The 400,000 Yuan Lifeline: Six Domestic Flagship SUVs, Their Fates Sealed Before Launch

04/20 2026

04/20 2026

449

449

April 17, 2026: Two launch events on the same day.

The Zeekr 8X officially launches, securing over 10,000 orders in 38 minutes of pre-sale and reaching 30,000 orders within 48 hours. The Wey V9X opens pre-sales, with Great Wall Chairman Wei Jianjun personally endorsing it—he’s staking his family name on this vehicle.

Just a year prior, Aito had already delivered 170,000 units of the M8, Nio delivered 90,000 units of the all-new ES8 in 195 days, and the Zeekr 9X maintained its position as the best-selling model in the 500,000 Yuan segment for four consecutive months with an average price of 530,000 Yuan. In one price segment, six models, two distinct fates.

This article answers three questions:

Why are all domestic brands crowding into the 400,000 Yuan segment this year?

What’s the real significance of this move for each brand?

And—which three models will meet expectations, and which three are destined to struggle?

We hope this article provides insights for professionals in product strategy, development, supply chain, investment, and even car buyers. There’s a poll at the end to see which of this year’s Chinese premium new energy vehicles targeting the 400,000 Yuan mark you think will succeed.

I. Introduction: The 400,000 Yuan Chinese New Energy Vehicle Phenomenon

Three common misconceptions about this collective charge:

Misconception 1: "All targeting 400,000 Yuan means homogeneous competition."

Wrong. Aito M8 sells as the 'Huawei Family Flagship,' Nio ES8 as the 'Pure Electric Three-Row Battery-Swap Flagship,' Zeekr 9X as the 'SEA 900V Luxury Hybrid,' Wey V9X as the 'Yuan Platform + Oriental Aesthetics,' and XPeng GX as the 'AI Luxury Six-Seater'—each sells unique emotional value, not just specs.

Misconception 2: "400,000 Yuan is a product definition issue; nail the definition and you succeed."

Also wrong. These vehicles all offer top-tier specs—air suspension, rear-wheel steering, LiDAR, 800V/900V architecture, 100+ kWh batteries, 0-100 km/h in 3-5 seconds, AI-assisted driving, and smart cockpits. But specs are just the entry ticket; emotional equity, locked in before launch, determines success or failure.

Misconception 3: "400,000 Yuan is the inevitable path for domestic brands to break upward."

Partially true, but incomplete. More accurately, 400,000 Yuan represents the last window for domestic brands to achieve premium positioning. Above (500,000+ Yuan), Aito M9 dominates; below (250,000-300,000 Yuan), it’s a bloodbath. Only the 350,000-500,000 Yuan segment, vacated by BBA, remains open. That’s the real logic behind this collective charge.

II. Current State: Same Price, Vastly Different Starting Points

First, divide the six models into two groups: 'Proven' vs. 'Unproven.'

2.1 The Three Proven Models: Uneven Starting Lines

Aito M8 (Launched April 2025)

170,000 cumulative deliveries in one year

#1 in 400,000 Yuan SUV sales—4 out of every 10 sold in this segment are M8s

466 daily deliveries, consistently over 15,000 monthly

Emotional equity sources: Huawei brand halo + Aito M9’s success + HarmonyOS Smart Mobility ecosystem

Nio All-New ES8 (Launched September 2025)

40,000 deliveries in 100 days—fastest record for models above 400,000 Yuan

90,000 cumulative deliveries in 195 days, three consecutive months as the best-selling model above 400,000 Yuan

In Hefei: 2 out of every 3 large SUVs sold are ES8s

Emotional equity sources: 7-year owner community + battery-swap network (exclusive) + ET9 technology devolution

Zeekr 9X (Launched September 2025)

10,000 deliveries in a single month, four consecutive months as the best-selling large SUV in the 500,000+ Yuan segment

Average transaction price exceeds 530,000 Yuan (list price: 455,900-599,900 Yuan)

3 out of every 10 new energy vehicles sold above 500,000 Yuan are 9Xs

80% of pre-sale buyers traded up from luxury brands, with 70% previously owning 500,000+ Yuan vehicles

Emotional equity sources: Geely Group ecosystem + SEA-S architecture tech label + selected as China Aerospace support vehicle

2.2 The Three Unproven Models: Riding Trends vs. Breaking Through

Zeekr 8X (Launched April 17, 2026)

10,000 orders in 38 minutes of pre-sale, 30,000 in 48 hours

Positioned as a 'high-performance large five-seater,' targeting BMW X5 and Porsche Cayenne

Technically aligned with the 9X (SEA-S, triple-motor megawatt drivetrain, 900V 6C ultra-fast charging)

Emotional equity source: Leveraging 9X’s momentum—Zeekr has already established itself as a 500,000 Yuan benchmark

Wey V9X (Pre-sale launched April 17, 2026, expected May launch)

Pre-sale price starts at 371,800 Yuan, targeting Li Auto L9 and Aito M9

First model on Great Wall’s Yuan S platform, based on the 2.0T Super Hi4 hybrid

Wei Jianjun personally endorses it—'staking his family name'

Emotional equity source: Great Wall’s 30-year automotive reputation + Oriental architectural aesthetics + Wei Jianjun’s personal IP

XPeng GX (Expected Q2 2026 launch)

Expected 300,000-400,000 Yuan price range, first model on SEPA 3.0 physical AI vehicle architecture

Positioned as an 'AI new luxury six-seater SUV,' dubbed the 'Greater Bay Area Range Rover'

XPeng X9 MPV genes devolved + pure electric/range-extended dual powertrains

Emotional equity source: XPeng’s AI autonomous driving label + spillover success from the MONA M03 phenomenon

Prop comparison: With pre-sale prices starting at 370,000 Yuan, Zeekr 8X hit 10,000 orders in 38 minutes, while XPeng GX and Wey V9X haven’t released pre-order numbers—market responses aren’t in the same dimension.

III. Contrast: Fates Sealed Before Launch

This is the article’s most counterintuitive yet crucial insight:

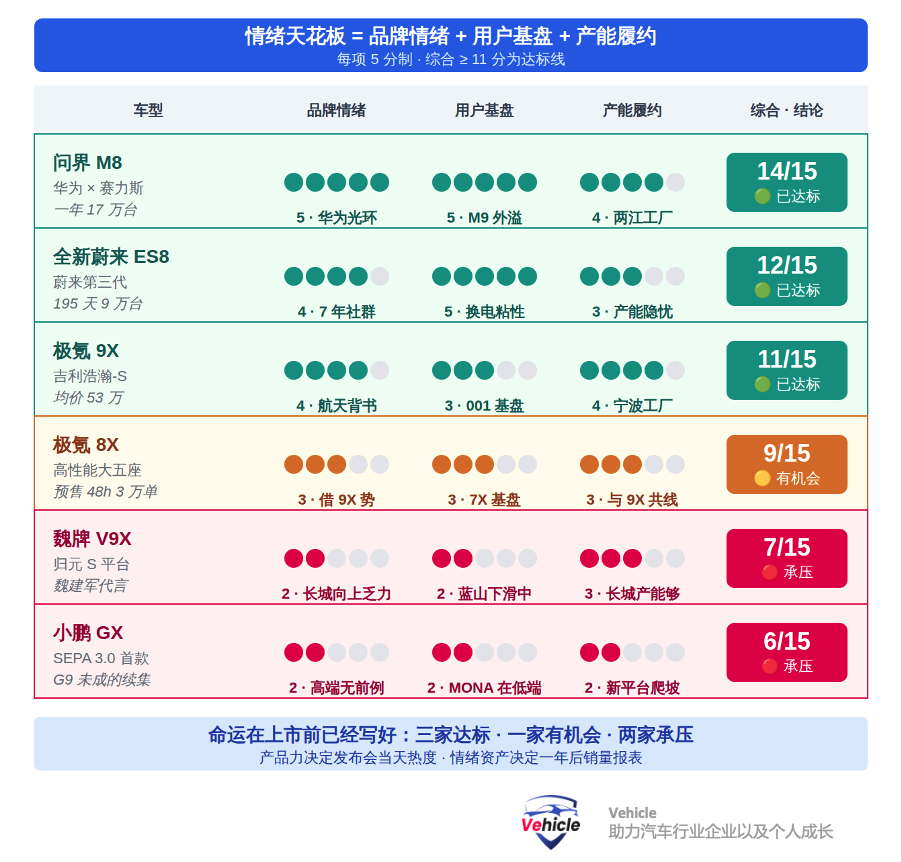

The destinies of these six models were largely locked in before their launch events by three factors: brand emotional equity, user base, and production fulfillment capabilities. Product strength determines launch-day hype, but emotional equity determines the numbers on the sales report a year later.

This isn’t a pessimistic conclusion; it’s a structural reality. Using the 'Emotional Ceiling Tri-Factor Formula' (tech premium + brand emotional premium + scarcity premium) to rescan these six models yields clear results.

3.1 Emotional Equity of the Six Models

Scoring dimensions (5 points max per category):

Brand emotion: Willingness to pay 50,000-100,000 Yuan extra for the badge

User base: How many orders existing owners/fans can contribute

Production fulfillment: Ability to maintain stable deliveries within six months of launch

3.2 Case Study 1: How Zeekr 8X Leveraged 9X’s Momentum

Zeekr 8X’s 10,000 pre-sale orders in 38 minutes stem from the foundation laid by the 9X six months earlier. Consider these details:

80% of 9X pre-sale buyers traded up from luxury brands—now recommending Zeekr to others

9X’s 530,000 Yuan average price established 'Zeekr = true luxury' perception

8X’s 'large five-seater + performance' positioning fills the family/sport gap left by the 9X’s six-seater business focus

Technically, 8X and 9X share the same DNA, so consumers don’t need to relearn the story

That’s why the 8X’s 376,800 Yuan pre-sale price was widely seen as 'below expectations'—Zeekr no longer needs to prove itself with low pricing.

3.3 Case Study 2: Why Wei Jianjun Had to Personally Endorse the V9X

Great Wall is a company whose brand emotion has long been underestimated. Haval created the national SUV (H6 cumulative sales: 5M+), but that label doesn’t translate upward to Wey. The Wey Blue Mountain’s monthly sales slipped from 10,000+ to 5,000, while the High Mountain MPV only gained traction at 280,000-350,000 Yuan—every price tier jump requires rebuilding trust.

The V9X, priced at 370,000+ Yuan, doesn’t need product strength (it has that); it needs a reason for consumers to pay 100,000 Yuan extra for Wey. Wei Jianjun’s personal endorsement provides that reason.

But this tactic has a flaw: it’s a one-time play. Wei can stake his name on one model, but not ten. If the V9X doesn’t hit 50,000+ sales in its first year, the next Wey flagship will struggle to replicate this approach.

3.4 Case Study 3: Why XPeng GX Faces the Toughest Challenge

XPeng’s issue is that it hasn’t successfully told a premium story before. The G9 underwent multiple revisions, struggling in the 250,000-280,000 Yuan segment. The X9 MPV built word of mouth (reputation), but in limited volumes. XPeng’s sales boom came from the 100,000-150,000 Yuan MONA M03.

This means XPeng must solve two problems simultaneously with the GX:

Persuade consumers that XPeng can deliver 300,000-400,000 Yuan luxury

Persuade consumers that the G9’s issues (insufficient space, missing family features) are resolved in the GX

Solving two narrative challenges at once is the hardest task. In comparison:

Aito only needs to convince consumers that 'Huawei family vehicles are superior'—the M9 already educated the market

Nio only needs to convince existing owners that 'the new ES8 is better than the old one'—the community is already built

Zeekr only needs to convince consumers that 'the 8X is the 9X’s sibling'—the 9X already proved itself

XPeng GX must start from scratch and compete head-on with established players. This is arguably the toughest battle in this 400,000 Yuan war.

Key Takeaway: The decisive factors in this war aren’t product strength or price, but three pre-locked elements: brand emotion, user base, and production fulfillment.

IV. Broader Context: Why 2025-2026?

Zooming out, this collective charge into the 400,000 Yuan segment results from three structural opportunities opening simultaneously.

4.1 Opportunity 1: Aito M9 Raised the Ceiling

Aito M9 delivered 280,000 units in 2024-2025, dominating the 500,000 Yuan segment for 20 consecutive months. It proved something domestic brands once dared not believe: Chinese consumers will pay 500,000+ Yuan for a domestic SUV if the brand emotion is strong enough. M9’s success shifted the industry’s perception upward: if 500,000+ Yuan is real, 400,000 Yuan is no longer a ceiling but a reasonable 'quasi-flagship' segment.

4.2 Opportunity 2: BBA’s Electrification Void

Traditional luxury SUVs like the BMW X5, Mercedes GLE, and Audi Q7 (500,000-800,000 Yuan) lag in electrification. Their pure electric/plug-in hybrid versions are either overpriced, underpowered, or suffer from range/charging issues. This left a 350,000-600,000 Yuan void. The fact that 80% of Zeekr 9X pre-sale buyers traded up from luxury brands confirms this: consumers are switching, but need a BBA alternative.

4.3 Opportunity 3: Core Technologies Matured

By 2025-2026, several technologies matured in domestic brands’ hands:

800V/900V architectures (Zeekr, Nio, XPeng all have them)

6C ultra-fast charging + large battery combos (solving range anxiety)

VLA/VLM large model autonomous driving (XPeng, Zeekr, Great Wall, Nio all deploying), plus Huawei sensor fusion

Air suspension + rear-wheel steering (devolved from 1M+ Yuan to 300,000 Yuan segments)

These technologies collectively make '400,000 Yuan pricing with 600,000 Yuan product strength' possible—something unachievable for domestic brands in 2022-2023.

4.4 But the Window Is Closing Fast

This charge carries an implicit timer: 2026 is the window; by 2027, it may slam shut. Two forces approach:

Force 1: BBA’s Counterattack

By 2026-2027, BMW’s Neue Klasse, Mercedes’ MMA, and Audi’s PPE electric platforms will launch. Once their products stabilize, the void will refill.",

V. A Framework for Judgment for Three Types of Readers

For Decision-Makers: Predictions on the Divergent Outcomes of Six Models

Based on a comprehensive analysis of the three key elements of the emotional ceiling, the divergence observable by the end of 2026 includes:

The Achievers (Annual Sales of 100,000+)

AITO M8: Already meeting the target, aiming for 180,000-220,000 units in 2026

NIO ES8: Highly likely to meet the target, projected to reach 150,000+ units by the end of 2026

Zeekr 9X: Meeting the target but with a ceiling (500,000+ is a small pool), 100,000-120,000 units in 2026

The Contenders (Annual Sales of 30,000-80,000)

Zeekr 8X: Clear leverage effect, but needs to avoid internal cannibalization with 9X; 60,000-80,000 units annually is reasonable

The Pressured (Annual Sales of <30,000, with a probability exceeding 60%)

WEY V9X: Insufficient emotional appeal from the Great Wall brand, and Wei Jianjun's personal IP is difficult to sustain in the long run. Achieving 30,000-50,000 units would already be a victory.

XPENG GX: Incomplete high-end narrative, likely to repeat the fate of G9, with annual sales probably below 30,000 units

Corresponding Investment Observation Points:

Whether AITO M8 can maintain monthly sales of 15,000+ (testing the erosion from internal competition within Harmony Intelligent Mobility Alliance)

Whether NIO ES8's battery-swapping advantage can be translated into brand premium (testing user stickiness in the pure electric era)

Monthly sales of WEY V9X three months after delivery (testing the true ceiling of Great Wall's premiumization)

Pricing of XPENG GX (below 330,000 yuan would make it a substitute for G7, while above 350,000 yuan might lead to failure)

For Practitioners: Four Paths to Break Through the Emotional Ceiling

From the strategies of the six models, four feasible paths to break into the 400,000 yuan price segment can be summarized:

Leveraging Brand Emotion (AITO Model) - Borrowing emotional assets from the parent brand, but the parent brand must be a tech brand, not a manufacturing brand.

Leveraging Community (NIO Model) - Using 7-10 years of accumulated assets in battery swapping, community, and services, with high barriers to entry but stable returns.

Leveraging Flagship Models (Zeekr Model) - First establishing a benchmark with ultra-high-end models (9X, U8), then introducing sub-premium models (8X) to capture volume.

Leveraging Personal IP (Wei Jianjun, Lei Jun Model) - The founder's personal IP becomes the primary source of brand emotion, but the ceiling depends on the scale of the IP.

Note: None of these four paths are "product strength paths." Relying solely on product strength cannot break through the 400,000 yuan barrier—this is the most important lesson from this collective charge for all practitioners.

For Researchers: Three Structural Issues Worth Tracking

Can the "emotional ceiling" of domestic brands move up further?

AITO M9 has pushed it to 500,000 yuan+. Where will the next breakthrough occur? Can ZEEKR S800 replicate AITO's path in the 700,000-1,000,000 yuan segment?

The Compound Effect of Brand Emotional Assets

The path from Zeekr 9X to 8X has validated the feasibility of "flagship models setting benchmarks, sub-flagship models capturing volume." But to what price segment can this model be replicated? Can brands like DENZA, FANGCHENGBAO, XPENG, and NIO follow suit?

The Pace of Joint Venture Brands' Electric Counterattack

After the launch of new platforms like BMW Neue Klasse and Mercedes MMA in 2027, how much of their home turf will be reclaimed? How much of the market share currently captured by domestic brands can be defended? This will determine the final landscape of China's luxury car market from 2028-2030.

The Ultimate Question: What is the True Significance of This 400,000 Yuan Battle?

It's not about who wins or loses among the six models. It's about domestic brands truly standing at the negotiating table for luxury cars for the first time.

Over the past decade, the story of China's automotive industry has been about "trading cost-effectiveness for market share"—from the 50,000 yuan segment (Wuling) to the 100,000 yuan segment (BYD Qin PLUS), and then to the 200,000 yuan segment (Li Auto L6, XPENG G6). In each round, prices were pushed down while configurations were piled up.

This round is different. AITO, NIO, Zeekr, WEY, and XPENG—five companies are using the same top-tier technologies to create the same flagship models in the same price segment and at the same time window. They are not competing for the cost-effective market but redefining the Chinese meaning of "luxury."

Some will win, and some will lose. But regardless of the outcome, one thing is already established: 2026 will be the most critical year in the history of China's domestic luxury car brands. Looking back a decade later, this might be the true significance of the 400,000 yuan battle.

*Reproduction or excerpting without permission is strictly prohibited-

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’