Beijing Kicks Off Six Vehicle-Road-Cloud Integration Projects with RMB 2.8 Billion Investment, Just a Fraction of the Grand Plan

07/06 2026

07/06 2026

553

553

This is the 82nd original article from ThinkAI Community.

Approximately 1,810 characters in total, estimated reading time: 6 minutes.

Beijing has been bustling with activity lately.

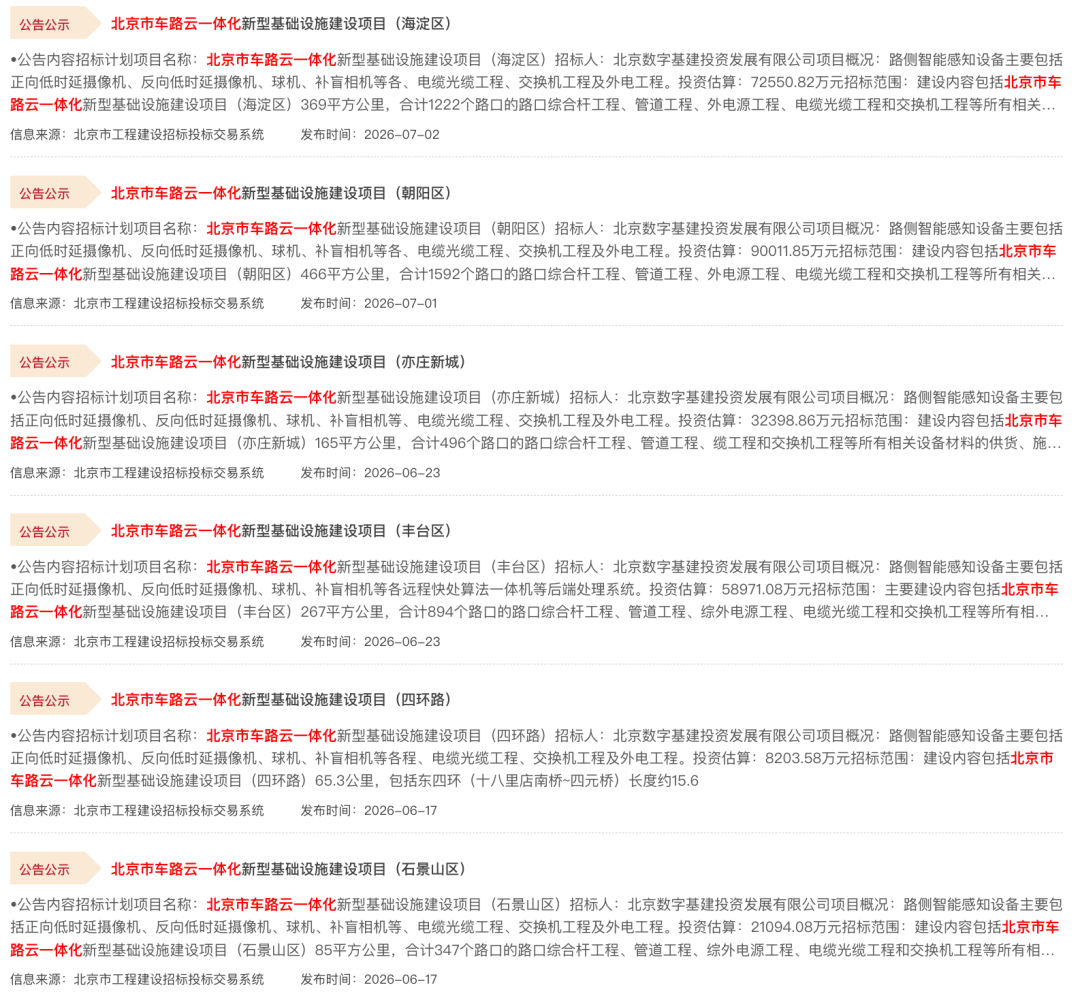

In early July, bidding plans for vehicle-road-cloud integration projects in Chaoyang and Haidian districts were unveiled, amounting to a total investment of RMB 1.63 billion.

Rewinding to June, similar projects were also initiated in Shijingshan, the Fourth Ring Road, Fengtai, and Yizhuang New City, bringing the total to six projects with a cumulative investment of RMB 1.21 billion.

In aggregate, RMB 2.84 billion has been earmarked for these six projects, spanning five districts plus one ring road, encompassing 4,551 intersections, and covering an area of 1,419 square kilometers.

While the scale and density may not be immediately clear, they are indeed significant on a national level.

How Extensive Are the Six Projects? Let's Delve into the Numbers

First, let's clarify the specifics of these six projects. I've compiled the key data here:

All data sources are derived from the bidding plan announcements on the Beijing Public Resources Trading Services Platform, with the bidding targets being the zonal sections of the "Beijing Vehicle-Road-Cloud Integration New Infrastructure Construction Project."

Several intriguing details emerge.

Firstly, all bidders are the same entity—Beijing Digital Infrastructure Investment and Development Co., Ltd. Rather than each district conducting its own bidding, it is uniformly managed by a municipal-level platform.

What does this signify? It indicates a city-wide, unified approach with standardized criteria, centralized procurement, and coordinated construction, rather than scattered pilot projects across various districts.

Secondly, the construction content is highly standardized. The descriptions for each project are nearly identical: roadside sensing (including forward and reverse low-latency cameras, radar-vision integrated machines, blind-spot cameras, edge computing nodes) + backend processing (intelligent sensing engines, video analysis, data distribution nodes, accident rapid response algorithms) + supporting infrastructure (integrated poles, pipelines, optical cables, external power supply).

These projects are no longer in the exploratory phase; they are at the engineering stage of mass replication.

Thirdly, Yizhuang stands out somewhat. Covering the same 165 square kilometers and 496 intersections, but with sensing equipment installed at only 100 intersections and an investment of RMB 320 million, it is the smallest among the six projects.

Why? Because Yizhuang was Beijing's earliest area to develop vehicle-road-cloud integration, with several phases already completed. This current phase focuses on adding increments and upgrading standards.

RMB 2.8 Billion Is Just the Tip of the Iceberg; What's the Total Investment?

If you think RMB 2.8 billion is already substantial, let me inform you that it's just a small fraction of Beijing's overall vehicle-road-cloud investment plan.

The initial total investment plan, announced in May 2024, was RMB 9.939 billion, covering 13 districts, 2,324 square kilometers, and 6,050 intersections across the city.

The funding is sourced from 70% government investment and 30% self-financing by enterprises.

By 2025, continuous coverage of 600 square kilometers has been achieved. The cloud control platform processes approximately 420TB of data daily and connects to about 1,100 test vehicles.

Now, in 2026, the combined coverage of Chaoyang, Haidian, Fengtai, Shijingshan, and Yizhuang New City reaches 1,419 square kilometers and 4,551 intersections, with an investment of RMB 2.84 billion.

Note that these are newly released bidding sections, part of the phased implementation of the RMB 9.9 billion total investment plan, not additional new projects.

Let's do the math: The total investment of RMB 9.9 billion covers 2,324 square kilometers and 6,050 intersections. This equates to approximately RMB 4.26 million per square kilometer and about RMB 1.64 million per intersection.

What does this cost level imply on a national scale?

To be honest, it's not inexpensive, but it's also not unreasonable.

Because each intersection requires a significant amount of equipment: low-latency cameras, radar-vision integrated machines, edge computing nodes, intelligent sensing engines, plus integrated poles, pipelines, optical cables, and external power supply matching (supporting infrastructure). The cost for a complete setup easily reaches tens of thousands of RMB.

Moreover, Beijing has a unique characteristic—high construction costs.

Consider excavating pipelines and erecting integrated poles on main roads in Chaoyang District, involving traffic diversion, nighttime construction, and coordination with various property rights units. These hidden costs are much higher than in second- and third-tier cities.

Why Beijing, and Why Now?

I believe there are three driving forces behind this wave of concentrated bidding.

Firstly, policy imperatives.

In early 2024, the Ministry of Industry and Information Technology and four other departments issued the "Notice on Conducting Application Pilots for 'Vehicle-Road-Cloud Integration' of Intelligent Connected Vehicles," announcing 20 pilot cities, with Beijing ranked first. The pilots have specific assessments and timelines, so construction progress cannot lag.

Secondly, the imminent rollout of L3 autonomous driving.

At the end of last year, pilot programs for L3 autonomous driving access and road operation were launched, and this year, several automakers have successively obtained L3 test licenses.

However, L3 cannot rely solely on vehicle intelligence, especially in complex urban scenarios. Roadside sensing and cloud control platforms provide vehicles with a "god's-eye view"—enabling visibility of blind spots, prediction beyond line-of-sight, and rapid accident response.

Vehicle-road-cloud integration is not just an enhancement; it is a necessary condition for the large-scale deployment of high-level autonomous driving.

Thirdly, the need for industrial implementation.

Beijing has long aimed to build a "world-class intelligent connected vehicle industry hub," but simply having demonstration zones and test fields is insufficient. Real construction projects and sustained orders are essential for the survival and growth of enterprises in the industrial chain.

The release of RMB 2.8 billion in projects benefits the entire chain:

Upstream: Cameras, millimeter-wave radars, radar-vision integrated machines, edge computing devices, fiber optic cables.

Midstream: System integrators, Zhilu OS, sensing algorithms, cloud control platforms.

Downstream: Test operations, mobility services, logistics and delivery.

Looking at Yizhuang, companies like Baidu, Pony.ai, and Baidu Apollo Go are already operating there. The more complete the infrastructure, the larger their operational scope can expand, and the faster commercialization can proceed.

Another detail that many may have overlooked: Among these six projects, the bidding plans for Chaoyang and Haidian were only released in early July, with formal announcements expected in early August; for Fengtai, Yizhuang, and the Fourth Ring Road, they were released in mid-to-late June, with formal announcements expected in mid-to-late July.

What does this mean? From now until early August, Beijing will intensively release formal bidding announcements for vehicle-road-cloud projects.

These are just six bidding sections; there may be more from districts like Shunyi, Changping, and Daxing later.

For those in the industry, the next one to two months represent a critical window for securing projects.

From an industry observation perspective, information on who wins the bids, the bid prices, and which equipment and solutions are used will truly reveal Beijing's technological approach and industrial landscape for vehicle-road-cloud integration.

In fact, debates about vehicle-road-cloud integration have never ceased.

Some argue that "the vehicle intelligence route is the right path, and vehicle-road-cloud integration is a capital-intensive bottomless pit," while others say that "China's national conditions necessitate the vehicle-road coordination route."

I believe it doesn't have to be an either-or situation. Vehicle intelligence and vehicle-road-cloud integration are not substitutes but complements; the vehicle handles "onboard intelligence," while vehicle-road-cloud integration provides "roadside safety redundancy and beyond-line-of-sight capabilities."

Beijing's RMB 2.8 billion, six projects, and 4,551 intersections are not the finish line but just the starting point for a new round of construction.

What will Beijing look like when the entire city's 2,324 square kilometers and 6,050 intersections are completed?

Perhaps by then, "smart vehicles, intelligent roads, and powerful clouds" will truly become more than just a slogan.

All content in the article is sourced from publicly available information.

Written casually in my spare time for sharing, representing only my personal views.

-

![]()

When AI Begins to Reshape Infrastructure: A Reshuffle in the U.S. Cloud Market

-

![]()

Tencent’s Strategic Maneuver: Selling Kuaishou, Investing in Kling

-

Has the Semi-Annual Achievement Rate Dipped Below 40%? Can AIVA Circumvent the 'Multi-Shareholder Death Spiral'?

-

![]()

Stepping Out of the Humanoid Robot Concept: Why is Autonomous Driving the First Large-Scale Implementation Track for Physical AI?

-

![]()

WPS: Criticism Warranted, Yet Open to Improvement

-

![]()

Farewell to Image-First: Robotic Vision is Undergoing a Fundamental Reconstruction

-

![]()

Former Huawei 'Genius Teen' Encounters a 'Hiccup' in DeepSeek's Recruitment Process

-

![]()

WPS Remains Unchanged; It’s the Users’ Perception of “Free” That Has Shifted