Profit Balancing Act for Handheld Imaging Device Manufacturers Amidst Price and Cost Wars

03/12 2026

03/12 2026

636

636

By 2026, the ripple effects of AI are spreading.

On one hand, its progress has significantly boosted the popularity of smart devices, such as the smart glasses market, which saw a new inflection point this year. On the other hand, the AI industry's development is consuming resources from sectors like storage, squeezing products such as smartphones and handheld smart imaging devices that also rely on these resources.

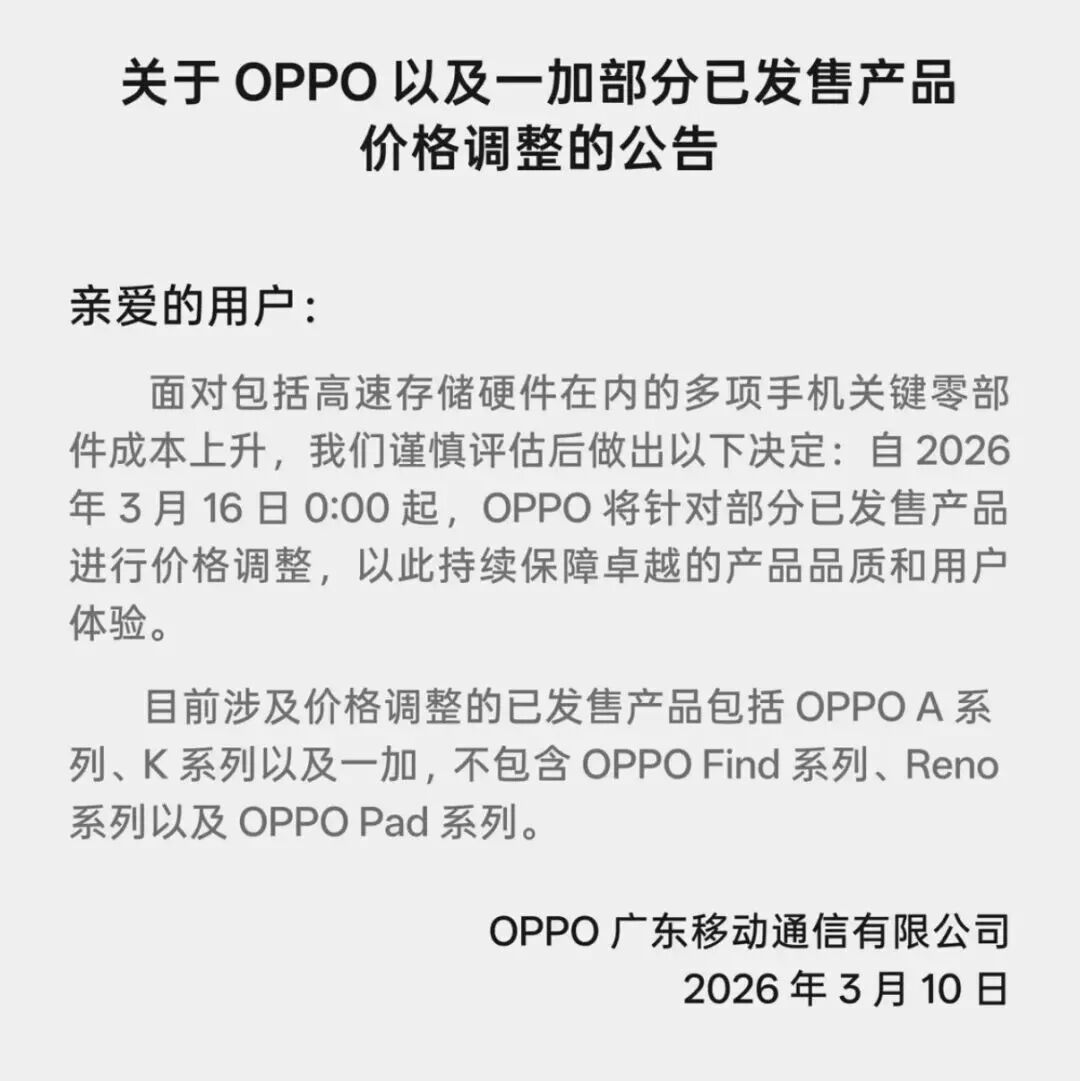

In the smartphone sector, major manufacturers have clearly signaled price hikes, with OPPO, for example, issuing a price increase notice on March 10.

(Image source: OPPO)

The same trend applies to the more niche market of handheld smart imaging devices. According to market research released by Jiutian Zhongtai on March 9, the global revenue scale of handheld smart imaging devices (excluding gimbal cameras) nearly doubled year-on-year last year, with action cameras, panoramic cameras, and small wearable sports cameras all advancing in tandem. However, this sector has been affected by the ripple effects of the AI industry.

This is primarily reflected in market competition, where flagship models from leading manufacturers have proactively lowered prices on e-commerce platforms, returning to a focus on "cost-effectiveness." However, at the same time, the cost of core components like memory chips has risen significantly, with DRAM spot and contract prices surging in a short period, impacting the overall bill of materials (BOM) for devices. The combination of price and cost wars has created an unavoidable "scissor gap" for the entire industry.

DJI, GoPro, and Insta360 are widely recognized as the top three players in the industry. According to Jiutian's estimates and publicly available industry information, despite facing the same environment of falling prices and rising costs, these three manufacturers do not operate under identical conditions and have thus adopted different approaches to balance profitability.

Unexpected Dual Pressures

Since the second half of 2025, competition in handheld smart imaging devices has centered on flagship new products.

(Image source: Luotu Technology)

In the Chinese e-commerce market, the DJI Action 5 Pro became the top-selling action camera, while the GoPro Hero 13 led overseas markets. In the panoramic camera segment, both DJI's Osmo 360 and Insta360's flagship models saw sales highly concentrated on the latest generation, with consumers clearly favoring new over old models.

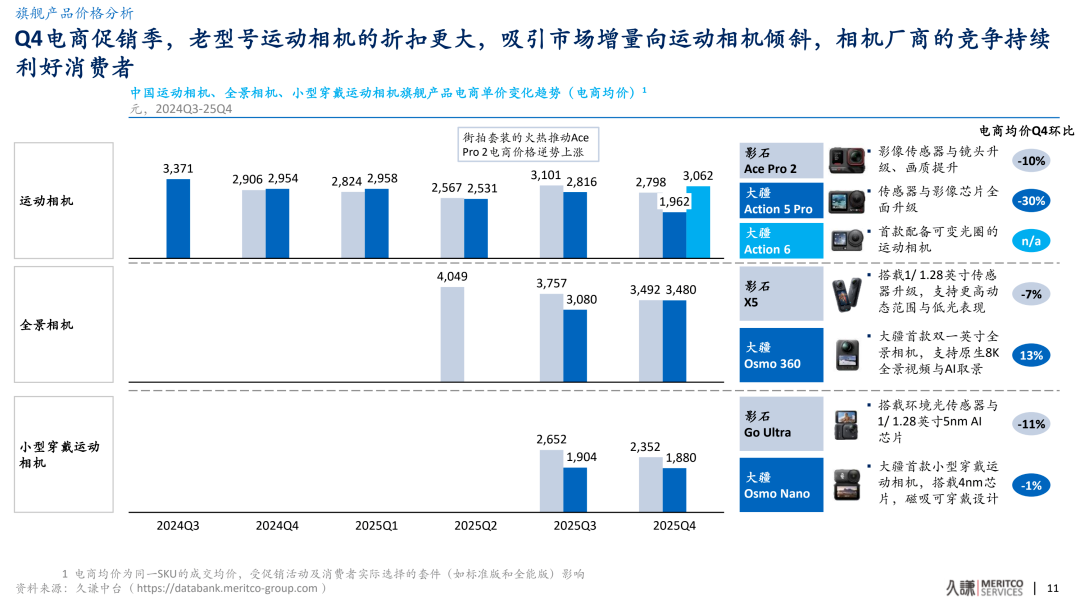

Leading brands have established a strong market presence around their flagship models but are also engaging in direct price competition. This is reflected in data showing that in Q4 2025 and beyond, these companies offered deeper discounts on flagship models during e-commerce promotions. Additionally, the launch of new small wearable cameras created internal competition within the same brand across different product forms.

(Image source: Jiutian Zhongtai)

As a result, unit selling prices have struggled to rise and have even been forced downward, with flagship models becoming "shock troops" for capturing market share rather than the most profitable products.

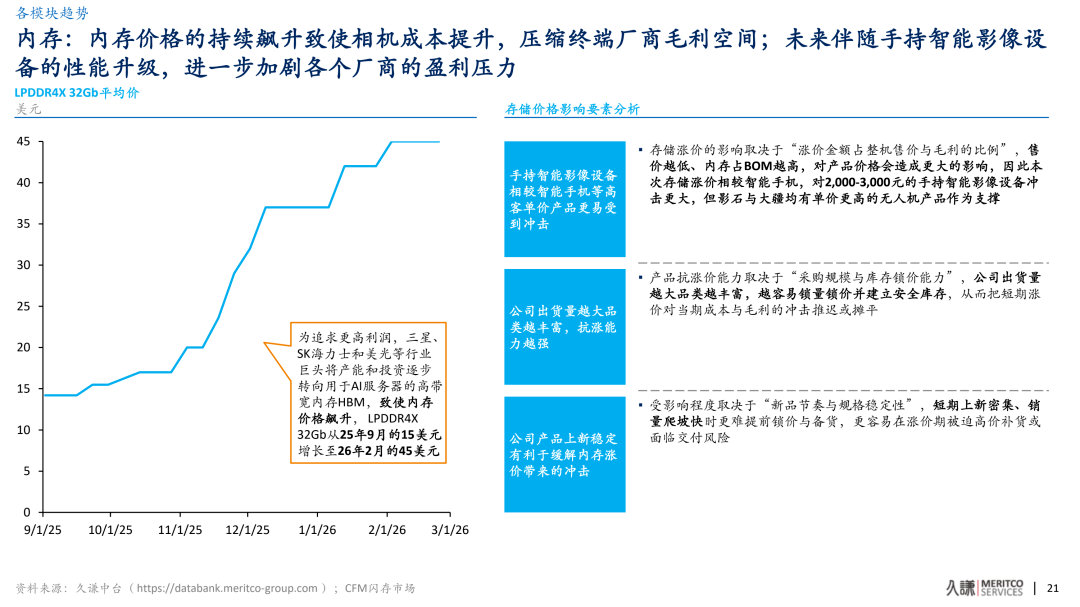

This would not have been a major issue, but in early 2026, global DRAM memory chips entered a new cycle of price hikes. Data released by TrendForce in February showed that spot prices for memory chips have surged by over 300% in the past three months, with first-quarter contract prices nearly doubling quarter-on-quarter.

Memory manufacturers such as Samsung and SK Hynix have shifted more advanced production capacity toward high-bandwidth memory and server memory, significantly reducing the effective supply of consumer-grade DRAM. Supply and demand are not expected to rebalance until around 2027, posing a dilemma for handheld smart imaging device manufacturers.

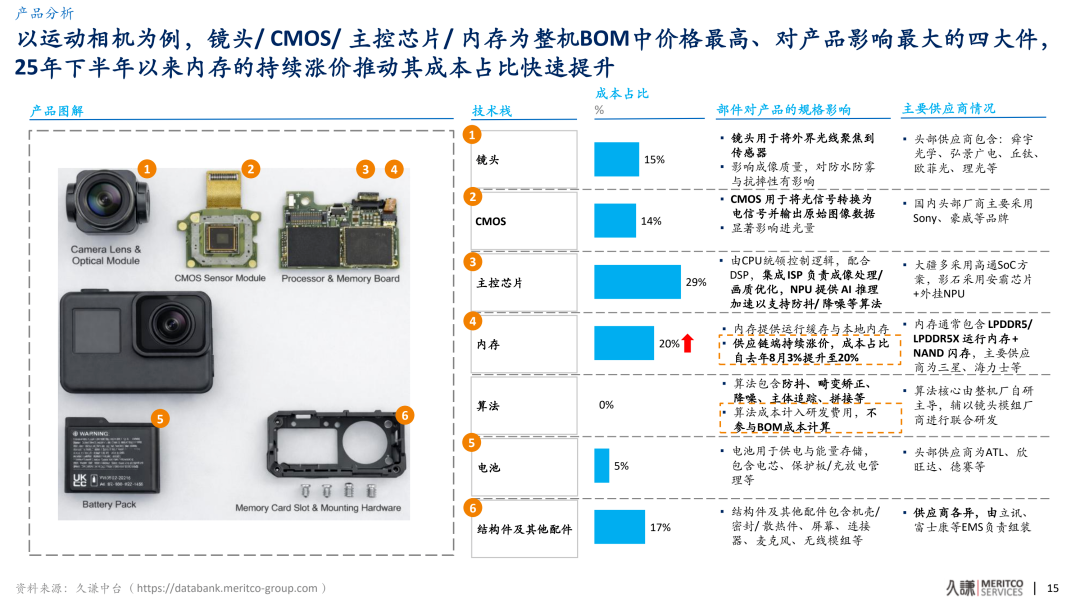

On one hand, these products are highly focused on imaging capabilities, with 4K/8K video recording, panoramic stitching, stabilization, and AI algorithms all relying on high-speed, large-capacity storage. Any reduction in storage performance would noticeably degrade the overall user experience, unlike smartphones, which can more easily adjust specifications.

(Image source: Jiutian Zhongtai)

On the other hand, annual shipments of handheld devices are in the tens of millions, lower than those of smartphones and PCs, making it difficult to secure equal bargaining power in upstream procurement and increasing sensitivity to price fluctuations.

In fact, according to Jiutian's research, while the markets for action cameras, panoramic cameras, and small wearable sports cameras each had their own dynamics in Q3 and Q4 of last year, the post-Q4 promotions coincided with this wave of memory price surges, intensifying profitability pressures on manufacturers.

(Image source: Jiutian Zhongtai)

Among the three major brands, DJI is not publicly listed, so its financial data is unavailable. GoPro, which is listed, has struggled to compete with DJI and Insta360 and has been operating at a loss. Meanwhile, Insta360's disclosed 2025 data shows that its gross margin declined from around 53% in the first three quarters to about 48% in the fourth quarter. While revenue growth nearly doubled year-on-year in Q4, net profit increased by only 13%.

In most cases, "increasing revenue without increasing profits" is the result of competitive or cost pressures. Given its market position, Insta360 is clearly affected by the storage industry. The company also noted in its 2025 earnings preview that it has made strategic investments in new products like handheld gimbal cameras. However, factors such as raw material price fluctuations and intensifying market competition pose significant challenges to its profitability.

Against this backdrop, the differences among leading manufacturers are more evident in how they address this unexpected cost gap.

The "Three Heroes" Battle Costs

From a business structure perspective, DJI has the broadest product lineup and the largest scale among the three. Action cameras are just one part of DJI's imaging business, which also includes drones and gimbal cameras, areas with higher gross margins and larger shipment volumes. DJI's overall revenue base is also far larger than that of manufacturers focused solely on handheld imaging.

(Image source: DJI product promotion)

From a manufacturing standpoint, this gives DJI two advantages.

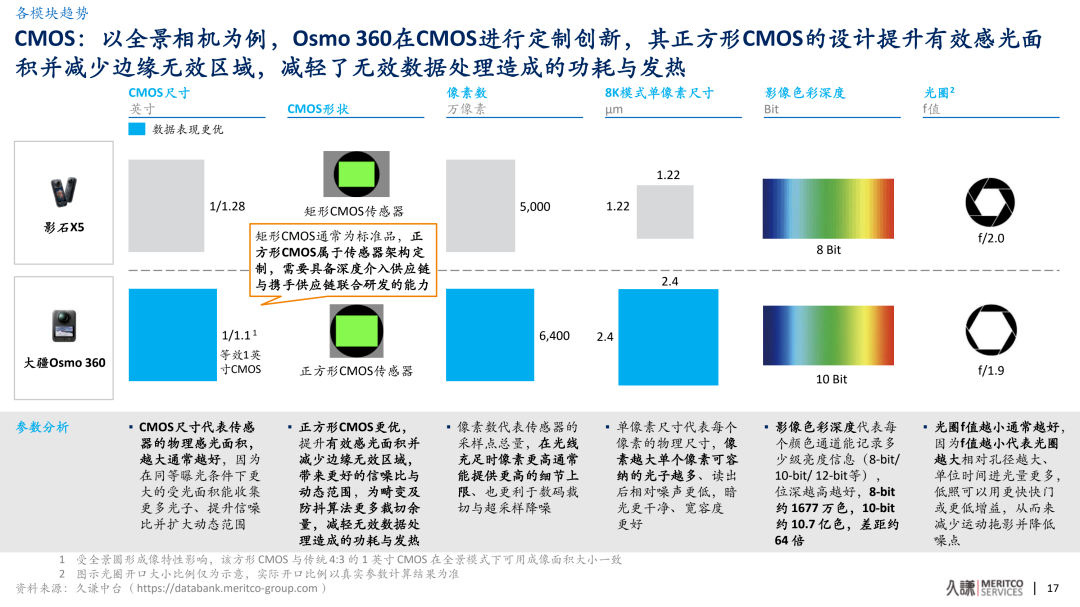

First is its scale and product diversity, which directly translate into supply chain leverage and cost adjustment flexibility. For example, DJI can negotiate long-term partnerships and custom development with upstream suppliers of lenses, CMOS sensors, storage, and main controllers based on larger order volumes, driving the development of specialized components and supporting relatively stable pricing through differentiated features.

Second, DJI has thicker profit margins from its drone and other high-margin businesses, providing a stronger buffer at the group level when its handheld imaging product line needs to lower prices to gain market share. This allows DJI to be more proactive in price wars: it can consolidate market share through strategic price reductions on flagship models while maintaining certain gross margins through high-end segments and professional user groups.

Jiutian's analysis notes that DJI's use of custom solutions for key components like CMOS sensors and lenses is built on sustained investment and large shipment volumes. For standard components like memory, DJI also benefits from its overall scale, securing more favorable procurement terms and partially offsetting price hike risks.

(Image source: Jiutian Zhongtai)

Insta360, one of the domestic leaders, operates in a more focused niche, with its business highly concentrated on handheld smart imaging devices, particularly panoramic cameras and small wearable sports cameras, while entering the action camera market relatively late. This makes it more cost-sensitive.

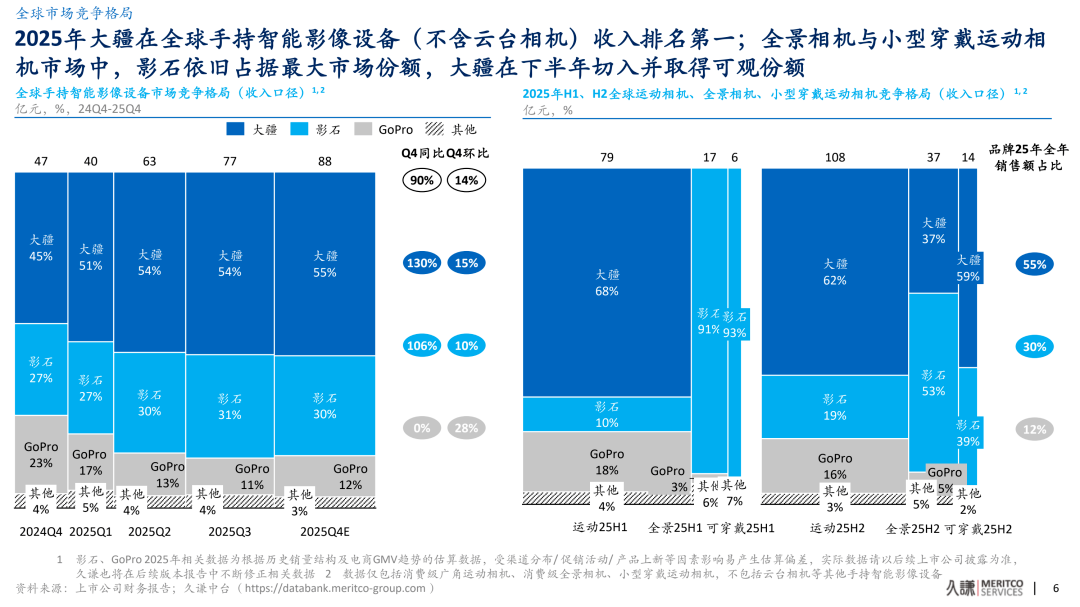

Jiutian's research shows that Insta360 holds a clear advantage in the panoramic and wearable camera segments while gaining share in action cameras, reaching an overall market share of around 30%, ranking second globally.

(Image source: Jiutian Zhongtai)

The benefits of this focus are clear brand positioning, rapid product iteration, and concentrated innovation. For example, Insta360 chose to add an external AI chip to its main control architecture to enhance on-device AI processing capabilities, enabling higher real-time performance in algorithms like in-camera panoramic stitching and image enhancement, aligning with its product philosophy of "allocating resources where they matter most."

However, from a cost structure perspective, this high-computing-power, algorithm-intensive approach makes Insta360 more sensitive to changes in chip and memory prices.

UBS predicted in a previous research report that due to rising prices of SoCs, DSPs, and DRAM chips in 2026, Insta360's BOM costs would increase by 9% year-on-year, dragging its gross margin down by 4 percentage points. Given the intense competition in the handheld imaging industry and the lack of significant pricing opportunities, cost increases are more likely to impact profits.

Additionally, since Insta360's revenue primarily comes from handheld imaging products, it has limited other businesses to absorb memory and chip price hikes. This means Insta360 must digest this cost impact [translates as "shock" or "impact"] internally by optimizing configurations, controlling expenses, and increasing per-customer value. Attempts at product differentiation, accessories, and service extensions may influence its profit structure over the next two years.

(Image source: Insta360 product promotion)

Compared to the domestic leaders, GoPro's situation remains uncertain.

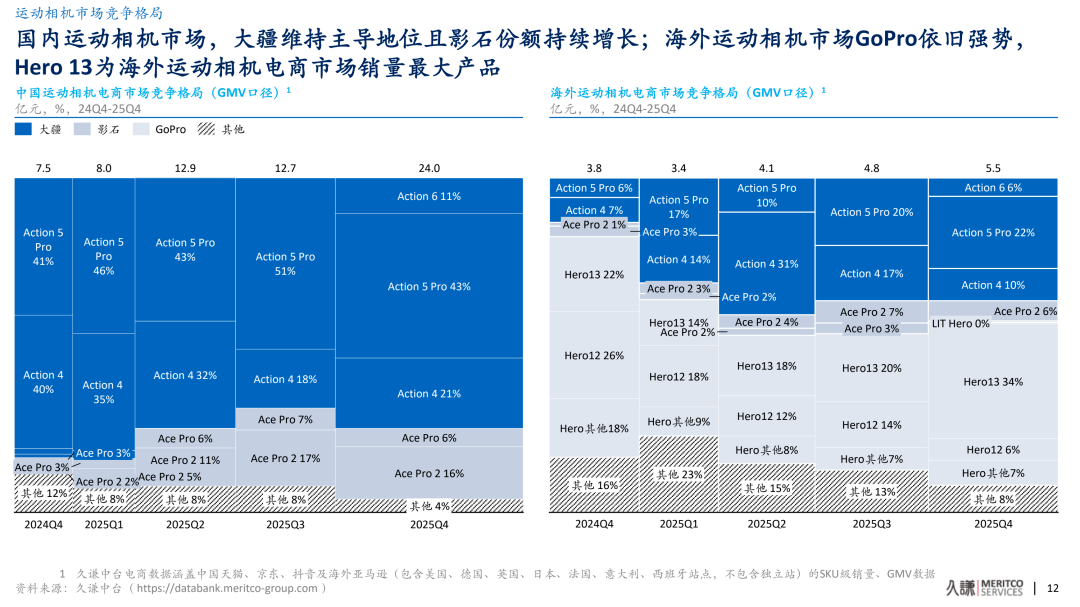

As one of the pioneers of the action camera category, GoPro still enjoys strong brand recognition and a well-established channel system overseas. Jiutian's e-commerce data shows that the Hero 13 remains one of the top-selling action camera SKUs overseas, maintaining high popularity in mature markets like Europe and the U.S.

(Image source: Jiutian Zhongtai)

However, from a competitive standpoint, GoPro is under dual pressure: on one hand, DJI continues to launch competitive products in the action camera segment, strengthening its position in China and globally; on the other hand, Insta360's breakthroughs in panoramic and small wearable cameras are eroding some of the action and creative scenarios previously dominated by GoPro.

In this context, GoPro has already made multiple pricing adjustments in recent years, with some product lines nearing their profitability bottom line [translates as "bottom line"] in terms of terminal pricing. Combined with external factors like tariffs, GoPro's overall profitability is under pressure. Recent financial data shows that GoPro incurred a cumulative loss of $93.5 million last year.

(Image source: Xueqiu)

Against this backdrop, discussing the impact of rising memory and core chip costs on GoPro alone is almost meaningless, as its room for further price reductions is relatively limited. Instead, GoPro is more likely to focus on streamlining its product lineup, enhancing flagship differentiation, and increasing subscription service penetration to stabilize average selling prices and per-unit gross margins, rather than engaging in excessive price competition with DJI and Insta360.

Currently, GoPro is building a subscription service as its second growth engine, generating recurring revenue through cloud storage, content services, and more. While this expansion provides a buffer when hardware gross margins are under pressure, it cannot fully offset hardware cost increases.

Finding a New Equilibrium Amid the Scissor Gap

It is foreseeable that memory and core chip prices are unlikely to return to their previous lows in the short term, while price competition among leading manufacturers around flagship models will not cool down quickly. For the entire handheld smart imaging industry, the superposition [translates as "combination"] of price and cost wars will be the norm rather than an exception in the coming period. Achieving profit balance may no longer be possible through a single approach but will require a multi-pronged strategy.

First, continue to leverage scale and supply chain collaboration to secure better cost positions. DJI's approach shows that sufficiently large order volumes, combined with custom development, can create favorable conditions for key components. GoPro and Insta360, whose core products have significant scale influence, can also enhance their bargaining power in memory and chip procurement through new product rhythms, product mixes, and medium- to long-term cooperation agreements.

Second, refine product structure management, expanding profit sources from "single hardware gross margin" to a combination of "hardware + accessories + services." Insta360 drives revenue through accessory bundles like street photography kits for panoramic cameras, while DJI and GoPro enhance long-term value through cloud services and membership subscriptions, all attempting to dilute per-unit gross margin fluctuations with more comprehensive per-customer contributions.

(Image source: GoPro)

Third, use technological and architectural adjustments to offset some hardware costs. This includes reducing storage requirements through more efficient video encoding, lowering reliance on extreme-specification components through algorithmic optimizations, and re-evaluating the cost-benefit balance of external versus integrated architectures as AI chips are gradually incorporated into main control systems.

In summary, manufacturers need to find the right pace between short-term profit pressures and long-term investments. From a consumer experience perspective, competition in handheld smart imaging has shifted from simple hardware specifications to a comprehensive contest of "hardware + algorithms + ecosystem," capabilities that often require sustained investment.

In an environment where cost and pricing pressures coexist, the challenge for all players is to maintain current financial health without compromising future product competitiveness.

Source: Songguo Finance

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan