Another AI 'Infrastructure Provider' Files for IPO, Backed by Alibaba, Huawei Habo, and Other Heavyweights

07/02 2026

07/02 2026

389

389

On June 30, 2026, Beijing Silicon Flow Technology Co., Ltd. (hereinafter referred to as "Silicon Flow") submitted its application to list on the Main Board of the Hong Kong Stock Exchange, intending to go public in Hong Kong through Chapter 18C. The joint sponsors for this IPO are Huatai International and Guotai Junan Securities.

Founded in August 2023 by Dr. Yuan Jinhui, the former founder of OneFlow, Silicon Flow has rapidly advanced towards a Hong Kong IPO, achieving this milestone just three years after its inception.

Investment Highlights: Silicon Flow's customer base continues to diversify, with on-premises deployment boasting a gross margin as high as 82.5%, supported by industrial heavyweights such as Alibaba and Huawei. However, a core risk is the negative gross margin, which has dipped to -24.0%, coupled with an average monthly cash burn of 14.8 million yuan and cash reserves sufficient to sustain operations for only about a year. Whether the gross margin can turn positive post-listing will be a crucial indicator of success.

Silicon Flow positions itself as "China's leading open and independent AI infrastructure provider." Its core business involves aggregating and optimizing heterogeneous computing resources from various suppliers and hardware architectures through its proprietary inference engine and computing resource orchestration system. It then supplies standardized "computing units" to customers, essentially functioning as a 'Computing Factory' in the AI era.

According to Frost & Sullivan data, based on the annual computing unit throughput in 2025, Silicon Flow is China's largest independent provider of ecological computing units and ranks among the top five overall providers, with a market share of approximately 1.5%.

In terms of platform operational data, as of April 30, 2026, Silicon Flow had over 10 million registered users.

In April 2026, the company's average daily computing unit throughput was approximately 578.5 billion units, with a single-day peak throughput of approximately 1,071.4 billion units. As of the last practical date, it had served over 13,000 enterprise customers and supported a cumulative total of over 170 models on the platform.

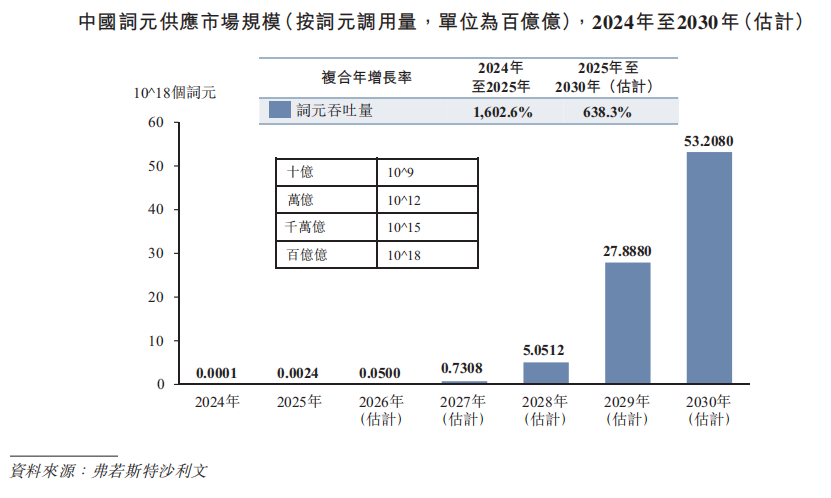

From an industry growth perspective, China's AI infrastructure market is experiencing explosive growth. Based on computing unit throughput, the market size expanded by 1602.6% from 2024 to 2025 and is projected to reach approximately 53.2 quintillion units by 2030, with a compound annual growth rate of 638.3% from 2025 to 2030.

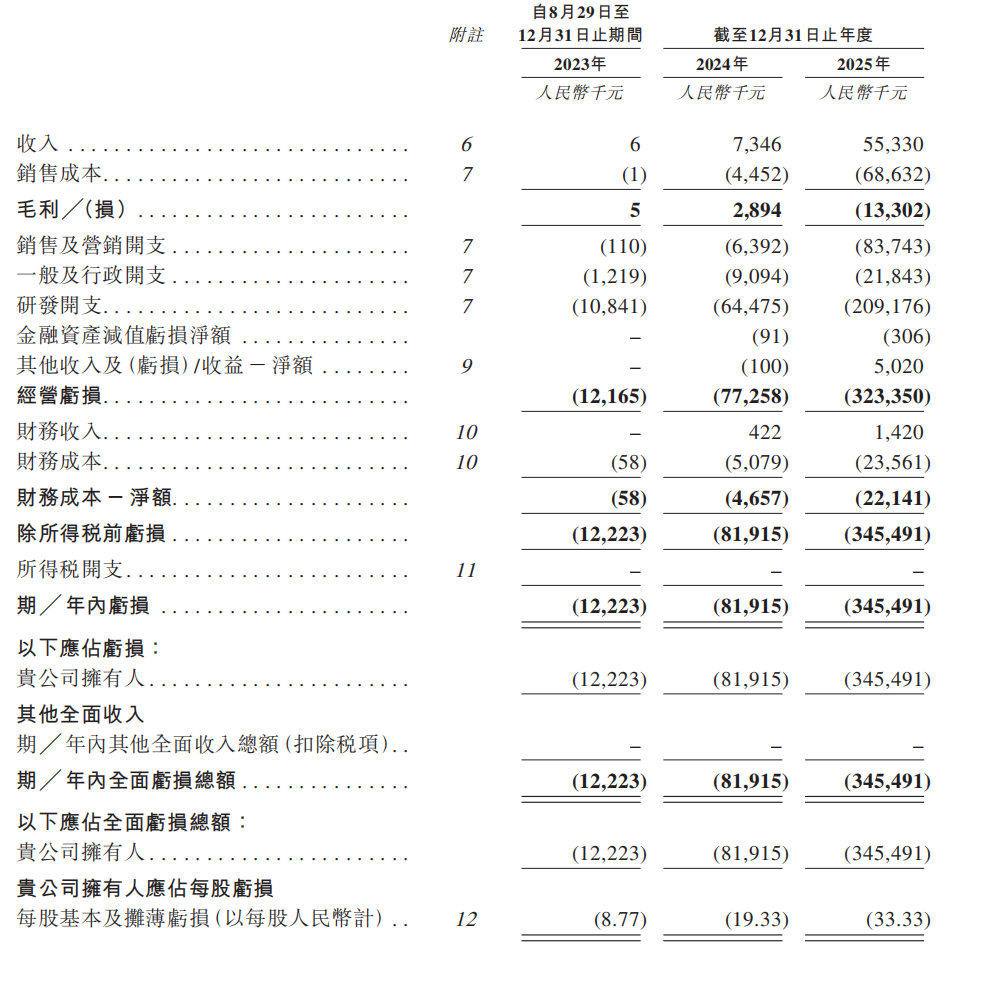

Financial Performance: Silicon Flow achieved revenues of 6,000 yuan, 73 million yuan, and 553 million yuan from 2023 to 2025, respectively. Revenue in 2025 increased by 653.2% compared to 2024.

Sales costs surged from 4.5 million yuan in 2024 to 68.6 million yuan in 2025, marking a growth of 1,441.6%.

In terms of profitability, from 2023 to 2025, Silicon Flow incurred losses of 12.2 million yuan, 81.9 million yuan, and 345.5 million yuan, respectively. Adjusted net losses were 12.2 million yuan, 54 million yuan, and 187.1 million yuan (Note: The original "187.1 billion yuan" has been corrected to "187.1 million yuan" for rationality), with losses in 2025 being approximately 4.2 times those in 2024.

During the reporting period, Silicon Flow's gross margin was 83.3% in 2023, 39.4% in 2024, and further declined to -24.0% in 2025, resulting in a gross loss of 13.3 million yuan.

Specifically, the gross loss rate for the public cloud business was -271.6% in 2024 and -119.0% in 2025, indicating significant losses.

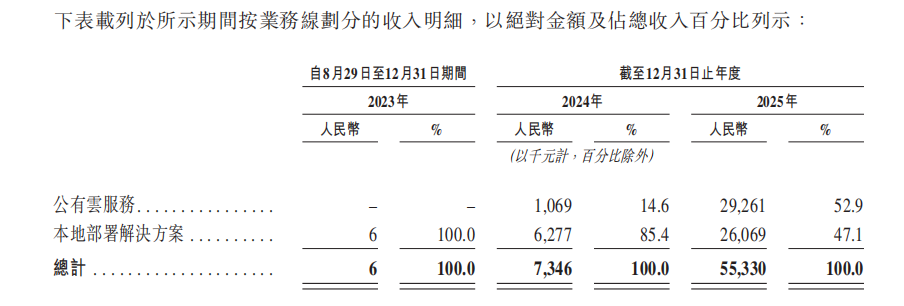

Silicon Flow's revenue is derived from two main segments: public cloud services and on-premises deployment solutions.

Public cloud services act as a gateway for user acquisition. The launch of serverless computing unit services in May 2024 marked the entry of public cloud services into a large-scale commercialization phase. Revenue from public cloud services accounted for 14.6% in 2024 and surged to 52.9% in 2025, amounting to approximately 292.61 million yuan.

Public cloud services prioritize scale over immediate profitability, with a gross loss rate as high as -119.0%. However, they play a strategic role in acquiring a massive user base, with registered users skyrocketing from 127,000 at the end of 2024 to 10.28 million by the end of April 2026.

On-premises deployment solutions are the primary source of profit. Silicon Flow deploys its inference engine and computing resource orchestration system in customers' own data centers or private computing environments, primarily targeting large enterprises and institutional customers.

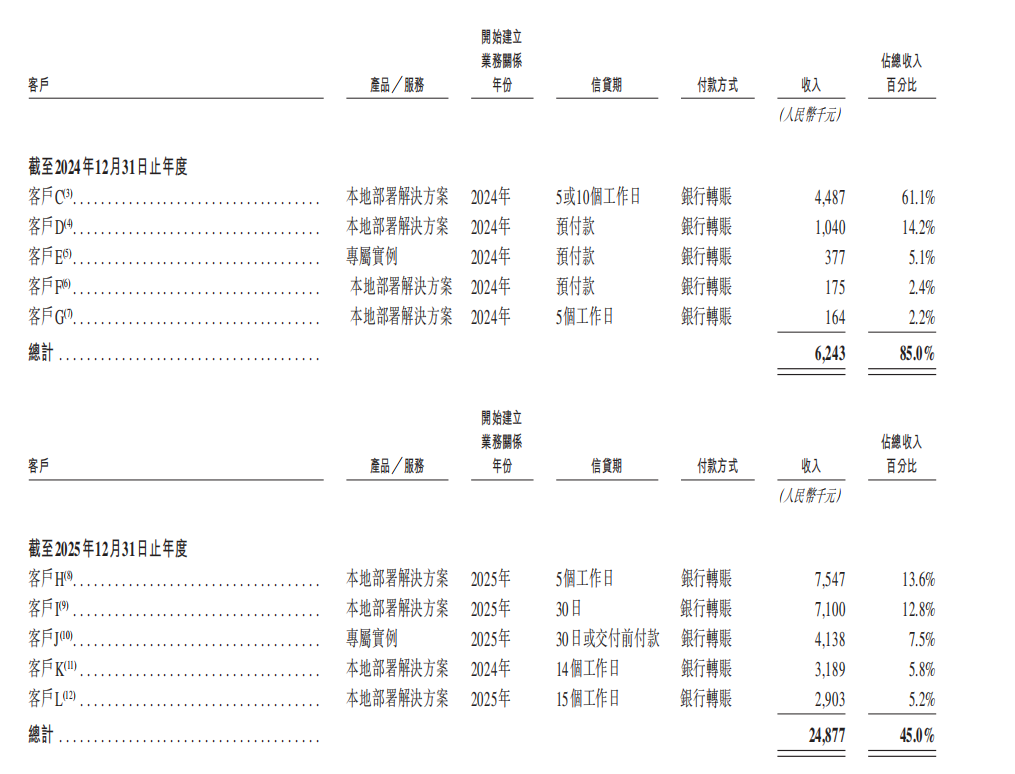

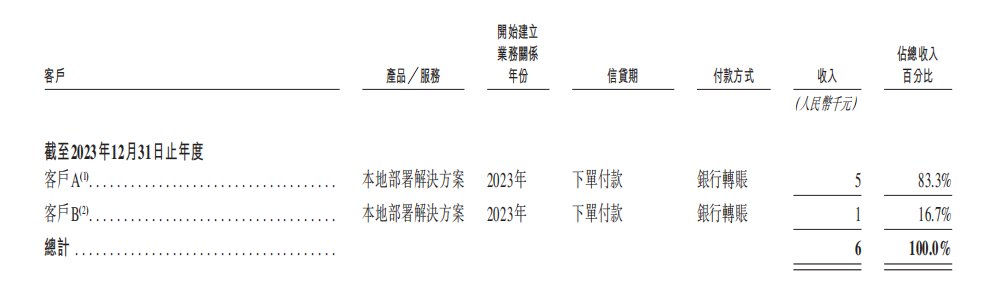

Customer and Supplier Concentration: Customer concentration has shown improvement. From 2023 to 2025, the top five customers accounted for 100.0%, 85.0%, and 45.0% of revenue, respectively. The proportion of the single largest customer was 83.3%, 61.1%, and 13.6%, respectively, indicating a continuous decline in customer concentration.

Although supplier concentration has decreased, it remains relatively high. From 2023 to 2025, the top five suppliers accounted for 100.0%, 87.6%, and 70.8% of total procurement, respectively. The proportion of the single largest supplier was 100.0%, 52.1%, and 20.4%, respectively.

In terms of trade receivables, as of December 31, 2025, they amounted to 10.6 million yuan, a significant increase from 3.6 million yuan in 2024.

As of December 31, 2025, Silicon Flow held cash and cash equivalents of 172 million yuan and time deposits of 100 million yuan. The average monthly cash consumption rate from 2023 to 2025 was 81,500 yuan, 4 million yuan, and 148 million yuan, respectively.

Operating cash outflow in 2025 was 172 million yuan. Based on the 2025 cash burn rate, existing cash reserves can only sustain operations for approximately 12-18 months.

R&D Investment and Financing History: R&D expenditures from 2023 to 2025 were 10.8 million yuan, 64.5 million yuan, and 209.2 million yuan, respectively, continuing to grow rapidly.

According to the prospectus, Silicon Flow has completed multiple rounds of financing since its establishment.

In February 2025, the company completed a Pre-A round financing of 71.48 million yuan, with a post-investment valuation of 985 million yuan. In June 2025, it secured 286 million yuan in financing, with a post-investment valuation of 2.286 billion yuan.

In March 2026, the company completed 220 million yuan in financing, with a post-investment valuation of 3.12 billion yuan. In June 2026, it completed 520 million yuan in Series B financing, with a post-investment valuation of 5.02 billion yuan. Later that same month, it completed an additional 740 million yuan in financing, with a post-investment valuation of 7.74 billion yuan, totaling 1.26 billion yuan in the two rounds. Silicon Flow has completed seven rounds of financing, with a current valuation of 7.74 billion yuan.

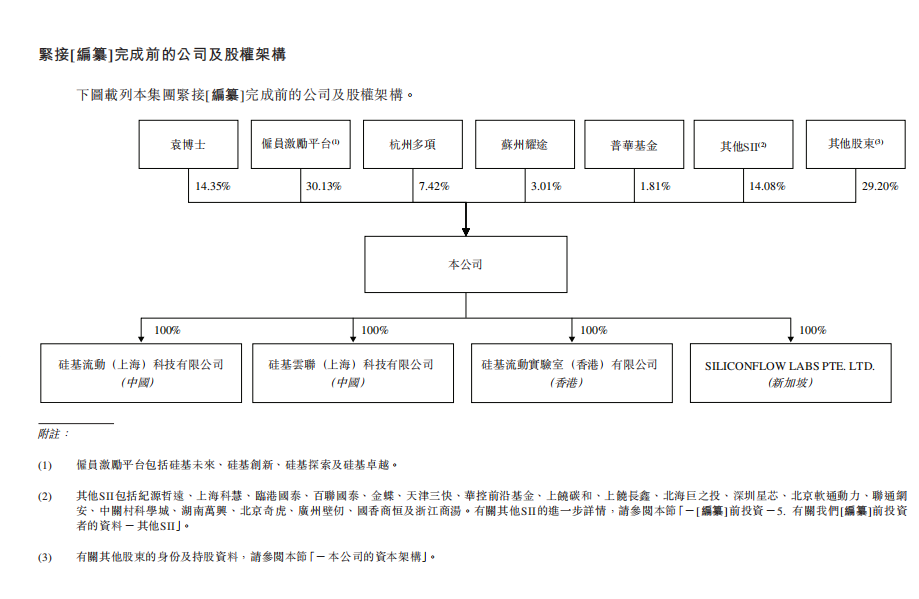

Shareholder Structure: Before the IPO, founder Dr. Yuan Jinhui and the employee incentive platform collectively controlled approximately 44.48% of the total voting rights of the issued shares.

Dr. Yuan Jinhui directly holds 14.35% of the shares. Silicon Innovation, Silicon Future, and Silicon Exploration each hold 7.85% of the shares, while Silicon Excellence holds 6.59%.

Among external shareholders, Alibaba's Hangzhou Duoxiang holds 7.42%, Huawei's Habo Technology holds 4.07%, and Beijing Innovation Works also holds shares. Additionally, Meituan, SenseTime, NIO, Zhipu, 360, and other prominent industrial players and AI investment institutions have also invested.

Management Team: Dr. Yuan Jinhui holds a Ph.D. in Computer Science and Technology from Tsinghua University and was a supervising researcher at Microsoft Research Asia. He invented the LightLDA algorithm in 2014, founded the distributed deep learning platform OneFlow in 2017, and established Silicon Flow in 2023. The core team boasts a strong technical background, but the challenge of commercial operation has just begun.

Risks: Silicon Flow faces challenges such as an unprofitable business model, uncontrollable computing resource costs, and significant upstream dependency risks. Computing resource costs account for 86.9% of revenue costs.

If computing resource prices rise, Silicon Flow may struggle to pass on the increased costs to customers, as large customers wield stronger bargaining power, making price hikes difficult.

Additionally, U.S. export controls on chips to China could impact suppliers and, consequently, have a substantial adverse effect on Silicon Flow's business.

Furthermore, the company faces risks associated with its reliance on open-source models. Most of the computing units generated and sold by Silicon Flow are sourced from open-source AI models. If these models transition to closed-source or start charging in the future, the company's business growth could be significantly hindered.

The company also grapples with issues such as an extremely short operating history and insufficient commercial validation. Founded in August 2023, the company has been in operation for less than three years. As a rapidly growing entity with a limited track record, there is considerable uncertainty regarding its ability to sustain technological advantages, retain customers, expand its market, etc.

Source/Hong Kong Stock Value Line

Material sourced from the company's prospectus

-END -

-

![]()

MathWorks: Generative AI Holds Great Potential, Yet a Trusted Toolchain is Essential for Flawless Operation

-

![]()

Small Earphones, Big Business

-

![]()

Volkswagen Slashes 100,000 Jobs, Mercedes-Benz Axes Year-End Bonuses: What’s Ailing German Auto Titans?

-

![]()

Doubao Can No Longer Offer Free Services to 345 Million Users: China's Era of Free AI Is Drawing to a Close

-

![]()

How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

-

![]()

Why are top intelligent driving players betting on reinforcement learning?

-

![]()

June 2026 Automobile Complaint Index Rankings: Persistent Problems Ignite Grievances Among Long-term Vehicle Owners

-

![]()

Avita Takes Another Stab at HKEX Listing: Facing the Urgency of Sustaining Operations Amid 11.2 Billion Yuan Loss Over Three Years