Auto Manufacturers Regain Pricing Power | 2026 Landscape and Trends ⑧

02/25 2026

02/25 2026

477

477

Introduction

Chinese automakers can only truly seize pricing initiative by making concerted efforts across four key dimensions: independent technology R&D, supply chain integration, product premiumization, and terminal market control.

This article is selected from 2026 Landscape and Trends

“Do you know what IPD and IPMS are?”

As the entire industry sets off a wave of enthusiasm for learning Huawei's IPD and IPMS models, seasoned product and marketing professionals with over 20 years of automotive experience have expressed profound sentiments: when faced with these systems, traditional OEM operating models appear as naive as those of elementary school students. For a time, Huawei's methodology seemed to be the only standard answer for achieving breakthroughs in the era of smart electric vehicles.

However, market realities carry far more practical weight than industry consensus. In 2025, Geely emerged as the top-performing automotive company in the market, yet it was also the one farthest from Huawei's technological ecosystem among leading manufacturers. Meanwhile, NIO, which had closely followed Huawei's model over the past three years, became the most disappointing new energy vehicle brand in 2025.

This contrast between perception and reality precisely reveals the core proposition of industry transformation: More important than copying models is finding a development path that suits one's own strengths. At the heart of this transformation lies the struggle for pricing power.

Cold, hard data further underscore this dilemma: In 2025, the overall profit margin of China's automotive industry was merely 4.1%, with OEM manufacturing segment profitability falling below 3%. This stands in stark contrast to the high gross profit margins of 35% in the chip industry and 22.41% in the battery industry.

ICT companies have captured nearly 30% of the premium for smart vehicle models, while overseas chip giants have firmly controlled core hardware costs. Under this layered squeeze, most automakers find themselves trapped in a dilemma: "Pricing too high means losing the market, while pricing too low means no profit."

Where, then, lies the key to breaking through this impasse? The practices of leading automakers such as Geely, BYD, and NIO have already provided a clear answer: Only by breaking external technological constraints with independent innovations and grasping industrial dominance through ecosystem construction can pricing power be restored to OEMs.

Geely, which defied industry trends to lead in 2025, stands as the best example of adhering to independent R&D while avoiding external technological constraints. The blockbuster performance of the Zeekr 9X provides concrete proof of its independent R&D capabilities. Geely founder Li Shufu's judgment is precise: "If Chinese automakers want to gain pricing power, they cannot 'slack off' on core technologies." Adhering to this philosophy, Geely insists on independent R&D of core components such as the three-electric systems (battery, motor, and electronic control), smart cockpits, and electronic electrical architectures, improving the self-sufficiency rate of core components and reducing per-vehicle R&D costs.

As Geely's core effort in premiumization, the Zeekr 9X is equipped with its self-developed Qianli Haohan G-ASD intelligent driving system, exclusive intelligent driving chips, and Leimotor hybrid technology. Leveraging the technical advantages of full-stack independent R&D, it achieves true independent pricing, with an average transaction price exceeding 500,000 yuan and a stable gross profit margin of over 20%, breaking the industry constraint of high-end smart vehicle models relying on external technological solutions.

If Geely's breakthrough represents the successful practice of independent R&D in the high-end market, then BYD's vertical integration path has become the ultimate model for industry self-reliance. Wang Chuanfu once bluntly stated: "Core technologies cannot be bought or begged for. Only by mastering the R&D and production of core components oneself can one gain absolute initiative in pricing." BYD has constructed a fully autonomous system across the entire chain, achieving self-R&D and self-production of core components such as blade batteries, IGBT chips, and electric drive systems.

Even when raw material prices for power batteries rose by 15% in the first half of 2025, BYD was able to offset cost pressures through efficient coordination within its internal supply chain. Models such as the Han and Tang can maintain reasonable pricing in the market while keeping gross profit margins above 15%. Their overseas models are priced 15%-20% higher than domestic ones, setting a profit benchmark for Chinese brands going global and using full-industry-chain autonomy to solidify dual barriers of cost and pricing.

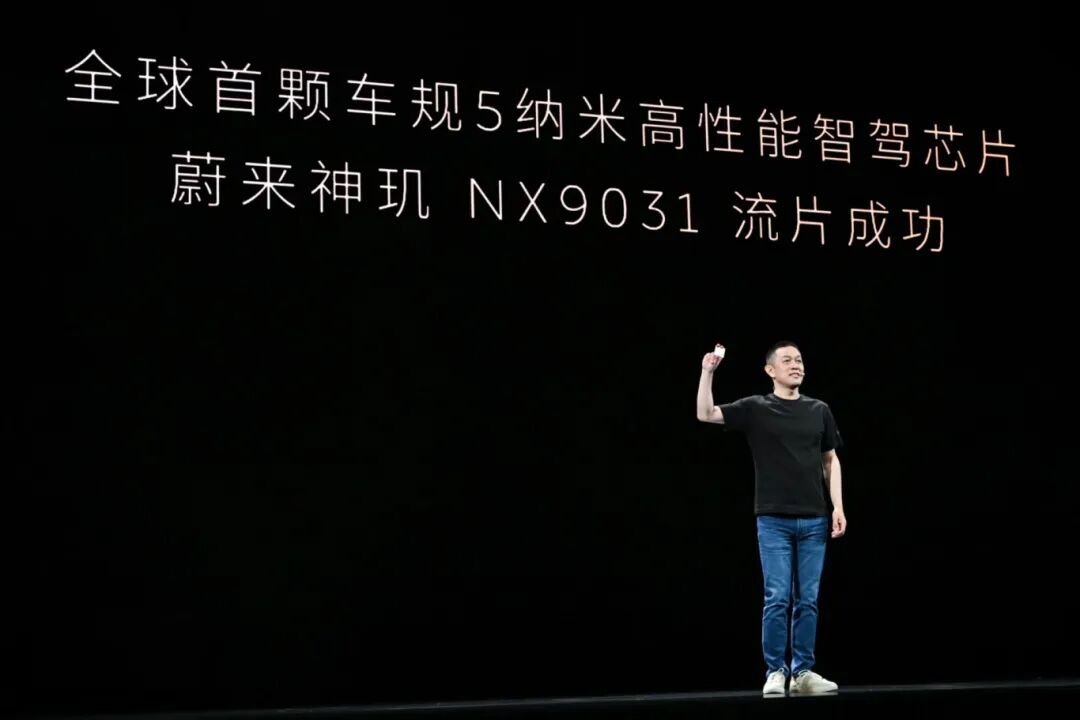

In the field of chips, which serve as the computational foundation for smart vehicles, the self-R&D breakthroughs by NIO, Xpeng, and Li Auto have marked a critical turning point for the return of pricing power. In early 2026, NIO announced that all its models would gradually switch to its self-developed Shenji NX9031 chip, directly reducing per-vehicle costs by 10,000 yuan and completely freeing itself from dependence on NVIDIA. Xpeng and Li Auto, following closely behind, introduced their respective Turing and Mach intelligent driving chips, targeting NVIDIA's Thor and even Tesla's AI5 chips.

More importantly, China's automotive self-R&D path is not merely about replacing chips but about regaining interpretation rights over intelligent driving functions, user experiences, and data value by mastering core computational power and algorithms, achieving a transformation from AI contract manufacturers to AI leaders.

Toyota, a global benchmark in supply chain integration, dared to spend $26 billion to privatize its core supplier, Toyota Industries, and integrate its internal parts supply system. In the Chinese market, Toyota further optimized its local supply chain, jointly developing core components adapted to its models with domestic suppliers. The BZ3X model, through localized integration, achieved an 18% reduction in per-vehicle battery costs, maintaining a stable gross profit margin of 8%-10% in the 140,000-150,000 yuan pricing range, becoming a classic case of supply chain integration empowering pricing.

The wave of OEM chip and battery self-R&D is not accidental but an inevitable result driven by multiple factors. The near-monopoly of ICT companies has left automakers constrained at every turn, while geopolitical factors, such as the Sino-U.S. technological decoupling since 2025, have accelerated this process. This shift from dependence to self-R&D also signals an important trend: Since the electrification and intelligent transformation in 2020, the industry pricing power that has been continuously stripped away from automakers is beginning to gradually return.

The rollback of purchase tax incentives, the looming China VII emission standards, coupled with rising prices of core raw materials such as lithium iron phosphate and soaring memory costs triggered by the AI industry boom... The battle for pricing power in 2026 will be far from smooth, and simple price hikes or price wars will not lead to a breakthrough. Only by making concerted efforts across the four dimensions of independent technology R&D, supply chain integration, product premiumization, and terminal market control can the initiative in pricing be truly grasped.

However, this thorny path also represents the next rise of China's automotive industry and determines whether we can shape the next generation of intelligent mobility civilization. Ultimately, the sparks and trajectories of this battle will etch the most profound mark on the rise of China's manufacturing industry and lead the future of human mobility even further.

——This article is selected from 2026 Landscape and Trends

Editor-in-Chief: Shi Jie Editor: He Zengrong

THE END

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?

-

![]()

Clearing Bugatti Stock Worth 7 Billion: Why is Porsche 'Cutting Ties'?

-

![]()

Don’t Dismiss Huawei’s Potential in Sedans Just Because the Shangjie Hasn’t Hit It Big Yet

-

![]()

Unsold Cars in China Find Success Overseas

-

![]()

Ghosn: Only I Can Save Nissan, Shareholders Beg Me to Return

-

![]()

Expanding Automobile Consumption: It's Time to Address the High Cost of Electric Vehicle Repairs

-

![]()

Luna Ultra Entangled in 'National Subsidy Fraud' Controversy, Insta360 Pushed to the Brink by DJI

-

![]()

People have long suffered from splash ads. Will the 'temporarily disappeared' traffic behemoth make a comeback?