Apple and Huawei Accidentally 'Teamed Up' to Silence Xiaomi

04/20 2026

04/20 2026

649

649

Actually, OV is hurting too, but the alarm hasn't sounded yet

It's unclear who the 'others' in the smartphone market are, but Xiaomi is clearly struggling under the pressure from Huawei and Apple.

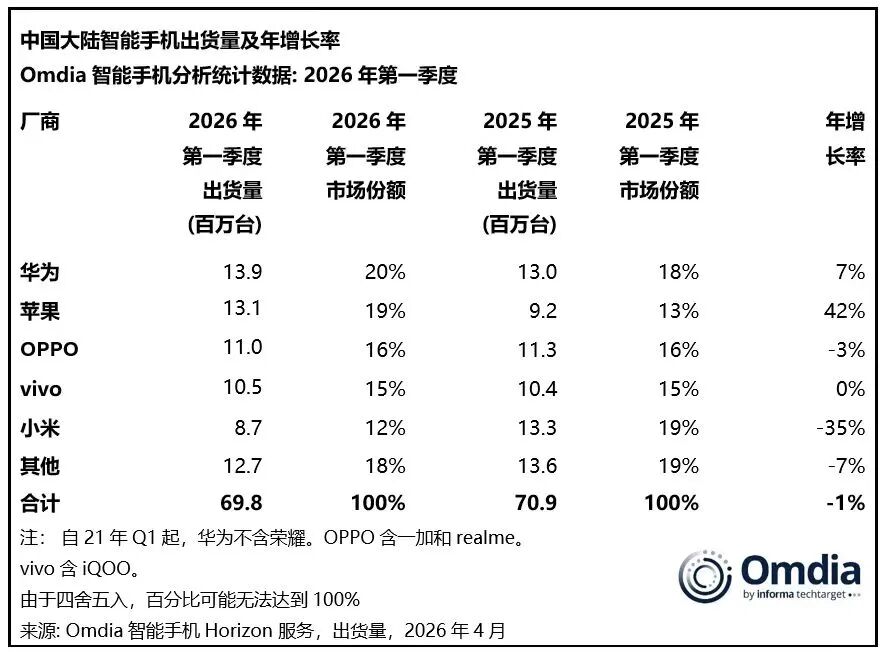

A few days ago, Omdia released data on China's domestic smartphone market for Q1 2026, showing total shipments reached 69.8 million units, down slightly by 1% year-on-year.

Huawei led with 13.9 million units shipped, capturing 20% of the market share. Apple surged 42% year-on-year, leveraging its high-end market advantage, with 13.1 million units shipped and a 19% market share. The most striking was Xiaomi, which, despite not raising prices on its main models, saw a 35% plunge due to peer competition.

Soon after, IDC's latest report further corroborated the credibility: Q1 shipment volumes and market shares by brand were similar to Omdia's data.

However, Xiaomi's exact decline was unknown as Honor took its fifth-place spot, relegating Xiaomi to the 'others' category.

Huawei topped the list with a 19.8% share, up 8.1% year-on-year, driven by ample supply of flagship models and volume push in low-end devices. Apple followed with an 18.9% share, surging 33.3% year-on-year. Sustained demand from high-end upgraders and stable iPhone pricing amid Android price hikes and reduced discounts fueled Apple's growth.

IDC's Global Quarterly Market Report showed Xiaomi's global growth also slowed by nearly 20%, the largest drop among the top five, directly linked to its heavier reliance on low-end smartphones.

From both agencies' data, Xiaomi and Honor are struggling similarly, with Xiaomi at 8.7 million units and Honor at 8.9 million—a gap easily reversible with slight statistical adjustments.

Under this extreme supply chain stress test, why did Apple and Huawei easily edge out Xiaomi, which had spent five years 'benchmarking and learning from Apple,' leaving it at the same table as Honor in Q1?

01

Don't Blame Apple for Stockpiling Storage

Is Xiaomi's Eight-Year Price Hike the Real Culprit?

Xiaomi's struggle against Apple is unsurprising, as the competition isn't just at the retail level but also involves supply chain pressure.

On April 3, Korean media Wccftech reported that Apple was aggressively procuring mobile DRAM at high prices, with sources saying Apple nearly 'cleaned out available mobile DRAM in the market' to secure capacity amid supply crunches and strengthen supply chain control.

This strategy aligns with recommendations from TF Securities analyst Ming-Chi Kuo, suggesting short-term profit concessions for long-term market share, turning the industry's chip shortage into a bottleneck for competitors.

In other words, Apple paid a premium to monopolize DRAM, prioritizing starving Android rivals over its own immediate usage needs.

Before Apple squeezed the memory market, Android phones were already struggling.

On March 10, OPPO and OnePlus announced price adjustments, effective March 16, for their OPPO A series, K series, and existing OnePlus models.

Six days later, vivo issued a notice on price adjustments for select vivo and iQOO products, citing significant global semiconductor and storage cost increases. After careful evaluation, vivo would adjust suggested retail prices starting at 10:00 AM on March 18, 2026.

In April, Xiaomi also announced price hikes. REDMI K90 Pro Max would increase by RMB 200, while Turbo 5 and Turbo 5 Max would cancel their New Year promotions, though 512GB models would retain a RMB 200 subsidy.

This made Apple, rarely associated with cost-effectiveness, suddenly seem like a bargain.

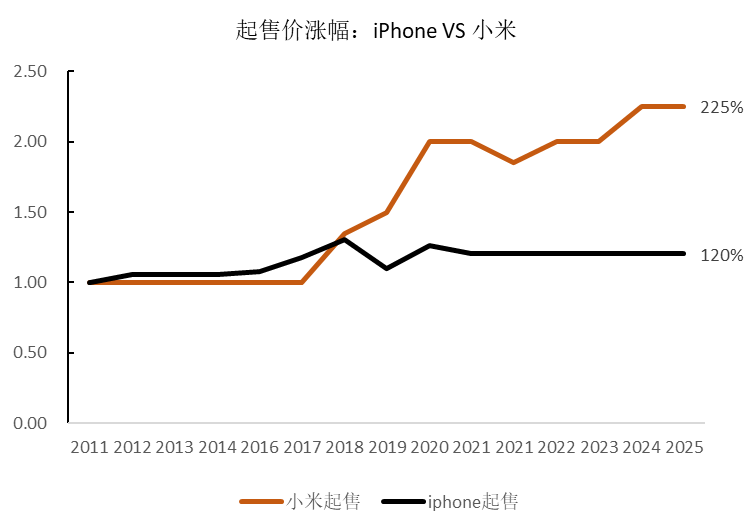

Over the years, Xiaomi's 'premium push' has been a steady price climb. According to 36Kr, since the Xiaomi 6's first price hike, each subsequent flagship's starting price has risen over 10%. The Xiaomi 10 series in 2020 marked a turning point, with its starting price soaring by RMB 1000 to RMB 3999, a >30% increase. After years of consolidation, Xiaomi stabilized the RMB 4000 segment, raised the baseline to RMB 4499 with last year's Xiaomi 15, and maintained this pricing with this year's Xiaomi 17.

While Xiaomi's flagships climbed, Apple remained remarkably consistent. Aside from minor 5G transition adjustments, Apple has largely kept prices steady while increasing specs. Since the iPhone 13 series, the standard model's starting price has been anchored at RMB 5999.

This dynamic has shifted the competitive landscape. In 2011, the iPhone 4S's starting price was nearly RMB 3000 higher than the RMB 1999 Xiaomi 1; now, the RMB 5999 iPhone and RMB 4499 Xiaomi have narrowed the gap to just RMB 1500.

Source: 36Kr

Not just Xiaomi's flagships—the Redmi K20 Pro to K90 Pro also jumped from RMB 2499 to RMB 3999, with top variants nearly matching Huawei's un price increase flagship Mate series.

Thus, amid a shrinking price gap, Apple's brand premium and price stability unexpectedly highlighted its 'cost-effectiveness' in the high-end market. This storage-driven price hike acts as a catalyst, and without Q2 policies to boost sales, Xiaomi's shipment decline may be unstoppable.

02

Huawei 'Backstabs' Xiaomi

Who Rules the Mid-to-Low-End Market?

If Apple's pricing discipline was a 'wall' Xiaomi hit in this storage price surge, Huawei's affordable volume strategy was even more proactive.

As the only major domestic player not raising prices, Huawei's 2026 move to 'reclaim' the mid-to-low-end market was a counter-trend play.

In late March, Huawei launched three new Enjoy series models—Enjoy 90 starting at RMB 1299, Enjoy Plus at RMB 1499, and Enjoy 90 Pro Max at RMB 1699 (top 512GB version RMB 2399). This was no easy feat in 2026, when peers were either hiking prices or cutting low-end lines. Despite achieving supply chain localization amid sanctions, storage cost hikes still impacted Huawei.

Yet Huawei, unlike rivals, didn't raise prices but doubled down on unprofitable mid-to-low-end markets.

While Apple's 'money power' stockpiling targeted high-end rivals, Huawei's move was like setting fires in peers' backyards. By offering large storage in budget models despite cost pressures, Huawei's unconventional 'self-damaging' tactic caught competitors off guard.

Strategically, this was one of Huawei's few windows of opportunity.

On the surface, Huawei faced short-term cost pressures, but the global storage price surge became its 'best ally' in returning to mid-to-low-end markets. If supply chains were stable, Android players would have entrenched positions in budget segments, making Huawei's breakthrough against Redmi and iQOO a protracted price war.

Now, sudden price hikes forced rivals into a corner: 'raise prices and lose users, or cut lines to protect profits.' Huawei's counterintuitive advance easily filled the market vacuum left by peers.

This choice to sacrifice margins for volume relied on group support.

According to Guangzhui Intelligence, sources close to Huawei said the company would prioritize expanding its new HarmonyOS ecosystem in mid-to-low-end markets.

They emphasized that since last year, Huawei has pushed offline channel expansion via provincial agent (agents), setting targets for Sinking customers ( Sinking customers : lower-tier customer) growth and sales volumes across price segments to penetrate Small and medium-sized merchants (small-to-medium merchants) and Township Market (rural markets) beyond chain stores, consolidating market share gains.

In 2026, Huawei's focus on mid-to-low-end markets put Xiaomi and Redmi in a bind.

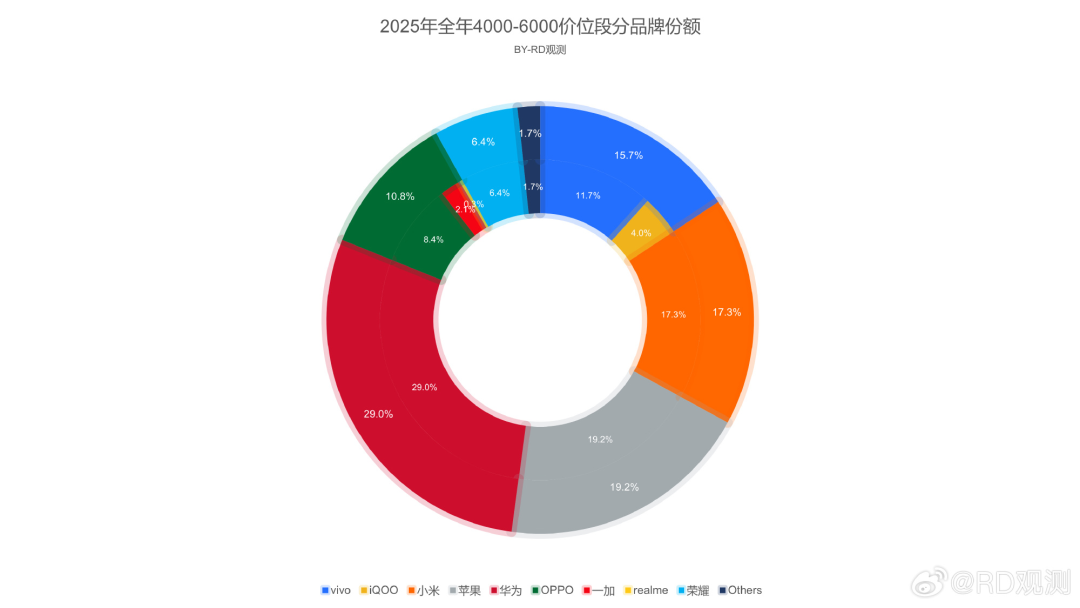

Upward, Apple's pricing and supply chain ceiling blocked Xiaomi's premium ambitions. When Xiaomi tried raising flagship prices above RMB 5000, users' 'cost-effectiveness' mindset hindered its premium push. Research by blogger 'RD Observation' showed Xiaomi held 17.3% of the RMB 4000-6000 segment in 2025, ranking second among domestic brands.

Downward, Huawei's guerrilla tactics breached Xiaomi's core market. As Redmi raised prices due to storage costs, Huawei's Enjoy series eroded Xiaomi's lower-tier market through brand downgrading. Agents close to terminal operations revealed Huawei's budget phones performed well, capturing nearly 25% regional market share in some areas.

Persisting in a high-end battle with Apple would strain revenues; competing head-on with Huawei in mid-to-low-end markets would hurt profits. Xiaomi's stock nearly halved in six months, and investors wouldn't accept either option, leaving Xiaomi 'treading water' and waiting for an opening.

Thus, shipment declines became inevitable. To survive this cycle, Xiaomi may need to redefine 'premium.'

True premium status can't rely solely on spec comparisons and price hikes in launch events without absolute supply chain control or full-stack self-developed core technologies. Such 'premium' is fragile 'pseudo-premium.'

During rapid growth, Xiaomi could snowball 'cost-effectiveness,' but supply chain volatility leaves it trapped between 'losing users via price hikes' and 'sacrificing margins to hold share.'

Yet the immediate reality may be harsher: How will Xiaomi solve this dilemma posed by Cook and Yu Chengdong, oceans apart and utterly uncoordinated?

- END -

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving