618 Battle Report | China's Online Learning Tablet Market Sees Significant Decline in Volume and Value; Zuoyebang, Xueersi, iFLYTEK, and Xiaoyuan Account for Nearly 90% of Sales

06/29 2026

06/29 2026

373

373

According to data from Runto, during the 2026 618 promotion cycle (May 18 to June 21), sales of learning tablets across all online channels in China reached 360,000 units, a year-on-year decrease of 18.2%. Sales revenue amounted to 1.31 billion yuan, down 11.4% year-on-year, while the average market price was 3,635 yuan, up 8.3% year-on-year.

This data stands in stark contrast to the robust growth trends of previous years, reflecting the industry's profound structural adjustments amid the waning of policy dividends and a return to rational demand.

Despite the overall market contraction, the decline in sales revenue was less pronounced than that in sales volume, with the rise in average prices somewhat offsetting the market downturn. This also indicates a trend toward premium products: students and parents are shifting their decision-making from "paying for functions" to "paying for effectiveness," accelerating the elimination of inefficient and homogeneous products.

Brand Competition: TOP 4 Brands Each Excel, Capturing Nearly 90% of Sales

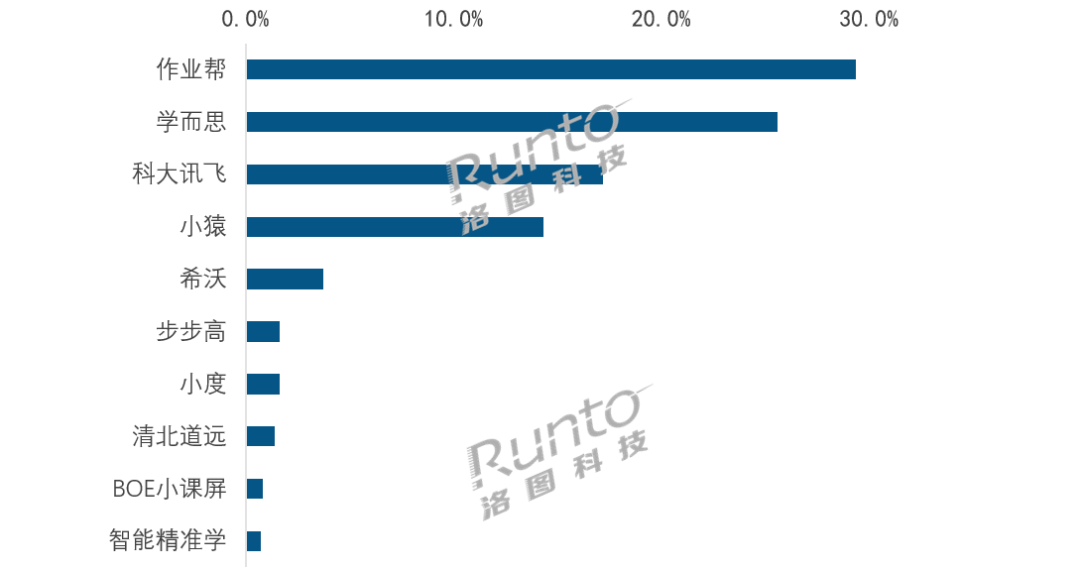

During the 2026 618 period, the online learning tablet market in China continued to be dominated by four major brands—Zuoyebang, Xueersi, iFLYTEK, and Xiaoyuan—which collectively held an 86.5% share of sales volume, roughly on par with the same period the previous year. Leveraging their financial resources, technological advancements, and content barriers, these leading brands maintained their market share even after the subsidy incentives faded. During promotions, the shortcomings of smaller brands became more apparent compared to the larger ones.

Zuoyebang maintained its position as the top seller in the online market, with a sales volume share of 29.3%. During the promotion, the brand differentiated itself with AI-powered full-process tutoring, offering basic AI grading and error organization functions across all price ranges. Its volume-driven model, the P60, targeted the entry-level mass market, catering to the basic after-school tutoring needs of ordinary families.

Xueersi held a 25.6% share of online sales volume. Relying on its exclusive teaching and research content, such as the self-developed tiered curriculum system, the brand established a competitive edge in the mid- to high-end market, with its T4 series consistently ranking among the top-selling mid- to high-end products.

iFLYTEK secured a 17.2% share of online sales volume. Leveraging AI technology as its selling point, the brand maintained high average selling prices, continuing to lead the 4,000+ yuan market and validating the long-term competitiveness of "AI + education" in the premium segment.

Xiaoyuan accounted for a 14.3% share of sales volume. Its competitive edge lies in constructing a closed-loop system of diagnosis, learning, practice, and testing through its proprietary proficiency model, creating a differentiated advantage with quantifiable learning assessments. Notably, its T6 series gained market recognition with data-driven learning feedback, demonstrating commendable sales performance.

Sales Volume Share of TOP Brands in China's Online All-Channel Learning Tablet Market During the 2026 618 Promotion Period

Data Source: Runto Online Data, Unit: %

Summary: Continuous Exploration Under Short-Term High Base Pressure; Long-Term Growth Prospects Remain Favorable

Since 2026, the impact of government subsidies has significantly diminished, leaving the market without external support. Additionally, with AI empowerment, general-purpose smart tablets have gradually incorporated rich learning resources, diverting the target customer base. Consequently, the market size has shifted from a slowdown in 2025 to a standstill.

According to Runto data, in the first quarter of 2026, sales of learning tablets across all online and offline channels in China reached 1.252 million units, a year-on-year decline of 1.0%. Looking ahead to the third quarter, the Chinese learning tablet market is expected to continue its downward trajectory, with a more severe decline than in the previous two quarters.

Runto analysis suggests that over the past five years, China's electronic education hardware market has experienced rapid development. Today, Chinese parents and students can relatively rationally and diversely choose tools and solutions that provide access to high-quality educational resources. Therefore, it will be challenging to find incremental growth to fill the gap left by the fading policy incentives in the short term.

However, unlike other conventional consumer electronics that bind users over the long term, learning tablets, as a core category of electronic education hardware, have low user tolerance for compromise. Coupled with the cyclical replacement of school-age populations, user demand will gradually recover, laying a solid foundation for medium- to long-term market growth.

The Runto

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?