The 'Wholesale to Retail' Arbitrage Dynamic in Block Trades: A Case Study of Insta360

07/06 2026

07/06 2026

341

341

When you encounter a block trade announcement stating, "XX shares traded 2.89 million shares via block trade, with 'Institutional Dedicated' identified as the buyer," does your immediate thought leap to, "Big institutions are seizing the opportunity to buy low?"

Wait a moment—let me clarify: That 'Institutional Dedicated' buyer is likely not long-term institutional capital, such as mutual funds or insurance companies. Instead, it's more probable to be short-term arbitrageurs—private equity firms, quant funds, or bridge capital providers. Even more surprising? Some of these shares could be sold to retail investors in the secondary market as early as the next day.

'Six-month lock-up for buyers'? Not quite accurate

Among retail investors, a common belief is: "Block trade buyers are subject to a six-month lock-up." While not entirely false, this statement is only partially correct. It's akin to saying, "You must wear a seatbelt while driving"—true, but you won't be fined for not wearing one on a motorcycle because the rule doesn't apply in that context.

Article 14 of the Interim Measures for the Administration of Share Reduction by Shareholders of Listed Companies (2025 Revision) indeed stipulates that transferees face a six-month lock-up. However, this rule only applies to two specific types of sellers: those holding over 5% of the shares or those selling 'pre-IPO shares' (those low-cost shares acquired before the company's listing).

Let's use an analogy to clarify: Pre-IPO shares are akin to 'ancestral homes'—acquired at minimal cost per share in large quantities. Regulators are concerned that shareholders might dump these shares immediately after listing, causing the stock price to plummet. Hence, anyone acquiring these shares must undergo a six-month 'cooling-off' period. In contrast, strategic placement shares from IPOs resemble 'new home purchases'—priced identically to the IPO offering price, with a lock-up period merely to stabilize the stock during its early trading days. Once this period ends, regulators do not require buyers to hold onto these shares, as they are not the primary focus of 'low-cost dumping' surveillance.

Here's the crux: If the seller holds less than 5% and is not selling pre-IPO shares, the buyer can sell the shares the next day—with no lock-up period, mirroring the T+1 trading pattern in the secondary market. Does this seem problematic? Think again: This implies that block trade shares are not necessarily locked up for six months but could instantly become a source of selling pressure.

A less obvious rule buried in regulatory documents: Even if the seller is a major shareholder, Article 14 does not apply if the shares being sold were purchased in the secondary market (rather than being pre-IPO shares). In this case, the buyer still avoids the six-month lock-up. Additionally, major shareholders (>5%) must announce block trade reductions 15 days in advance, but strategic placement shareholders (<5%) face no such announcement requirement—their sold shares can enter the market the next day, potentially catching retail investors off guard.

Summarizing the lock-up rules for block trade transferees under regulatory documents:

Discounts are not 'bargains'—they're 'toll fees'

Why offer discounts if shares can be sold the next day? Many assume buyers are 'snagging deals,' but the discount actually represents the seller's 'toll fee' for facilitating a quick sale.

Imagine you're a vegetable vendor with ten tons of potatoes. Selling them individually at the market would take days and might depress prices due to the sheer volume. Instead, you offer a discount to wholesalers who take the entire lot at once—saving you time, effort, and market impact.

Consider Insta360's block trades since June: For shareholders with extremely low-cost bases, a 1% discount is negligible. Strategic placement shares from its IPO cost 47.27 yuan each. Even sold at a 1% discount from 148 yuan, each share still yields a profit of approximately 100 yuan—the 1% discount is merely a 'shipping fee.'

Who are these wholesalers? Probably not the 'bullish on the company's future' long-term institutions you might imagine. They typically fall into three categories: arbitrageurs (private equity firms, quant funds, bridge capital providers earning on discount spreads), conduits ('alternative hands' assisting sellers in offloading shares), and investors (mutual funds/insurance companies genuinely holding for the long term—though these are rare).

A common misconception must be addressed: The 'Institutional Dedicated' label in block trade disclosures is a standardized term for institutional trading units. All regulated institutions can participate in block trades via rented brokerage trading units, including private equity products specializing in arbitrage strategies. These trades are also disclosed as 'Institutional Dedicated.' Thus, 'Institutional Dedicated' does not equate to 'institutional bullishness'—don't misinterpret this equation.

The arbitrage calculation for block trades is straightforward: Profit = Discount Rate - Stock Price Decline During Holding Period. With no lock-up (for strategic placement shares), buying at a discount post-market close on Day T and selling in batches in the secondary market on T+1 generates profit as long as the stock doesn't drop more than the discount rate. This 'fast in, fast out' strategy typically employs low discount rates (1%-10%) as a 'safety cushion' against overnight volatility.

The process unfolds as follows: Unlocked shareholders (wholesalers) sell at a discount to arbitrageurs (middlemen), who then 'retail' the shares in the secondary market—with retail investors typically at the end of this chain.

Empirical Analysis of Insta360's Two Block Trade Waves

After explaining the rules and logic, let's examine real-world cases. Two distinct waves of block trades emerged after Insta360's share lock-up expired on June 11, validating the T+1 arbitrage process.

Wave 1 (June 12-16): The seller's seat consistently belonged to China International Capital Corporation's Beijing Jianguomenwai Avenue securities branch, with six transactions totaling 2.8984 million shares sold. This volume nearly matches the combined allocation of Insta360's Employee Strategic Placement Asset Management Plans 1 and 2 managed by CICC during its IPO. Market speculation suggests this wave represented a concentrated liquidation of the employee stock plan, though no official confirmation exists. If these were IPO employee shares, they qualify as strategic placement with <5% ownership, resulting in zero lock-up for buyers and a 1% discount—hallmarks of T+1 arbitrage.

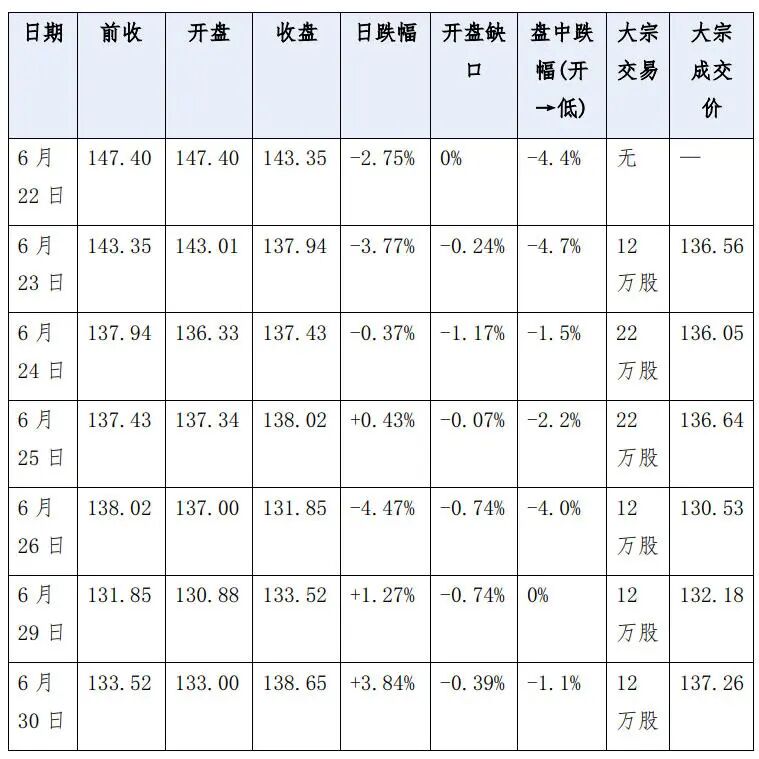

Wave 2 (June 23-30): Fixed daily volumes of 120,000 or 100,000 shares—like 'cruise control'—totaling 920,000 shares sold regularly with a 1% discount. Seller branches included Guotai Haitong Securities' Bao'an Yifang Center branch and Ping An Securities' Shenzhen Shennan Avenue branch (Insta360's HQ is also in Shenzhen). The 1% discount is grossly mismatched with the risk/reward of a six-month lock-up, aligning instead with a no-lock-up T+1 model. Again, no official confirmation exists on the seller's identity or share nature—this remains inference from trading patterns, not a definitive conclusion.

A common market misconception: Many believe no-lock-up T+1 arbitrage causes 'next-day stock price gaps down.' However, Insta360's price action from June 22-30 contradicts this. For example, on June 23, the stock closed at 143.35 yuan and opened at 143.01 yuan—a mere -0.24% gap—but weakened intra-day to a 4.7% drop, closing -3.77%. On June 26, it gapped down -0.74% but closed -4.47%. Instead of 'opening plunges,' the decline was gradual—like water leaking slowly from a basin, unnoticeable until 'soaked.'

Why a 'slow leak' instead of a 'dump'? Block trade arbitrageurs calculate precisely: (1) Dumping tens of thousands of shares at open depresses their own average selling price—better to dribble out small orders intra-day for higher averages. (2) Blending sales with normal trades avoids detection. (3) Selling on intra-day rebounds yields better prices. (4) Selling alongside market weakness appears natural, masking arbitrage-driven liquidation.

Overall, Insta360's stock fell from a June 22 intra-day high of 149 yuan to a June 29 low of 130.88 yuan—a 12.16% drop. This reflected both unappealing fundamentals (revenue growth without profit) and lock-up expiration pressure, with block trade arbitrage acting as just 'one pipe' releasing selling pressure.

An Interlude: During the block trade surge, Insta360 was embroiled in a patent infringement lawsuit with DJI. On June 10, DJI sued Insta360 in the U.S. (six patents + permanent injunction). On June 12, Insta360 countersued with five patents. Both sides filed to dismiss U.S. cases on June 28, with dismissal ruled on June 29. However, domestic litigation continues—DJI's new infringement case in Shenzhen opens on August 3. The first block trade wave coincided with the U.S. lawsuit, the second during undisclosed dismissal negotiations, possibly facing 'litigation pressure + lock-up selling' from both sides.

Three Questions Retail Investors Should Ask About Block Trades

Next time you see a block trade announcement, pause and ask three core questions.

Question 1: Is the buyer 'arbitraging for spreads' or 'genuinely bullish'? Arbitrageurs typically switch buyer branches frequently, use fixed discounts, trade rhythmically, and show net capital outflows later. Genuinely bullish buyers concentrate seats, use low/no discounts, and show no short-term selling patterns.

Question 2: Does the buyer face a lock-up? This determines if block trade shares 'hit tomorrow' or 'wait six months.' Pre-IPO shares or >5% shareholder reductions mandate six-month lock-ups; strategic placement with <5% ownership has zero lock-up—sellable next day.

Question 3: What does the discount rate mean? Discounts aren't 'buyer bargains' but seller 'toll fees.' A stable 1% discount nearly always indicates short-term T+1 arbitrage, needing just enough 'safety cushion' for overnight risk. Discounts of 10%-20% usually imply six-month lock-ups, requiring buyers to endure half a year of volatility for that premium. Insta360's two waves used 1% discounts—a classic 'thin margin, fast turnover' model.

Of course, block trades aren't black-and-white shareholder reductions. The nuanced distinctions in share nature and shareholder identity create a 'wholesale-to-retail' arbitrage path. While compliant, retail investors unaware of these rules risk ending up at the chain's end.

Next time you see 'Institutional Dedicated,' don't get excited—revert to rule fundamentals, factor in share nature, discount rates, and subsequent price action before judging. Insta360 is just one sample, but its underlying logic broadly applies to block trades.

References

1. Interim Measures for the Administration of Share Reduction by Shareholders of Listed Companies (2025 Revision) (CSRC)

2. Insta360's IPO Strategic Placement Results Announcement (SSE)

3. Insta360 Block Trade Data (Eastmoney.com)

4. Insta360 Daily K-line Data (Investing.com)

5. Reports on the 'Subsidy Fraud' Incident (Nanfang Metropolis Daily Bay Area Wealth/New Express/First Finance)

6. Block Trade Arbitrage Models: Popular Science and Empirical Analysis (Xueqiu/Zhihu/Eastmoney)

7. Reports on DJI and Insta360's U.S. Patent Lawsuit Dismissal (PRIP/Tencent News/Jiemian News)

Risk Warning: This content is compiled from public information and does not constitute investment advice. Stock markets involve risks; decisions require caution.

-

![]()

When AI Begins to Reshape Infrastructure: A Reshuffle in the U.S. Cloud Market

-

![]()

Tencent’s Strategic Maneuver: Selling Kuaishou, Investing in Kling

-

Has the Semi-Annual Achievement Rate Dipped Below 40%? Can AIVA Circumvent the 'Multi-Shareholder Death Spiral'?

-

![]()

Stepping Out of the Humanoid Robot Concept: Why is Autonomous Driving the First Large-Scale Implementation Track for Physical AI?

-

![]()

WPS: Criticism Warranted, Yet Open to Improvement

-

![]()

Farewell to Image-First: Robotic Vision is Undergoing a Fundamental Reconstruction

-

![]()

Former Huawei 'Genius Teen' Encounters a 'Hiccup' in DeepSeek's Recruitment Process

-

![]()

WPS Remains Unchanged; It’s the Users’ Perception of “Free” That Has Shifted