Final Verdict: German Automakers' Market Share in China Slips Annually, Prompting Accelerated Reforms to Reclaim Dominance

02/27 2026

02/27 2026

653

653

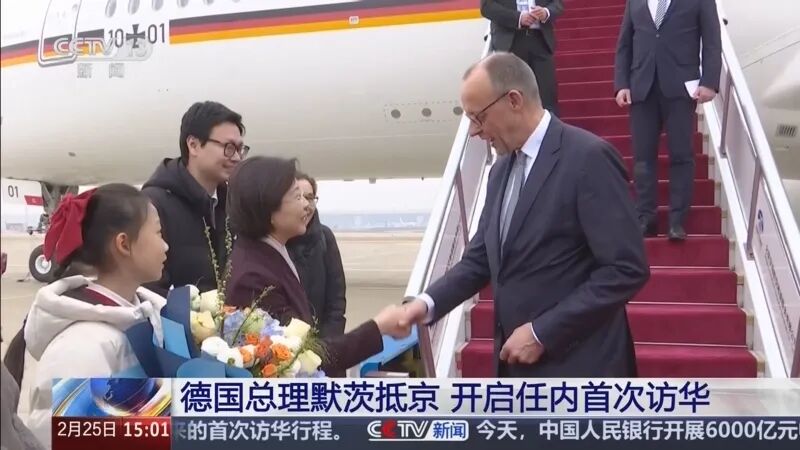

Shortly after the Spring Festival holiday, on February 25-26, German Chancellor Mertz headed a high-level economic delegation to China, where both sides engaged in comprehensive discussions in the economic and trade sectors, yielding positive results. This visit marked Mertz's inaugural trip to China as Chancellor. Accompanying the delegation were over 200 executives from nearly 30 leading companies in sectors such as automotive, chemicals, biopharmaceuticals, machinery manufacturing, and the circular economy, underscoring Germany's keen interest in deepening bilateral economic and trade ties. Among the delegates were the CEOs of Germany's three automotive giants: Volkswagen's Oliver Blume, Mercedes-Benz's Ola Källenius, and BMW's Chairman Oliver Zipse.

As part of the visiting delegation, BMW Chairman Oliver Zipse remarked in an exclusive media interview prior to the trip that this visit to China sends a strong message of unwavering commitment to dialogue, cooperation, and mutual trust. BMW has been deeply embedded in the Chinese market for over three decades, and those seeking global success cannot overlook China's innovative prowess. During the visit, BMW Group and CATL signed a memorandum of understanding in Beijing to jointly advance collaborative carbon reduction efforts in the electric vehicle battery supply chain. Chinese and German companies inked more than a dozen business agreements spanning automotive, machinery, energy, logistics, and finance.

Germany stands as the largest investor in China's automotive sector, with German automakers having established numerous joint ventures in the country. Despite a gradual annual decline in market share for German-branded cars in China in recent years, China remains the largest market for many German automotive brands.

Volkswagen Group, BMW Group, and Mercedes-Benz maintain an optimistic outlook on the Chinese automotive market's future, actively adjusting and transforming to expedite and deepen their "In China, For China" strategy. The joint visit by Germany's three automotive titans underscores their high regard for the Chinese market.

German Brands Once Reigned Supreme in China's Passenger Car Market

Since entering the Chinese market in the 1980s, German automakers have long dominated China's passenger car market, thanks to their superior engineering, rigorous manufacturing processes, and a brand image synonymous with "luxury, safety, and reliability." Brands like Volkswagen, Audi, BMW, and Mercedes-Benz not only grace China's roads but have also become emblematic of "quality" and "status" for a generation of Chinese consumers.

German brands, led by Volkswagen, were pioneers in deep joint venture cooperation with the Chinese automotive industry. The establishment of Shanghai Volkswagen and FAW-Volkswagen not only introduced capital, technology, and advanced products but also fostered a complete local supply chain and sales service system, laying a solid market foundation.

German brands accurately captured the core demands of Chinese consumers during the automotive consumption upgrade—seeking texture, safety, and brand value. From the dominance of the Passat and Audi A6 in the official vehicle market to the BMW 3 Series and Mercedes-Benz C-Class becoming aspirational vehicles for the middle class, German brands successfully positioned themselves as paragons of technology and luxury.

The global reputation of "Made in Germany" resonates deeply with Chinese consumers' traditional car-buying values of durability, reliability, and value retention. Technical labels like Volkswagen's TSI+DSG "golden powertrain combination" once set industry benchmarks.

In China's luxury car market, Audi, Mercedes-Benz, and BMW have long held sway. From 2016 to 2017, German passenger cars reached their peak market share in China at 25%, while in the luxury car segment, their share once surpassed 90%.

German Passenger Car Brands' Market Share Wanes in Recent Years

In recent years, with the explosive growth of China's new energy vehicle sector and the rise of domestic automakers, the market share of joint venture brands has continued to decline, and German passenger cars are no exception.

Statistics reveal that in 2020, German brands held a 23.9% share of China's passenger car market, which dipped to 20.6% in 2021 and further to 19.5% in 2022, falling below 20% for the first time. In 2023, it declined to 17.8%, and by 2025, it had dropped to 15.17%.

Compared to Japanese, Korean, and American brands, German brands still command the highest market share, but it has plummeted nearly 10 percentage points from its peak.

Analysts attribute the decline in market share for German passenger car brands to a confluence of drastic external changes and sluggish internal responses.

Firstly, the impact from Chinese domestic brands is a pivotal external factor. Chinese domestic brands, exemplified by BYD, Geely, Changan, NIO, and XPeng, have achieved "overtaking on a new track" in the new energy vehicle sector. These domestic brands better comprehend Chinese consumers' demands for smart cockpits, spacious interiors, and comfortable configurations, offering experiences that transcend traditional automotive norms. Zeng Qinghong, former Chairman of GAC Group, once remarked that the primary reason joint venture brands lag behind is their failure to advance in new energy vehicles. Currently, nearly all joint venture automakers, including German brands, have low penetration rates in new energy vehicles.

In terms of automotive technology, Chinese domestic automakers have invested heavily in electrification platforms, battery technology, and intelligent driving, with much faster iteration cycles than traditional foreign giants. Leveraging a complete local supply chain and economies of scale, they often offer significantly lower prices than comparable German models while maintaining equal or superior configurations.

In the era of smart electric vehicles, the traditional advantages of the "three major components" (engine, transmission, chassis) have been partially supplanted by the "three electric systems" (battery, motor, electric control) and intelligent software. When Chinese domestic brands offer leading experiences in these areas, the brand premium capability of German cars faces challenges.

Simultaneously, global supply chain fluctuations and Europe's energy crisis have also impacted German automakers' cost control and production stability. When responding to China's rapidly evolving supply chain demands, German automakers, with their longer decision-making chains, appear less agile.

Moreover, shifts in Chinese consumer attitudes pose challenges to German cars. The new generation of mainstream car buyers (Generation Z and young families) exhibit more pragmatic, open, and experience-focused consumption attitudes. Their admiration for foreign brands has significantly waned, and they place greater emphasis on actual smart experiences, service ecosystems, and emotional resonance in products. The "brand halo" effect that German cars once relied on is fading.

German Automakers Are Fully Addressing Shortcomings to Reclaim Glory

Facing the challenging situation in the Chinese market, German automakers recognize the crisis and are actively adjusting their strategies to make a mark in the world's largest automotive and new energy vehicle market and reclaim their former dominance.

Volkswagen, Mercedes-Benz, and BMW are accelerating and deepening their "In China, For China" strategy, elevating their R&D centers in China to a global core position, conducting in-depth development of electrification and intelligent platforms tailored specifically to Chinese market demands, and establishing more independent and agile decision-making mechanisms in China.

To address shortcomings in software, smart cockpits, and advanced intelligent driving, German automakers are engaging in more open and deeper cooperation with outstanding Chinese tech companies (such as Huawei, Horizon Robotics, and CATL) to rapidly enhance product competitiveness.

While maintaining fundamental quality and safety, German automakers are reevaluating the relationship between product configurations and pricing, offering more sincere products, and exploring new energy sub-brands or new product lines specifically for the Chinese market to compete with greater flexibility.

While the situation is undoubtedly challenging, German brands' deep manufacturing heritage, global operational experience, and decades of accumulation in China remain invaluable assets. German automotive brands boast a vast installed base and a strong reputation in China. By accelerating reform efforts and truly transitioning from "Made in Germany" to "Intelligently Made in China for China," they have every chance of continuing their glory in the new era. (End)

-

![]()

Can the Brand-New Hongqi H7 Forge Its Own Identity in the Hybrid Vehicle Market?

-

![]()

Challenges in Redeeming Certificates for New Cars: Mercedes-Benz Dealership Group Grapples with Operational Hurdles Once Again

-

![]()

Porsche Returns to Volkswagen, Ending the 'Electric Ferrari' Story

-

![]()

"Chinese Version of Mythos": Can It Rise to the Challenge and Keep Pace?

-

![]()

Equity Changes Hands Three Times in Seven Years: JMCG Leans on Contract Manufacturing for Survival Amid Brand Deficits

-

![]()

Automotive Market News: Nine Departments Jointly Roll Out Aftermarket Consumption Initiatives

-

How Electronic Fabric Became the Critical Chokepoint for AI’s Trillion-Dollar Computing Infrastructure

-

![]()

Depreciation Rate on Par with Mobile Phones: Just 40% Value Retention After Three Years—Why Do Battery Electric Vehicles Lose Their Worth?