Can Apple Hold On? Prices Surge by $300 Across the Board, Cook "Outmaneuvered" by Suppliers

06/29 2026

06/29 2026

328

328

Has Apple Lost Its Bargaining Power?

Produced by | U.S.-Hong Kong Detective

Who would have thought that Apple, a company that has dominated upstream suppliers for decades with its unparalleled purchasing scale and bargaining power, would find itself in this position today?

Whenever Apple pushed for lower prices, suppliers had no choice but to accept them. However, this "supplier myth" that has persisted for over two decades has now been shattered.

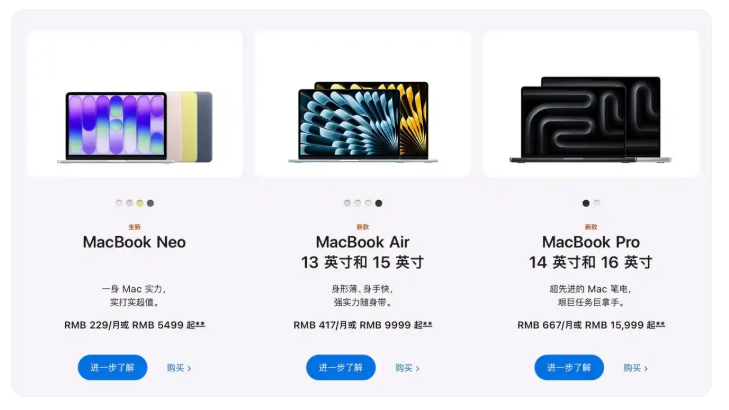

Recently, Apple unexpectedly raised prices on its global websites, increasing costs for key hardware products like MacBook, iPad, and Vision Pro by $100 to $300, with some high-end Mac Studio models seeing hikes of over $500.

According to previous reports from IT Home, Apple raised prices on 14 products, including Mac, iPad, Vision Pro, and HomePod, just the day before. The starting price of the MacBook Air increased from 8,499 RMB to 9,999 RMB, a 1,500 RMB hike. The iPad Pro's starting price rose from 8,999 RMB to 10,799 RMB, an 1,800 RMB increase.

Apple explained that the price hikes were primarily driven by rising costs of RAM and SSD storage components:

This is concrete evidence that the entire tech industry value chain is being reshaped by artificial intelligence.

1. Clash in the Clouds: Cook Calls Out, Micron Fights Back

Just a week before the price hikes, outgoing Apple CEO Tim Cook, in a rare interview with The Wall Street Journal, publicly named and criticized memory suppliers for "passing on enormous cost pressures":

"Supply has decreased, while consumer demand for devices remains high, and memory manufacturers are imposing significant price increases."

"We absolutely need memory pricing and supply to return to reasonable levels for consumer products. That’s the bottom line."

"Unfortunately, price hikes are inevitable. We’ve been doing everything possible to manage our tremendous growth and protect our customers from these increases, but the situation has become unsustainable."

This time, however, major manufacturers are no longer willing to stay silent.

Shortly after Cook’s remarks, Wall Street Journal reporter Rolfe Winkler interviewed Micron’s Chief Business Officer, Sumit Sadana.

Sadana responded to Apple’s public accusations with a blunt, face-to-face rebuttal.

He stated that during the severe memory market downturn in 2022-2023, when Micron’s gross margins even turned negative, certain "key customers" leveraged their massive negotiating power to extract "rock-bottom prices."

"We told some of these valuable, forward-looking customers at the time that their approach was unconstructive," Sadana said.

He pointed out that the extremely low prices forced upon the industry during that period directly led to significant cuts—and even shutdowns—of capital expenditures and production capacity across the memory sector in 2023.

While Sadana did not directly name Apple, it was widely understood that the customer "squeezing every last drop of blood from suppliers" was none other than Apple.

2. Apple’s "Squeeze Play" Loses Its Edge

Those familiar with Apple’s financial and supply chain operations know that the company once relied on an almost unbeatable "gross margin defense" mechanism and negotiating playbook:

• The Ultimate Scale Threat: As the world’s largest buyer of memory, Apple used its massive, stable orders to force suppliers into offering the lowest market prices.

• Multi-Sourcing Deadly Competition: Simultaneously certifying 2-3 suppliers like Samsung, SK Hynix, and Micron, pitting them against each other in a race to the bottom on pricing.

• Extreme Financial Terms: Imposing payment terms of 60-90 days or longer, shifting financial pressure upstream.

• Mandatory Annual Cost-Down Targets: Requiring yearly price reductions in contracts due to process shrinks or yield improvements.

In the pre-AI era, this system worked flawlessly. Memory was highly "commoditized," and Apple reigned supreme.

But now, pricing power has shifted decisively upstream.

This time, the memory trio (Samsung, SK Hynix, Micron) holds a strategic trump card more valuable than Apple’s: HBM.

Compared to traditional DRAM for phones and computers, HBM commands extremely high profit margins and faces overwhelming demand. Critically, companies rushing to build AI data centers are vying for HBM capacity with strong cooperation intention (willingness to collaborate).

They are even proactively signing long-term "Strategic Customer Agreements" (SCAs) with memory manufacturers, committing to "price floors" and paying massive upfront deposits to secure capacity.

Traditional memory for phones and computers has become a "residual capacity" scarcity, and Apple can no longer fully absorb or negotiate away these costs.

When manufacturers like Micron can easily sell their capacity to AI customers offering high margins and strong commitments, Apple’s traditional threat of "cancel orders if you don’t lower prices" loses its potency.

3. The "Supply Chain Master" De-mythologized?

This power shift is forcing the market to reexamine a long-held belief: Is Tim Cook’s Apple truly invincible in supply chain management?

For years, global business schools have held up Apple’s supply chain as a textbook example of excellence. Surveys show Apple’s success wasn’t merely about "bullying" smaller suppliers.

The company demonstrated unmatched expertise in joint R&D for manufacturing process yields, early investments in critical equipment (such as securing ASML’s advanced lithography machine capacity), maximizing inventory turnover, and precisely controlling upstream components.

However, behind these sophisticated management techniques lay a crucial, often overlooked driver: Apple was the market’s irreplaceable "super-single buyer."

Historically, for most semiconductor and component manufacturers, losing Apple’s orders was tantamount to bankruptcy. Under this "absolute monopoly" structure, Apple’s management artistry could shine at full strength. Suppliers tolerated razor-thin margins and harsh terms to remain on Apple’s approved vendor list.

But the AI era has obliterated Apple’s "uniqueness."

When Microsoft, Meta, Google, Amazon, and other giants entered the market with billions in AI capital expenditures, they competed for HBM, advanced manufacturing processes, and high-end packaging.

This led to a subtle shift: Apple remains a major buyer, but it’s no longer suppliers’ "only and most critical" customer.

When suppliers gain confidence that they can "survive and even profit more without Apple," the negotiating leverage built on Apple’s "absolute scale advantage" begins to erode.

When market structure fundamentally shifts and hegemonic advantages dilute, even the world’s top supply chain master has limited cards to play against upstream price hikes.

This raises the question: As the protective umbrella of scale advantages shrinks, will Apple redefine its supply chain strategy for the new era?

4. Historic Profit Surge

The memory industry is notoriously cyclical. During the 2016-2018 "DRAM supercycle," suppliers briefly regained dominance, with Micron’s gross margins hitting a record 40-45%.

This AI cycle, however, has surpassed all historical norms, with margins reaching an astonishing 85%.

Such explosive growth has raised market skepticism: Can these obscene profit levels be sustained?

For memory manufacturers, the question isn’t "how long will high margins last" but rather that, having experienced the industry’s brutal cycles firsthand, they must now ruthlessly capture every possible profit.

Memory has always been an extremely cruel, even destructive, cyclical industry. During the 2022-2023 downturn, companies like Micron faced massive losses, inventory write-downs, and negative gross margins.

At market lows, downstream customers showed no mercy, exploiting the situation to drive prices below depreciation and production costs.

For memory manufacturers, this is a survival game where "you must dig bunkers during sunny days."

Having finally regained pricing power through the AI boom, HBM capacity constraints, and advanced process node competition, why wouldn’t they push profit margins to the limit now, rather than waiting for the next downturn to be at the mercy of others?

These "obscene profit" figures are essentially "war reserves" for cyclical industries during peaceful times. Companies must seize the windfall to accumulate sufficient excess profits to cover losses and fund next-generation fab construction, which costs billions of dollars.

This explains Micron CEO Sanjay Mehrotra’s confidence.

He publicly stated that new long-term agreements (LTAs) will ensure Micron’s future gross margins "far exceed previous cyclical peaks."

This signals that memory manufacturers are no longer content to be bit players who "make small profits in good times and lose half their lives in bad times." Instead, they aim to use this structural shift to completely rewrite the rules of the game.

5. The Edge AI Dilemma Amidst AI Prosperity

The memory price hikes have triggered a chain reaction with profound second-order effects:

Cloud AI development is now cannibalizing edge AI progress.

The market narrative claims "AI will drive a new wave of smartphone and PC upgrades." But physical limitations persist:

• To run local AI models, smartphones need larger, faster memory.

• Cloud AI is consuming all memory capacity, causing costs to skyrocket.

• Higher costs lead to significant price hikes for smartphones and computers (e.g., iPads rose by $100-$200).

• As devices become more expensive, consumer replacement cycles (already extended to ~3.7 years) will lengthen further.

This creates a vicious cycle: More aggressive cloud infrastructure builds → Higher upstream component costs → Harder to sell end devices → Slower edge AI adoption.

For two decades, Apple masterfully "digested" all costs and risks upstream through flawless supply chain management.

This time, the structural power shift wrought by the AI tsunami means even mighty Apple must accept this "AI tax" and pass it directly to global consumers.

Disclaimer: This article is based on the public company attributes of listed companies. U.S.-Hong Kong Detective strives for objectivity and fairness in its content and viewpoints but does not guarantee accuracy, completeness, or timeliness. The information and opinions expressed herein do not constitute investment advice. U.S.-Hong Kong Detective assumes no responsibility for any actions taken based on this article.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?