Automobile Companies Must Recover and Gear Up for Future Challenges in the Year of the Horse

02/24 2026

02/24 2026

540

540

Introduction | Lead

With car ownership on the rise, roads becoming increasingly congested, and the automotive market grappling with oversupply, the era of reckless expansion for automakers is drawing to a close. The Year of the Horse is not the time for automakers to engage in a volume sprint (chōnglǐng, a term referring to the pursuit of high sales volume); rather, it is a period for recovery and preparation for future challenges.

Produced by | Heyan Yueche Studio

Written by | Li Suwan

Edited by | He Zi

Full text: 2,238 characters

Reading time: 4 minutes

On one side of my thoughts lies my hometown, and on the other, the city where I work and reside. As the "longest Spring Festival holiday in history" nears its end, migrant workers who had returned home or were traveling are now returning to the cities in droves.

During the first 20 days of the 2026 Spring Festival travel rush, it is estimated that there will be 5.08 billion cross-regional personnel movements across society, averaging 250 million per day, marking a new historical high for the same period. On February 21st alone, cross-regional personnel movements are expected to surpass 360 million. According to the Ministry of Transport, over the 40-day Spring Festival travel period, cross-regional personnel movements are projected to reach a record 9.5 billion.

△ During the Spring Festival travel rush, some road segments become so congested that navigation maps turn red and even purple.

At the peak of the Spring Festival travel rush, heavy traffic significantly lengthens the journey. Normally, the 400-plus-mile drive from Zhanjiang to Guangzhou takes about 5 hours; however, on February 21st, due to increased traffic, the journey time doubled to around 10 hours. If vehicle breakdowns or frequent traffic accidents occur along the way, the congestion becomes even more exasperating. February 22nd and 23rd marked the peak return-to-city period, with multiple road segments across the country experiencing severe congestion, some so bad that navigation maps turned purple, leaving drivers questioning their life choices.

The growing number of vehicles, intentionally or unintentionally, affects the pace and speed of returning home and returning to cities during the Spring Festival travel rush. By the end of 2025, the national car ownership reached 366 million vehicles, with new registrations exceeding 30 million for the 11th consecutive year, indicating a sustained growth trend. The national ownership of new energy vehicles reached 43.97 million, accounting for 12.01% of the total vehicle population. In 2025, 12.93 million new energy vehicles were newly registered, accounting for 49.38% of all new vehicle registrations, an increase of 1.68 million or 14.93% compared to 2024. As car ownership continues to rise, self-driving during the Spring Festival travel rush has also become increasingly popular. In this collective migration, the presence of new energy vehicles is becoming more pronounced, but it also adds uncertainties to the journey.

In recent years, range anxiety, such as waiting in line for charging stations and slow charging speeds, has occasionally troubled car owners traveling during holidays. However, continuous breakthroughs in battery technology and charging/swapping technologies, along with the improvement of infrastructure like charging/swapping stations, are striving to alleviate these concerns. Data released by NIO shows that on the fifth day of the Lunar New Year this year, the total number of battery swaps reached 175,976 in a single day, setting a new record for four consecutive days, with an average of less than 0.5 seconds per swap.

△ The continuous improvement of infrastructure, such as charging/swapping stations, is striving to alleviate the concerns of electric vehicle owners about recharging.

During this year's Spring Festival travel peak, traffic congestion and range anxiety for new energy vehicles have become recurring topics, while auxiliary driving videos frequently circulating online have become a new hotspot for self-driving tours. From the widespread adoption of L2 to the readiness of L3 and the deep reshaping by AI large models, China's autonomous driving has entered a critical phase of transitioning from laboratory exploration to large-scale implementation. Whether autonomous driving can truly become a solution for car owners to eliminate fatigue from long-distance driving and congestion remains to be seen, and it requires efforts from the automotive industry to provide an answer.

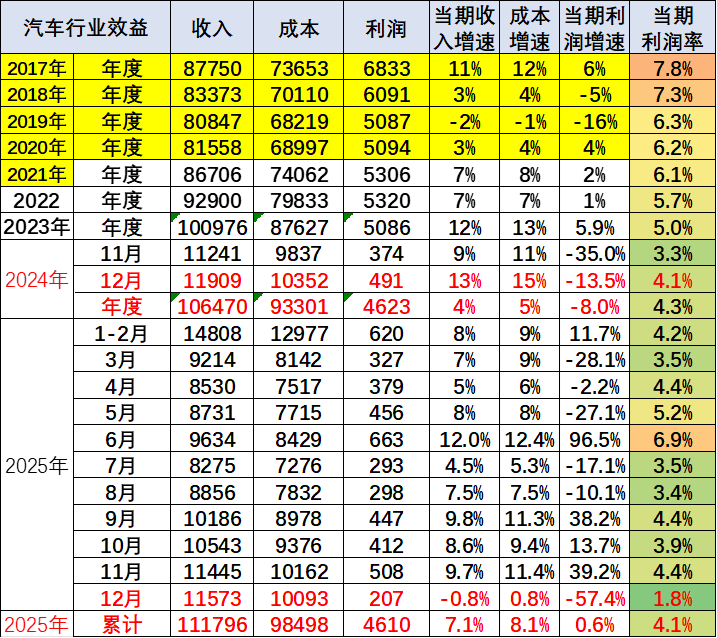

The automotive industry is undergoing profound changes, especially catalyzed by the internet and traffic, with the entire industry seizing every moment. Despite the continuous emergence of new technologies and products, the current automotive market situation is not optimistic due to issues such as overcapacity and intensified internal competition, with prominent inventory pressure. By the end of December 2025, the national passenger car inventory stood at 3.65 million units, with a destocking period of 66 days, an increase of 20 days compared to the same period in 2024; among them, the new energy vehicle inventory was 780,000 units. In December 2025, the comprehensive dealer inventory coefficient was 1.31, with joint ventures, domestic brands, and luxury brands at 1.40, 1.26, and 1.35, respectively, all approaching the warning threshold of 1.5.

The situation is also not optimistic when looking at the inventory warning index. In January 2026, the inventory warning index rose to 59.4%, remaining above the boom-bust line for consecutive periods, with the Spring Festival off-season further exacerbating inventory pressure. High inventory has led to a sharp increase in financial pressure for automakers, with dealers experiencing price inversions and expanding losses. Some companies even have inventory coefficients exceeding 2.5, falling into (xiànrù, meaning falling into) a high-risk situation.

Corresponding to the high inventory is the sluggish and weak profitability. In 2025, the sales profit margin of the automotive industry dropped to 4.1%, with December's profit margin falling to 1.8%, setting a recent low. Although domestic brands such as BYD, Geely, Chery, and AITO saw sales climb last year, their profits still need improvement. For example, BYD's profit margin in the first three quarters of last year was only 4.3%, still lagging behind global giants like Toyota in terms of profitability.

△ Data sourced from Cui Dongshu, Secretary-General of the China Passenger Car Association.

Since the beginning of 2026, the first-month sales in the Chinese automotive market have shown negative growth, with no signs of recovery yet. If the annual automotive market experiences negative sales growth and automakers continue to engage in price wars, it may further impact the declining profit margins, raising doubts about whether the automotive industry belongs to high-end or low-end manufacturing and even causing confusion and concern about its future healthy and orderly development: Aren't we constantly innovating? Where has all the profit gone?

△ The automotive industry needs to recuperate.

The decline in profits in the automotive industry is related to multiple pressures, including price wars, rising costs, and transformation investments. In an environment where car ownership is increasing, roads are becoming more congested, and the automotive market has shifted from an incremental to a stock market with oversupply, the difficulty for automakers to rapidly expand sales scale to improve profit margins is inevitably rising. Regarding the trend of the automotive market in 2026, the China Association of Automobile Manufacturers analyzes that China's total automotive sales are expected to reach 34.75 million units this year, a year-on-year increase of 1%. However, institutions like UBS are more pessimistic, believing that China's automotive market may experience negative growth this year.

This year's automotive market competition will undoubtedly be fiercer and more brutal (kùdù, meaning brutal). Instead of blindly charging ahead, automakers should focus on recuperation, which is not "inaction" but hidden "proactivity." The sluggish automotive market requires a process of adjustment and recovery. During this period, automakers can choose to optimize their product structures, reduce costs and increase efficiency, and even reduce production to assist dealers in destocking, while improving product quality and safety, as well as engaging in technological differentiation and innovation to boost profit margins, jointly promoting the healthy development of the industry. This year will mark a critical moment for breakthroughs in new technologies such as solid-state batteries and autonomous driving, but many technological breakthroughs and safety verifications still require time; haste makes waste. Automakers urgently need to calm down and focus on internal improvements during the market downturn, preparing for future challenges. Destocking in the automotive market is an unavoidable pain for the industry, and recuperation for automakers helps reduce burdens and restore vitality, just as migrant workers, after resting during the "longest Spring Festival holiday," will embark on their journeys again in a better state.

Commentary

2026 is not a year for automakers to engage in a volume sprint (chōnglǐng) but a year to survive and thrive through recuperation. However, achieving recuperation is not easy. Faced with the pain of oversupply in the automotive market, automakers often resort to even more fierce price wars rather than focusing on self-improvement. 2026 will become a new watershed, with the era of reckless expansion gradually fading. Those with superior technology who prepare for future challenges have a greater chance of success.

(This article is original to Heyan Yueche and may not be reproduced without authorization.)

-

![]()

Don’t Dismiss Huawei’s Potential in Sedans Just Because the Shangjie Hasn’t Hit It Big Yet

-

![]()

Unsold Cars in China Find Success Overseas

-

![]()

Ghosn: Only I Can Save Nissan, Shareholders Beg Me to Return

-

![]()

Expanding Automobile Consumption: It's Time to Address the High Cost of Electric Vehicle Repairs

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?

-

![]()

GPT 5.6 Reclaims the Throne, Only to Face Strict Controls Again! Has AI Truly Reached a Turning Point?

-

![]()

When the Traffic Bubble Fades, AI Giants Start to Compete on 'Real Skills'