Blockade of the Strait of Hormuz: Impacts on China and the Global Auto Industry

04/20 2026

04/20 2026

622

622

Today is April 18, 2026. In the early morning, an Iranian spokesperson announced via state television that the Strait of Hormuz had "returned to its previous state"—meaning that after declaring it "fully open" just yesterday, it has now been closed again.

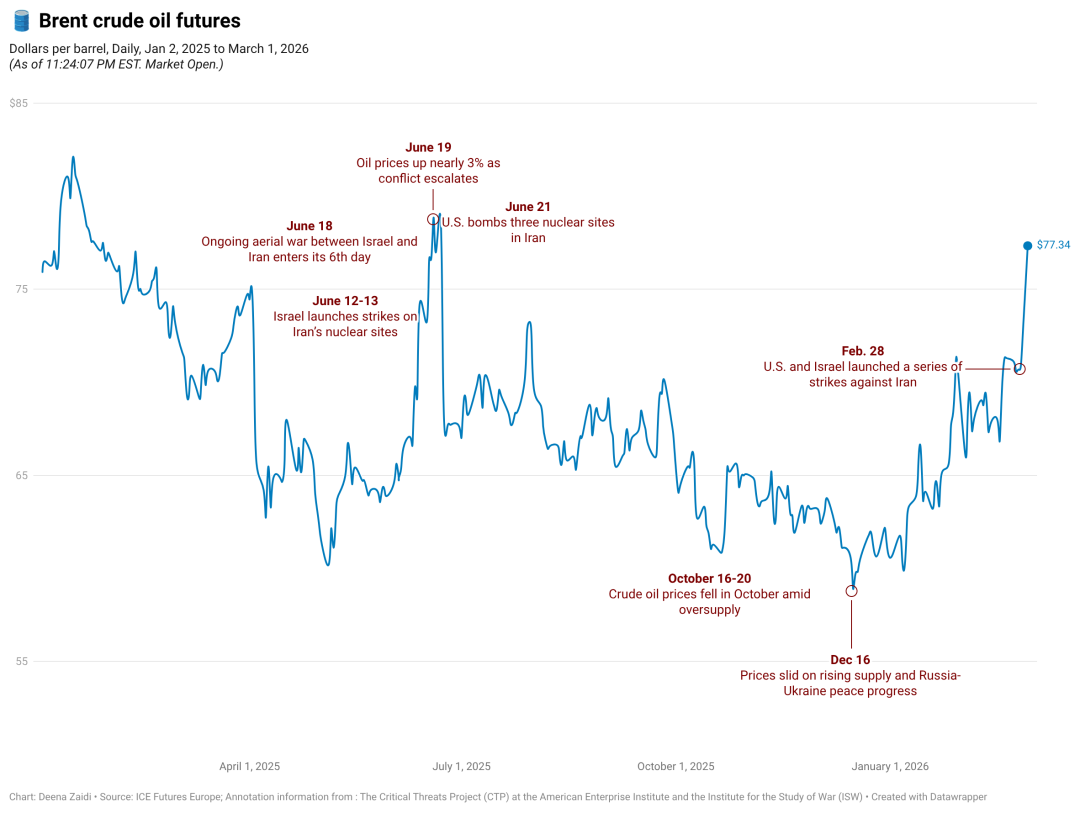

Starting from the joint U.S.-Israel airstrikes on Iran on February 28, this war has now lasted 50 days. Over the past seven weeks, the strait has been blocked, partially opened, blocked again, reopened, and then closed once more—headlines you see today may be outdated in just two hours.

However, one thing remains unchanged: the global automotive industry is facing, for the first time, a triple shock of "energy + logistics + upstream materials."

This article will help you answer four key questions:

What does this war mean for the global automotive industry?

How severely have China's auto imports and exports been impacted?

Where are the real pain points for Chinese automakers—and why are they different from what you might think?

What are the specific impacts of this war on the global automotive market?

A counterintuitive judgment upfront:

For China's automotive industry, the real damage from the Hormuz blockade is not in oil prices.

I'm not saying oil prices are unimportant. Brent crude surged from $80 before the war to $120, nearing the historic peak of $147 in July 2008. The International Energy Agency (IEA) has labeled this the "largest supply disruption in global oil market history." U.S. average gasoline prices rose by $0.43 per gallon in one week, and Australia has already seen fuel station shortages.

But China can withstand this.

Why? Here are four key data points:

Before the war, China's strategic crude reserves stood at approximately 1.39 billion barrels, sufficient to last 120 days at 2025 net import levels.

In 2025, Russia (via pipelines + maritime shipments) accounted for 17.8% of China's crude imports, none of which passed through the Strait of Hormuz.

While 35% of China's total crude supply passed through Hormuz, Saudi Arabia and the UAE have about 5 million barrels per day of production capacity that can bypass the strait via pipelines.

In April 2026, China unusually approved the use of commercial oil reserves by state-owned refiners, releasing about 1 million barrels per day to offset declining Middle Eastern supplies—without touching national strategic reserves.

China can sustain oil supply issues for over three months. This is the consensus view of Columbia University's Global Energy Policy Center and Vortexa.

But high oil prices are not entirely harmless—they strike China's automotive industry from an unexpected direction, as we'll explain below.

So where is the real trouble?

On the map of China's auto exports, specifically at a point called Dubai.

One number reveals the hidden pathway of China's auto exports:

A set of data that surprises many:

In 2025, China exported 567,000 vehicles to the UAE, a 70% year-on-year increase, surpassing Japan and South Korea to become China's third-largest auto export destination after Mexico and Russia.

That same year, local auto sales in the UAE were less than 400,000 units.

Where did the difference go? The answer lies in a comment from a Chinese automaker's export manager to Caixin:

"Dubai is essentially a forward warehouse. Many companies ship vehicles there first, then redistribute them to final markets in the Middle East, West Africa, and North Africa. Our company alone sent nearly 30,000 vehicles to Dubai last year."

In other words, the vast majority of vehicles exported to the UAE do not stay there. They are redistributed from Dubai's Jebel Ali Port to Riyadh in Saudi Arabia, Cairo in Egypt, Lagos in Nigeria, and even deeper into West African interiors.

This hidden "transshipment model" has been a core driver of China's auto exports over the past five years. The Middle East accounts for 17% of China's total passenger vehicle exports, with a compound annual growth rate of 59%—faster than Mexico or Russia.

Understanding this is crucial to grasping the real damage the strait blockade inflicts on Chinese autos.

How the damage unfolds: A vehicle's journey + A bill

Let's track a vehicle from Changan's factory in Chongqing to see its real-world experience during the war:

Day 0 (pre-war): Chengdu-Chongqing → Qinzhou Port in Guangxi (via the new "rail-sea intermodal" route opened in April 2025) → Jebel Ali Port, taking about 18 days—efficient and cheap for Middle East deliveries. Ocean freight cost per vehicle: ~$1,500.

Day 1 (March 1): Jebel Ali Port is hit by Iranian missiles, operations temporarily halted. Although DP World announces partial berth resumption hours later, major shipping lines suspend services—the port remains "technically open but practically empty."

Day 30 (late March): Marine war insurance premiums skyrocket from 0.015%-0.025% of cargo value to 0.125%, with some routes reaching 1%. For a roll-on/roll-off vessel carrying $150 million in cars, insurance costs for a single voyage surge from tens of thousands to over $1.5 million. Top maritime mutual insurers (P&I Clubs) like Gard, Skuld, and NorthStandard cancel coverage for the Persian Gulf.

Day 50 (today): Vessels entering the strait require approval from Iran's Revolutionary Guard Navy on a ship-by-ship basis. After rerouting around the Cape of Good Hope (why not use the nearby Bab al-Mandeb Strait in the Red Sea? However, due to Houthi attacks and spillover from Middle East conflicts, security risks in the Bab al-Mandeb and Red Sea routes are also extremely high), ocean freight costs to Saudi Arabia double from $1,500 to over $3,000 per vehicle. Delivery delays of 4-6 weeks are common for Chinese vehicles in first-tier cities across Saudi Arabia, the UAE, and Egypt, with some model orders being canceled.

Even more damaging is the ripple effect: Shanghai Port exported over 400,000 new energy vehicles in Q1 2026, averaging 6,600 per day, with Lingang South Port surging 176% year-on-year. But behind these robust numbers lies a fragile logistics node: Taicang Port (the largest automotive export base along the Yangtze River, with 771,600 vehicles exported in 2025) saw 3,000-4,000 vehicles backed up at its Haitong Auto Terminal awaiting shipment. Despite deploying foldable vehicle racks, specialized container loading, and green channels, port congestion persisted.

All this occurred just as China's auto exports surpassed 7.09 million vehicles (2025 CAAM data)—up 20% from 2024.

Another overlooked blow: Upstream materials

If exports represent "the road out being blocked," another strike comes from upstream supply chain vulnerabilities.

China's NEV industry has several little-known dependencies on the Middle East:

Celestite → Strontium Carbonate → Permanent Magnets for Motors: Iran controls ~85% of global high-grade celestite reserves, with China importing 60-70% from Iran. After air strikes on Bandar Abbas Port in March, domestic strontium carbonate prices doubled from 8,000 to 16,000 yuan per ton, with smelters holding only three months of inventory.

Low-Sulfur Petroleum Coke → Synthetic Graphite → Battery Anodes: China relies on imports for 62% of its needs, with the Middle East supplying over 75%. International prices have surged 42%, forcing NEV manufacturing costs up by 25-30%.

Methanol → Engineering Plastics, Polyurethane Foam (seats), Automotive Coatings: China imported over 7.92 million tons from Iran in 2025, accounting for 55%+ of total imports.

These aren't the familiar lithium, cobalt, or nickel, but each can halt an entire vehicle production line.

Their common traits: cheap, used in small quantities, extremely difficult to substitute, and highly concentrated in the Middle East.

This is the most dangerous combination in supply chains—topics that rarely make it onto executive agendas because they're neither "expensive" nor "sexy." But when disrupted, they paralyze entire industries.

This mirrors the 2021 automotive chip shortage, where a $5 MCU chip caused global automakers to lose hundreds of billions in output. The lesson: in supply chains, what determines your fate isn't the most expensive component, but the one most easily overlooked.

Oil prices strike from another direction: Collapsing fuel vehicle demand

Back to "oil." While China can withstand oil shortages, consumers cannot bear high prices—which reverse-strike the other half of China's auto industry: domestic fuel vehicle sales.

In March 2026, China's domestic passenger vehicle sales fell 15.2% year-on-year, with fuel vehicle sales dropping 15.7%. Dealer inventory indices continued to climb. The China Association of Automobile Manufacturers (CAAM) slashed its 2026 auto sales growth forecast from 9.4% (2025 actual) to just 1%. Industry average profit margins, already at a historic low of 4.1% in 2025, further bottomed out at 2.9% in the first two months of 2026.

Counterintuitively, high oil prices benefit NEVs.

Quantitative models show: at $100/barrel oil, NEVs effectively become 1.7%-3.7% cheaper. An estimated 100,000-360,000 vehicle purchases will shift irreversibly from fuel vehicles to NEVs by mid-2026 in China. For every 1 yuan/liter increase in gasoline prices, fuel vehicle sales lose an additional 750,000-850,000 units annually.

The European market is even more dramatic: German diesel prices briefly hit 2.50 euros/liter, with electric vehicle [electric vehicle] inquiries on Mobile.de and Carwow surging 20%-50% month-on-month in March.

To stabilize the market, China's government raised "trade-in" subsidies: up to 15,000 yuan for scrapping old vehicles to buy NEVs, and up to 10,000 yuan for fuel vehicles under 2.0L—clear policy tilt. These subsidies essentially use fiscal transfers to absorb upstream material price hikes, preventing terminal pricing collapses.

The outcome is bifurcated: The Hormuz blockade makes fuel vehicles harder to sell in China but accelerates NEV adoption. This war has, unexpectedly, become a catalyst for global electrification.

The real loser in the global auto industry: Japanese automakers

Zooming out globally, Japanese automakers are facing a severely underestimated disaster.

The Japanese automotive industry has two fatal weaknesses: 70% of automotive aluminum and 65% of automotive naphtha depend on Middle Eastern imports, almost entirely via the Strait of Hormuz. With the strait blocked, raw material transport cycles extend by over 20 days.

The consequences were immediate:

Toyota: Announced a 24,000-unit cut in Middle East export production in April.

Subaru, Mazda: Forced to completely halt Middle East export operations.

Japanese brands held ~30% market share across ten Middle Eastern countries (Toyota alone at 17%), with 870,000 units sold in 2025—a market now rapidly slipping away.

In stark contrast to Toyota and Subaru, Chinese automakers had already filled the vacuum in Iran during Western sanctions. AlixPartners predicts Chinese brands' Middle East and Africa market share will surge from 10% in 2024 to 34% by 2030. This war will only accelerate that shift.

But Chinese automakers shouldn't celebrate prematurely—doubled ocean freight costs, 10-15-day longer transit times tying up working capital, and exchange rate fluctuations are all sharply eroding export profits. Automakers who hoped to offset domestic price war losses with overseas premiums are now recalculating. Second- and third-tier automakers lacking global resource coordination capabilities face risks of cash flow ruptures.

Chinese automakers' responses: Three-tier strategy + One new policy

In 50 days of crisis, leading Chinese automakers have responded on three levels:

Level 1 - Rerouting: Ships bypass Hormuz via Oman's Duqm, Salalah, and Sohar deep-water ports. These ports on the Arabian Sea side theoretically avoid the strait but have far less capacity than Jebel Ali.

Level 2 - Order conversion: Temporarily switch export orders from "complete vehicles" to "KD/SKD kits + local assembly." BYD accelerated its 2026 factory launch in Turkey; FAW began building an EV production line in Egypt; Geely deepened local channels with Saudi Arabia's Aljomaih Group. KD factory construction in Saudi Arabia and Egypt was compressed from 3-5 years to 12-18 months.

Level 3 - Rail alternatives: The China-Europe Railway Express ran 5,460 trains in Q1 2026, shipping 546,000 TEUs—up 29% and 22% year-on-year, respectively. NEV-dedicated trains introduced electronic seals, cutting customs clearance to just 30 minutes. But be realistic: World Bank data shows rail accounts for <5% of China-Europe freight (vs. >95% maritime). The Central Asia corridor costs ~$5,500 per TEU—more than double the Northern Corridor. Rail can't save bulk vehicle exports, only high-value urgent shipments.

There's also an underestimated policy lever: The "Notice on Further Regulating Used Car Exports" implemented on January 1, 2026. The new rule requires vehicles registered for <180 days to provide original manufacturer "After-Sales Service Commitment Letters" for export—a direct blow to the rampant gray-market "zero-mileage used car" exports of recent years.

Why does this matter amid war? Because transport capacity is tight. Allocating precious roll-on/roll-off vessel space to legitimate exporters with overseas service networks, rather than speculative resellers without support—this is a "special rationing system" for capacity.

To recap the core judgment:

The real damage to China's autos from the Hormuz blockade isn't oil (which China can manage), but the fragility of an export system overly reliant on a single node:

17% of export volume concentrated in the Middle East;

Within that, heavily concentrated at Jebel Ali Port;

Which handles significant "non-UAE market" redistribution.

China's auto exports became global leaders over the past decade (nearly 6 million in 2024, 7.09 million in 2025) by leveraging an "efficient, low-cost, single-channel" export model. This model was an advantage in peacetime but a vulnerability during geopolitical conflicts.

This crisis will not cause a 'collapse' in China's auto exports—the assessment by Cui Dongshu, Secretary-General of the CPCA, is well-founded: short-term fluctuations do not alter long-term trends. However, it will permanently reshape the map of China's auto exports: shifting from the single-line model of 'shipping out from Shanghai/Guangzhou → transshipment in Dubai → global distribution' to a networked model of 'multi-port departures + multi-regional KD factories + multimodal transport.'

Put another way: this war has compressed the timeline for transforming China's auto industry from an 'export powerhouse' to a 'global production capacity nation' from five years to just two.

Data sources: Columbia University's Center on Global Energy Policy, AlixPartners, Vortexa, IEA, CAAM, CPCA, Caixin, Reuters, Bernstein, Wikipedia's 2026 Iran War entry, as well as domestic research data on strontium carbonate, petroleum coke, and methanol industries. All data is current as of the publication date of this article. Some images are AI-generated; while Jack has made every effort to verify them, they are provided for reference only.

*Reproduction or excerpting without permission is strictly prohibited-

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’