Why Is It So Hard to Be Fourth in China's Smartphone Industry?

03/23 2026

03/23 2026

579

579

Failing to break into the top three in an industry reshuffle means standing on the brink of survival?

“In the long run, it’s unlikely that all seven Chinese players will survive.” This was Lei Jun’s earlier statement regarding the outcome of competition among domestic smartphone manufacturers.

This implies that the intense and cutthroat competition within the smartphone supply chain shows no signs of easing.

However, among all the manufacturers engaged in this fierce struggle, the most disheartened are those ranked fourth. This position means that, on one hand, several leading brands maintain absolute control over the market, making it difficult to surpass them; on the other hand, they are not entirely in the “others” category, still holding a glimmer of hope for recovery.

Hoping to reclaim a top position yet teetering on the edge of falling to the bottom, this is the greatest dilemma for the fourth-place player.

Over the past three years, multiple manufacturers have taken turns being fourth. In the eyes of many in the smartphone industry, “Few industries are as brutally competitive as smartphones. In most other sectors, once the market hierarchy of top, mid, and bottom tiers is established, it rarely changes. However, the smartphone industry is unique, with rankings shifting every quarter.”

For each manufacturer, almost no one can afford to relax. In a highly saturated and mature market, any company could accidentally find itself in fourth place.

Now, the consumer electronics industry is facing the issue of rising prices for memory chips. Is the fourth-place player closer to victory or to defeat?

In any case, a new round of reshuffling in the smartphone industry has arrived.

The Rotating Fourth Place: No One Escapes Survival Anxiety

Competition for market share among domestic smartphone manufacturers is a life-and-death struggle.

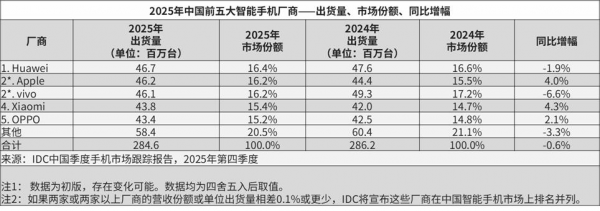

According to IDC statistics, from 2023 to 2025, nearly all major players—VIVO, Huawei, Xiaomi, OPPO, and Honor—have experienced the challenges of being fourth.

In 2023, VIVO held a 16.5% market share, ranking fourth (though some statistics claim VIVO remained domestic first for multiple years). If only domestic manufacturers are considered, Huawei took fourth place. That year, despite Huawei’s sudden rise with the Mate60 series, becoming synonymous with “far ahead” and seeing a 50% increase in shipments, it still failed to crack the top five. With its self-developed chip production capacity not fully restored, Huawei remained at the tail end of the mainstream camp (mainstream camp).

This changed rapidly in 2024, when the market dynamics completely reversed. Honor began to fall behind in the second half of 2024, finishing the year in fourth place, tied with OPPO, while Xiaomi disappeared from the top five. In 2024, Honor faced the toughest challenges among domestic manufacturers, undergoing significant personnel changes, experiencing a sharp market contraction, and seeing shipments plummet to their lowest since independence.

Just a year later, in 2025, the pattern (landscape) reversed again. Last year, Apple achieved counter-trend growth, VIVO ended its previous high period, and Honor returned to the top five in the third quarter. However, for the full year, Honor dropped from fourth in 2024 to “others” on IDC’s list, with Xiaomi taking fourth place and Huawei surging to the top as the domestic leader.

Looking back at the industry’s shake-ups over the past three years, the top positions have rarely been truly stable, and the fourth-place spot could change hands at any moment.

As a seasoned industry insider, Mr. Zhu told Lukou Business Review that some outsiders believe the domestic smartphone industry is forming a “Huawei-Vivo-Xiaomi” pattern (landscape), but this view is hard to support. IDC’s 2025 data shows Huawei, Apple, Vivo, Xiaomi, and OPPO in the top five. Notably, the top five companies have not pulled significantly ahead, with all holding over 15% market share and the shipment gap between first and fourth place being less than 3 million units.

Even going back to 2024 and 2023, the differences in share and shipments between first and fourth place were minimal. Such small margins prove the intensity of market competition.

Nevertheless, during the growth era, when the market pie was expanding, fourth-place players could still grow by catching up and enjoying industry dividends. But in the stagnant growth era, every share must be taken from competitors. Standing on the edge of the top tier, the fourth-place player faces insurmountable barriers ahead and fierce pursuers behind, making every step precarious.

New Changes in the Smartphone Industry: Where Does the Fourth-Place Player Get Stuck?

The difficulties faced by the fourth-place player are largely tied to the industry’s characteristics in recent years, with crises lurking everywhere.

At the macro level, the smartphone industry has ended its high-growth phase, entering an era of “stagnant growth meat grinder” in the red ocean market. Specifically, over the past three years, total domestic smartphone shipments have hovered around 270–280 million units, even declining by 0.6% last year and expected to fall by over 10% this year.

With weak industry demand, previous consumer subsidy policies and hype around AI phones have failed to trigger a large-scale replacement cycle. The average replacement cycle for domestic users has extended to at least 36 months, and the market has entered a zero-sum game of stagnant growth.

In this context, the fourth-place player often struggles to gain market share from the overall pie and finds itself in a precarious position, forced to compete for existing users among the top players.

However, market segmentation at the product level has become increasingly pronounced. In the high-end market above 4,000 yuan, Huawei and Apple have maintained a near-80% combined share, forming an unshakable duopoly thanks to their early establishment of moats in systems, self-developed chips, and brand perception. Moreover, Apple’s shipments surged by 4% in 2025, making it the second-fastest-growing manufacturer in the Chinese market and increasing pressure on competitors.

The remaining share is divided among various players, but none hold more than a 20% share in the high-end market. For example, despite OPPO’s Find X9 Pro debuting Hasselblad 8K ultra-clear photo capabilities, such technologically advanced products have not been enough to propel it into the high-end leadership, and it even faced quality control issues like screen green lines last year.

Similarly, as the fourth-place player in IDC’s 2025 rankings, while Xiaomi’s automotive business has brought significant momentum and growth to its flagship phones, with the Xiaomi 14, 15, and even 17 series performing well, it still lacks the strength to challenge the top duopoly.

In the mid-range market, which accounts for over 50% of total shipments and serves as the foundation for all manufacturers, competition is the fiercest. With a mature domestic smartphone supply chain, mid-range phones continue to feature cost-performance battles and differentiated innovations. Flagship chips, 100W fast charging, and large-sensor imaging—features once exclusive to high-end models—are now standard in mid-range devices, pushing parameters to their limits while reducing differentiation. Combined with frequent price adjustments and promotional incentives, profit margins have been squeezed to the extreme, with some mid-range models seeing net profit margins below 15%.

This creates a vicious cycle. Without brand premium in the high-end market, there is insufficient profit for core R&D investment. Without sustained technological breakthroughs, it is impossible to secure a foothold in the high-end market. Manufacturers must rely on mid-range models for volume to maintain market share, but the intense competition in this segment further compresses profit margins, ultimately trapping them in an awkward position of failing to excel in either high-end or low-end markets, with both profitability and growth hitting bottlenecks.

Thus, whether it’s OPPO, Honor, or others who have been fourth, all face the dilemma of “failing to disrupt the high-end market while struggling with parameter and profit competition in the mid-range.”

The outcome is similar to the PC industry, where after multiple reshuffles, Lenovo, HP, and Dell firmly occupy the top spots, while manufacturers below fourth place are either acquired or exit the market entirely. Once they fall behind, there is no chance of recovery. Former players like Founder, Tsinghua Tongfang, and TCL computers are now relics of the past. Occasional entrants like Huawei and Xiaomi laptops only occupy niche markets driven by their smartphone brands.

Today, the smartphone industry is similar, with each manufacturer developing distinct characteristics and varying levels of risk tolerance.

Huawei has its pure HarmonyOS system, Kirin chips, and automotive business as second growth engines; Xiaomi has its self-developed Surge chips and a growing automotive business, enabling sufficient ecological synergy and long-term investment capabilities. Vivo relies on user experience, imaging capabilities, and the unique positioning of its IQOO gaming phones to maintain a relatively stable consumer base.

Apple, with the iPhone 17’s rapid technological advancements in display and camera systems, is expected to maintain even more saturated investments in the Chinese market. Meanwhile, OPPO and Honor lack industrial scale beyond hardware and must rely on profits from smartphones, wearables, and tablets to sustain R&D. If their market share declines and profits shrink, their long-term investment capabilities will inevitably suffer, increasing the risk of falling behind.

In other words, the market never leaves much room for error for challengers. The difficulty for the fourth-place player is not just about failing to capture more market share but about not yet finding a moat to stand on. Once trapped in the dilemma of declining share and profits, it becomes hard to escape this vicious cycle.

Although IDC currently ranks Xiaomi as fourth, the story is far from over. It is foreseeable that the fourth-place position will likely change hands again in the coming years, as it has in previous years.

The Fourth-Place Player’s Survival Space Continues to Shrink on the Eve of Technological and Industry Reshuffles

Li Ming has his own judgment on the future evolution of the smartphone industry. He believes that, looking ahead, the smartphone industry is undergoing unprecedented technological restructuring, inevitably leading to increased brand concentration. Manufacturers will not only compete in traditional smartphone businesses but also in new areas.

If a company falls to fourth place, the intense competition between old and new businesses will further narrow its survival space.

“AI phones have shifted from mere parameter hype to genuine user experience upgrades, with large models and smartphones deeply integrating to redefine the value of smartphones.”

Li Ming also emphasizes that AI has intensified industry competition. The collaboration between Doubao and ZTE has propelled the smartphone industry into a new phase defined by joint efforts between large model companies and hardware manufacturers. Honor’s launch of robotic phones is pushing embodied AI technology to integrate with smartphones. Phones are becoming personal intelligent assistants for users and even control terminals for embodied AI.

Currently, no AI phone has yet become an absolute blockbuster with massive sales. Once a manufacturer takes the lead, it could be a ticking time bomb for other players, including the fourth-place player.

At the new business level, expanding industrial boundaries is indeed a prominent feature of the current smartphone industry, with both established and new players making covert moves in this arena.

For example, Huawei’s automotive business has entered a profitable phase; Xiaomi’s car deliveries have surpassed 40,000 units per month, and its ecosystem of robots and smart home devices is becoming increasingly mature. OPPO has reportedly initiated a project for handheld smart imaging devices, directly competing with GoPro and DJI, while Vivo is exploring layout (layouts) in MR (mixed reality) and humanoid robots.

However, the commercialization progress of new businesses and their impact on smartphone manufacturers remain to be seen over time. Even so, new uncertainties continue to emerge in the market.

On one hand, internet giants are cross-border entering the smartphone arena, and tail-end manufacturers like ZTE may attempt to reclaim mainstream market share in the future. On the other hand, since 2025, prices for memory and storage chips have continued to rise, potentially pushing the market into an adjustment period characterized by “high costs, product roadmap revisions, and slowing sales growth.”

With rising hardware costs for manufacturers, many have raised prices to maintain market share, but following industry norms, they may eventually resort to price cuts and promotions, further squeezing profit margins. If they adopt a machine-sea tactics, releasing large numbers of mid-range models, they can temporarily boost market share but risk lowering their brand positioning and losing high-end opportunities. Conversely, if they streamline their product lines and focus on the high end, they face the risk of declining market share.

Therefore, once a manufacturer becomes the next fourth-place player on the eve of technological and industry transformations, it will be torn between short-term gains and long-term development, with its survival space only shrinking further.

Looking back, Lei Jun’s words hold some credibility.

After all, over the past decade, China’s smartphone industry has eliminated brands like Meizu, Lenovo, Gionee, Coolpad, and Smartisan one by one. Similarly, over the past three years, the fourth-place position on IDC’s list has changed hands repeatedly. This ranking will continue to shift in the future. But no matter who sits in fourth place, the challenges will only grow.

In this stagnant growth market, there are no permanent leaders, nor are there permanent challengers.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once