From cloud computing to AI large models, cloud giants take a key step in the ecological revolution

08/26 2024

08/26 2024

515

515

2024 is destined to be a crucial year for the development of cloud computing. Over the past two years, the most discussed topic in the cloud computing industry has been "price cuts." With slowing market growth and even some companies advocating for "de-clouding," cloud vendors have resorted to "price wars," leading the entire industry into a "low-level internal competition." Today, fueled by large models, the intelligent transformation of various industries is intensifying. Cloud computing power, as a flexible, efficient, and cost-effective way to acquire computing resources, is becoming the new foundation for AI vendors. If chips are the "oil" of the intelligent era, cloud computing power is the "new energy" for AI development. This shift from old to new business models affects cloud computing beyond just public opinion; the "golden age" of cloud computing may only just be beginning.

The next-generation cloud is becoming intelligent

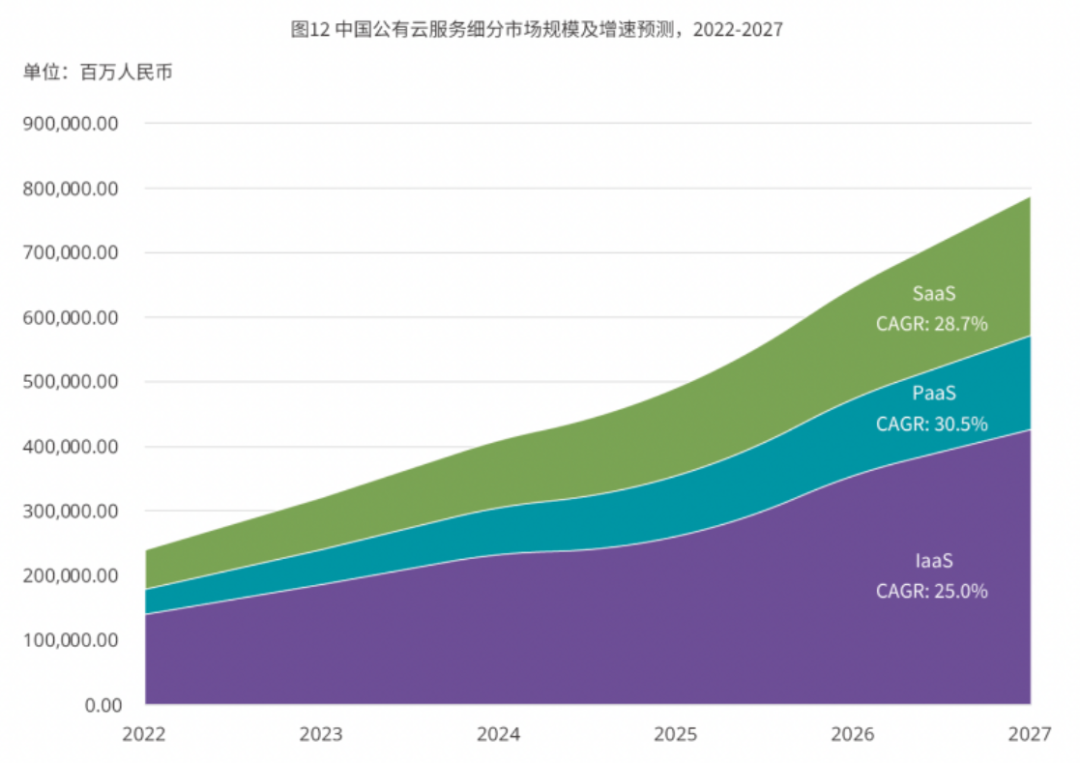

IDC's report, "Focusing on Platform Capabilities to Support Intelligent Business Development," states that China's public cloud market will grow at a CAGR of 26.9% from 2022 to 2027, with PaaS growing the fastest at 30.5% and SaaS following closely at 28.7%. As cloud computing infrastructure matures, China's public cloud market is evolving from a resource-driven to a technology and business-driven model.

IDC's report also highlights how the rapid development of generative AI and large models is accelerating PaaS's emergence as the core capability of the next-generation intelligent cloud. As the middle layer, PaaS must both handle the pressures of IaaS's rapid scale-up and support SaaS's platform-enabled capabilities. PaaS will become a crucial link in helping enterprises build and apply AI natively across all aspects. Business users' evolving cloud needs center around three areas: acquiring AI capabilities on the cloud, accessing AI-powered tools, and realizing intelligence-driven application innovation on the cloud. IDC believes the next-generation cloud will be an "intelligent cloud" tailored to enterprises' intelligent development needs. The cloud serves as the soil for AI's implementation and growth, which in turn propels cloud platform development. Technically, enterprises need smart architectures and systems to expedite the adoption of smart infrastructure. Operationally, they require cloud platforms' resource management capabilities to automate workflows and enable smart operations. Ecologically, enterprises rely on next-generation cloud-based smart tools to enhance product development efficiency and industrial synergy, fostering smart innovation. After more than a decade of development, cloud computing, when combined with AI, especially large models, is evolving into a more intelligent form.

The "Second Growth Curve" of Cloud Computing

Generative AI is transforming industries, and "going cloud" is often the first choice for enterprises seeking to navigate this new era. Generative AI not only relies on cloud computing but also provides new impetus for its growth. Microsoft, with OpenAI as its copilot, is a prime example.

Microsoft released its fiscal Q3 2024 earnings report on April 25th, revealing that its cloud business generated revenue of $35.1 billion, up 23% YoY. Intelligent Cloud Services revenue reached $26.7 billion, up 21% YoY, with Azure and other cloud services growing 31% and AI contributing 7% of Azure's revenue, up from 6% in Q2 2024 and 3% in Q1. Apple's AI strategy, notably, revolves around integrating ChatGPT, allowing users to invoke Siri and ChatGPT across system-wide writing tools for chatbots, image generation, and more. These requests are processed in the cloud, highlighting AI inference's cloud-centric future for at least the next three to five years. China's market is also preparing, with Huawei Cloud's Ascend Cloud Service, launched in September 2022, offering efficient large model training environments and toolchains for end-to-end development of 100 billion-parameter industry models, reducing development time from 5 months to 1 month. Large model vendors are also turning to cloud training and inference, with MiniMax leasing cloud computing power instead of buying GPUs. Beyond cloud and large model vendors, many large and medium-sized enterprises in traditional industries are adopting AI and cloud as strategic directions.

Taking the automotive industry as an example, intelligent and connected vehicles are expected to exceed 90% penetration in the next five years, generating petabytes of data. Given the underutilized value of automotive data, AI-driven data application is essential. Cloud-based autonomous driving data closed-loop platforms build an end-to-end AI foundation spanning computing power, algorithms, and data. If resource and application cloud adoption represent cloud computing's "first growth curve," surging generative AI demand will create a "second growth curve," opening new incremental markets as foundational resource demand gradually saturates.

Cloud Giants Forge Ahead in Large Model Ecosystems

Domestic cloud giants have all-in on AI since last year. The IaaS+PaaS market saw its lowest YoY growth rate in nearly three years in the first half of this year, making large models a new growth driver for cloud vendors, with AI ecosystems as a vital component. Alibaba Cloud introduced the MaaS (Model as a Service) concept in late 2022, coinciding with ChatGPT's rise. At the 2023 Yunqi Conference, Alibaba Cloud CTO Zhou Jingren revealed that half of China's large model companies, including Baichuan Intelligence, Zhipu AI, Lingyi, Kunlun Tech, vivo, and Fudan University, run on Alibaba Cloud.

Alibaba Cloud's ModelScope offers two services: direct access to computing power, large model training, and inference platforms, and one-stop services for ecosystem partners; and model re-development, providing model and data training with scenario-specific optimizations. Tencent Cloud has also made strides, announcing a 200% YoY increase in integrated revenue over the past two years at its Tencent Cloud Ecosystem Conference earlier this year. After launching its large model, Tencent Cloud allocated 80%-90% of integrated business revenue to partners. Tencent Cloud has accelerated its "integration" business, transitioning from a "prime integrator" role to an ecosystem based on the MaaS model. This shift has deepened Tencent Cloud's industry expertise in verticals like healthcare, finance, tourism, media, government, and education.

Many of these vertical large models are developed in collaboration with ecosystem partners. Tencent Cloud provides PaaS capabilities, while large enterprises in verticals contribute data and requirements. Professional vertical model development teams then complete industry-specific private deployments. Huawei Cloud is also active, collaborating with software partners, service partners, consulting and system integration partners to support the deployment of Pangu large models, open-source models, and third-party commercial models. Huawei Cloud offers data engineering, model development, and application development suites to help users build independent datasets and upgrade base models. Alibaba Cloud, Tencent Cloud, and Huawei Cloud have adopted more open and decisive attitudes towards ecosystem development at the MaaS level, providing ample space for ecosystem partners in computing power and data. Each vendor's MaaS ecosystem is now well-established, leveraging computing power as a foundation and focusing on large model collection, annotation, pre-training, and other aspects to accelerate ecosystem development and support large model deployments.

The Evolution of Cloud Vendors' "Public Cloud" in the Era of Large Models

The shift from IaaS+PaaS+SaaS to IaaS+PaaS+MaaS represents a new profit model for cloud vendors in the era of large models. This transition from SaaS to MaaS signals cloud vendors' commitment to an "integration" ecosystem model, aligning with the trend towards "public cloud + AI." Public clouds significantly reduce AI model costs due to GPU computing power shortages, while their AI large model offerings drive cloud vendor growth. Cloud vendors earn revenue through API calls charged per token count or by providing secondary development services to large enterprises. The former relies on the vendor's computing power, while the latter leverages domain partners.

Alibaba Cloud, Tencent Cloud, and Huawei Cloud have focused on developing vertical large models, training domain-specific models with leading enterprises in those verticals, and integrating their capabilities into public cloud models. This enhances base model capabilities and integrates them into products like Baidu Wenku, Tencent Meeting, and Alibaba's DingTalk. Overseas cloud vendors have also explored AI large model ecosystems, with Microsoft Azure offering GPT-based services through deep integration rather than developing its own large model. Microsoft products like Windows, Office, and Bing feature AI Copilot assistants, forming a cloud-AI-software business loop. Cloud computing's growth engine is shifting from price-driven to demand- and value-driven, compelling vendors to reallocate resources to core areas and return to rational growth. AI's disruption of cloud computing is just beginning. Future cloud services will be scenario-centric, leveraging large model capabilities to transcend functional boundaries and deeply address scenario-specific problems. Cloud computing will gradually evolve from a resource-based system to an underlying system for the intelligent world. A new era has dawned, with new energies integrating and new waves surging forward.

"Large Models + Robots": Embodied AI Ushers in the "Age of Intelligent Machines"

AIGC Sparks a Revolution in Computing Power Demand, Making Edge Computing No Longer 'Edge'

From 'Computing Power Nuclear Bomb' to Generative AI: How Far Are We from the New Era?

Large Models Drive Technological Waves, Posing a 'Grand Examination' for AI Safety Governance

AI and Cloud Computing Co-evolve: Can They Unlock the Next High-growth Space?

-

![]()

Internet Valuation Logic Shifts: From Scale Narrative to Profit Accountability

-

VOYAH Struggles to Find Its Niche in the Competitive Auto Market

-

![]()

Maxwell Technologies Gains Indirect Stake in Precision Optics via New Venture

-

![]()

Raising 1.8 Billion! This Domestic Optical Inspection 'Little Giant' is Going Public

-

China's AI 'Normandy Moment': The Explicit and Implicit Threads of BATL

-

![]()

Starting at 4999 Yuan! Nubia RedMagic Gaming Tablet 5 Pro Review: Impressive Performance, But Hefty Price Tag

-

![]()

ByteDance Initiates First Major Management Reform

-

![]()

AI is Quietly Destroying a Trillion-Dollar Industry