Can Tencent Music Win This Defensive Battle by Integrating Himalaya?

05/13 2026

05/13 2026

407

407

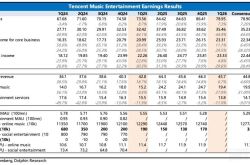

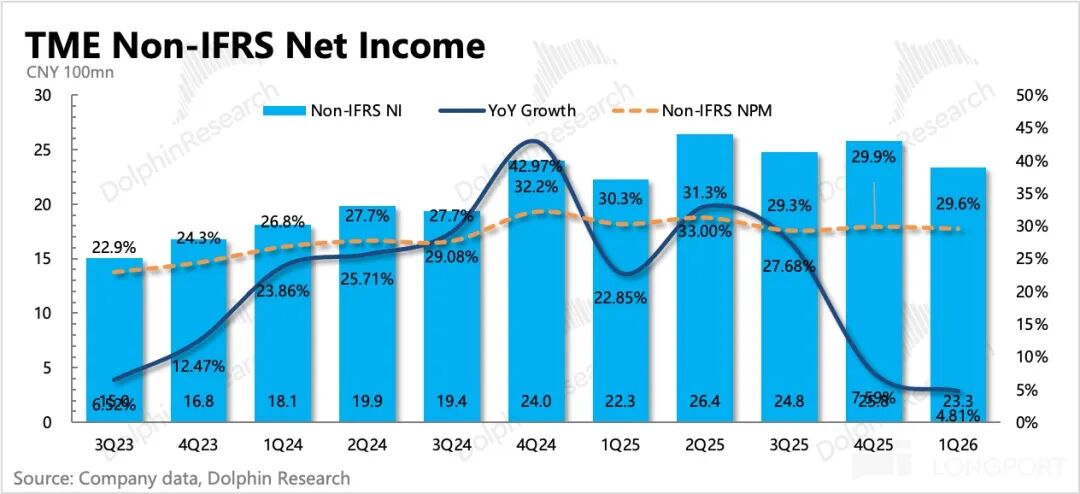

Tencent Music (TME.US) delivered Q1 results largely in line with expectations, aligning with the guidance provided in the previous quarter, though expenses were slightly lower than market forecasts. Overall, the company demonstrated a state where core subscription growth is showing signs of fatigue amid competition, necessitating continuous exploration of non-subscription music-derived monetization opportunities.

However, more noteworthy than the performance itself is the pre-market news of Himalaya's acquisition receiving regulatory approval. This not only enables Tencent Music to accelerate business integration and incorporate audiobook users but also opens the door for "self-rescue" through share buybacks.

A closer look reveals:

1. Ecosystem Defense Remains Critical: The company has ceased disclosing user data since the beginning of the year. By analyzing trends from Questmobile and back-calculating subscription revenue, Dolphin Research approximates Q1's situation (for reference only):

Monthly Active Users (MAU) continued to decline quarter-over-quarter, with a stable overall decline rate. However, sustaining a 500 million-user ecosystem requires greater efforts. Himalaya's integration may present an opportunity, as historical data shows limited overlap between Himalaya's core users and Tencent Music's user base.

Nevertheless, AI and free music platforms continue to erode the appeal of copyrighted music, but the competition remains platform-versus-platform at its core. Thus, even if self-revolution accelerates internal cannibalization, proactive adoption of AI is necessary to slow user attrition.

2. Subscription Growth Fatigue: Q1 revenue grew by 6.6%, slightly exceeding expectations but masking underlying weakness. Aligning with the company's strategy of lowering paywalls to enhance user stickiness, Dolphin Research estimates a net addition of 1 million subscription users in Q1, with ARPPU declining to RMB 11.7 month-over-month (for reference only).

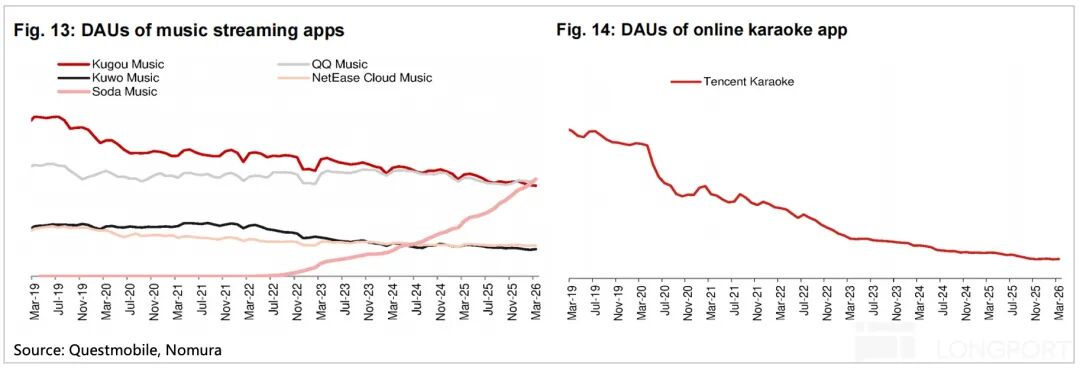

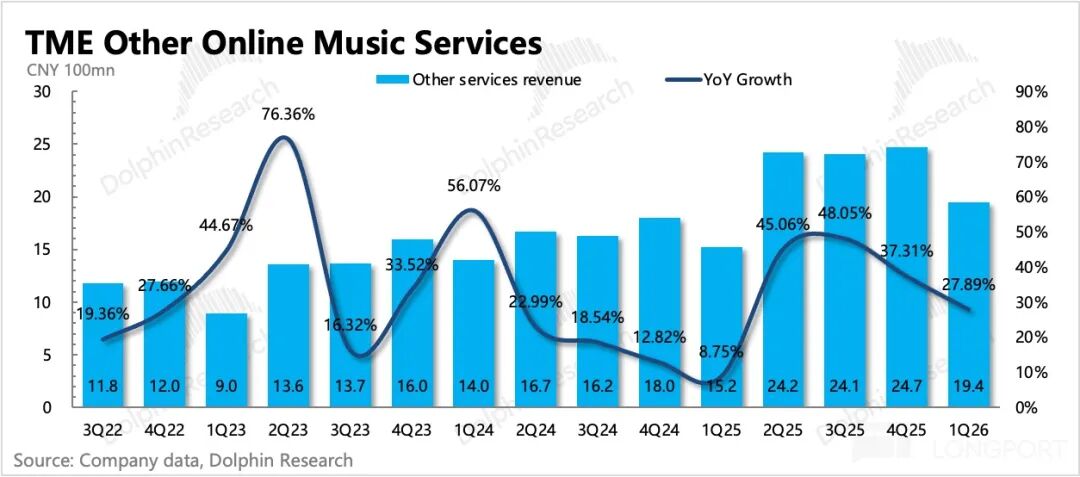

3. Robust Music Derivatives: Other music-related revenue (advertising + offline concerts + digital albums, etc.) surged by 28%, though growth slowed quarter-over-quarter, possibly due to the late Chinese New Year amplifying the off-peak concert season. Despite falling short of expectations, this growth remains strong. Jay Chou's new album released in late March received a weaker response compared to his previous release four years ago. However, some revenue should still be recognized next quarter.

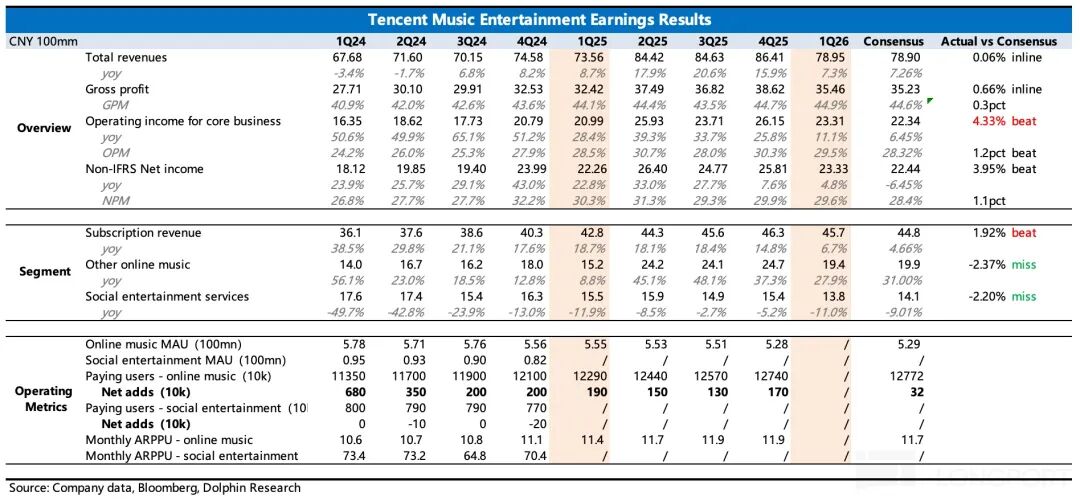

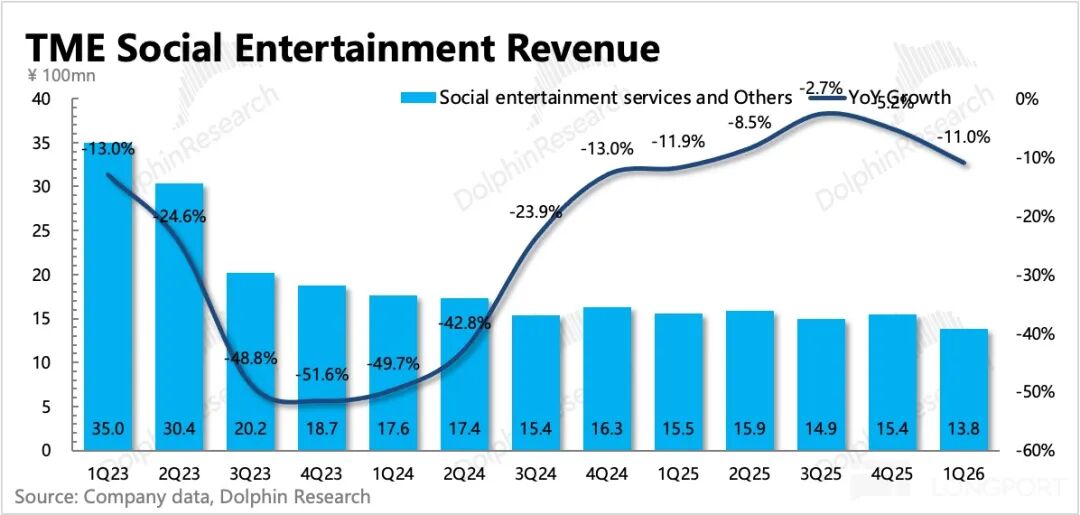

4. Social Entertainment Deteriorates Again: Social entertainment revenue, previously thought to have stabilized, dropped 11% quarter-over-quarter in Q1. Listening to the earnings call will provide clarity, but Dolphin Research speculates that, beyond persistent live-streaming headwinds, QM data suggests significant competition impact on the K-song business from traditional peers and AI. AI's primary C-end application—cover songs—overlaps with the K-song experience, leading to a sustained decline in active users for all the people K song (WeSing).

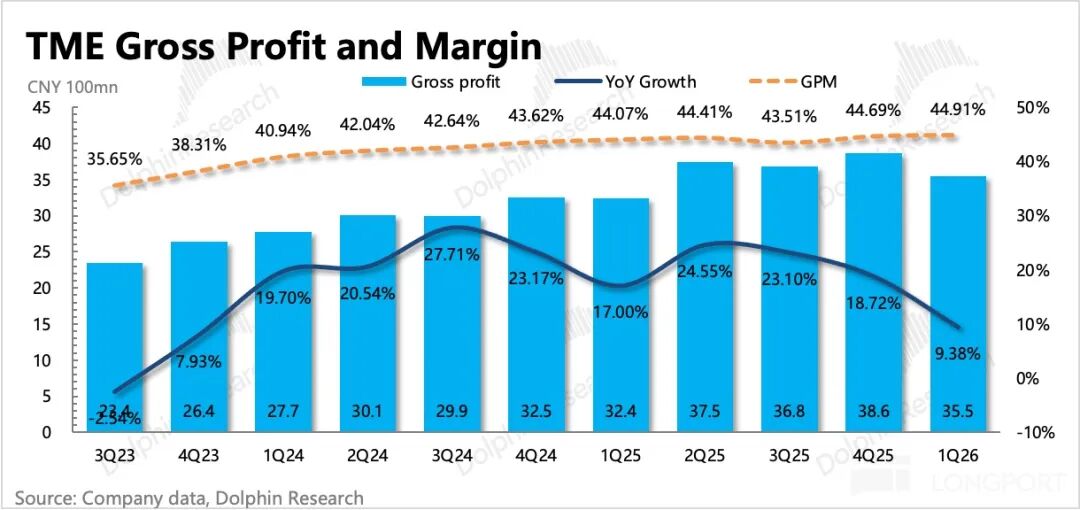

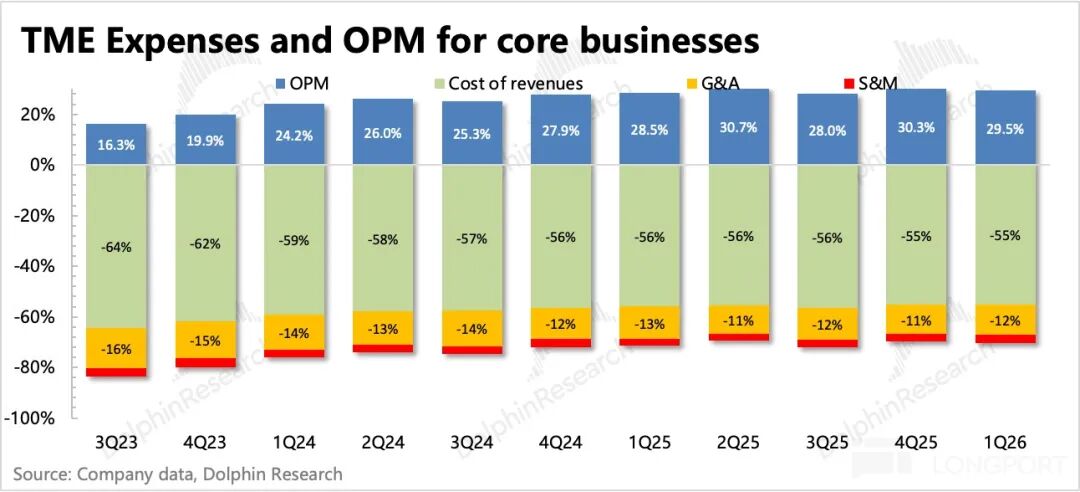

5. Investment Expansion with Continued Internal Efficiency: Q1 gross margin improved by 30bps quarter-over-quarter to 44.9%, driven by a higher revenue share from non-subscription businesses (advertising, etc., which boast high margins) and optimized licensing costs. Operating expenses saw sales expenses maintain high growth, reflecting ongoing business development and customer acquisition efforts. Meanwhile, general and administrative expenses remained flat year-over-year and declined quarter-over-quarter, likely indicating workforce optimization.

6. Promising Shareholder Returns: As of Q1's end, Tencent Music held RMB 25 billion in short-term net cash (cash + short-term investments - short-term interest-bearing debt), equivalent to USD 3.6 billion. With substantial cash reserves and a healthy cash flow business model, the company has barely utilized its USD 1 billion share buyback budget announced in March last year for a two-year period.

If buybacks proceed normally and are fully utilized by March 2027, combined with RMB 370 million in dividends, the implied total shareholder return at the current market cap of RMB 14 billion approaches 10%, demonstrating significant commitment.

7. Detailed Financial Data Overview

Dolphin Research's Perspective

Q4's performance and guidance last year shattered Tencent Music's previously advantageous investment logic: shifting from "streaming price hikes" to "user acquisition through price cuts," reflecting weakened competitive barriers. Coupled with uncertainty over acquisition approval timelines, which impacted buyback-supported valuations, the P/E ratio plummeted from the historical 20x to the current 10x. Based on company guidance, this year's revenue is projected at RMB 36 billion, with adjusted profit reaching RMB 10.4 billion, up 8% year-over-year. At yesterday's closing market cap of RMB 14.4 billion, this translates to a 9.6x P/E.

While valuations are now below historical and internet peer averages, until competition stabilizes, market confidence in future growth remains subdued. This determines expectations for Tencent Music's ability to sustain long-term CAGR above 10%, potentially driving the P/E ratio from 10x to 15x or higher.

Current user data suggests the inflection point has not yet arrived. Q1 saw DAUs for Soda Music (Qishui Music) surpass 50 million, overtaking both Kugou and QQ Music, with no significant slowdown in growth. Meanwhile, Kugou continues to lose users, WeSing weakens further, and QQ Music barely holds steady.

Thus, based solely on financials, capital is unlikely to provide a positive response. However, the pre-market news of Himalaya's approval serves as a true "confidence" catalyst. It may modestly boost expectations for user ecosystem maintenance and competitive restoration while addressing the critical buyback issue.

Tencent Music is not cash-strapped; beyond its substantial cash holdings, its business model is a cash cow. Previously, management could not use buybacks to support the stock during price pressures due to the acquisition involving TME share swaps. With approval secured, the two-year, USD 1 billion buyback program initiated last year can resume.

A more detailed value analysis has been published in the Longbridge App's 「Dynamic-Depth」 section under the same article title.

In-Depth Analysis Below

I. Subscription Growth Fatigue as Expected

Q1 subscription revenue growth fell below 7%, with the company ceasing to disclose "volume-price" details. Dolphin Research estimates a net addition of approximately 1 million subscription users and an ARPPU of RMB 11.7/month, reflecting the company's early-year promotional activities and strategic shift to lower membership thresholds for user scale expansion.

Post-Himalaya integration, a short-term opportunity may arise. Questmobile data shows only 15% overlap in core users between the two platforms. However, as music is a universal demand, bundling packages (e.g., existing memberships plus a RMB 1-2 premium) could easily drive paid conversions.

Attempting to leverage "market leadership" for higher premiums is unfeasible amid the current consumption environment and explicit regulatory bans against raising service prices, reducing service quality, lowering free content ratios, securing exclusive licenses with copyright holders, or bundling music platforms with automakers.

While the acquisition's value is diminished, it remains better than nothing for Tencent Music. Beyond long-form audio user integration, internal growth may primarily rely on penetrating the Super VIP (SVIP) tier by continuously adding fan-centric benefits.

II. Other Music Services: Growth Remains Robust

Q1 revenue from other music services grew 28% year-over-year, slightly below expectations with a sequential slowdown, likely influenced by the off-peak concert season. Nonetheless, multiple large-scale K-Pop group concerts and NCT-WISH's Hong Kong concert were held during the period.

Other revenue streams include advertising, digital album sales, copyright sublicensing, and value-added services. These represent IP-derived peripheral businesses monetizing fan value. While their audience scale is far smaller than music's core demand, per-user value is exceptionally high, with Chinese core users' spending power rivaling that of Europe and America (Western) markets.

III. Social Entertainment: Bottom Unstable, Deteriorates Again

Q1 social entertainment revenue dropped 11% quarter-over-quarter, worsening further. Beyond persistent live-streaming headwinds, QM data suggests significant competition impact on the K-song business from traditional peers and AI.

IV. Profitability: External Investments and Internal Efficiency in Tandem

Q1 gross margin improved by 30bps quarter-over-quarter to 44.9%, driven by a higher revenue share from non-subscription businesses (advertising, etc., which boast high margins) and optimized licensing costs.

Despite modest sales expenses, they maintained high growth at 36%, reflecting ongoing business development and customer acquisition efforts. Meanwhile, general and administrative expenses remained flat year-over-year and declined quarter-over-quarter, likely indicating workforce optimization.

Ultimately, core business operating profit reached RMB 2.3 billion, up 11% year-over-year, outpacing total revenue growth of 7%, with the profit margin improving by 1pct year-over-year to 29.5%.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for users of Dolphin Research and its affiliates for general reading and data reference. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or unique needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any person using or referring to the content or information in this report for investment decisions assumes all associated risks. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of data in this report. The information and data herein are based on publicly available sources and are for reference only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of such information and data.

The information or viewpoints mentioned in this report shall not be construed as or deemed as an offer to sell securities or an invitation to buy or sell securities in any jurisdiction. They also do not constitute recommendations, inquiries, or endorsements of relevant securities or financial instruments. The information, tools, and data herein are not intended for or designed for distribution to jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations, or where Dolphin Research and/or its affiliates or related companies must comply with registration or licensing requirements in such jurisdictions for citizens or residents thereof.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright solely owned by Dolphin Research. No institution or individual may, without prior written consent from Dolphin Research, (i) produce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer to other unauthorized persons. Dolphin Research reserves all related rights.

-

![]()

Auto China 2026: Chinese Brands Lead the Green and Smart Future | Cover Story: In China, for the World – Auto China 2026 Special Report (Part 3)

-

![]()

Can Tencent Music Win This Defensive Battle by Integrating Himalaya?

-

![]()

Volvo Asia Pacific: No More 'Successor' Era!

-

![]()

China's Auto Market in April: A 2.5% Sales Decline, a 74% Export Surge, and Profit Margins Below 3.5%

-

![]()

Toyota's Era of Sky-High Profits Draws to a Close

-

![]()

Can Trump Pave the Way for Chinese Automobiles in the US Market with Musk’s China Visit?

-

![]()

Can the New Unisplendour Group Break Away from Being a 'Huawei Alternative' After Resolving Its Hundred-Billion-Yuan Debt?

-

![]()

What technology enabled XPENG to eliminate LiDAR from its intelligent driving systems?