Wishes Thwarted: Insta360 Under Renewed Pressure as Price Hikes Remain Out of Reach

03/12 2026

03/12 2026

597

597

Source: YuanMedia

As 2026 unfolds, supply chain challenges, particularly the volatility in upstream costs such as memory, have emerged as an unavoidable hurdle for numerous domestic smart hardware manufacturers.

Counterpoint Research forecasts that memory chip prices will surge by 40% to 50% on a quarter-on-quarter basis in the first quarter of 2026, with an additional increase of approximately 20% anticipated in the second quarter.

Handheld imaging devices, which heavily rely on storage performance and have relatively limited procurement volumes, are among the most severely affected segments. This upstream component price surge not only directly escalates production costs for terminal manufacturers but also triggers a reshuffling of the industry's competitive landscape.

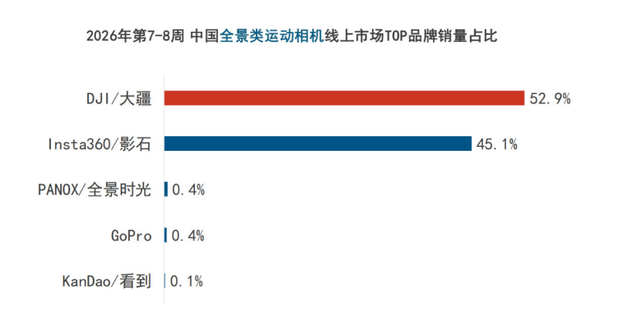

Currently, the handheld smart imaging market is dominated by three key players—DJI, GoPro, and Insta360—with smaller brands supplementing the market and smartphone manufacturers encroaching upon it. The persistent impact of rising memory prices is accentuating the strengths and weaknesses of these various competitors.

It can be argued that fluctuations in the component cycle are serving as a litmus test for a company's core competitiveness, and a new wave of reshuffling in the handheld smart imaging market has already commenced.

01

Price Hikes Reshape Industry Dynamics

The current frenzied surge in memory chip prices is not merely a simple cost pass-through but a comprehensive reconfiguration from upstream supply chains to downstream consumer markets, rewriting the competitive playbook for the handheld smart imaging sector.

According to market research firm DRAMeXchange, prices for generic DRAM have been on the rise for 11 consecutive months since April 2025, reaching their highest average level since surveys began in June 2016 in February.

In this price surge, the ability to withstand risk varies significantly among market players. Leading companies leverage their supply chain advantages to mitigate cost increases, while mid-tier players find themselves caught in the middle, facing pressure from both ends.

Overall, DJI, the market leader across multiple categories, has further solidified its supply chain influence amid the price hikes. As a top player in handheld smart imaging, DJI has forged long-term strategic cooperation agreements with leading memory manufacturers such as Samsung, Kioxia, and Yangtze Memory Storage Technology, granting it significant advantages in procurement pricing and supply stability.

This means that when faced with cost pressures from rising memory prices, DJI can negotiate further with its supply chain partners using its market sales and brand influence, avoiding the need to pass on the pressure through price hikes. Instead, it can potentially capture more market share by lowering prices or maintaining them.

Recently, LuoTu Technology released its

Image Source: LuoTu Technology

Another report by JiuQian ZhongTai on March 9 noted that sustained innovation on the supply side, coupled with rapid market growth driven by popular activities like skiing, cycling, and surfing, led to a 96% year-on-year revenue increase in the 2025 handheld smart imaging market. Action cameras accounted for 70% of the market, making them the largest segment. DJI maintained its position as the top global revenue earner in handheld smart imaging devices (excluding gimbal cameras) thanks to its leading market share in action cameras.

For professional imaging manufacturers like Sony, their full-industry-chain advantages enable them to expand barriers in the high-end market. Cost pressures from rising memory prices can be absorbed through premium pricing for high-end products, further solidifying their position in professional imaging.

In contrast, Insta360, a professional imaging manufacturer in a high-growth phase, has become the most typical mid-tier player in this price surge.

It faces insurmountable barriers from DJI and Sony in the high-end market, mature user barriers from GoPro in the core action camera market, and cost pressures from rising memory prices that further constrain its strategic maneuvering space.

UBS predicts that due to price hikes in SOC, DSP, and DRAM chips in 2026, Insta360's bill of materials (BOM) costs will increase by 9% year-on-year, dragging down its gross margin by 4 percentage points.

Additionally, pressure from the downstream consumer market continues to shrink the base of handheld smart imaging devices.

On one hand, leading smartphone manufacturers like Apple and Huawei are constantly upgrading their imaging capabilities, with full focal-length coverage (primary, telephoto, ultra-wide) and mature computational photography technologies making smartphones the preferred tool for daily recording.

On the other hand, rising memory prices have increased costs for core components of handheld smart imaging devices, such as Sony sensors and Ambarella main controllers, causing module prices to rise. Terminal manufacturers must either raise prices to pass on costs or compress profit margins.

Either choice may ultimately drive users further toward smartphones—when the price advantage of consumer-grade action cameras disappears, their presence in daily recording scenarios is significantly weakened. According to media reports, smartphone manufacturers like vivo, OPPO, and Honor have all initiated Vlog camera projects, intensifying cross-border competition in the handheld smart imaging sector.

02

Market Player Rankings Begin to Solidify

Unlike previous upstream price hikes, this round of memory price increases is not a short-term fluctuation but a medium- to long-term trend influenced by factors like rising AI computing demand and capacity restructuring. Its impact on the handheld smart imaging sector will continue to unfold.

It is foreseeable that when the price hike cycle ends, the industry's competitive landscape will undergo significant changes, with market concentration continuing to rise and player rankings likely to solidify. Smaller brands will accelerate their exit, while the Matthew effect among top players becomes more pronounced.

Rising memory prices have significantly raised the industry entry barriers for handheld smart imaging. Smaller brands lack supply chain bargaining power, have small procurement scales, and weak cost control capabilities, leaving their profit margins continuously squeezed during price hikes.

Take Insta360 as an example. Currently, its high-end product pricing approaches DJI's. Under pressure from rising upstream costs like memory, if Insta360 raises prices further, it risks losing price competitiveness. However, if it fails to raise prices, the profitability of related products cannot improve, and the company's gross margin will continue to be compressed.

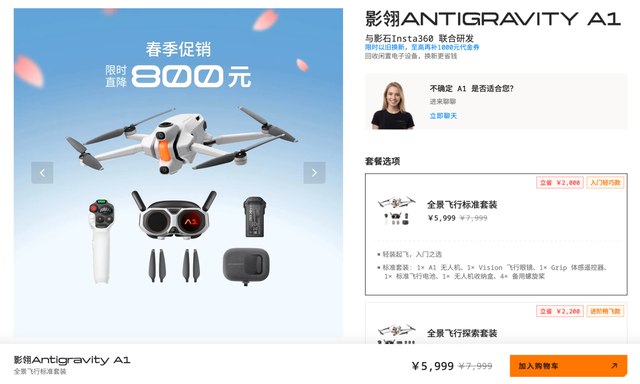

In late 2025, Insta360 launched its flagship product, the panoramic drone Yingling Antigravity A1. However, after just three months on the market, the full-system kit began offering discounts, with the original 7,999 RMB standard kit reduced to 5,999 RMB.

Screenshot from the company's official online store

Operating data further illustrates this point. Currently, Insta360 is trapped in a dilemma of increasing revenue but declining profits. In 2025, its revenue grew by 76.85% year-on-year, but net profit attributable to shareholders fell by 3.08% year-on-year.

In the long run, under sustained R&D investment and cost pressures, if Insta360 cannot quickly address supply chain and ecosystem shortcomings, its position among top players will become increasingly awkward.

The aforementioned JiuQian ZhongTai report noted that memory price hikes are impacting the entire consumer electronics industry. For camera brands, other high-priced product lines, high shipment volumes leading to high inventory, stable new product release schedules, and sales growth rates collectively form a buffer against cost risks. Considering the difficulty of memory price declines in the short term, price wars in the camera sector, and memory upgrades driven by AI capabilities in products, camera brands will face further profit pressure in the future.

In contrast, leading manufacturers can leverage supply chain advantages, brand premiums, and financial strength to expand counter-cyclically during industry adjustments and further seize market share.

Among them, DJI has formed a full-scenario imaging matrix encompassing 360-degree cameras, action cameras, handheld gimbals, and drones through its full-category layout, supply chain advantages, and ecosystem synergy. It holds advantages in both consumer and professional markets. Rising memory prices have not significantly impacted DJI but have instead become an opportunity to squeeze competitors.

Although its market share continues to erode and memory price hikes affect its gross margin, GoPro can still rely on its mature supply chain system, subscription service growth, and user barriers in the core action camera market to diversify its profit structure and maintain relatively stable market performance.

03

Anti-Cycle Capabilities Emerge as Core Valuation Metric

The memory price surge not only reshapes the industry's competitive landscape but also triggers a reassessment of handheld smart imaging companies by the capital markets.

Generally, the core valuation metrics for consumer electronics listed companies have always been the certainty of earnings growth, gross margin stability, and anti-cycle capabilities. This memory price hike comprehensively tests these three capabilities.

During periods of stable component prices, earnings growth primarily relies on market share expansion, product innovation, and capacity expansion. Capital markets are more willing to assign high valuation premiums to high-growth companies. However, when core components like memory enter a price hike cycle, a company's cost control capabilities and anti-cycle abilities become new variables in valuation metrics.

Against this backdrop, only companies that can digest cost pressures through supply chain advantages and product structure adjustments while maintaining stable earnings and gross margins will gain recognition from capital markets. Conversely, companies unable to pass on cost pressures, facing declining earnings growth and gross margins, will see their valuations sharply revised downward.

Top companies at different growth stages have shown starkly different performances in this valuation reassessment.

GoPro, a mature overseas listed company, has entered a stable profitability phase, with its valuation consistently at the consumer electronics industry average. In recent years, GoPro has advanced its "hardware + services" transformation, with subscription services accounting for an increasing share, significantly reducing its sensitivity to hardware cost fluctuations.

Of course, GoPro's biggest challenge remains its lack of product innovation. In recent years, GoPro has faced a multi-year product gap in the 360-degree camera segment, with its market share continuously shrinking.

GoPro Camera | Screenshot from the official website

Data shows that in 2025, GoPro's revenue was $652 million, down sharply by about 19% year-on-year; camera shipments were approximately 2 million units, down about 20% year-on-year.

Meanwhile, Insta360, a newly listed domestic company, faces dual pressure on valuation and earnings.

After its listing, Insta360 received a valuation premium significantly higher than the industry average, with its market cap once exceeding 140 billion RMB, based on expectations of increasing market share, gross margin, and sustained earnings growth.

However, cost pressures from rising memory prices have shattered these earnings expectations: rising costs compress profit margins, while the consumer market faces sustained pressure from competitors like DJI, slowing earnings growth. Although the company can smooth short-term earnings through non-recurring items, this does not address the core issue. Once earnings fall short of expectations, capital market valuation downgrades become inevitable.

This memory price surge has also exposed common issues in the consumer electronics industry: the capital markets' high sensitivity to cost fluctuations and valuation divergence among companies at different growth stages.

For mature companies, capital markets prioritize profit stability and anti-cycle capabilities, with relatively rational valuation pricing. For high-growth companies, capital markets often assign high valuation premiums, but these premiums are based on the certainty of high growth. Once cost fluctuations increase earnings uncertainty, high valuations quickly collapse.

This serves as a warning for the handheld smart imaging sector: high valuations must match high-certainty growth and profitability. Only by continuously enhancing cost control capabilities, supply chain bargaining power, and anti-cycle capabilities can companies gain long-term stable valuation recognition in capital markets.

In the future, competition in the handheld smart imaging sector will no longer be solely about products and technologies but also a comprehensive competition involving supply chains, ecosystems, and anti-cycle capabilities. Only by comprehensively enhancing core competitiveness can companies stand firm amid industry upheavals.

Some images sourced from the internet. Please notify us for removal if infringement occurs.

-

![]()

Hardware is the skeleton, AI is the soul, and data integrates the two

-

![]()

China’s AI Industry: A Unified Pivot Towards Monetization?

-

![]()

New Progress! Infineon Completes Acquisition of ams OSRAM's Non-Optical Sensor Business

-

![]()

35 Million Bet on an Optical Future! Tengjing Technology Makes a Move in AR

-

![]()

Why World Models Get Stuck on Construction Roads in Autonomous Driving Applications

-

Alibaba Initiates Cultural Transformation: Is Jack Ma Making a Strategic Comeback?

-

Tianfeng Heads to Hong Kong for IPO with RMB 3.8 Billion in Funds: Xingyu's Cross-Border Foray into Embodied AI Faces Uncertain Future

-

![]()

Mengshi Auto’s High-End Aspirations Dashed: Huawei Partnership Fails to Revive Sales, New Model’s Entry Price Dips Below 300,000 Yuan