 190 million (26.3%). Local deployment gross margin plunged from 66% in 2024 to 48.8%; cloud margin soared from 3.3% to 18.9%. Overall gross margin dropped from 56.3% to 41%.

The rising cloud share dragged down overall margins, but MaaS's explosion gave the market new imagination. By March 2026, MaaS's annual recurring revenue (ARR) hit RMB 1.7 billion, growing 60-fold in a year. The platform connects over 4 million enterprises and developers, with 9 of China's top 10 internet firms deeply using GLM daily.

This is key to Zhipu's valuation logic shift. The market's valuation anchor is moving from technical races ("model parameters, benchmarks") to commercialization pricing ("certain revenue from AI industry adoption").

ARR, a quantifiable SaaS metric, finally gives Zhipu something measurable by traditional valuation frameworks.

But can a RMB 1.7 billion ARR justify a HK$1 trillion market cap?

The price-to-sales ratio is about 1,600x. This means the market has discounted "future success many years ahead" into today's price.

Hidden Risks Behind the Glory

First, the threat of price wars looms. On May 22, DeepSeek quietly announced API input price cuts across all tiers, with limited-time discounts on flagship models, effectively a permanent 75% reduction. Output price gaps exceed 100x.

This isn't just competing with peers—it forces everyone to answer: If your model can't match DeepSeek's cost-effectiveness, what's your market position?

In June, Xiaomi, ByteDance, and Tencent followed with price cuts. OpenAI also launched its first large-scale API price reduction.

Zhipu took the opposite path, raising prices. It slashed prices by 90% in April 2025; began raising them with GLM-5's release in February 2026, with cumulative API price hikes of 83%; and increased Coding Plan prices by 30%.

How long can this strategy last? Can Zhipu remain unscathed if the entire industry engages in price wars?

Second, how long can technological leadership last? GLM-5.2 performs well on benchmarks. But developers note that for similar task completion rates, GLM-5.2 consumes significantly more time and tokens than peer models.

This suggests inefficiency in "figuring out what to do."

Musk's point holds: Close benchmark scores ≠ similar model productivity. Technological leads in large models are hard to sustain long-term. ByteDance, Alibaba, Tencent, Baidu, DeepSeek, Kimi, and MiniMax are all vying for dominance.

Third, profitability remains distant. At current loss rates, when will Zhipu turn profitable? No one knows.

Assuming a mature 20x price-to-sales ratio, it needs RMB 50 billion in revenue; at 50x, RMB 20 billion. Yet 2025 revenue was under RMB 1 billion.

The market is betting on "whether it can become China's core AI infrastructure entrance ."

This is a probability, not a certainty.

A Respectable Gamble

Despite these risks, a fundamental question remains: Does China need its own top-tier large model?

The answer is clearly yes.

When Anthropic cut off supply, non-U.S. developers worldwide were caught off guard.

Without domestic alternatives, China's entire AI supply chain would be held hostage.

Zhipu stepped up at a critical moment, responding within 24 hours to open GLM-5.2 fully. This has strategic value beyond financial statements.

Zhipu's courage deserves recognition. Amid industry trends toward zero-margin tokens, it chose to raise prices, betting that "high-order intelligence is scarce, and whoever controls the upper bound controls pricing power."

Time will tell if this judgment is correct. But making it requires boldness.

Its technical strength is real. GLM-5.2 ranks among global top models, forming a "Coding Big Three" pattern with peers. Chinese open-source models now have pricing power in programming—a high-commercial-value field. These aren't just claims but hard-earned benchmark results.

Commercialization paths are clarifying. MaaS ARR reached RMB 1.7 billion with a 4 million-developer ecosystem. Local deployment client renewal rates hit 95%. Zhipu isn't just burning cash—it's building a sustainable model.

Of course, opinions on its HK$1 trillion valuation are divided. A 1,600x price-to-sales ratio and RMB 4.7 billion loss would be absurd in any traditional industry.

But AI can't be judged by traditional logic. Like Amazon's years of losses followed by soaring valuation, the market is betting on a distant future.

Soros said, "Financial market prices are always wrong, but errors can self-reinforce for a long time, even becoming right in the end."

Whether Zhipu's valuation is foam or vision will only be clear in three years.

But one thing is certain: China's AI needs its own flag.

Zhipu has raised it. However unsteady its steps now, this act alone deserves respect.

How far it can carry this flag—time will tell.

What's your view on Zhipu's market cap and future trajectory?

Disclaimer: This analysis is for financial hotspot discussion only. Data and references are from public queries, company announcements, and Tonghuashun IFinD. Views are for reference only and do not constitute investment or consumption advice.

#FinancialHotspots #InDepthAnalysis #BusinessFinance #InvestmentBankingCircle #ListedCompanies #AI #PrimaryMarket #IPO #Zhipu #AILargeModels

-

![]()

Caocao Mobility (2643.HK) Launches RoboX Strategy: Taking Hong Kong as the First Stop to Build a Global Intelligent Transportation Network

-

![]()

Satellite Internet: Exploring NTN Antenna Polarization

-

![]()

ByteDance's Seedance 2.5 Video Generation Model Released: Native Output Duration Doubled to 30 Seconds

-

![]()

Robot Traffic Outpaces Human Traffic: With AI Needing No Rest or Cash, Who Will Purchase Ad Slots?

-

![]()

BMW Suspends Production of All Locally-Manufactured BEV Models: Should You Grab a Bargain Now or Hold Out for the Next Generation?

-

![]()

End of CATL's Exclusive Supply! Reflections Behind HIMA's Signing with Three Battery Makers

-

![]()

A Dark Horse Emerges in the AI Vision Track: A 50-Year-Old Veteran Creates an 'AI Eye' and Establishes the 'First Physical AI Stock'

-

![]()

Alipay Builds a City, JD.com Paves the Road, WeChat Guards the Gate: The Three-Way Battle of AI Payments