Farewell to Looking Up! Commercial Space Starts to Calculate the Costs

04/30 2026

04/30 2026

658

658

By the end of 2025, a Chinese private rocket attempted recovery after orbit insertion but fell short at the last moment. Two years ago, this would have made headlines as a "glorious failure," but today, it is met with more sober technical analysis.

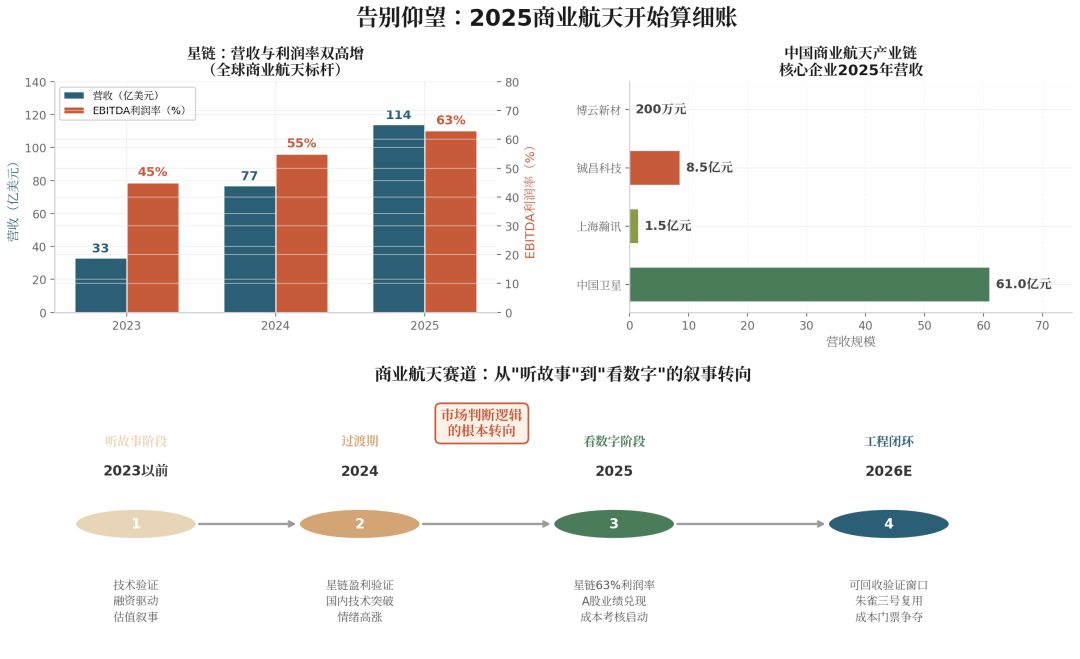

Behind this subtle shift lies a more fundamental transformation: the market's logic for judging commercial space is switching from "listening to stories" to "looking at the numbers." As overseas leaders begin delivering profit statements and domestic players enter a phase of rigorous technical validation, the narrative focus of the sector naturally shifts—profitability and cost reduction have become the core questions.

01. Starlink's Profit Statement Sets the Industry's Passing Grade

Commercial space has long been plagued by a business model dilemma: Is it a viable business or a tech race requiring continuous capital infusion?

This year, Starlink provided an answer with its financial data. In 2025, Starlink generated $11.4 billion in revenue, up nearly 50% year-on-year, with its user base doubling. But what truly captivated capital markets was its 63% EBITDA margin—a figure comparable to top-tier software companies.

What does a 63% margin signify? It means Starlink is not operating under the traditional heavy-asset model of communication operators, which rely on "building base stations, laying cables, and maintaining teams." Its marginal customer acquisition costs are extremely low—adding a user in Alaska costs virtually the same as in New York. With high-margin aviation, maritime, and government contracts accounting for an increasing share of revenue, and satellites, rockets, and terminals all in-house, cost advantages have become its widest moat.

The moment this passing grade was set, global capital markets responded immediately. Amazon's acquisition of satellite assets for over $10 billion and accelerated entries by various giants now have the clearest rationale.

In China's A-share market, the satellite communications sector similarly entered a performance delivery phase. Capital's enthusiasm for the satellite industry chain is not unfounded—according to annual reports, China Satellite generated 6.103 billion yuan in revenue in 2025, up 18.35% year-on-year, with net profit growing 27.38%. The company secured a record number of new orders, deeply participating in satellite internet constellation construction with increased deliveries of Aerospace Department Components [assuming this refers to aerospace components] aerospace components and ground system integration projects. China Satcom successfully landed the Zhongxing-26 satellite in Laos and launched network services, achieving its first overseas commercialization of high-throughput services.

Another notable clue lies upstream in the industry chain. On March 20, Shanghai Hanson disclosed that its low-Earth orbit satellite communications business had begun deliveries, generating approximately 150 million yuan in revenue. The company has comprehensively deployed across space, ground, and user segments, deeply participating in relevant constellation projects. Chengchang Technology, with over 80% market share in satellite-borne phased-array T/R chips, has achieved mass production and sustained deliveries, capable of supporting the 10-billion-yuan chip demand from future 25,000 low-Earth orbit satellite networks.

It's worth mentioning that market sentiment can sometimes "overload." For example, Boyun New Materials saw its stock price hit five consecutive daily limits, but the company later clarified that its 2025 commercial space revenue was just over 2 million yuan, accounting for less than 1% of its main business income. This phenomenon of "stock prices surging before performance" underscores the market's high expectations for the commercial space sector.

02. Reusable Rockets: China's First "Cost Barrier" to Overcome

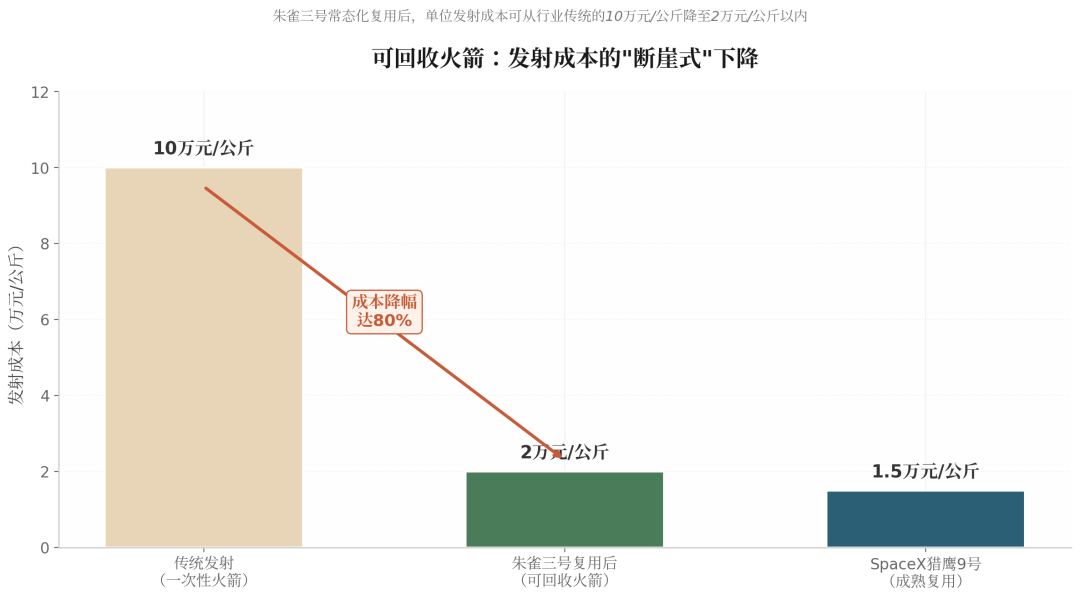

With overseas players achieving commercial closure, the toughest challenge for China's commercial space remains: how to slash launch costs to the floor.

The answer lies in reusable rockets. SpaceX's moat lies not just in satellites but in the cost restructuring enabled by Falcon 9 reuse. For China to compete, this is an unavoidable hurdle.

Currently, domestic players are at the "final push" stage. In late April 2026, China's commercial space will enter a dense [assuming it should be omitted in translation] dense validation window for reusable rockets, driven by two milestone events: First, the Long March 10B is expected to debut at the Wenchang Space Launch Site on April 28, simultaneously conducting in-orbit validation of the world's first sea-based net recovery technology. Second, the Zhuque-3 Yao-2 rocket will launch in Q2 2026, making another attempt at full-process orbital-level first-stage recovery.

The net recovery approach theoretically eliminates the weight and complexity of landing legs, representing China's differentiated original breakthrough in reusable technology. However, whether engineering advantages translate to reality depends on rigorous flight tests.

Private rocket companies are also accelerating. Landspace's Zhuque-3 completed its maiden flight in December 2025, successfully reaching orbit but failing in recovery—debris landed at the edge of the recovery zone, missing "perfection" by a hair. Landspace Chief Designer Zhang Xiaodong stated at the 2026 Space Computing Industry Conference that the Yao-2 rocket will conduct another recovery test in H1, aiming for its first reused flight in Q4 based on test results. Landspace calculates that once Zhuque-3 achieves normalized reuse, unit launch costs could drop from the industry's traditional 100,000 yuan/kg to below 20,000 yuan/kg, reducing costs by up to 80%.

At the industry chain support level, listed companies are also vying for position. PLT uses metal 3D printing technology to supply core components like engine body blanks and pintle-type gas generators for the Zhuque-2, Long March-7, and other launch vehicles. During Zhuque-3's maiden flight, PLT's reliable additive manufacturing solutions enabled its key parts to transition from engineering validation to mass production. Aerospace HuanYu has delivered spacecraft process equipment such as satellite antenna reflectors and rocket fairings, achieving import substitution for some critical tools.

We must stay sober. Aerospace has never followed a "might makes right" script. Blue Origin continues to pay for reusable rocket stability—even at the technical frontier, reusable rockets remain the industry's ultimate challenge. For China, the priority is not valuation races but first achieving a "0-to-1" engineering closure, proving rockets can return reliably and routinely.

03. Conclusion: Profitability is the Baseline, Cost is the Lifeline

The narrative focus of the 2025 commercial space sector has fundamentally shifted—markets no longer pay for stories but vote with financial data and engineering progress. Starlink's $11.4 billion revenue and 63% EBITDA margin have drawn a clear passing grade for the global industry: commercial space is not a tech race's money pit but a business that must deliver profit statements. This threshold quickly rippled through A-shares, with the satellite industry chain entering a performance delivery phase, but diverging capital sentiment reveals the market's sharpening ability to distinguish "real performance" from "pure hype."

Meanwhile, reusable rockets have become the first cost barrier Chinese players must overcome. With Zhuque-3 one step away from recovery success and Long March 10B set to validate the world's first sea-based net recovery technology, the dense [assuming it should be omitted in translation] dense launch windows represent the industry's perilous leap from "orbit-capable" to "reusable." Only by driving launch costs below 20,000 yuan/kg through normalized reuse can China secure a cost ticket for global competition. The core proposition at this stage is crystal clear: whoever first achieves a reusable engineering closure will define the rules of the next industry shakeout.

- End -

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving